Renewable Aviation Fuel Market

Renewable Aviation Fuel Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701177 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

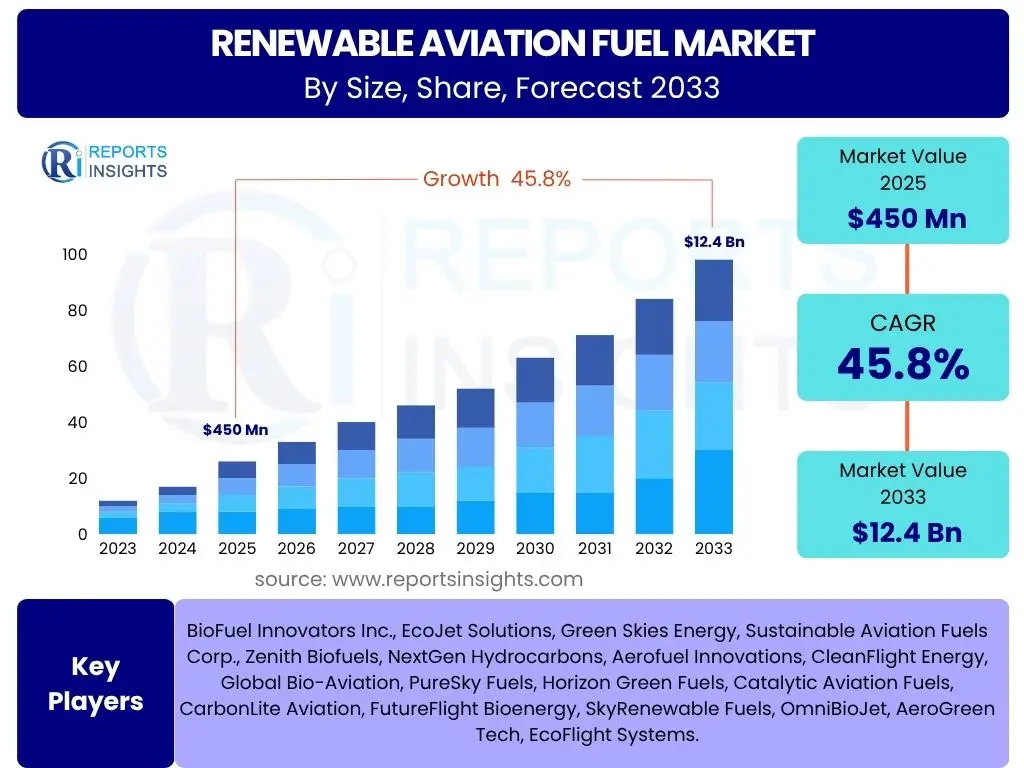

Renewable Aviation Fuel Market Size

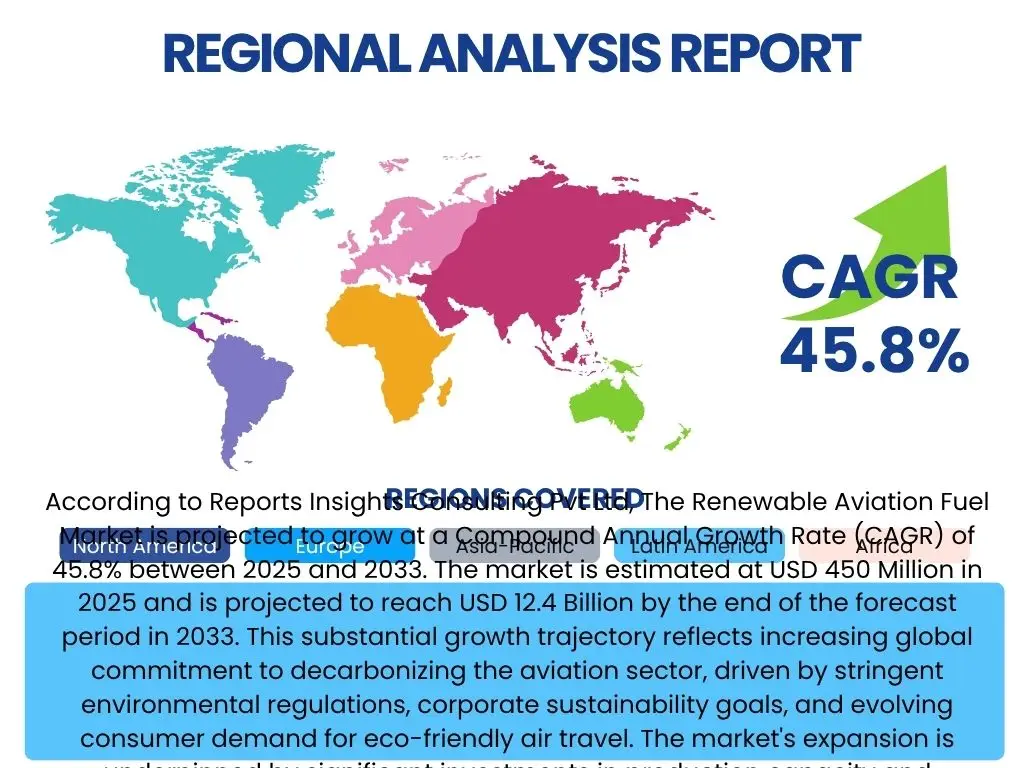

According to Reports Insights Consulting Pvt Ltd, The Renewable Aviation Fuel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 45.8% between 2025 and 2033. The market is estimated at USD 450 Million in 2025 and is projected to reach USD 12.4 Billion by the end of the forecast period in 2033. This substantial growth trajectory reflects increasing global commitment to decarbonizing the aviation sector, driven by stringent environmental regulations, corporate sustainability goals, and evolving consumer demand for eco-friendly air travel. The market's expansion is underpinned by significant investments in production capacity and technological advancements aimed at improving feedstock diversification and conversion efficiencies.

Key Renewable Aviation Fuel Market Trends & Insights

Common user questions often revolve around the evolving landscape of Renewable Aviation Fuel (RAF), focusing on the drivers behind its rapid adoption, technological breakthroughs, and the shifting dynamics of global supply chains. Users are particularly interested in understanding how policy frameworks influence market growth, the emergence of new feedstock sources beyond conventional options, and the strategies employed by airlines and fuel producers to meet ambitious decarbonization targets. Furthermore, there is considerable curiosity regarding the long-term viability and scalability of RAF production methods and their economic competitiveness against traditional jet fuel.

The market is witnessing a profound shift towards sustainable practices, with a growing emphasis on circular economy principles in RAF production. Innovations in enzymatic and catalytic conversion technologies are enhancing efficiency and yield from diverse biomass sources, including agricultural waste and municipal solid waste. Concurrently, the increasing collaboration between aviation industry stakeholders, governments, and technology providers is accelerating research, development, and deployment of next-generation RAF solutions, paving the way for wider commercialization and infrastructure development.

- Escalating Corporate Sustainability Mandates: Airlines and large corporations are setting aggressive net-zero targets, driving demand for RAF.

- Diversification of Feedstock Sources: Expansion beyond used cooking oil and animal fats to include municipal solid waste, agricultural residues, and algae.

- Advancements in Production Technologies: Development of novel pathways like Alcohol-to-Jet (ATJ) and Power-to-Liquid (PtL) alongside traditional HEFA.

- Strong Government Policy Support: Implementation of blending mandates, tax incentives, and research grants globally.

- Increasing Investment in Production Capacity: Significant capital infusion into new RAF biorefineries and expansion of existing facilities.

- Focus on Supply Chain Optimization: Efforts to streamline feedstock collection, transportation, and processing for greater efficiency and reduced costs.

- Emergence of Carbon Capture and Utilization (CCU) for PtL: Integration of CO2 capture to enhance the sustainability profile of synthetic fuels.

AI Impact Analysis on Renewable Aviation Fuel

Users frequently inquire about the transformative potential of Artificial Intelligence (AI) in optimizing the Renewable Aviation Fuel (RAF) value chain, from feedstock procurement to fuel distribution. Concerns often include how AI can enhance efficiency, reduce costs, and accelerate innovation in this complex sector. There is a keen interest in understanding AI's role in predictive maintenance for biorefineries, optimizing supply chain logistics for biomass, and even aiding in the discovery of novel enzyme or catalyst formulations for more efficient fuel conversion processes. Expectations are high for AI to provide a competitive edge and address inherent challenges in scaling RAF production.

AI's analytical capabilities are proving instrumental in refining operational efficiencies across the RAF lifecycle. Machine learning algorithms can analyze vast datasets from biorefinery operations to predict equipment failures, optimize reaction conditions for maximum yield, and manage complex feedstock inventories more effectively. Furthermore, AI-driven simulations are accelerating research and development by rapidly testing new material compositions for catalysts or exploring different process parameters, significantly reducing the time and cost associated with laboratory experimentation. This integration of AI is not merely an incremental improvement but a fundamental shift towards more intelligent and autonomous RAF production systems.

- Optimized Feedstock Sourcing and Logistics: AI algorithms can predict feedstock availability, manage inventory, and optimize transportation routes, reducing costs and emissions.

- Enhanced Biorefinery Operations: Predictive maintenance and process optimization using AI reduce downtime and improve conversion efficiency.

- Accelerated R&D for Novel Pathways: Machine learning facilitates the discovery of new catalysts and enzymes, speeding up the development of more efficient RAF production methods.

- Improved Carbon Footprint Tracking: AI provides precise real-time monitoring and reporting of emissions across the value chain, supporting sustainability claims.

- Predictive Market Demand Analysis: AI models can forecast future RAF demand, assisting producers in capacity planning and investment decisions.

- Automated Quality Control: AI-powered sensors and analytics ensure consistent fuel quality, meeting stringent aviation standards.

- Smart Grid Integration for PtL: AI optimizes energy consumption for Power-to-Liquid processes by integrating with renewable energy sources.

Key Takeaways Renewable Aviation Fuel Market Size & Forecast

Analysis of common user questions concerning the Renewable Aviation Fuel (RAF) market size and forecast reveals a strong emphasis on understanding the drivers of its projected exponential growth, the potential for market disruptions, and the long-term investment landscape. Users are keen to grasp the underlying factors contributing to the remarkable Compound Annual Growth Rate (CAGR), seeking clarity on whether this growth is sustainable and what macroeconomic or regulatory shifts could influence the trajectory. There is also significant interest in identifying the primary segments and regions that will contribute most significantly to this growth, along with potential bottlenecks that might impede progress.

The market is poised for transformative expansion, driven by an unequivocal global commitment to aviation decarbonization and robust policy support. The impressive CAGR forecast reflects not just a nascent industry but one that is rapidly maturing, characterized by increasing production capacities, technological breakthroughs making diverse feedstocks viable, and an expanding global regulatory framework. While challenges related to cost competitiveness and feedstock availability persist, the sheer scale of investment and the urgency of climate goals suggest a sustained growth phase, making RAF a pivotal component of future energy transition strategies for the aviation sector.

- Exponential Growth Trajectory: The RAF market is set for unprecedented expansion, driven by aggressive decarbonization targets and policy mandates.

- Critical Role in Aviation Decarbonization: RAF is identified as the most viable near-term solution for significantly reducing aviation's carbon footprint.

- Policy-Driven Demand: Government blending mandates and incentives are foundational to stimulating market growth and production ramp-up.

- Investment Hotbed: The sector is attracting substantial capital from governments, energy companies, and aviation industry players.

- Technological Advancements are Key: Ongoing R&D in production pathways and feedstock diversification will unlock further market potential.

- Supply Chain Scalability Challenges: While growth is rapid, scaling up feedstock supply and production infrastructure remains a key hurdle.

- Regional Leadership: Europe and North America are expected to lead in adoption and production capacity due to early policy implementation.

Renewable Aviation Fuel Market Drivers Analysis

The Renewable Aviation Fuel (RAF) market is profoundly influenced by a confluence of powerful drivers, primarily stemming from the urgent global imperative to mitigate climate change and the specific challenges faced by the aviation sector in decarbonizing. International bodies and national governments are increasingly imposing stricter emissions regulations on airlines, compelling them to integrate sustainable solutions. This regulatory push is complemented by a growing demand from corporate and leisure travelers for more environmentally responsible travel options, exerting consumer pressure on airlines to adopt RAF.

Furthermore, significant technological advancements are making RAF production more efficient and economically viable, broadening the range of usable feedstocks beyond traditional sources. The aviation industry itself, recognizing its unique position as a significant emitter with limited alternative propulsion technologies for long-haul flights, is actively investing in and advocating for RAF. This internal commitment, coupled with cross-sector collaborations and government incentives, creates a robust ecosystem supporting the market's rapid expansion. The drive for energy security and diversification away from fossil fuels also plays a role, positioning RAF as a strategic national asset.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stricter Environmental Regulations & Decarbonization Goals | +5.0% | Global, particularly EU, UK, US | Short to Long-term (2025-2033) |

| Increasing Airline & Corporate Sustainability Commitments | +4.5% | Global, major airlines & corporations | Mid to Long-term (2026-2033) |

| Government Incentives & Blending Mandates | +3.8% | EU, US, Japan, Canada | Short to Mid-term (2025-2029) |

| Technological Advancements in Production Pathways | +3.2% | Global, R&D hubs | Mid to Long-term (2027-2033) |

| Growing Consumer Awareness & Demand for Sustainable Travel | +2.5% | North America, Europe | Mid to Long-term (2028-2033) |

Renewable Aviation Fuel Market Restraints Analysis

Despite the strong growth potential, the Renewable Aviation Fuel (RAF) market faces significant restraints that could temper its expansion. A primary hurdle is the high production cost of RAF compared to conventional jet fuel. This cost disparity makes it challenging for airlines to adopt RAF widely without substantial financial incentives or regulatory mandates, as it directly impacts their operational expenses and profitability. The nascent nature of the industry means that economies of scale have not yet been fully achieved, contributing to higher unit costs for production and distribution.

Another critical restraint is the limited availability and sustainability concerns surrounding certain preferred feedstocks. While efforts are underway to diversify feedstock sources, the current reliance on specific biomass types, such as used cooking oil (UCO) and animal fats, creates supply bottlenecks and raises ethical questions about land use, food security, and deforestation if not sourced responsibly. Furthermore, the existing infrastructure for producing, blending, and distributing RAF is still developing, particularly outside major aviation hubs, which poses logistical challenges and adds to the overall cost of integration for airlines globally. Overcoming these restraints requires sustained investment, policy intervention, and continuous innovation.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Production Cost Compared to Conventional Jet Fuel | -4.0% | Global | Short to Mid-term (2025-2029) |

| Limited Availability of Sustainable Feedstock at Scale | -3.5% | Global, particularly emerging markets | Short to Mid-term (2025-2030) |

| Infrastructure Limitations for Production & Distribution | -2.8% | Developing regions, smaller airports | Mid-term (2026-2031) |

| Complex Certification & Regulatory Approval Processes | -2.0% | Global, regulatory bodies | Short-term (2025-2027) |

| Competition for Feedstock with Other Biofuel Industries | -1.5% | Global | Mid to Long-term (2027-2033) |

Renewable Aviation Fuel Market Opportunities Analysis

The Renewable Aviation Fuel (RAF) market is rich with opportunities driven by a global push towards decarbonization and technological innovation. A significant opportunity lies in the expanding array of sustainable feedstock sources beyond traditional options. The development of advanced conversion technologies now allows for the utilization of municipal solid waste, agricultural residues, forestry waste, and even direct air capture CO2, transforming these abundant and often low-cost materials into valuable aviation fuel. This diversification not only addresses supply limitations but also enhances the overall sustainability profile of RAF, opening new avenues for circular economy initiatives.

Moreover, the increasing demand for sustainable travel presents a compelling business opportunity for airlines and fuel producers alike. Airlines that proactively integrate RAF into their operations can enhance their brand image, attract environmentally conscious customers, and gain a competitive edge in a market increasingly focused on sustainability. The development of international carbon offsetting schemes and regulatory frameworks, such as the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA), further incentivizes RAF adoption by providing a clear compliance pathway and potential financial benefits. Strategic partnerships across the value chain, from feedstock suppliers to airlines, are also creating integrated solutions that can accelerate market scale-up and cost reduction, unlocking significant growth potential.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Diversification of Feedstock to Non-Food Sources (e.g., waste, algae) | +4.2% | Global, particularly Asia Pacific, North America | Mid to Long-term (2027-2033) |

| Development of Power-to-Liquid (PtL) for Synthetic RAF Production | +3.8% | Europe, North America | Long-term (2029-2033) |

| Emergence of Carbon Markets & Carbon Credits for RAF | +3.5% | Global, regulated markets | Short to Mid-term (2025-2030) |

| Strategic Partnerships & Joint Ventures across Value Chain | +3.0% | Global | Short to Mid-term (2025-2028) |

| Expansion into New Regional Markets & Developing Economies | +2.5% | Asia Pacific, Latin America, MEA | Mid to Long-term (2028-2033) |

Renewable Aviation Fuel Market Challenges Impact Analysis

The Renewable Aviation Fuel (RAF) market, while promising, faces a series of significant challenges that could impede its rapid growth and widespread adoption. One of the most pressing challenges is the substantial capital investment required to build new RAF production facilities and retrofit existing ones. This high upfront cost, coupled with the long lead times for construction and regulatory approvals, creates a barrier to entry and expansion for many potential producers. Furthermore, the complexity of developing efficient and scalable supply chains for diverse and often geographically dispersed feedstocks presents logistical and economic hurdles that need to be systematically addressed.

Another critical challenge revolves around achieving cost competitiveness with conventional jet fuel without relying heavily on government subsidies. As the industry scales, the need for cost reduction becomes paramount to ensure widespread commercial viability. This involves continuous innovation in production technologies, optimization of feedstock sourcing, and the realization of economies of scale. Moreover, ensuring the long-term sustainability and traceability of feedstocks remains a significant concern, requiring robust certification mechanisms and strict adherence to environmental and social standards to avoid unintended negative impacts such as deforestation or land-use change. Navigating these multifaceted challenges will be crucial for the sustained growth and success of the Renewable Aviation Fuel market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure for New Production Facilities | -3.5% | Global | Short to Mid-term (2025-2029) |

| Securing Consistent & Sustainable Feedstock Supply Chains | -3.0% | Global | Mid-term (2026-2031) |

| Achieving Cost Parity with Fossil Jet Fuel | -2.8% | Global | Long-term (2029-2033) |

| Technological Scalability & Commercialization Risks | -2.0% | Global, R&D hubs | Mid-term (2027-2031) |

| Public Perception & Acceptance of Different Feedstock Types | -1.5% | Europe, North America | Short to Mid-term (2025-2028) |

Renewable Aviation Fuel Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Renewable Aviation Fuel (RAF) market, covering its current status, historical performance, and future growth projections from 2025 to 2033. The report meticulously examines market size, key trends, drivers, restraints, opportunities, and challenges influencing the industry's trajectory. It offers a detailed segmentation analysis based on various parameters such as feedstock type, production process, blending capacity, and end-use applications. Furthermore, the report provides a thorough regional analysis, highlighting key country-level developments and regulatory landscapes. It also includes profiles of leading market players, offering insights into their strategic initiatives and competitive positioning to provide a holistic view of the RAF ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 450 Million |

| Market Forecast in 2033 | USD 12.4 Billion |

| Growth Rate | 45.8% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | BioFuel Innovators Inc., EcoJet Solutions, Green Skies Energy, Sustainable Aviation Fuels Corp., Zenith Biofuels, NextGen Hydrocarbons, Aerofuel Innovations, CleanFlight Energy, Global Bio-Aviation, PureSky Fuels, Horizon Green Fuels, Catalytic Aviation Fuels, CarbonLite Aviation, FutureFlight Bioenergy, SkyRenewable Fuels, OmniBioJet, AeroGreen Tech, EcoFlight Systems. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Renewable Aviation Fuel (RAF) market is segmented to provide a granular understanding of its diverse components and growth drivers. These segments highlight the varied approaches to RAF production, the different types of raw materials utilized, and the specific applications within the aviation sector. Such detailed segmentation allows for a precise analysis of market dynamics, identifies high-growth areas, and informs strategic decision-making for stakeholders across the value chain, from feedstock suppliers to airline operators.

Each segment is influenced by distinct technological advancements, regulatory frameworks, and economic factors. For instance, the feedstock segment reflects the industry's continuous effort to move towards more sustainable and abundant non-food sources, while the production process segment showcases the evolution of conversion technologies. Understanding these interdependencies and the relative market share of each segment is crucial for forecasting future trends and identifying investment opportunities in a rapidly evolving market aiming for large-scale decarbonization.

- By Feedstock: This segment analyzes the various raw materials used for RAF production, differentiating between biomass-based sources (e.g., used cooking oil, animal fats, municipal solid waste, agricultural residues, algae) and non-biomass pathways such as Power-to-Liquid (PtL) utilizing renewable electricity and captured CO2, and Alcohol-to-Jet (ATJ).

- By Production Process: This segment examines the different technologies employed to convert feedstocks into RAF. Key processes include Hydroprocessed Esters and Fatty Acids (HEFA), Fischer-Tropsch (FT), Alcohol-to-Jet (ATJ), Direct Sugars to Hydrocarbons (DSHC), and emerging methods like synthetic biology and advanced catalytic conversion.

- By Blending Capacity: This segmentation categorizes RAF based on the maximum percentage it can be blended with conventional jet fuel. Categories typically include blends up to 20%, 20% to 50%, and pure (100%) Renewable Aviation Fuel, which is crucial for future aviation decarbonization goals.

- By End-Use: This segment distinguishes the applications of RAF across different aviation sectors, primarily commercial aviation, military aviation, and business and general aviation, each with unique operational demands and regulatory landscapes.

Regional Highlights

- North America: Expected to be a dominant market driven by the U.S. government's SAF Grand Challenge aiming for significant production targets, coupled with tax credits and a strong domestic feedstock base. Canada is also progressing with its clean fuel standards.

- Europe: A global leader in RAF adoption and policy, propelled by the "Fit for 55" package's ReFuelEU Aviation initiative, mandating increasing blending levels. Countries like France, Germany, and the Netherlands are at the forefront of policy implementation and investment in production facilities.

- Asia Pacific (APAC): Rapidly emerging as a key growth region due to increasing air travel demand, growing environmental awareness, and government initiatives in countries like Japan, South Korea, China, and Australia focusing on sustainable aviation. Significant potential for diverse feedstock availability.

- Latin America: Brazil stands out with its established biofuel industry providing a strong foundation for RAF production, leveraging abundant biomass resources. Other countries are exploring policy frameworks to encourage RAF adoption.

- Middle East and Africa (MEA): Growing interest in RAF driven by sustainability goals and potential for renewable energy development. Countries like UAE and Saudi Arabia are investing in green hydrogen and PtL projects, positioning themselves as future RAF hubs.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Renewable Aviation Fuel Market.- BioFuel Innovators Inc.

- EcoJet Solutions

- Green Skies Energy

- Sustainable Aviation Fuels Corp.

- Zenith Biofuels

- NextGen Hydrocarbons

- Aerofuel Innovations

- CleanFlight Energy

- Global Bio-Aviation

- PureSky Fuels

- Horizon Green Fuels

- Catalytic Aviation Fuels

- CarbonLite Aviation

- FutureFlight Bioenergy

- SkyRenewable Fuels

- OmniBioJet

- AeroGreen Tech

- EcoFlight Systems

- Renewable Air Solutions

- FlightPath Green

Frequently Asked Questions

Analyze common user questions about the Renewable Aviation Fuel market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Renewable Aviation Fuel (RAF)?

Renewable Aviation Fuel (RAF), also known as Sustainable Aviation Fuel (SAF), is a jet fuel alternative made from renewable resources, designed to significantly reduce carbon emissions from air travel compared to conventional jet fuel. It can be produced from various feedstocks, including biomass, agricultural waste, and even captured carbon dioxide, and is chemically similar enough to traditional jet fuel to be used in existing aircraft engines without modifications.

Why is Renewable Aviation Fuel (RAF) important for the aviation industry?

RAF is crucial for the aviation industry because it offers a direct and near-term solution to decarbonize air travel, which is a major contributor to global greenhouse gas emissions and challenging to electrify. It enables airlines to meet increasingly stringent environmental regulations, achieve their net-zero targets, and satisfy growing consumer and corporate demand for sustainable travel, all while utilizing existing infrastructure.

What are the primary challenges facing the widespread adoption of RAF?

The primary challenges for RAF adoption include its significantly higher production cost compared to conventional jet fuel, the limited availability of sustainable feedstocks at the necessary scale, and the substantial capital investment required for new production facilities. Additionally, the development of robust supply chain infrastructure and consistent regulatory frameworks across different regions remain key hurdles.

How do governments and policies support the growth of the RAF market?

Governments worldwide support the RAF market through various policy mechanisms, including blending mandates that require airlines to use a certain percentage of RAF, tax incentives and subsidies for producers and consumers, and grants for research and development into new production technologies. These policies aim to lower the cost of RAF, stimulate production, and create a stable demand signal for the industry.

What is the future outlook for the Renewable Aviation Fuel market?

The future outlook for the Renewable Aviation Fuel market is exceptionally positive, characterized by rapid growth driven by escalating global climate commitments and continuous technological advancements. As production scales up, costs are expected to decrease, and a wider array of feedstocks will become viable. RAF is poised to become an indispensable component of the aviation industry's long-term sustainability strategy.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted