Laminating Adhesive for Flexible Packaging Market

Laminating Adhesive for Flexible Packaging Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706310 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

Laminating Adhesive for Flexible Packaging Market Size

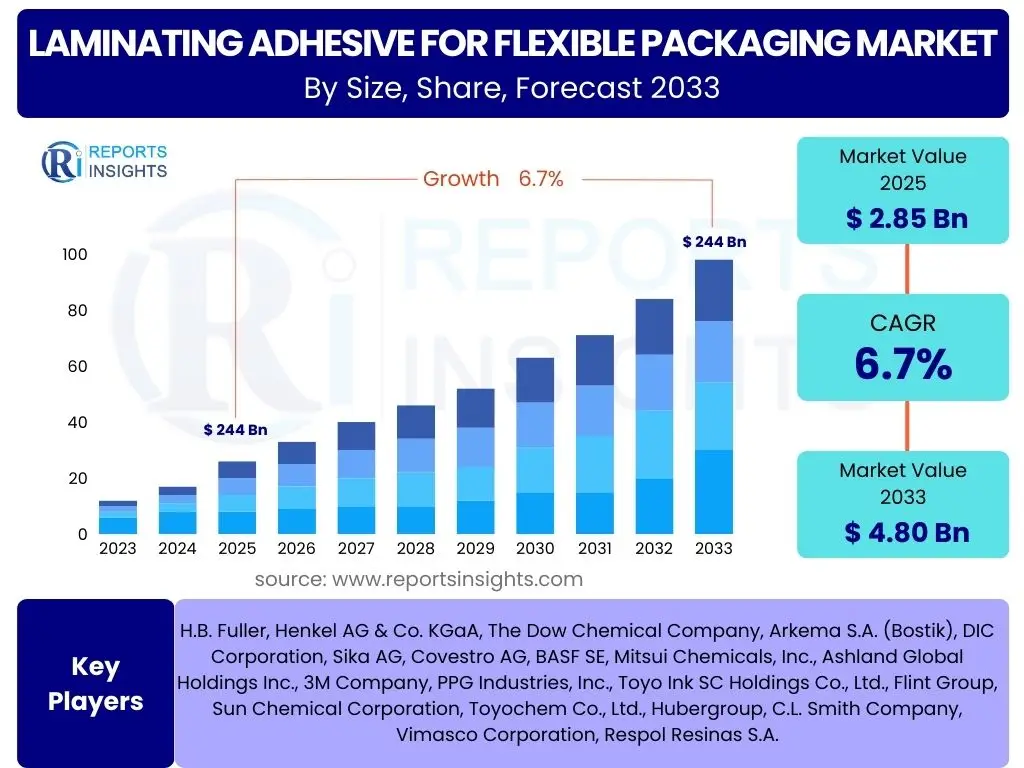

According to Reports Insights Consulting Pvt Ltd, The Laminating Adhesive for Flexible Packaging Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033. The market is estimated at USD 2.85 billion in 2025 and is projected to reach USD 4.80 billion by the end of the forecast period in 2033.

Key Laminating Adhesive for Flexible Packaging Market Trends & Insights

The laminating adhesive for flexible packaging market is witnessing significant transformation driven by evolving consumer preferences, stringent regulatory frameworks, and technological advancements. Key trends revolve around enhanced sustainability, with a strong push towards solvent-free, water-based, and bio-based adhesive solutions that minimize environmental impact and improve worker safety. Performance remains critical, leading to innovations in adhesives that offer superior barrier properties, retort resistance, and improved adhesion for diverse film substrates. The rapid growth of e-commerce also necessitates new adhesive formulations capable of withstanding the rigors of transit while maintaining package integrity and aesthetic appeal, directly influencing material selection and processing techniques.

Furthermore, there is a rising demand for high-performance adhesives that cater to specialized applications such as medical packaging and demanding food products, requiring robust chemical resistance, thermal stability, and product compatibility. Digitalization and automation in manufacturing processes are also impacting adhesive selection, favoring formulations that offer faster curing times and improved processing efficiency. The industry is also exploring circular economy principles, with efforts focused on developing adhesives that facilitate easier de-lamination for recycling or enable mono-material flexible packaging structures that are inherently more recyclable.

- Increased demand for sustainable and eco-friendly adhesive solutions.

- Rising adoption of solvent-free and water-based laminating adhesives.

- Focus on high-performance adhesives for barrier and retort applications.

- Growth driven by e-commerce and changing consumer packaging needs.

- Development of adhesives supporting circular economy initiatives.

AI Impact Analysis on Laminating Adhesive for Flexible Packaging

Artificial Intelligence (AI) is poised to significantly impact the laminating adhesive for flexible packaging market by revolutionizing various stages of the value chain, from research and development to manufacturing and quality control. AI's capabilities in data analysis and predictive modeling can accelerate the discovery and formulation of new adhesive compositions, optimizing material properties for specific packaging requirements such as barrier performance, bond strength, and thermal resistance. This includes identifying optimal raw material combinations, predicting cure rates, and simulating adhesive behavior under different environmental conditions, leading to faster innovation cycles and reduced R&D costs. Furthermore, AI-driven process optimization in manufacturing facilities can enhance efficiency, minimize waste, and improve consistency in adhesive production, leading to higher quality products and reduced operational expenses.

In quality assurance, AI-powered vision systems and sensors can monitor production lines in real-time, detecting defects or inconsistencies in laminating adhesive application with unprecedented accuracy, thereby reducing product recalls and improving overall product reliability. Predictive maintenance facilitated by AI algorithms can anticipate equipment failures in adhesive manufacturing or lamination machinery, minimizing downtime and optimizing maintenance schedules. Beyond production, AI can also contribute to supply chain optimization by predicting demand fluctuations for specific adhesive types, managing inventory more effectively, and optimizing logistics, leading to more resilient and responsive supply networks. Ultimately, AI's integration is expected to drive greater efficiency, innovation, and sustainability within the laminating adhesive industry, enabling manufacturers to meet increasingly complex market demands.

- Accelerated R&D and formulation optimization through AI-driven material discovery.

- Enhanced manufacturing efficiency and quality control via AI-powered process optimization.

- Predictive maintenance for production machinery to reduce downtime.

- Improved supply chain management and demand forecasting for raw materials and finished goods.

- Real-time defect detection in adhesive application using AI vision systems.

Key Takeaways Laminating Adhesive for Flexible Packaging Market Size & Forecast

The laminating adhesive for flexible packaging market is positioned for robust growth over the forecast period, primarily propelled by the expanding flexible packaging industry and the continuous innovation in adhesive technologies. A significant shift towards sustainable solutions, including solvent-free and water-based adhesives, is a critical growth enabler, driven by increasing environmental regulations and consumer demand for eco-friendly products. The market's expansion is further supported by the burgeoning food and beverage sector, especially in emerging economies, which heavily relies on flexible packaging for convenience, shelf-life extension, and cost efficiency. The evolving landscape of e-commerce also contributes to this growth, necessitating resilient and protective packaging solutions that laminating adhesives facilitate.

Geographically, the Asia Pacific region is expected to lead the market in terms of both consumption and production, owing to its rapidly industrializing economies, growing middle-class population, and expanding manufacturing base. While raw material price volatility and the complexity of achieving full recyclability for multi-layer films present ongoing challenges, opportunities abound in developing high-performance, retort-compatible, and bio-based adhesive formulations. The competitive landscape is characterized by established global players investing heavily in R&D to meet these emerging demands, ensuring a dynamic and innovation-driven market outlook.

- Significant market growth fueled by flexible packaging demand and sustainability trends.

- Asia Pacific identified as the leading growth region.

- Strong emphasis on solvent-free and water-based adhesive innovation.

- Food & beverage and e-commerce sectors are primary demand drivers.

- Challenges remain in raw material stability and true recyclability of packaging structures.

Laminating Adhesive for Flexible Packaging Market Drivers Analysis

The market for laminating adhesives in flexible packaging is fundamentally driven by the escalating global demand for flexible packaging solutions. This growth is attributable to flexible packaging's inherent advantages, including its lightweight nature, cost-effectiveness, reduced material consumption, and extended shelf-life capabilities, particularly beneficial for food and beverage products. The convenience factor, such as ease of storage and portability offered by flexible formats like pouches and stand-up bags, resonates strongly with modern consumer lifestyles. Furthermore, advancements in film technologies necessitate sophisticated adhesive solutions capable of bonding diverse substrates while maintaining package integrity, barrier properties, and aesthetic appeal. The rapid expansion of e-commerce platforms further accelerates this demand, as flexible packaging offers optimal protection during transit with minimal weight.

Innovations in adhesive chemistry are also a significant driver, with ongoing research and development efforts leading to the commercialization of high-performance, environmentally friendly adhesives. The shift towards solvent-free and water-based formulations addresses growing environmental concerns and regulatory pressures, while also improving worker safety and reducing Volatile Organic Compound (VOC) emissions. These newer formulations often provide comparable or superior bond strengths and processing speeds, making them increasingly attractive to packaging converters. Additionally, the pharmaceutical and personal care industries are contributing to market growth, requiring specialized laminating adhesives that meet stringent regulatory standards for product safety, sterility, and tamper-evidence, driving demand for high-barrier and chemically resistant adhesive types.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Flexible Packaging | +2.5% | Global, particularly Asia Pacific | Short to Long-term |

| Growth in Food & Beverage Industry | +1.8% | Global, especially Emerging Markets | Short to Mid-term |

| Technological Advancements in Adhesives (e.g., Solvent-free, Water-based) | +1.5% | North America, Europe, Asia Pacific | Mid to Long-term |

| Expansion of E-commerce Sector | +1.2% | Global | Short to Mid-term |

| Emphasis on Sustainable Packaging Solutions | +1.0% | Europe, North America | Mid to Long-term |

Laminating Adhesive for Flexible Packaging Market Restraints Analysis

The laminating adhesive for flexible packaging market faces several significant restraints that could impede its growth trajectory. One primary concern is the volatility and fluctuating prices of raw materials, such as petrochemical derivatives (e.g., polyols, isocyanates) used in polyurethane adhesives and other base chemicals. These price fluctuations are often influenced by geopolitical events, supply chain disruptions, and crude oil prices, leading to increased production costs for adhesive manufacturers. Such instability can erode profit margins, compel manufacturers to pass costs onto converters, and potentially slow down market expansion as end-users seek cost-effective alternatives or scale back packaging development. The reliance on petrochemicals also introduces susceptibility to supply chain vulnerabilities and sustainability pressures, pushing for the development of alternative bio-based materials which are still in nascent stages for widespread commercial viability.

Another notable restraint is the stringent regulatory landscape, particularly concerning food contact applications and environmental emissions. Regulations like those from the FDA in North America and the EU's REACH require extensive testing and compliance for adhesives used in food packaging, adding to R&D costs and time-to-market for new formulations. Furthermore, the increasing focus on packaging recyclability and the circular economy presents a significant challenge. Many multi-layer flexible packaging structures, though highly functional, are difficult to recycle due to the disparate materials and the robust nature of the laminating adhesives used to bond them. While efforts are underway to develop de-laminatable adhesives or mono-material structures, these solutions often involve trade-offs in performance or cost, hindering widespread adoption and creating a tension between functionality and environmental goals.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -1.5% | Global | Short to Mid-term |

| Stringent Environmental & Food Safety Regulations | -1.2% | Europe, North America | Mid-term |

| Challenges in Recycling Multi-layer Flexible Packaging | -1.0% | Global, especially Developed Markets | Mid to Long-term |

| High R&D Investment for New Formulations | -0.8% | Global | Short to Mid-term |

Laminating Adhesive for Flexible Packaging Market Opportunities Analysis

Significant opportunities in the laminating adhesive for flexible packaging market are emerging from the escalating demand for sustainable packaging solutions. This includes the development and adoption of bio-based adhesives, which utilize renewable resources and offer a reduced carbon footprint compared to traditional petroleum-derived counterparts. As consumers and brands increasingly prioritize environmental responsibility, the market for compostable, biodegradable, and recyclable-enabling adhesives is set to expand. This trend is particularly pronounced in regions with strong environmental policies and consumer awareness, driving innovation in adhesive formulations that support circular economy initiatives, such as those allowing for easier de-lamination for recycling or facilitating mono-material packaging structures.

Furthermore, the continuous evolution of specialized packaging applications presents lucrative opportunities. The demand for high-barrier flexible packaging, critical for extending the shelf life of sensitive food products, pharmaceuticals, and medical devices, is growing rapidly. This requires adhesives that can withstand extreme conditions, such as retort sterilization, high temperatures, and aggressive chemicals, while maintaining exceptional bond strength and barrier integrity. Opportunities also exist in emerging markets, particularly across Asia Pacific and Latin America, where urbanization, rising disposable incomes, and the expansion of organized retail are fueling an unprecedented demand for packaged goods. These regions offer substantial growth potential for both conventional and advanced laminating adhesive technologies, as local manufacturers scale up production to meet growing consumer needs.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Sustainable & Bio-based Adhesives | +2.0% | Global, particularly Europe & North America | Mid to Long-term |

| Rising Demand for High-Performance & Barrier Adhesives | +1.7% | Global | Short to Mid-term |

| Expansion in Emerging Markets | +1.5% | Asia Pacific, Latin America, MEA | Short to Long-term |

| Technological Advancements for Enhanced Processing Efficiency | +1.0% | Global | Mid-term |

Laminating Adhesive for Flexible Packaging Market Challenges Impact Analysis

The laminating adhesive for flexible packaging market faces several inherent challenges that require continuous innovation and strategic adaptation. One significant challenge is the ongoing quest to achieve truly recyclable multi-layer flexible packaging. While flexible packaging offers numerous benefits, its multi-material composition, often bonded by durable adhesives, makes conventional recycling difficult and costly. This creates a dilemma for manufacturers trying to balance performance requirements like barrier properties and mechanical strength with environmental sustainability goals. Developing adhesives that allow for easier de-lamination during the recycling process, or enabling the creation of mono-material flexible packaging with comparable performance, remains a complex technical and economic hurdle that requires extensive R&D investment and collaboration across the value chain.

Another challenge stems from the dynamic and competitive nature of the packaging industry, where packaging converters and brand owners continuously seek cost-effective solutions without compromising on quality or performance. This puts pressure on adhesive manufacturers to innovate rapidly while managing production costs and ensuring competitive pricing. Furthermore, the diversity of film substrates and end-use applications necessitates a wide range of specialized adhesive solutions, adding complexity to product development, manufacturing, and inventory management. Navigating varying regional regulations, particularly regarding food safety and environmental compliance, further complicates market entry and product commercialization, requiring manufacturers to tailor products and strategies for different geographical markets, increasing operational complexity and compliance costs.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving Full Recyclability for Multi-layer Films | -1.8% | Global, particularly Developed Markets | Mid to Long-term |

| Raw Material Supply Chain Disruptions | -1.3% | Global | Short to Mid-term |

| Intense Competition and Price Pressure | -1.0% | Global | Short to Mid-term |

| Meeting Diverse Performance & Regulatory Requirements | -0.7% | Global | Mid-term |

Laminating Adhesive for Flexible Packaging Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global laminating adhesive for flexible packaging market, covering market sizing, growth forecasts, key trends, drivers, restraints, opportunities, and challenges. It includes detailed segmentation analysis by technology, resin type, and application, offering insights into the most lucrative segments. The report also provides a regional breakdown, highlighting the market dynamics in major geographies. A competitive landscape section profiles key market players, their strategies, and recent developments, offering stakeholders a complete understanding of the market's current state and future potential.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.85 Billion |

| Market Forecast in 2033 | USD 4.80 Billion |

| Growth Rate | 6.7% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | H.B. Fuller, Henkel AG & Co. KGaA, The Dow Chemical Company, Arkema S.A. (Bostik), DIC Corporation, Sika AG, Covestro AG, BASF SE, Mitsui Chemicals, Inc., Ashland Global Holdings Inc., 3M Company, PPG Industries, Inc., Toyo Ink SC Holdings Co., Ltd., Flint Group, Sun Chemical Corporation, Toyochem Co., Ltd., Hubergroup, C.L. Smith Company, Vimasco Corporation, Respol Resinas S.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The laminating adhesive for flexible packaging market is broadly segmented based on key attributes such as technology, resin type, and application, reflecting the diverse requirements and evolving landscape of the flexible packaging industry. Each segment plays a crucial role in shaping market dynamics, driven by specific performance needs, regulatory considerations, and end-user demands. Technological advancements continue to redefine these segments, particularly with the ongoing shift towards more sustainable and efficient adhesive systems. Understanding these segmentations is vital for stakeholders to identify growth pockets and develop targeted strategies, ensuring that products align with specific market niches and their unique demands.

The technological segmentation, encompassing solvent-based, solvent-less, and water-based adhesives, highlights the industry's progression towards more environmentally friendly solutions, with solvent-less and water-based types gaining increasing traction due to lower VOC emissions and improved safety profiles. Resin type differentiation, including polyurethane, acrylic, and polyester-based adhesives, signifies the varied performance characteristics and suitability for different substrates and applications. Finally, the application segment, which covers food and beverage, pharmaceutical, personal care, and industrial packaging, underscores the widespread utility of flexible packaging across critical consumer and industrial sectors, each demanding specialized adhesive properties for optimal product protection and shelf life.

- By Technology:

- Solvent-based

- Solvent-less

- Water-based

- Others (e.g., UV-curable, Hot-melt)

- By Resin Type:

- Polyurethane (PU)

- Acrylic

- Polyester

- Epoxy

- Others (e.g., Silicone, Polyolefin)

- By Application:

- Food & Beverage Packaging

- Snacks

- Confectionery

- Dairy

- Bakery

- Frozen Foods

- Beverages

- Other Foods

- Pharmaceutical Packaging

- Personal Care & Cosmetics Packaging

- Industrial & Other Consumer Goods Packaging

- Food & Beverage Packaging

Regional Highlights

The global laminating adhesive for flexible packaging market exhibits distinct growth patterns and maturity levels across different geographical regions. Asia Pacific (APAC) stands out as the fastest-growing region, primarily driven by rapid industrialization, increasing urbanization, and a burgeoning middle-class population with rising disposable incomes. Countries like China, India, and Southeast Asian nations are witnessing unprecedented growth in the food and beverage, pharmaceutical, and e-commerce sectors, leading to a surge in demand for flexible packaging and, consequently, laminating adhesives. The region also benefits from a robust manufacturing base and significant investments in packaging infrastructure, further solidifying its market leadership. This dynamic environment fosters both high-volume production and the adoption of advanced adhesive technologies to meet diverse market needs.

North America and Europe represent mature yet innovation-driven markets. In these regions, the emphasis is heavily placed on sustainable and high-performance adhesive solutions, driven by stringent environmental regulations, consumer demand for eco-friendly products, and advancements in packaging design. The demand here is characterized by a shift towards solvent-free, water-based, and bio-based adhesives, along with a focus on solutions that facilitate recyclability or enable mono-material packaging. While growth rates may be more moderate compared to APAC, these regions lead in technological adoption, premium applications (e.g., medical, high-barrier foods), and the development of circular economy initiatives. Latin America and the Middle East & Africa (MEA) are emerging markets, showing significant potential due to urbanization, increasing consumption of packaged goods, and growing investments in local manufacturing capabilities, promising steady growth in the long term for laminating adhesives.

- Asia Pacific (APAC): Dominates the market with the highest growth rate, fueled by robust economic development, expanding population, and rising demand from food, beverage, and pharmaceutical industries in China, India, and Southeast Asian countries.

- North America: A mature market characterized by high adoption of advanced adhesive technologies, focus on sustainability, and strong demand from the processed food and medical packaging sectors.

- Europe: A key region prioritizing environmental regulations and sustainable packaging. Driving innovation in solvent-free, water-based, and recyclable adhesive solutions, with significant demand from food packaging and personal care industries.

- Latin America: Exhibiting steady growth due to increasing urbanization, improving economic conditions, and expanding retail infrastructure, leading to higher consumption of packaged goods.

- Middle East & Africa (MEA): Emerging market with growing potential driven by population growth, diversifying economies, and increasing adoption of modern retail formats.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Laminating Adhesive for Flexible Packaging Market.- H.B. Fuller

- Henkel AG & Co. KGaA

- The Dow Chemical Company

- Arkema S.A. (Bostik)

- DIC Corporation

- Sika AG

- Covestro AG

- BASF SE

- Mitsui Chemicals, Inc.

- Ashland Global Holdings Inc.

- 3M Company

- PPG Industries, Inc.

- Toyo Ink SC Holdings Co., Ltd.

- Flint Group

- Sun Chemical Corporation

- Toyochem Co., Ltd.

- Hubergroup

- C.L. Smith Company

- Vimasco Corporation

- Respol Resinas S.A.

Frequently Asked Questions

What are laminating adhesives for flexible packaging?

Laminating adhesives are specialized chemical formulations used to bond multiple layers of flexible film substrates together, creating multi-layer packaging structures. These adhesives ensure strong bond strength, maintain barrier properties, and enable the combination of different material characteristics to meet specific packaging requirements for products like food, pharmaceuticals, and consumer goods.

What are the primary types of laminating adhesives used in flexible packaging?

The primary types are solvent-based, solvent-less, and water-based adhesives. Solvent-based adhesives offer strong bonds and high performance but require VOC emission controls. Solvent-less adhesives are environmentally friendly with fast curing times. Water-based adhesives are also eco-friendly, offering good adhesion, especially for certain substrates, and improved worker safety.

Which industries are the main consumers of laminating adhesives for flexible packaging?

The food and beverage industry is the largest consumer, utilizing these adhesives for snacks, dairy, baked goods, and beverages to enhance shelf life and protection. Other significant consumers include the pharmaceutical industry (for sterile and tamper-evident packaging), personal care and cosmetics, and various industrial and consumer goods sectors.

What are the key benefits of using flexible packaging with laminating adhesives?

Flexible packaging offers numerous benefits, including lightweight design reducing transportation costs, extended product shelf life due to enhanced barrier properties, reduced material consumption compared to rigid packaging, improved convenience for consumers (e.g., resealable pouches), and often a lower environmental footprint due to less material use and energy consumption in production.

What future trends are expected to influence the laminating adhesive market?

Future trends include a continued strong emphasis on sustainability, driving demand for bio-based, solvent-free, and water-based adhesive solutions. There will be increased focus on high-performance adhesives for barrier and retort applications, alongside the development of adhesives that facilitate the recyclability of multi-layer flexible packaging to align with circular economy goals. E-commerce growth will also continue to shape adhesive requirements for durable transit packaging.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted