Paper Packaging Material Market

Paper Packaging Material Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705966 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

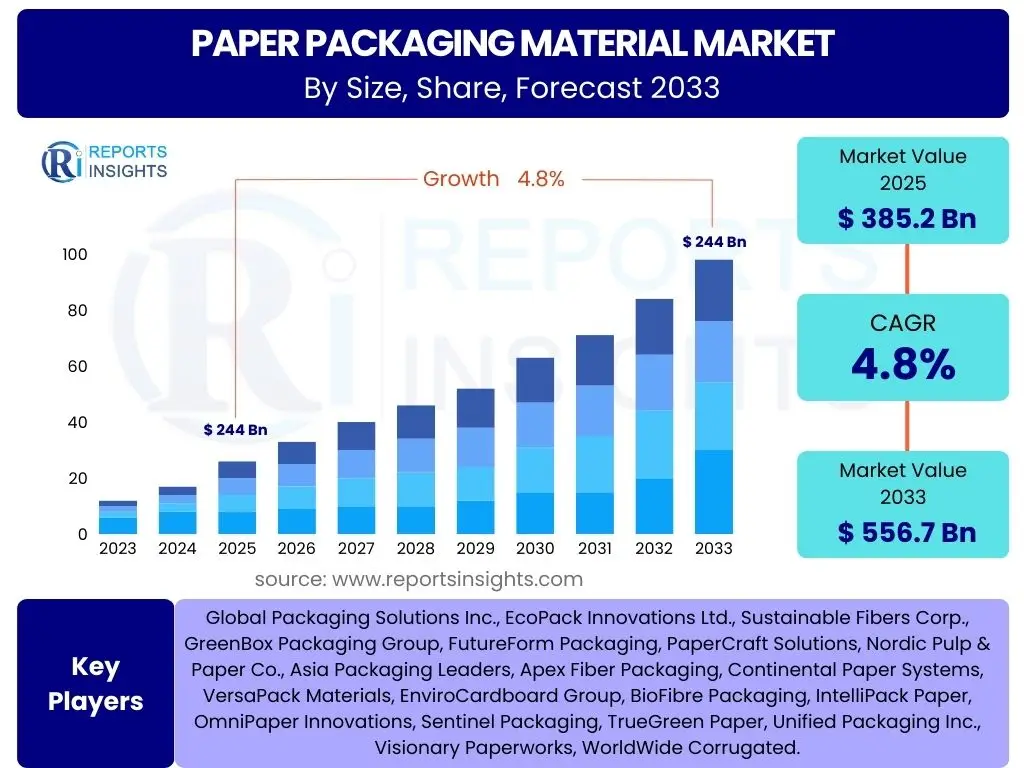

Paper Packaging Material Market Size

According to Reports Insights Consulting Pvt Ltd, The Paper Packaging Material Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. The market is estimated at USD 385.2 Billion in 2025 and is projected to reach USD 556.7 Billion by the end of the forecast period in 2033.

Key Paper Packaging Material Market Trends & Insights

User inquiries frequently focus on the transformative forces shaping the paper packaging industry. A primary theme is the overwhelming global shift towards sustainable and eco-friendly solutions, driven by heightened environmental awareness among consumers and stringent governmental regulations on plastic use. Another significant area of interest revolves around the impact of the booming e-commerce sector, which necessitates innovative, protective, and often branded paper-based packaging solutions. Users also explore advancements in material science, particularly concerning barrier properties and the integration of smart technologies, indicating a desire for packaging that offers both functionality and connectivity.

The market is witnessing a profound evolution, moving beyond basic protective functions to embrace advanced capabilities. There is a growing demand for packaging that is not only recyclable and biodegradable but also compostable, reflecting a comprehensive approach to circular economy principles. Innovations in lightweighting and structural design are enhancing efficiency and reducing logistics costs, while advancements in printing technologies enable greater customization and branding opportunities. Furthermore, the integration of intelligent features like QR codes and RFID tags is paving the way for enhanced consumer engagement and supply chain transparency, reflecting the market's trajectory towards a more sophisticated and interconnected future.

- Accelerated adoption of sustainable and recyclable paper-based solutions.

- Significant growth fueled by the expansion of the e-commerce sector.

- Innovation in barrier coatings for moisture, grease, and oxygen protection.

- Development of lightweight yet durable packaging designs to optimize logistics.

- Increasing integration of smart packaging technologies (e.g., QR codes, NFC).

- Shift towards mono-material paper solutions to simplify recycling.

- Greater emphasis on aesthetic appeal and customized branding through digital printing.

AI Impact Analysis on Paper Packaging Material

Common user questions regarding AI's influence on the paper packaging material sector highlight curiosity about efficiency gains, cost reduction, and enhanced sustainability. Users are keen to understand how AI can optimize manufacturing processes, streamline supply chains, and improve product quality. There is significant interest in AI's role in predictive maintenance for machinery, minimizing downtime, and its application in demand forecasting to reduce waste and inventory levels. Additionally, inquiries often touch upon AI's potential in designing more sustainable and functional packaging solutions, reflecting an expectation for intelligent systems to drive innovation and responsible resource management.

The integration of Artificial Intelligence is poised to revolutionize the paper packaging industry across multiple facets, from raw material sourcing to end-of-life cycle management. AI algorithms can analyze vast datasets to predict raw material price fluctuations, optimize production schedules for maximum yield and energy efficiency, and fine-tune machine parameters for precise cuts and folds, thereby reducing material waste. In the realm of design, generative AI can explore numerous structural possibilities, creating designs that are both aesthetically pleasing and structurally sound while minimizing material usage. Furthermore, AI-powered vision systems are enhancing quality control by rapidly identifying defects, ensuring higher product standards and reducing recalls, ultimately contributing to a more resilient, efficient, and sustainable packaging ecosystem.

- Optimized production planning and scheduling through predictive analytics.

- Enhanced quality control with AI-powered vision inspection systems, reducing defects.

- Predictive maintenance for machinery, minimizing downtime and operational costs.

- Improved supply chain efficiency and logistics management via AI-driven forecasting.

- Development of innovative and sustainable packaging designs using generative AI.

- Personalized packaging solutions based on consumer data analysis.

- Automated waste sorting and recycling process enhancement.

Key Takeaways Paper Packaging Material Market Size & Forecast

Analysis of common user questions regarding the Paper Packaging Material market size and forecast reveals a consistent focus on understanding the primary drivers of growth and the long-term viability of paper-based solutions. Users are particularly interested in the sustained momentum driven by environmental regulations and consumer preferences for eco-friendly alternatives. The robust growth projected for the market underscores a fundamental shift away from conventional plastics in various applications, indicating significant investment opportunities and strategic realignments across the packaging value chain. The forecast suggests that paper packaging will not only expand its traditional strongholds but also penetrate new segments previously dominated by other materials, solidifying its position as a cornerstone of sustainable commerce.

The market's trajectory is firmly upward, propelled by irreversible global trends towards sustainability and the digital transformation of retail. The significant projected increase in market value by 2033 highlights the industry's resilience and adaptability in responding to evolving consumer demands and regulatory pressures. Key insights suggest that companies investing in advanced paper technologies, circular economy initiatives, and intelligent packaging solutions will be best positioned to capitalize on this growth. Furthermore, the forecast indicates a growing emphasis on regional manufacturing capabilities to shorten supply chains and reduce environmental footprints, fostering localized innovations and strengthening market presence in high-growth regions.

- Significant and sustained market growth driven by global sustainability mandates.

- E-commerce expansion remains a critical catalyst for demand across various product types.

- Innovation in barrier properties and functional coatings is crucial for market penetration.

- Strong investment in advanced manufacturing and automation is anticipated.

- Regional markets like Asia Pacific and Europe are poised for substantial expansion due to regulatory support and consumer awareness.

Paper Packaging Material Market Drivers Analysis

The global shift towards sustainability and environmental consciousness is a paramount driver for the paper packaging material market. Consumers are increasingly prioritizing eco-friendly products, compelling brands to adopt recyclable, biodegradable, and compostable packaging solutions. This trend is strongly supported by a growing number of governmental bans and restrictions on single-use plastics, creating an imperative for industries to pivot towards paper-based alternatives. The rapid proliferation of e-commerce has also significantly boosted demand for corrugated boxes and flexible paper packaging, which are essential for safe and efficient product delivery, further fueling market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Consumer Preference for Sustainable Packaging | +1.5% | Global, particularly Europe & North America | Short to Mid-term (2025-2030) |

| Increasing E-commerce Penetration and Demand for Shipping Packaging | +1.2% | Global, with strong impact in Asia Pacific & North America | Short to Mid-term (2025-2030) |

| Strict Regulatory Frameworks and Plastic Bans | +1.0% | Europe, parts of Asia Pacific, selected North American states | Mid to Long-term (2025-2033) |

| Technological Advancements in Paper Material Functionality | +0.8% | Global | Mid to Long-term (2027-2033) |

Paper Packaging Material Market Restraints Analysis

Despite the strong growth drivers, the paper packaging material market faces several notable restraints. The volatility in raw material prices, particularly for wood pulp, can significantly impact production costs and profit margins for manufacturers. This fluctuation is often influenced by factors such as climate events, energy costs, and global supply-demand dynamics. Additionally, competition from alternative packaging materials, especially lightweight and durable plastics, continues to pose a challenge in specific applications where cost-effectiveness and barrier properties are paramount. The inherent bulkiness and weight of some paper packaging compared to plastics can also lead to higher transportation costs, particularly for international shipments, affecting overall supply chain efficiency and sustainability goals.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices (Pulp) | -0.7% | Global | Short to Mid-term (2025-2028) |

| Competition from Alternative Packaging Materials (e.g., lightweight plastics) | -0.5% | Global | Mid-term (2026-2031) |

| Higher Production and Energy Costs | -0.4% | Europe, Asia Pacific (energy-intensive production) | Short-term (2025-2027) |

Paper Packaging Material Market Opportunities Analysis

The paper packaging material market is poised for significant opportunities driven by ongoing innovations and evolving market needs. A key opportunity lies in the development of advanced barrier coatings that enable paper to protect against moisture, oxygen, and grease, thus expanding its applicability to sensitive products like food and pharmaceuticals currently dominated by plastic. The rising demand for customized and personalized packaging, fueled by digital printing technologies, presents a lucrative niche for brands seeking unique market differentiation. Furthermore, the exploration of novel fiber sources, including agricultural waste and recycled materials, offers avenues for more sustainable and cost-effective raw material procurement, reducing reliance on virgin forest resources and enhancing circularity within the industry.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Barrier Coatings for Food & Liquid Packaging | +0.9% | Global, especially North America & Europe | Mid to Long-term (2027-2033) |

| Growth in Demand for Sustainable Packaging in Healthcare and Personal Care | +0.8% | Global | Mid-term (2026-2030) |

| Innovation in Smart and Connected Packaging Solutions | +0.6% | Europe, North America, parts of Asia Pacific | Long-term (2028-2033) |

Paper Packaging Material Market Challenges Impact Analysis

The paper packaging material market faces several significant challenges that could impede its growth trajectory. The complexity and cost associated with establishing efficient recycling and waste collection infrastructure for paper-based packaging, especially composite materials, remain a substantial hurdle. Many regions lack the necessary facilities to handle the increasing volume of paper waste, leading to lower recycling rates than desired. Furthermore, intense competition from well-established and often cheaper plastic packaging solutions in certain applications, particularly those requiring extreme durability or specific barrier properties at a lower cost, continues to be a persistent challenge. Managing the environmental footprint of paper production, including water usage and energy consumption, also presents an ongoing challenge as the industry strives for greater overall sustainability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Inefficient Recycling and Waste Management Infrastructure | -0.6% | Developing Economies, parts of Asia Pacific | Mid to Long-term (2026-2033) |

| Higher Per-Unit Cost Compared to Traditional Plastics in Some Applications | -0.4% | Global | Short to Mid-term (2025-2029) |

| Supply Chain Disruptions and Raw Material Availability | -0.3% | Global | Short-term (2025-2027) |

Paper Packaging Material Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the Paper Packaging Material market, offering detailed insights into market size, growth drivers, restraints, opportunities, and challenges. It covers a historical period from 2019 to 2023, with projections extending to 2033, enabling a thorough understanding of market dynamics and future trends. The report meticulously segments the market by product type, application, and region, providing a granular view of specific market niches and their growth potential. It also profiles key industry players, offering strategic intelligence for stakeholders seeking to navigate the evolving landscape of sustainable packaging.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 385.2 Billion |

| Market Forecast in 2033 | USD 556.7 Billion |

| Growth Rate | 4.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Packaging Solutions Inc., EcoPack Innovations Ltd., Sustainable Fibers Corp., GreenBox Packaging Group, FutureForm Packaging, PaperCraft Solutions, Nordic Pulp & Paper Co., Asia Packaging Leaders, Apex Fiber Packaging, Continental Paper Systems, VersaPack Materials, EnviroCardboard Group, BioFibre Packaging, IntelliPack Paper, OmniPaper Innovations, Sentinel Packaging, TrueGreen Paper, Unified Packaging Inc., Visionary Paperworks, WorldWide Corrugated. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Paper Packaging Material market is comprehensively segmented to provide a detailed understanding of its diverse landscape and specific growth avenues. Segmentation by product type includes corrugated board, which dominates due to its versatility and strength for shipping, alongside cartonboard and liquid packaging board crucial for consumer goods and beverages. Flexible paper packaging and specialty papers represent innovative segments expanding into new applications requiring specific barrier properties or aesthetic appeal. Further segmentation by application highlights key end-use industries such as food & beverages, healthcare, e-commerce, and industrial sectors, each driving distinct demands for paper packaging solutions, reflecting varied functional and regulatory requirements across the value chain.

Each segment within the paper packaging market exhibits unique growth patterns and technological advancements. The food and beverage sector, for instance, demands advanced barrier solutions for paper-based containers to ensure product freshness and safety, driving innovation in coatings. The burgeoning e-commerce segment necessitates durable and sustainable shipping solutions, propelling demand for corrugated materials and optimized void fill. Healthcare and personal care industries are increasingly adopting paper packaging to meet consumer preferences for eco-friendly alternatives while adhering to stringent hygiene and regulatory standards. Understanding these distinct segment dynamics is crucial for market participants to tailor their strategies and capitalize on specific growth opportunities within this evolving industry.

- By Product Type:

- Corrugated Board: Widely used for shipping containers and industrial packaging due to high strength and cushioning properties.

- Cartonboard/Folding Boxboard: Essential for retail packaging, food boxes, and pharmaceutical cartons, offering excellent printability and foldability.

- Liquid Packaging Board: Specifically designed for beverages and dairy products, often with barrier layers for liquid containment.

- Flexible Paper Packaging: Includes pouches, bags, and wraps, growing in popularity for snacks and single-serve portions.

- Specialty Paper: Encompasses papers with specific functional properties like grease resistance or high tensile strength for niche applications.

- Paper Bags & Sacks: Traditional segment for retail and industrial bulk packaging.

- Others: Includes molded pulp products, honeycomb paper, etc.

- By Application:

- Food & Beverages: Largest segment, driven by demand for sustainable food containers, beverage cartons, and snack wrappers.

- Healthcare: Expanding use for pharmaceutical packaging, medical devices, and sterile barrier systems.

- Personal Care & Cosmetics: Increasing adoption for cosmetic boxes, soap wrappers, and other personal hygiene product packaging.

- E-commerce: Crucial for protective packaging, shipping boxes, and mailers due to online retail growth.

- Industrial: Used for heavy-duty sacks, intermediate bulk containers, and protective wraps for industrial goods.

- Consumer Goods: Encompasses packaging for electronics, apparel, and various household products.

- Others: Includes automotive, building materials, and agricultural applications.

- By End-Use Industry:

- Retail: Packaging for products sold in retail stores, focusing on shelf appeal and brand recognition.

- Food Service: Disposable cups, plates, and containers for cafes, restaurants, and catering services.

- Manufacturing: Packaging used within manufacturing processes for component protection and transport.

- Logistics: Primarily shipping and protective packaging for efficient supply chain movement.

- Pharmaceuticals: Compliance-driven packaging for medicines and health products.

- Others: Diverse applications across various commercial and industrial sectors.

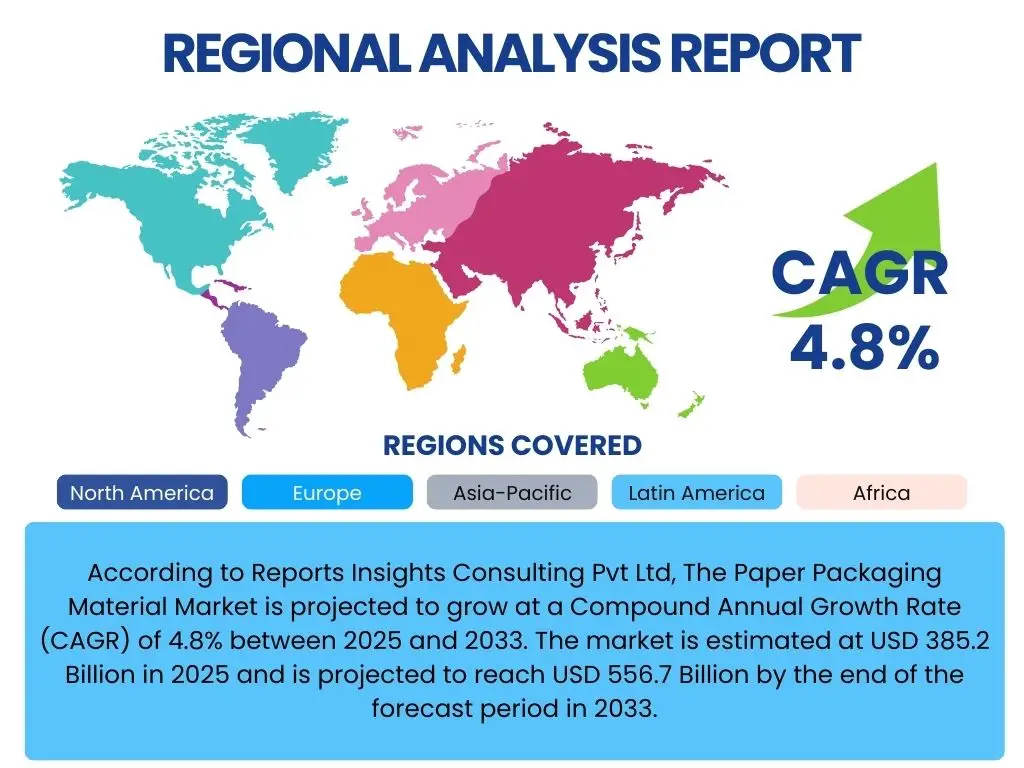

Regional Highlights

- North America: This region is characterized by high consumer awareness regarding sustainable practices and robust growth in e-commerce, driving significant demand for recyclable and innovative paper packaging solutions. The market is propelled by stringent environmental regulations and a strong presence of key industry players focused on advanced packaging technologies. Investment in automation and digitally enhanced packaging is prominent, aligning with smart factory initiatives.

- Europe: A leading region in sustainability initiatives, Europe is a major adopter of paper packaging due to pioneering regulations against single-use plastics and a strong circular economy framework. Countries like Germany, the UK, and France are at the forefront of innovation in paperboard and flexible paper solutions, particularly for the food and beverage sector. There is a strong emphasis on compostable and biodegradable solutions, driven by proactive governmental policies and consumer demand.

- Asia Pacific (APAC): Expected to be the fastest-growing market, APAC's expansion is fueled by rapid industrialization, burgeoning populations, and increasing disposable incomes, leading to higher consumption of packaged goods. Countries like China, India, and Japan are experiencing a surge in e-commerce, significantly boosting demand for corrugated and flexible paper packaging. While sustainability adoption is growing, balancing cost-effectiveness with environmental concerns remains a key regional dynamic.

- Latin America: This region presents emerging opportunities, with increasing urbanization and a growing middle class contributing to higher consumption of packaged food and consumer goods. While still developing in terms of robust recycling infrastructure, there is a growing interest in sustainable packaging solutions, influenced by global trends and increasing environmental awareness. Local production capabilities are expanding, driven by both domestic and international investments.

- Middle East & Africa (MEA): The MEA region is witnessing gradual adoption of paper packaging, driven by infrastructure development and a rising awareness of environmental issues. While the market is currently smaller compared to other regions, opportunities exist in specific segments such as food service and retail, as governments and consumers increasingly seek alternatives to plastic. Investment in local manufacturing and sustainable practices is anticipated to grow as the region diversifies its economies.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Paper Packaging Material Market.- Global Packaging Solutions Inc.

- EcoPack Innovations Ltd.

- Sustainable Fibers Corp.

- GreenBox Packaging Group

- FutureForm Packaging

- PaperCraft Solutions

- Nordic Pulp & Paper Co.

- Asia Packaging Leaders

- Apex Fiber Packaging

- Continental Paper Systems

- VersaPack Materials

- EnviroCardboard Group

- BioFibre Packaging

- IntelliPack Paper

- OmniPaper Innovations

- Sentinel Packaging

- TrueGreen Paper

- Unified Packaging Inc.

- Visionary Paperworks

- WorldWide Corrugated

Frequently Asked Questions

What is the projected growth rate for the Paper Packaging Material Market?

The Paper Packaging Material Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033, reaching an estimated value of USD 556.7 Billion by 2033.

What are the primary drivers of growth in the Paper Packaging Material Market?

Key drivers include the increasing global demand for sustainable and eco-friendly packaging solutions, rapid expansion of the e-commerce sector requiring robust shipping materials, and stringent governmental regulations enforcing bans on single-use plastics.

How is AI impacting the Paper Packaging Material industry?

AI is transforming the industry by optimizing production processes, enhancing quality control through advanced inspection systems, improving supply chain efficiency with predictive analytics, and enabling the design of innovative and sustainable packaging solutions.

Which regions are leading the adoption of Paper Packaging Materials?

Europe and North America are leading regions due to strong sustainability initiatives and e-commerce growth. The Asia Pacific region is expected to be the fastest-growing market due to rapid industrialization and increasing consumer demand.

What are the main types of Paper Packaging Materials and their applications?

The main types include corrugated board (for shipping), cartonboard (for retail and food boxes), liquid packaging board (for beverages), and flexible paper packaging (for snacks). These are widely applied across food & beverages, e-commerce, healthcare, and consumer goods industries.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted