Paper and Paperboard Packaging Market

Paper and Paperboard Packaging Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706096 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

Paper and Paperboard Packaging Market Size

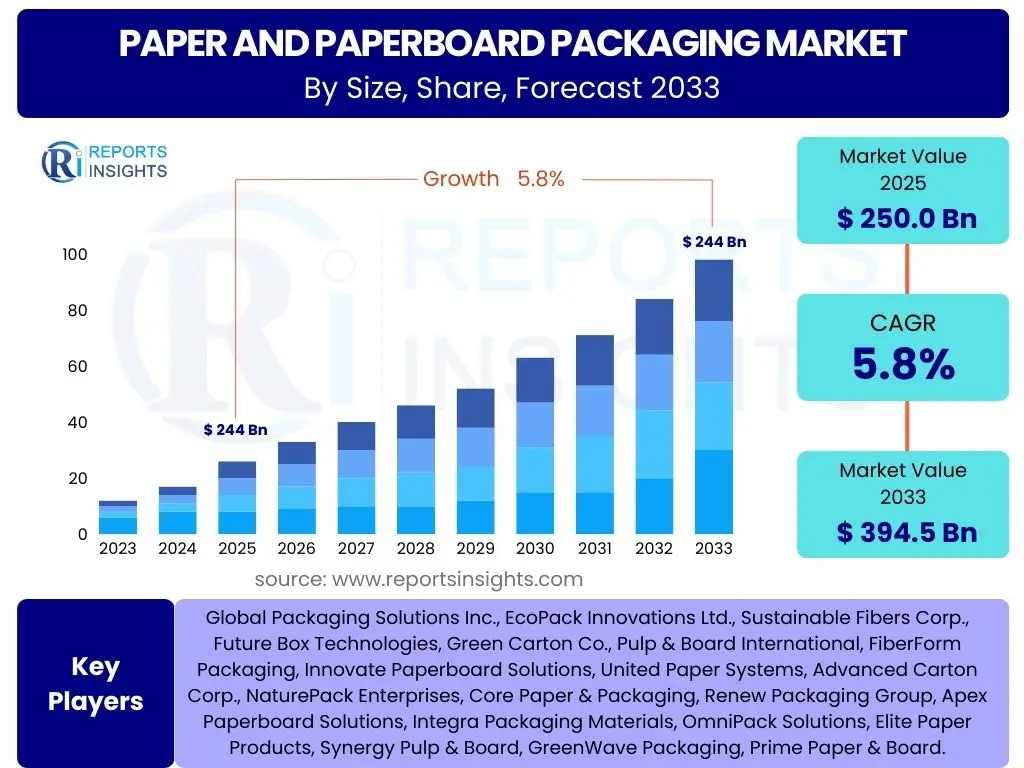

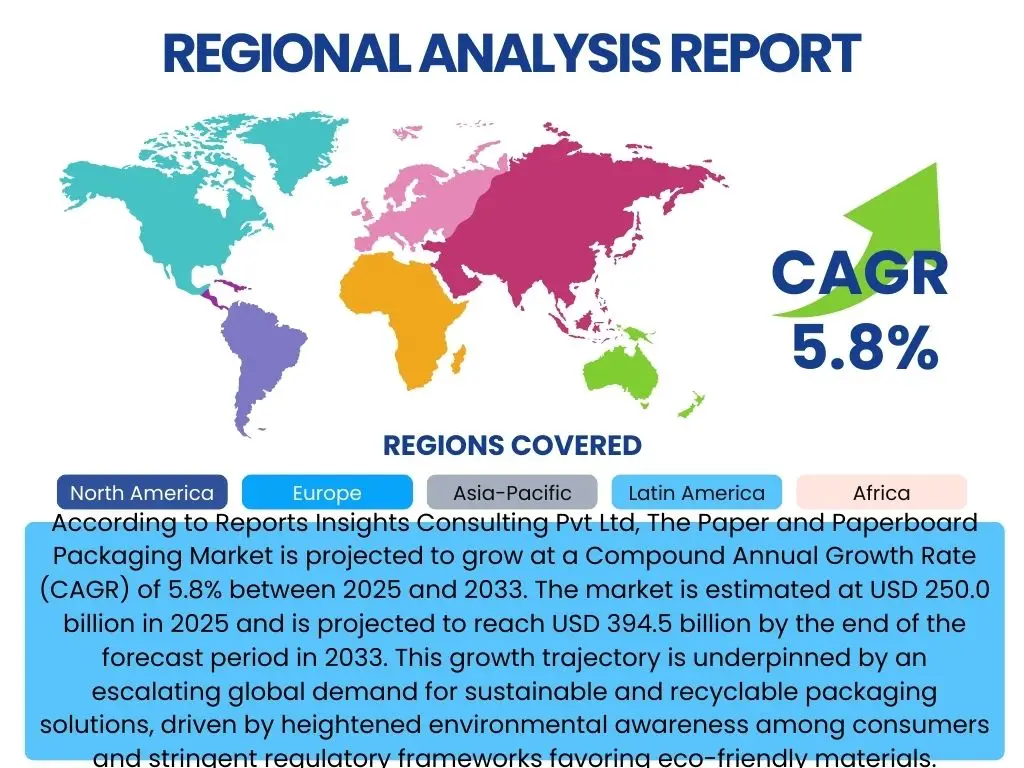

According to Reports Insights Consulting Pvt Ltd, The Paper and Paperboard Packaging Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 250.0 billion in 2025 and is projected to reach USD 394.5 billion by the end of the forecast period in 2033. This growth trajectory is underpinned by an escalating global demand for sustainable and recyclable packaging solutions, driven by heightened environmental awareness among consumers and stringent regulatory frameworks favoring eco-friendly materials.

The consistent expansion of the e-commerce sector significantly contributes to the market's robust growth, with paper and paperboard packaging offering versatile, lightweight, and protective options for online retail goods. Furthermore, innovations in packaging design, such as improved barrier properties and lightweighting, are enhancing the appeal and functional applications of paper-based solutions across various industries, including food and beverages, pharmaceuticals, and consumer goods. This sustained demand, coupled with ongoing technological advancements, positions the paper and paperboard packaging market for steady progression over the coming decade.

Key Paper and Paperboard Packaging Market Trends & Insights

Common user inquiries regarding the Paper and Paperboard Packaging market frequently revolve around its adaptability to evolving consumer demands and environmental regulations. Users often seek to understand how sustainability initiatives are reshaping packaging design, the role of digital printing in customization, and the impact of lightweighting on material consumption. There is also significant interest in the integration of smart packaging technologies and the growth of e-commerce specific packaging solutions. These questions collectively point to a market in dynamic transition, striving for both ecological responsibility and operational efficiency.

The market is witnessing a profound shift towards circular economy principles, with a strong emphasis on recyclability and the use of recycled content. Brands are increasingly adopting fiber-based alternatives to plastics to meet consumer preferences and comply with evolving environmental policies. Furthermore, technological advancements in barrier coatings are expanding the application of paperboard into new areas, enabling it to protect sensitive products that traditionally required plastic or aluminum. This confluence of environmental consciousness and material innovation is defining the current landscape of the paper and paperboard packaging industry.

- Sustainability and Recyclability Focus: Growing demand for eco-friendly, biodegradable, and recyclable packaging options, driven by consumer preference and regulatory pressures.

- E-commerce Boom: Significant increase in demand for protective, lightweight, and customizable packaging solutions for online retail.

- Smart Packaging Integration: Adoption of QR codes, RFID tags, and NFC for enhanced traceability, brand interaction, and supply chain efficiency.

- Lightweighting and Material Efficiency: Development of lighter yet stronger paperboard grades to reduce material consumption and transportation costs.

- Digital Printing Advancements: Increased use of digital printing for customization, shorter production runs, and enhanced brand aesthetics.

- Barrier Coating Innovations: Development of high-performance, recyclable barrier coatings to extend the shelf life of products in paper-based packaging.

AI Impact Analysis on Paper and Paperboard Packaging

User queries concerning the impact of Artificial Intelligence (AI) on the Paper and Paperboard Packaging market often center on its potential to revolutionize operational efficiency, supply chain management, and design processes. Stakeholders are interested in how AI can optimize manufacturing lines, predict demand fluctuations, and enhance quality control. There is also curiosity about AI's role in sustainable practices, such as waste reduction and material optimization, alongside its capabilities in personalized packaging design and predictive maintenance for machinery.

AI is set to transform the paper and paperboard packaging industry by enabling greater precision and responsiveness across the entire value chain. In manufacturing, AI-powered systems can monitor production lines in real-time, identifying anomalies, predicting equipment failures, and optimizing resource allocation, thereby minimizing downtime and waste. For supply chain logistics, AI algorithms can analyze vast datasets to forecast demand, optimize inventory levels, and streamline distribution, leading to more efficient delivery and reduced carbon footprints. Furthermore, AI can assist in the design phase by generating optimized structural designs, assessing material usage for sustainability goals, and even personalizing graphics based on consumer data.

While the adoption of AI presents significant opportunities for innovation and efficiency, it also introduces challenges related to data privacy, the need for skilled labor to manage AI systems, and the initial investment required for implementation. However, the long-term benefits in terms of cost savings, increased productivity, and enhanced product quality are expected to drive its widespread integration. AI's capacity to process complex information and identify patterns will be instrumental in fostering a more resilient, sustainable, and consumer-centric packaging ecosystem.

- Optimized Production Lines: AI-driven analytics for predictive maintenance, real-time quality control, and efficiency improvements in manufacturing processes.

- Enhanced Supply Chain Management: AI algorithms for demand forecasting, inventory optimization, and logistics planning, reducing waste and improving delivery times.

- Sustainable Material Optimization: AI tools to analyze material properties and design for reduced resource consumption and improved recyclability.

- Automated Design and Personalization: AI-powered software for rapid prototyping, structural design optimization, and custom graphic generation.

- Predictive Quality Assurance: AI systems identifying defects and inconsistencies early in the production cycle, minimizing waste and ensuring product integrity.

Key Takeaways Paper and Paperboard Packaging Market Size & Forecast

Common user questions regarding the key takeaways from the Paper and Paperboard Packaging market size and forecast typically focus on the overall growth narrative, the primary drivers of this growth, and the most significant opportunities for stakeholders. Users want to understand the market's stability, its resilience against economic fluctuations, and its alignment with global sustainability trends. There is also considerable interest in identifying which segments or regions are expected to exhibit the most promising growth and where innovation will primarily be concentrated over the forecast period.

The market's projected growth indicates a strong and sustained demand for paper-based packaging, primarily fueled by a global shift towards environmental consciousness and the relentless expansion of e-commerce. This forecast underscores the industry's critical role in circular economy initiatives, highlighting the increasing preference for renewable and recyclable materials. Stakeholders should recognize that investment in sustainable manufacturing practices, advanced barrier technologies, and digital integration will be paramount to capitalizing on future market opportunities. The robust CAGR signifies not just expansion, but also a fundamental transformation of the packaging landscape driven by evolving consumer and regulatory expectations.

- Consistent Growth Trajectory: The market demonstrates robust and steady growth, driven by fundamental shifts in consumer behavior and regulatory landscapes.

- Sustainability as a Core Driver: Environmental concerns and demand for recyclable solutions are paramount to market expansion, pushing innovation in material science and design.

- E-commerce Sector's Dominance: The exponential rise of online retail continues to be a primary catalyst for demand, particularly for protective and customizable packaging.

- Innovation in Functionality: Advances in barrier properties and lightweighting are key to expanding paper and paperboard applications across diverse industries.

- Strategic Investment Areas: Companies should prioritize investments in sustainable production, digital technologies, and R&D for advanced packaging solutions to maintain competitiveness.

Paper and Paperboard Packaging Market Drivers Analysis

The Paper and Paperboard Packaging market is predominantly driven by a global push towards sustainable and environmentally friendly packaging solutions. Increasing consumer awareness regarding plastic pollution and climate change has significantly shifted preferences towards renewable, recyclable, and biodegradable materials. This consumer-driven demand is amplified by stringent government regulations worldwide, which are increasingly mandating the use of sustainable packaging and imposing restrictions on single-use plastics. The industry is responding by innovating new paper-based solutions that meet both performance and environmental criteria.

Another pivotal driver is the unprecedented growth of the e-commerce sector. With more consumers purchasing goods online, there is a burgeoning need for protective, lightweight, and cost-effective packaging that can withstand the rigors of shipping while also offering an unboxing experience. Paper and paperboard solutions, with their versatility in design and printability, are ideally suited to meet these diverse requirements, from corrugated boxes for shipping to custom carton designs for product presentation. This dynamic interplay between environmental mandates, consumer preference, and digital retail expansion continues to propel market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Consumer Preference for Sustainable Packaging | +1.5% | Global (Europe, North America, APAC leading) | Short to Long Term |

| Expansion of E-commerce and Online Retail | +1.2% | Global (APAC, North America, Europe) | Short to Medium Term |

| Strict Environmental Regulations and Plastic Bans | +1.0% | Europe, North America, India, China | Short to Medium Term |

| Demand from Food & Beverage Industry for Safe & Hygienic Packaging | +0.8% | Global | Short to Long Term |

Paper and Paperboard Packaging Market Restraints Analysis

Despite its significant growth prospects, the Paper and Paperboard Packaging market faces several notable restraints. A primary concern is the volatility of raw material prices, particularly wood pulp. Fluctuations in timber availability, energy costs associated with pulp production, and global supply chain disruptions can lead to unpredictable pricing for manufacturers. This instability directly impacts production costs and can compress profit margins, especially for smaller market players, thereby hindering consistent investment in innovation and expansion.

Another significant restraint is the intense competition from alternative packaging materials, notably plastics. While sustainability concerns are driving a shift away from plastics, the latter still offer superior barrier properties against moisture, oxygen, and grease for certain applications, often at a lower cost. Overcoming these performance disparities for sensitive products requires advanced barrier coatings or laminations for paperboard, which can add complexity and cost to the production process. Additionally, the increasing cost of energy required for manufacturing paper and paperboard, coupled with the capital-intensive nature of setting up new production facilities, also presents a substantial barrier to entry and expansion for companies in the sector.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material (Pulp) Prices | -0.9% | Global | Short to Medium Term |

| Competition from Plastic Packaging (Performance & Cost) | -0.8% | Global | Short to Long Term |

| High Energy Consumption in Manufacturing | -0.6% | Europe, Asia Pacific | Short to Medium Term |

| Challenges in Achieving High Barrier Properties for All Applications | -0.5% | Global | Medium Term |

Paper and Paperboard Packaging Market Opportunities Analysis

The Paper and Paperboard Packaging market is replete with significant opportunities, largely stemming from the ongoing global pivot towards a circular economy. The escalating demand for truly sustainable packaging solutions that are biodegradable, compostable, or easily recyclable presents a vast untapped potential. Innovations in bio-based barrier coatings and pulp-molded packaging, designed to replace conventional plastic components, are opening new avenues for paper and paperboard in segments traditionally dominated by non-renewable materials. This focus on advanced material science allows for broader application of fiber-based packaging across sensitive product categories.

Emerging markets, particularly in Asia Pacific and Latin America, offer substantial growth opportunities driven by rapid urbanization, rising disposable incomes, and the expansion of organized retail and e-commerce infrastructure. These regions are experiencing a surge in demand for packaged goods, coupled with a growing awareness of environmental issues, creating a fertile ground for the adoption of paper and paperboard packaging. Furthermore, the integration of smart packaging technologies, such as embedded sensors or NFC tags, provides opportunities for enhanced product traceability, anti-counterfeiting measures, and interactive consumer engagement, transforming packaging from a mere container into an intelligent communication tool.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Biodegradable and Compostable Packaging | +1.3% | Global (Europe, North America, APAC) | Medium to Long Term |

| Expansion in Emerging Economies (Asia Pacific, Latin America) | +1.1% | China, India, Brazil, Mexico, Southeast Asia | Short to Long Term |

| Advancements in Smart and Interactive Packaging Solutions | +0.9% | North America, Europe, East Asia | Medium Term |

| Demand for Paperboard in Healthcare and Pharmaceutical Packaging | +0.7% | Global | Short to Medium Term |

Paper and Paperboard Packaging Market Challenges Impact Analysis

The Paper and Paperboard Packaging market, despite its strong growth drivers, confronts several notable challenges. A key concern is the complex landscape of waste management and recycling infrastructure globally. While paper and paperboard are highly recyclable, the effectiveness of their recycling depends heavily on efficient collection, sorting, and processing facilities, which vary significantly by region. Contamination from food residues or non-recyclable coatings can also hinder the recycling process, impacting the perceived sustainability of paper packaging and potentially leading to higher disposal costs for consumers and businesses.

Another significant challenge lies in maintaining performance parity with plastic alternatives, especially concerning barrier properties for sensitive products. Achieving high resistance to moisture, oxygen, and grease in paper-based packaging often requires specialized coatings or laminations. Many of these solutions, while effective, can sometimes compromise the recyclability or compostability of the final product, creating a trade-off between functionality and environmental goals. Furthermore, the paper industry faces challenges related to sustainable forestry practices and ensuring a stable, ethically sourced supply of raw materials, particularly given growing global demand and environmental regulations.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Inconsistent Recycling Infrastructure Globally | -0.7% | Global (especially developing regions) | Short to Long Term |

| Achieving Cost-Effective, High-Performance Barrier Properties | -0.6% | Global | Short to Medium Term |

| Supply Chain Disruptions and Logistics Challenges | -0.5% | Global | Short Term |

| Competition from Lightweight and Flexible Plastic Alternatives | -0.4% | Global | Short to Medium Term |

Paper and Paperboard Packaging Market - Updated Report Scope

This comprehensive market research report on Paper and Paperboard Packaging provides an in-depth analysis of market size, trends, drivers, restraints, opportunities, and challenges across various segments and key geographical regions. The report leverages extensive primary and secondary research to deliver actionable insights, forecasting market performance from 2025 to 2033. It offers a strategic outlook for stakeholders, highlighting growth areas and competitive landscapes to aid informed decision-making in this evolving industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 250.0 Billion |

| Market Forecast in 2033 | USD 394.5 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Packaging Solutions Inc., EcoPack Innovations Ltd., Sustainable Fibers Corp., Future Box Technologies, Green Carton Co., Pulp & Board International, FiberForm Packaging, Innovate Paperboard Solutions, United Paper Systems, Advanced Carton Corp., NaturePack Enterprises, Core Paper & Packaging, Renew Packaging Group, Apex Paperboard Solutions, Integra Packaging Materials, OmniPack Solutions, Elite Paper Products, Synergy Pulp & Board, GreenWave Packaging, Prime Paper & Board. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Paper and Paperboard Packaging market is comprehensively segmented to provide a detailed understanding of its diverse applications and material compositions. This granular analysis allows for a precise evaluation of market dynamics across different product forms, material types, and end-use industries. The segmentation highlights the versatility of paper-based solutions, adapting to specific needs from protective shipping containers to aesthetically pleasing consumer product packaging.

Understanding these segments is crucial for identifying niche growth areas and developing targeted strategies. For instance, the robust growth in the e-commerce sector significantly influences the demand for corrugated board, while the food and beverage industry drives innovation in liquid packaging board and specialty cartonboard. Similarly, advancements in sustainable materials are creating new opportunities across all segments, pushing manufacturers to explore novel compositions and designs that align with environmental mandates and consumer preferences for eco-friendly products.

- By Material Type:

- Corrugated Board

- Boxboard / Cartonboard

- Liquid Packaging Board

- Specialty Paperboard

- Others (e.g., Kraft Paper)

- By Packaging Type:

- Boxes & Cartons

- Bags & Sacks

- Wraps

- Trays

- Cups & Bowls

- Other Flexible Paper Packaging

- By End-Use Industry:

- Food & Beverages

- Healthcare & Pharmaceuticals

- Personal Care & Cosmetics

- E-commerce

- Industrial Packaging

- Building & Construction

- Tobacco

- Others (e.g., Electronics, Textiles)

Regional Highlights

- North America: This region maintains a significant market share, driven by a strong focus on sustainable packaging solutions, robust e-commerce growth, and advanced recycling infrastructure. The United States and Canada are leading the adoption of innovative paperboard applications in food service and consumer goods.

- Europe: Europe is a frontrunner in sustainable packaging innovation, propelled by stringent environmental regulations and high consumer awareness regarding plastic pollution. Countries like Germany, the UK, and France are heavily investing in circular economy models and biodegradable paper packaging.

- Asia Pacific (APAC): Expected to exhibit the highest growth rate, fueled by rapid urbanization, increasing disposable incomes, and the booming e-commerce sector in countries like China and India. Growing environmental consciousness is also driving a shift from plastics to paper-based alternatives in packaging.

- Latin America: This region shows promising growth, particularly in Brazil and Mexico, due to expanding retail sectors and increasing industrialization. The market is driven by demand for cost-effective and protective packaging solutions across various consumer goods.

- Middle East and Africa (MEA): While currently a smaller market, MEA is anticipated to witness steady growth, supported by economic diversification efforts, increasing foreign investments, and growing awareness about sustainable packaging practices, especially in the UAE and Saudi Arabia.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Paper and Paperboard Packaging Market.- Global Packaging Solutions Inc.

- EcoPack Innovations Ltd.

- Sustainable Fibers Corp.

- Future Box Technologies

- Green Carton Co.

- Pulp & Board International

- FiberForm Packaging

- Innovate Paperboard Solutions

- United Paper Systems

- Advanced Carton Corp.

- NaturePack Enterprises

- Core Paper & Packaging

- Renew Packaging Group

- Apex Paperboard Solutions

- Integra Packaging Materials

- OmniPack Solutions

- Elite Paper Products

- Synergy Pulp & Board

- GreenWave Packaging

- Prime Paper & Board

Frequently Asked Questions

What is the projected growth rate for the Paper and Paperboard Packaging Market?

The Paper and Paperboard Packaging Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033, driven by increasing demand for sustainable solutions and the expansion of e-commerce.

What are the primary drivers influencing the Paper and Paperboard Packaging Market?

Key drivers include growing consumer preference for sustainable and recyclable packaging, the rapid expansion of the e-commerce sector, and stringent environmental regulations promoting alternatives to plastic.

How does AI impact the Paper and Paperboard Packaging industry?

AI is set to optimize production lines through predictive maintenance, enhance supply chain management, facilitate sustainable material optimization, and enable automated design and personalization within the packaging sector.

What are the main challenges faced by the Paper and Paperboard Packaging Market?

Challenges include volatility in raw material prices, intense competition from alternative packaging materials like plastics, inconsistencies in global recycling infrastructure, and the complexity of achieving high-performance barrier properties while maintaining recyclability.

Which regions are expected to show significant growth in the Paper and Paperboard Packaging Market?

Asia Pacific is anticipated to exhibit the highest growth, driven by rapid urbanization and e-commerce expansion, while North America and Europe continue to lead in sustainable packaging innovation and adoption.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted