Power Grid System Component Market

Power Grid System Component Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704305 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Power Grid System Component Market Size

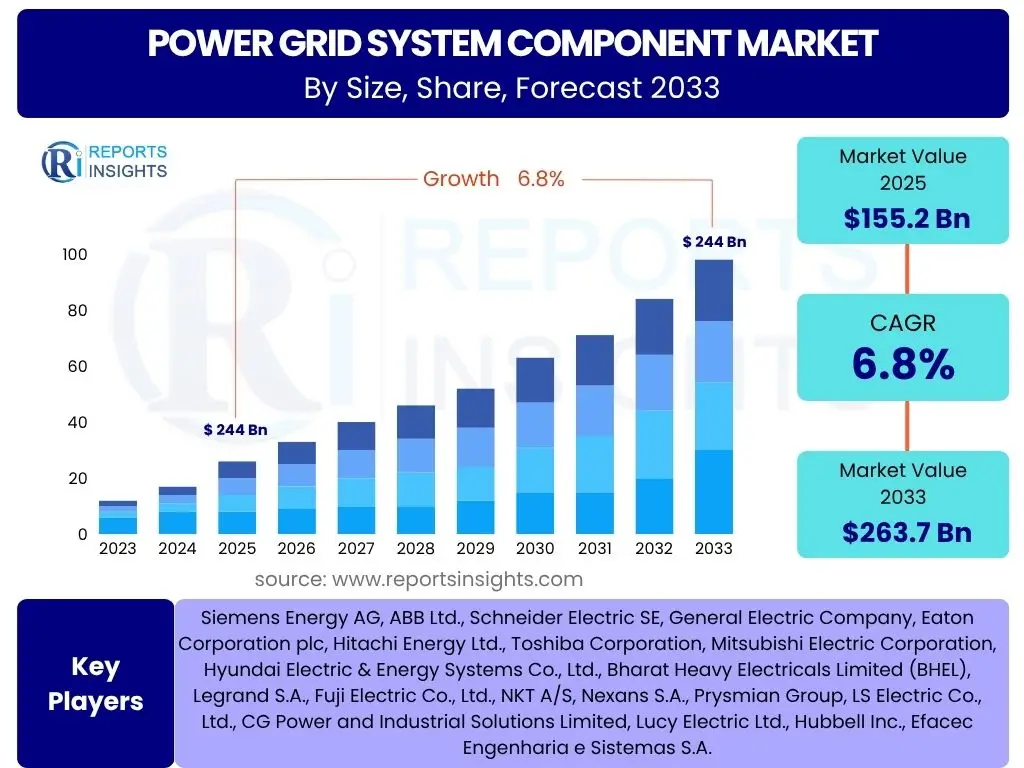

According to Reports Insights Consulting Pvt Ltd, The Power Grid System Component Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 155.2 Billion in 2025 and is projected to reach USD 263.7 Billion by the end of the forecast period in 2033.

Key Power Grid System Component Market Trends & Insights

The power grid system component market is undergoing significant transformation, driven by an array of macro and micro-economic factors. Common user inquiries often revolve around the prevailing forces shaping grid infrastructure, highlighting a strong interest in the transition towards sustainable energy and the digitalization of grid operations. There is a palpable curiosity regarding how the integration of renewable energy sources, such as solar and wind, is influencing the design, demand, and deployment of traditional and advanced grid components. Furthermore, stakeholders are keenly observing the evolution of smart grid technologies, which promise enhanced efficiency, reliability, and security of power supply.

Another prominent area of interest concerns the modernization of aging grid infrastructure in developed economies and the rapid expansion of grid networks in developing regions. Users frequently seek information on the technological advancements in components like smart meters, advanced transformers, and digital switchgear, which are foundational to future-proof grids. The increasing focus on energy efficiency, coupled with government initiatives and regulations promoting grid resilience against natural disasters and cyber threats, also represents a critical trend shaping investment and innovation within the sector. These trends collectively underscore a global pivot towards more intelligent, resilient, and sustainable energy delivery systems.

- Accelerated integration of renewable energy sources into national grids.

- Significant investments in smart grid technologies and digitalization initiatives.

- Modernization and replacement of aging power infrastructure across developed nations.

- Growing adoption of decentralized energy generation and microgrid solutions.

- Increasing demand for efficient and resilient transmission and distribution components.

- Electrification of transportation and industrial sectors driving power demand.

- Emphasis on cybersecurity measures for critical grid infrastructure.

AI Impact Analysis on Power Grid System Component

The profound impact of Artificial Intelligence (AI) on the power grid system component market is a subject of escalating interest among users and industry stakeholders. Common user questions frequently address how AI technologies are being leveraged to enhance grid performance, reliability, and operational efficiency. Predictive maintenance, a key application of AI, is revolutionizing how utilities manage critical assets like transformers, circuit breakers, and cables. By analyzing vast datasets from sensors and operational history, AI algorithms can forecast equipment failures, optimize maintenance schedules, and significantly extend the lifespan of grid components, thereby reducing downtime and operational costs.

Furthermore, AI plays a pivotal role in optimizing energy flow and demand-side management within complex power grids. Intelligent algorithms can balance electricity supply and demand in real-time, integrating fluctuating renewable energy sources more effectively and minimizing transmission losses. Users are also concerned with AI's contribution to grid security, particularly in detecting and mitigating cyber threats that target critical infrastructure components. AI-powered anomaly detection systems can identify unusual patterns indicative of cyberattacks or operational anomalies, enabling rapid response and enhanced grid resilience. This pervasive integration of AI is not only improving the functionality of existing components but also driving the development of new, AI-ready grid technologies capable of autonomous operation and intelligent decision-making, setting a new paradigm for grid management.

- Enabling predictive maintenance for critical grid components, reducing downtime.

- Optimizing real-time energy dispatch and load balancing for enhanced efficiency.

- Facilitating seamless integration of intermittent renewable energy sources.

- Enhancing cybersecurity through anomaly detection and threat intelligence.

- Improving grid resilience and responsiveness to unforeseen events.

- Automating grid operations and fault detection for faster recovery.

- Driving demand for AI-compatible sensors and smart grid components.

Key Takeaways Power Grid System Component Market Size & Forecast

Analysis of common user questions regarding the Power Grid System Component Market size and forecast reveals a keen interest in understanding the core growth drivers, the transformative impact of technological advancements, and the long-term sustainability outlook. Users are primarily concerned with the overarching factors that will sustain the projected growth, seeking reassurance about the stability and expansion of investments in power infrastructure. The transition to clean energy sources and the global push for decarbonization are consistently highlighted as primary catalysts for market expansion, driving demand for new and upgraded grid components capable of handling distributed generation and bidirectional power flows.

Moreover, the forecast demonstrates a robust upward trajectory, indicating sustained confidence in the sector's growth potential through 2033. This growth is underpinned by continuous innovation in smart grid technologies, which are making grids more intelligent, efficient, and resilient. The market's significant valuation by 2033 underscores the critical role power grid components play in national infrastructure development and energy security strategies worldwide. The anticipated growth is not merely incremental but represents a fundamental shift towards a more connected, sustainable, and reliable global energy system, propelled by both technological imperative and environmental necessity.

- Significant market expansion anticipated, driven by global energy transition.

- Substantial investment in modernizing and expanding power transmission and distribution networks.

- Growth influenced by increasing global electricity demand and urbanization.

- Technological advancements in smart grid components are key to market evolution.

- Market size forecast reflects a strong commitment to grid resilience and sustainability.

- Developed and developing economies contributing uniquely to market growth dynamics.

- Long-term market outlook remains positive, indicating strategic importance of components.

Power Grid System Component Market Drivers Analysis

The Power Grid System Component Market is primarily driven by the escalating global demand for electricity, fueled by rapid urbanization, industrialization, and the electrification of various sectors including transportation. As economies grow and populations expand, the need for robust and reliable electricity supply intensifies, necessitating significant investments in both new and upgraded grid infrastructure. This foundational demand inherently boosts the consumption of essential grid components across generation, transmission, and distribution networks. Furthermore, the pervasive trend of replacing aging power infrastructure, particularly in developed regions, acts as a substantial market driver. Decades-old grids are increasingly inefficient, prone to failures, and unable to support modern energy requirements, thus creating a continuous demand for advanced, more durable, and smarter components.

A critical driver is the global energy transition towards renewable sources. The integration of large-scale solar and wind farms, along with distributed energy resources, requires significant modifications and enhancements to existing grid architectures. Traditional grid components were not designed for the intermittent and often decentralized nature of renewable power. Consequently, there is a burgeoning need for flexible, intelligent, and resilient components such as smart transformers, advanced switchgear, and digital control systems that can manage bidirectional power flows and ensure grid stability. Government policies and regulations promoting grid modernization, energy efficiency, and carbon reduction goals also provide strong impetus, often backed by substantial funding and incentives for grid infrastructure projects, thereby accelerating market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Energy Transition & Renewable Integration | +2.1% | Europe, Asia Pacific, North America | 2025-2033 |

| Aging Infrastructure Modernization | +1.8% | North America, Europe | 2025-2033 |

| Increasing Global Electricity Demand | +1.5% | Asia Pacific, Latin America, MEA | 2025-2033 |

| Government Initiatives & Smart Grid Investments | +1.4% | Global | 2025-2033 |

| Urbanization & Industrialization | +1.0% | Asia Pacific, Africa | 2025-2033 |

Power Grid System Component Market Restraints Analysis

Despite robust growth prospects, the Power Grid System Component Market faces several significant restraints that could impede its expansion. One of the primary inhibitors is the substantial capital expenditure required for grid infrastructure projects and component upgrades. The high upfront costs associated with manufacturing, purchasing, and installing advanced power grid components, particularly for large-scale transmission and distribution networks, can pose a considerable financial burden for utilities and governments. This financial constraint is often exacerbated by lengthy project approval processes and complex regulatory frameworks, which can delay or even deter necessary investments in grid modernization and expansion, thereby restraining market growth.

Another crucial restraint pertains to the complexities of integrating new technologies and systems into existing, often disparate, grid architectures. Legacy infrastructure may not be compatible with advanced smart grid components, leading to high integration costs, technical challenges, and extended implementation timelines. Furthermore, geopolitical uncertainties, trade protectionism, and disruptions in global supply chains, as witnessed in recent years, can significantly impact the availability and cost of raw materials and finished components. This volatility introduces risks for manufacturers and project developers, potentially leading to project delays or cancellations. The shortage of skilled labor capable of designing, installing, and maintaining complex modern grid components also presents a long-term challenge, limiting the pace of new deployments and upgrades in certain regions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure & Investment Barriers | -1.2% | Global | 2025-2033 |

| Complex Regulatory Frameworks & Approvals | -0.9% | North America, Europe | 2025-2033 |

| Supply Chain Disruptions & Material Price Volatility | -0.7% | Global | 2025-2030 |

| Integration Challenges with Legacy Infrastructure | -0.6% | Europe, North America | 2025-2033 |

| Shortage of Skilled Workforce | -0.5% | Global | 2025-2033 |

Power Grid System Component Market Opportunities Analysis

Significant opportunities are emerging within the Power Grid System Component Market, primarily driven by the imperative for grid modernization and the global pursuit of energy sustainability. The increasing adoption of smart grid technologies presents a vast avenue for growth, as utilities invest in advanced meters, sensors, digital substations, and intelligent control systems. These technologies enhance grid efficiency, reliability, and enable better integration of distributed energy resources, opening new markets for component manufacturers specializing in smart and digitally enabled solutions. Furthermore, the expansion of energy storage systems, especially large-scale batteries, creates opportunities for grid components designed to handle bidirectional power flow and provide grid stabilization services, bridging the gap between intermittent renewable generation and consistent power supply.

The development of microgrids and decentralized energy systems also represents a compelling opportunity, particularly in remote areas or for critical facilities requiring enhanced energy independence and resilience. These smaller, self-contained grids necessitate specialized components tailored for localized generation, storage, and distribution, distinct from traditional large-scale grid infrastructure. Moreover, the electrification of new sectors, such as electric vehicles (EVs) and industrial processes, is placing unprecedented demands on power grids, driving the need for upgraded charging infrastructure, reinforced distribution networks, and innovative components capable of managing higher loads and peak demands. Emerging markets in Asia Pacific, Latin America, and Africa, with their rapidly expanding electricity access and infrastructure development projects, offer substantial greenfield opportunities for component deployment and market penetration.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Smart Grid Technologies | +1.9% | Global | 2025-2033 |

| Integration of Energy Storage Systems | +1.6% | North America, Europe, Asia Pacific | 2025-2033 |

| Growth of Microgrids & Decentralized Energy Systems | +1.3% | Remote Regions, Critical Infrastructure | 2025-2033 |

| Electrification of Transportation & Industry | +1.2% | Global | 2025-2033 |

| Emerging Markets Infrastructure Development | +1.0% | Asia Pacific, Africa, Latin America | 2025-2033 |

Power Grid System Component Market Challenges Impact Analysis

The Power Grid System Component Market contends with several significant challenges that can impact its trajectory and operational efficiency. One formidable challenge is the inherent complexity of integrating diverse and often incompatible technologies into a seamless, interconnected grid. As grids evolve to incorporate a mix of centralized and distributed renewable energy sources, energy storage, and smart devices, ensuring interoperability and managing the technical complexities of these varied components becomes increasingly difficult. This technical complexity can lead to extended project timelines, cost overruns, and potential operational bottlenecks, particularly in regions with fragmented or outdated grid architectures.

Cybersecurity threats pose another critical challenge. As power grids become more digitized and interconnected, they also become more vulnerable to sophisticated cyberattacks that can target critical components, disrupt operations, and compromise data integrity. Protecting an expansive network of components from malicious actors requires continuous investment in advanced security measures, robust monitoring systems, and highly skilled cybersecurity personnel, adding to the operational burden and cost. Furthermore, environmental and climate change impacts, such as extreme weather events, place immense stress on grid infrastructure, leading to frequent damages and the need for more resilient, albeit more expensive, components. Navigating the stringent environmental regulations and obtaining land use approvals for new transmission lines and substations also present logistical and bureaucratic hurdles, slowing down critical infrastructure development.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cybersecurity Threats to Digitalized Grids | -1.0% | Global | 2025-2033 |

| Complexity of Grid Modernization & Integration | -0.8% | North America, Europe | 2025-2033 |

| Environmental Regulations & Land Use Issues | -0.7% | Global | 2025-2033 |

| Impact of Extreme Weather Events | -0.6% | Coastal Regions, Disaster-Prone Areas | 2025-2033 |

| Maintaining Grid Stability with Intermittent Renewables | -0.5% | Global | 2025-2033 |

Power Grid System Component Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the Power Grid System Component Market, offering a detailed forecast from 2025 to 2033. It encompasses a thorough examination of market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. The report delivers actionable insights into market dynamics, competitive landscape, and technological advancements shaping the future of power grid infrastructure globally.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 155.2 Billion |

| Market Forecast in 2033 | USD 263.7 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 247 |

| Key Trends | |

| Segments Covered | |

| Key Companies Covered | Siemens Energy AG, ABB Ltd., Schneider Electric SE, General Electric Company, Eaton Corporation plc, Hitachi Energy Ltd., Toshiba Corporation, Mitsubishi Electric Corporation, Hyundai Electric & Energy Systems Co., Ltd., Bharat Heavy Electricals Limited (BHEL), Legrand S.A., Fuji Electric Co., Ltd., NKT A/S, Nexans S.A., Prysmian Group, LS Electric Co., Ltd., CG Power and Industrial Solutions Limited, Lucy Electric Ltd., Hubbell Inc., Efacec Engenharia e Sistemas S.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Power Grid System Component Market is comprehensively segmented to provide a granular understanding of its diverse landscape and intricate dynamics. This segmentation facilitates detailed analysis of market performance across various component types, voltage levels, applications, and end-user categories, enabling stakeholders to identify specific growth areas and strategic opportunities. Each segment reflects unique demand patterns, technological requirements, and regulatory influences, contributing to the overall market trajectory.

- By Component: This segment encompasses the fundamental building blocks of any power grid, ranging from major power equipment to intricate control systems.

- Transformers: Essential for voltage conversion, including Power Transformers for transmission, Distribution Transformers for local supply, and Instrument Transformers for measurement and protection.

- Switchgear: Devices used to control, protect, and isolate electrical equipment, categorized by voltage levels such as High Voltage Switchgear, Medium Voltage Switchgear, and Low Voltage Switchgear.

- Conductors & Cables: Materials used for transmitting electricity, including Overhead Cables, Underground Cables for urban areas, and Submarine Cables for underwater power transmission.

- Insulators: Components that prevent unwanted current flow, crucial for safety and efficiency.

- Circuit Breakers: Safety devices that protect electrical circuits from damage caused by overcurrent or short circuit.

- Relays: Electrical switches that open or close circuits based on control signals, vital for protection and control systems.

- Capacitors & Reactors: Used for reactive power compensation and voltage stabilization in the grid.

- SCADA Systems: Supervisory Control and Data Acquisition systems, providing real-time monitoring and control of grid operations.

- Others: Includes components such as surge arresters, meters, and various fittings and accessories.

- By Voltage Level: Categorizes components based on the voltage at which they operate, impacting design and application.

- High Voltage: Typically used for long-distance power transmission (e.g., >230 kV).

- Medium Voltage: Used for local transmission and distribution (e.g., 1 kV to 230 kV).

- Low Voltage: Used for final power distribution to end-users (e.g., <1 kV).

- By Application: Defines the specific stage of the power delivery chain where components are utilized.

- Generation: Components used in power plants to generate electricity.

- Transmission: Equipment for long-distance bulk power transfer.

- Distribution: Components used for delivering electricity from substations to consumers.

- By End-User: Identifies the primary consumers of power grid components.

- Utilities: National and private power companies responsible for generation, transmission, and distribution.

- Industrial: Large industrial complexes with significant power demands and private grid infrastructure.

- Commercial: Commercial establishments requiring grid components for their operational needs.

- Residential: Components supporting household power connectivity and smart home integration.

Regional Highlights

- North America: This region is characterized by substantial investments in grid modernization and resilience, particularly in response to aging infrastructure and increasing extreme weather events. The focus is on integrating renewable energy, enhancing cybersecurity, and deploying smart grid technologies to improve efficiency and reliability. The United States and Canada are leading these efforts.

- Europe: Europe's market is primarily driven by ambitious decarbonization goals and the widespread integration of renewable energy sources. Significant investments are being made in upgrading cross-border interconnectors and developing smart grid solutions to manage complex energy flows. Germany, the UK, France, and the Nordic countries are at the forefront of this transition.

- Asia Pacific (APAC): The APAC region represents the largest and fastest-growing market, propelled by rapid industrialization, urbanization, and increasing electricity demand, particularly in developing economies. Extensive infrastructure development projects, coupled with a push for renewable energy adoption in countries like China, India, Japan, and Australia, are fueling strong demand for all types of grid components.

- Latin America: This region is witnessing growth due to increasing energy access initiatives, infrastructure development, and a rising focus on renewable energy projects. Brazil, Mexico, and Chile are key markets, driven by the need to expand and modernize their power grids to support economic growth and address energy deficits.

- Middle East and Africa (MEA): The MEA market is expanding driven by ongoing electrification projects, economic diversification efforts, and substantial investments in smart city initiatives and renewable energy plants, particularly in the GCC countries and South Africa. The need for reliable power supply in rapidly developing urban centers is a significant driver.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Power Grid System Component Market.- Siemens Energy AG

- ABB Ltd.

- Schneider Electric SE

- General Electric Company

- Eaton Corporation plc

- Hitachi Energy Ltd.

- Toshiba Corporation

- Mitsubishi Electric Corporation

- Hyundai Electric & Energy Systems Co., Ltd.

- Bharat Heavy Electricals Limited (BHEL)

- Legrand S.A.

- Fuji Electric Co., Ltd.

- NKT A/S

- Nexans S.A.

- Prysmian Group

- LS Electric Co., Ltd.

- CG Power and Industrial Solutions Limited

- Lucy Electric Ltd.

- Hubbell Inc.

- Efacec Engenharia e Sistemas S.A.

Frequently Asked Questions

What is the projected growth rate of the Power Grid System Component Market?

The Power Grid System Component Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, driven by global energy transitions and grid modernization efforts.

How large is the Power Grid System Component Market expected to be by 2033?

The market for Power Grid System Components is projected to reach an estimated USD 263.7 Billion by the end of the forecast period in 2033, up from USD 155.2 Billion in 2025.

What are the primary drivers for the Power Grid System Component Market?

Key drivers include the global energy transition towards renewables, the modernization of aging grid infrastructure, increasing global electricity demand, and supportive government initiatives for smart grid development.

How is AI impacting the Power Grid System Component Market?

AI is significantly impacting the market by enabling predictive maintenance for components, optimizing real-time energy management, facilitating renewable integration, and enhancing grid cybersecurity and resilience.

Which regions are expected to be the key growth areas for Power Grid System Components?

Asia Pacific is anticipated to be the largest and fastest-growing market due to rapid urbanization and industrialization, while North America and Europe will see significant investments in grid modernization and renewable integration.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted