MEM Device, Equipment, and Material Market

MEM Device, Equipment, and Material Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705904 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

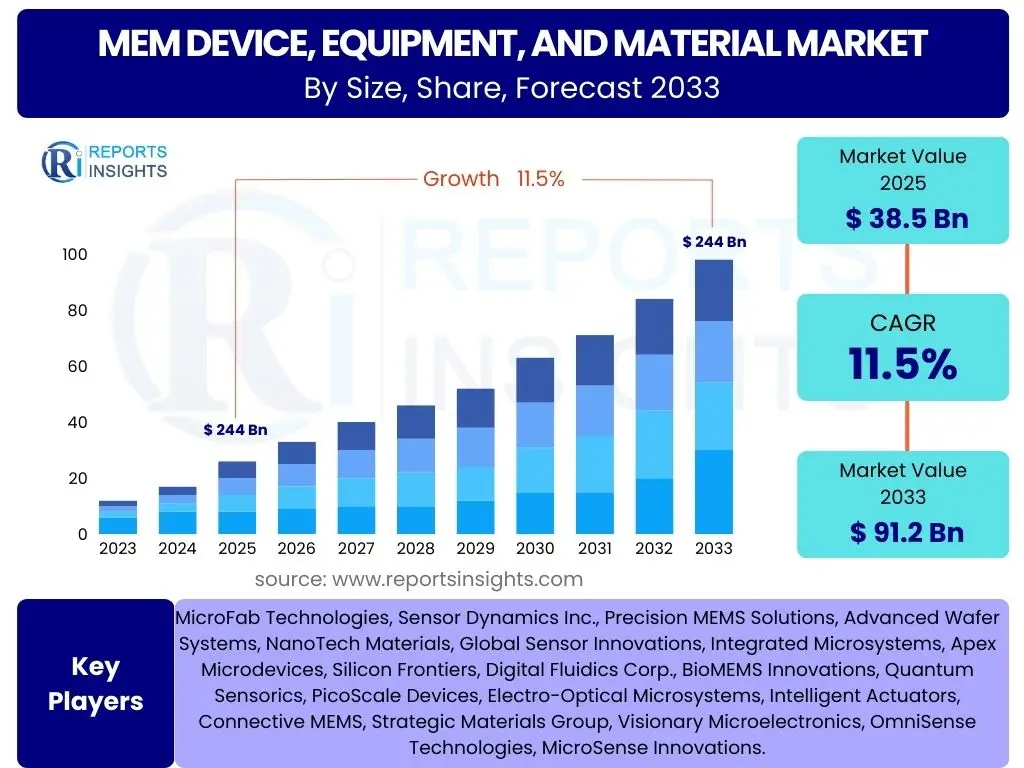

MEM Device, Equipment, and Material Market Size

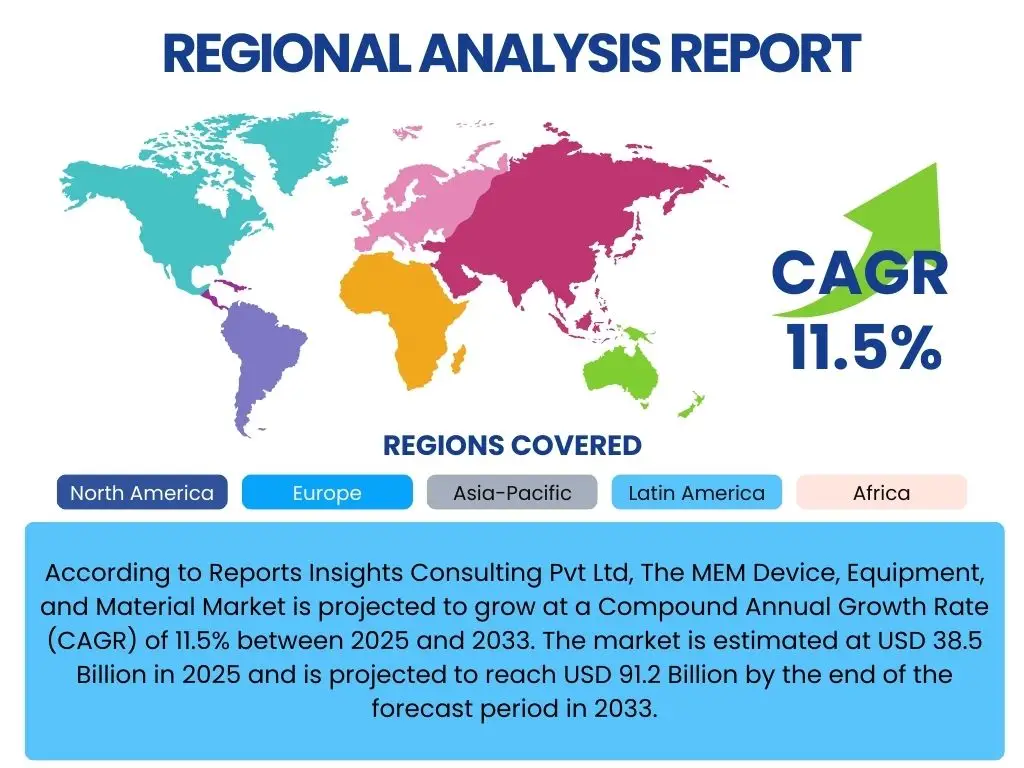

According to Reports Insights Consulting Pvt Ltd, The MEM Device, Equipment, and Material Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2025 and 2033. The market is estimated at USD 38.5 Billion in 2025 and is projected to reach USD 91.2 Billion by the end of the forecast period in 2033.

Key MEM Device, Equipment, and Material Market Trends & Insights

Common user inquiries regarding trends in the MEM Device, Equipment, and Material market frequently highlight the increasing demand for miniaturized and integrated systems, the proliferation of smart devices, and the growing adoption of MEMS across diverse industries. There is significant interest in how advanced materials and fabrication techniques are influencing performance and cost-efficiency. Users also seek to understand the impact of emerging technologies like the Internet of Things (IoT), 5G, and artificial intelligence on market dynamics, as well as the push towards more sustainable and energy-efficient MEMS solutions.

These inquiries reveal a collective expectation for continued innovation that will broaden the application scope of MEMS technology. The market is actively responding to the need for higher precision, lower power consumption, and enhanced durability in components. Furthermore, the drive towards compact, multi-functional devices is a consistent theme, prompting advancements in packaging and integration technologies. The focus extends to how these trends translate into tangible benefits for end-users and how they reshape the competitive landscape.

The convergence of various technological advancements is propelling the market forward, fostering an environment where cross-industry collaboration becomes increasingly vital. This includes partnerships between material scientists, device manufacturers, and software developers to create holistic solutions. The evolving regulatory landscape and the emphasis on device reliability and safety, particularly in critical applications like healthcare and automotive, also stand out as significant factors shaping market trends.

- Miniaturization and multi-functional integration driving device innovation.

- Proliferation of MEMS in consumer electronics and automotive sectors.

- Growth in industrial IoT and automation applications.

- Emergence of advanced materials enhancing performance and durability.

- Increased demand for energy-efficient and low-power MEMS solutions.

- Advancements in packaging technologies for complex MEMS systems.

AI Impact Analysis on MEM Device, Equipment, and Material

User questions about the impact of Artificial Intelligence (AI) on the MEM Device, Equipment, and Material domain frequently center on its potential to revolutionize design, manufacturing, and performance optimization. There is considerable interest in how AI can enhance the accuracy and reliability of MEMS devices, particularly through predictive maintenance and real-time data analysis. Users are also keen to understand AI's role in accelerating the R&D process, enabling faster prototyping, and optimizing complex fabrication steps, thereby reducing costs and improving yield.

The adoption of AI in MEMS manufacturing processes is anticipated to lead to more efficient and adaptable production lines. AI-powered algorithms can analyze vast datasets from sensors and manufacturing equipment to identify anomalies, predict failures, and fine-tune parameters, resulting in higher quality products and reduced waste. Furthermore, AI contributes to the development of 'smart' MEMS devices that can learn from their environment and adapt their functionality, opening new avenues for applications in areas like adaptive sensing and cognitive systems.

Beyond manufacturing, AI is expected to significantly influence the post-deployment phase of MEMS devices by enabling advanced data interpretation and decision-making capabilities. This includes AI-driven calibration, self-diagnosis, and enhanced sensor fusion for complex applications. The integration of AI tools promises to unlock unprecedented levels of efficiency and intelligence across the entire lifecycle of MEMS products, from initial concept to end-use, ultimately enhancing their value proposition in a highly competitive market.

- AI-driven optimization of MEMS design and simulation processes.

- Enhanced predictive maintenance and fault detection in manufacturing equipment.

- Improved yield and quality control through AI-powered process monitoring.

- Development of smart, adaptive MEMS sensors with integrated AI capabilities.

- Accelerated R&D cycles and material discovery using machine learning algorithms.

Key Takeaways MEM Device, Equipment, and Material Market Size & Forecast

Common user inquiries regarding key takeaways from the MEM Device, Equipment, and Material market size and forecast reveal a strong focus on understanding the primary growth catalysts and the resilience of the market against potential headwinds. There is a clear interest in identifying which application segments are poised for the most significant expansion and which regions will dominate future market share. Users are also eager to grasp the fundamental technologies driving innovation and the investment opportunities stemming from these trends.

The insights indicate a robust growth trajectory for the MEM Device, Equipment, and Material market, underpinned by increasing demand across diversified end-use industries such as automotive, healthcare, and consumer electronics. Miniaturization, enhanced performance, and cost-effectiveness continue to be critical factors fueling this expansion. Furthermore, the ongoing integration of MEMS with emerging technologies like IoT and AI is creating new revenue streams and extending the reach of MEMS applications into previously untapped sectors.

Despite potential challenges like supply chain vulnerabilities and high R&D expenditures, the market demonstrates strong resilience, driven by continuous innovation and strategic investments. The Asia Pacific region is expected to remain a dominant force due to its manufacturing capabilities and large consumer base, while North America and Europe will continue to lead in technological advancements and high-value applications. The competitive landscape is characterized by both established players and agile startups, fostering a dynamic environment for innovation and market penetration.

- Significant growth primarily driven by automotive, consumer electronics, and healthcare sectors.

- Asia Pacific is projected to lead market growth due to manufacturing prowess and demand.

- Technological advancements in miniaturization and integration are crucial for market expansion.

- IoT, 5G, and AI integration are opening new application avenues and driving innovation.

- High R&D investment is essential for competitive advantage and addressing market demands.

MEM Device, Equipment, and Material Market Drivers Analysis

The MEM Device, Equipment, and Material market is propelled by several robust drivers, fundamentally transforming its landscape and expanding its application horizons. The pervasive integration of sensors and actuators into everyday devices and industrial systems is a primary catalyst, driven by the escalating demand for smart, connected solutions. This includes advancements in the automotive sector, where MEMS are integral to safety systems and autonomous driving, and in consumer electronics, where they enable sophisticated functionalities in smartphones and wearables.

Another significant driver is the continuous innovation in healthcare and biotechnology, where MEMS devices facilitate precise diagnostics, drug delivery, and minimally invasive surgical tools. The pursuit of miniaturization, higher performance, and lower power consumption across industries also serves as a strong impetus, fostering research and development in novel materials and fabrication techniques. Furthermore, the growth of the Internet of Things (IoT) and Industry 4.0 initiatives necessitates a vast array of compact, intelligent sensors, directly boosting the demand for MEMS components and the equipment required to produce them.

The global shift towards energy efficiency and environmental monitoring further stimulates the market, with MEMS sensors playing a crucial role in smart grids, environmental sensing, and industrial process control. The advent of 5G technology also creates new opportunities, particularly for RF MEMS, which are essential for high-frequency communication modules. These combined forces create a synergistic effect, ensuring sustained demand and continuous evolution within the MEM Device, Equipment, and Material market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Smart Consumer Electronics | +2.5% | Global, particularly Asia Pacific (China, South Korea) | 2025-2033 |

| Growth in Automotive Electronics and ADAS | +2.0% | North America, Europe, Asia Pacific (Japan, Germany, US) | 2025-2033 |

| Advancements in Healthcare and Medical Devices | +1.8% | North America, Europe (US, Germany, Switzerland) | 2026-2033 |

| Expansion of Industrial IoT and Automation | +1.5% | Global, particularly Europe, Asia Pacific | 2025-2033 |

| Emergence of 5G Technology and Infrastructure | +1.2% | Global, particularly North America, Asia Pacific | 2027-2033 |

MEM Device, Equipment, and Material Market Restraints Analysis

Despite its significant growth potential, the MEM Device, Equipment, and Material market faces several notable restraints that could temper its expansion. One primary challenge is the high upfront capital expenditure required for establishing and maintaining MEMS fabrication facilities. The complexity of MEMS manufacturing processes, which often involve cleanroom environments and highly specialized equipment, contributes to these substantial investment costs, making market entry challenging for new players and imposing financial burdens on existing ones.

Another significant restraint is the intricate and often lengthy research and development cycles inherent in MEMS technology. Developing new MEMS devices, particularly for niche or highly regulated applications like healthcare, demands extensive testing, validation, and adherence to stringent quality standards, which can delay time-to-market and increase overall development costs. This complexity is further exacerbated by the need for multidisciplinary expertise spanning physics, materials science, electrical engineering, and mechanical engineering.

Furthermore, supply chain vulnerabilities, particularly concerning critical raw materials and specialized components, can pose a risk to market stability. Geopolitical factors, trade tensions, and unforeseen global events can disrupt the availability and pricing of essential materials, leading to production delays and increased costs. The lack of standardized manufacturing processes across different MEMS applications also presents a challenge, hindering mass production efficiencies and increasing the need for customized solutions, which can be more expensive and time-consuming to produce.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure for Fabrication Facilities | -1.5% | Global | 2025-2033 |

| Complex and Lengthy R&D Cycles | -1.2% | Global | 2025-2030 |

| Supply Chain Vulnerabilities and Material Scarcity | -1.0% | Global, particularly Asia Pacific | 2025-2028 |

| Lack of Standardization in Manufacturing Processes | -0.8% | Global | 2025-2033 |

MEM Device, Equipment, and Material Market Opportunities Analysis

The MEM Device, Equipment, and Material market is ripe with significant opportunities that promise to accelerate its growth and diversify its application base. One major area of opportunity lies in the expanding adoption of MEMS in emerging technological domains such as augmented reality (AR), virtual reality (VR), and haptic feedback systems. These applications require highly responsive and compact sensors and actuators, creating new niches for advanced MEMS solutions and driving innovation in miniaturization and integration.

Another compelling opportunity stems from the increasing demand for advanced medical diagnostics and implantable devices. The precision and biocompatibility offered by MEMS make them ideal for point-of-care testing, continuous health monitoring, and sophisticated medical interventions. The development of bio-MEMS and lab-on-a-chip technologies represents a substantial growth area, driven by aging populations and the rising prevalence of chronic diseases, requiring personalized and efficient healthcare solutions.

Furthermore, the ongoing development of smart city initiatives and the widespread deployment of 5G infrastructure are opening vast opportunities for MEMS sensors in environmental monitoring, traffic management, and smart grid applications. The integration of artificial intelligence and machine learning with MEMS data analysis also presents avenues for enhanced functionality and predictive capabilities, transforming raw sensor data into actionable insights. This continuous evolution of connected environments creates a sustained demand for intelligent, robust, and cost-effective MEMS components across various infrastructure layers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emerging Applications in AR/VR and Haptics | +1.8% | North America, Asia Pacific (US, China, Japan) | 2026-2033 |

| Growth in Bio-MEMS and Medical Diagnostics | +1.5% | Global, particularly North America, Europe | 2025-2033 |

| Expansion of Smart City and Environmental Monitoring | +1.3% | Europe, Asia Pacific, North America | 2025-2033 |

| Integration with Artificial Intelligence and Edge Computing | +1.0% | Global | 2027-2033 |

MEM Device, Equipment, and Material Market Challenges Impact Analysis

The MEM Device, Equipment, and Material market faces several critical challenges that require strategic navigation to ensure sustained growth. One prominent challenge is the increasing cost pressure from end-user industries, particularly in high-volume consumer electronics segments, where competitive pricing is paramount. Manufacturers are constantly pressured to reduce production costs while maintaining or enhancing performance, which necessitates continuous innovation in materials and fabrication processes.

Another significant challenge revolves around the complexity of integration and packaging of MEMS devices. As MEMS become more sophisticated and multi-functional, integrating them seamlessly into larger systems while ensuring robust performance and reliability in diverse operating environments becomes increasingly difficult. This often requires highly specialized packaging solutions and advanced testing methodologies, adding to the overall cost and development time.

Furthermore, the market grapples with intellectual property (IP) disputes and the need for robust IP protection. Given the highly specialized nature of MEMS technology, patent infringement and the protection of proprietary designs are critical concerns for companies. The rapid pace of technological advancements also poses a challenge, requiring continuous investment in research and development to stay competitive and prevent technological obsolescence. Finally, a persistent talent gap, particularly in skilled MEMS engineers and technicians, presents a constraint on innovation and scaling manufacturing capabilities across the industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Cost Pressure and Price Erosion | -1.5% | Global, particularly Asia Pacific | 2025-2033 |

| Complexity of Integration and Packaging | -1.2% | Global | 2025-2030 |

| Intellectual Property Protection and Disputes | -1.0% | North America, Europe | 2025-2033 |

| Skilled Workforce Shortage | -0.8% | Global | 2025-2033 |

MEM Device, Equipment, and Material Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the MEM Device, Equipment, and Material market, encompassing historical data, current market dynamics, and future projections. It offers a detailed examination of market size, growth drivers, restraints, opportunities, and key trends influencing the industry landscape. The report segments the market by device type, equipment type, material type, application, and wafer size, providing granular insights into each category. Furthermore, it includes a thorough regional analysis and profiles of leading market participants, offering a holistic view for stakeholders seeking strategic market intelligence and investment opportunities.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 38.5 Billion |

| Market Forecast in 2033 | USD 91.2 Billion |

| Growth Rate | 11.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | MicroFab Technologies, Sensor Dynamics Inc., Precision MEMS Solutions, Advanced Wafer Systems, NanoTech Materials, Global Sensor Innovations, Integrated Microsystems, Apex Microdevices, Silicon Frontiers, Digital Fluidics Corp., BioMEMS Innovations, Quantum Sensorics, PicoScale Devices, Electro-Optical Microsystems, Intelligent Actuators, Connective MEMS, Strategic Materials Group, Visionary Microelectronics, OmniSense Technologies, MicroSense Innovations. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The MEM Device, Equipment, and Material market is extensively segmented to provide a granular view of its diverse components and applications. This segmentation highlights the various technological facets and end-user industries driving market demand and innovation. Understanding these segments is crucial for stakeholders to identify high-growth areas, assess competitive landscapes, and formulate targeted market strategies, allowing for a precise understanding of where specific investments and developments are concentrated across the value chain. Each segment reflects unique market dynamics, technological requirements, and regulatory considerations.

The segmentation by device type reveals the dominance of sensors, particularly accelerometers and gyroscopes, in consumer electronics and automotive applications, while actuators and RF MEMS exhibit robust growth in industrial and telecommunications sectors. Equipment segmentation illustrates the critical role of advanced deposition and lithography tools in manufacturing precision MEMS components, with continuous innovation aimed at enhancing throughput and yield. Material type segmentation underscores the enduring importance of silicon, alongside the rising prominence of new materials like Gallium Nitride (GaN) and Silicon Carbide (SiC) for high-performance and harsh environment applications.

Application-based segmentation demonstrates the widespread utility of MEMS across pivotal industries, with automotive, consumer electronics, and healthcare emerging as leading segments due to their high adoption rates. Industrial applications, driven by IoT and automation, also represent a substantial and growing market. Furthermore, wafer size segmentation highlights the industry's progression towards larger wafer sizes (e.g., 8-inch and 12-inch) to achieve economies of scale and reduce manufacturing costs, reflecting a maturation in production capabilities and a focus on cost-efficiency.

- By Device Type: Sensors (Accelerometers, Gyroscopes, Pressure Sensors, Magnetometers, Microphones, Others), Actuators (Micropumps, Valves, Optical Switches, Others), RF MEMS (Switches, Filters, Oscillators), Microfluidics, Bio-MEMS.

- By Equipment Type: Deposition Equipment (PVD, CVD, ALD), Lithography Equipment (Photolithography, E-beam lithography), Etching Equipment (Dry Etching, Wet Etching), Dicing and Grinding Equipment, Wafer Bonding Equipment, Inspection and Metrology Equipment.

- By Material Type: Silicon, Polymers, Glass, Metals, Ceramics, Gallium Nitride (GaN), Silicon Carbide (SiC).

- By Application: Automotive (ADAS, Airbag Sensors, Tire Pressure Monitoring), Consumer Electronics (Smartphones, Wearables, Gaming Consoles), Healthcare (Medical Implants, Drug Delivery, Diagnostics), Industrial (Automation, Robotics, IoT Devices), Aerospace & Defense (Navigation, Pressure Sensing), Telecommunications (5G Infrastructure, Optical Networking).

- By Wafer Size: 6-inch, 8-inch, 12-inch, Others.

Regional Highlights

- North America: This region is a powerhouse for MEMS research and development, particularly in advanced applications like aerospace and defense, medical devices, and high-end industrial sensors. The presence of leading technology companies and robust government funding for R&D fuels innovation. Strong adoption of IoT and AI technologies further drives demand for sophisticated MEMS solutions.

- Europe: Characterized by a strong automotive industry and significant investments in Industry 4.0 initiatives, Europe is a crucial market for MEMS devices, equipment, and materials. Countries like Germany and France are at the forefront of automotive MEMS and industrial automation. Strict environmental regulations also drive demand for MEMS sensors in environmental monitoring and smart cities.

- Asia Pacific (APAC): APAC is expected to be the fastest-growing region, primarily driven by its dominance in consumer electronics manufacturing and the rapid expansion of its automotive sector. Countries like China, South Korea, and Japan are major hubs for MEMS production and consumption. The increasing disposable income and growing demand for smart devices further contribute to market expansion.

- Latin America: While a smaller market, Latin America shows promising growth, particularly in the automotive and industrial sectors, as manufacturing capabilities expand and digital transformation initiatives gain traction. Investments in smart infrastructure and the adoption of consumer electronics contribute to the rising demand for MEMS.

- Middle East and Africa (MEA): This region is experiencing nascent growth, primarily fueled by investments in smart city projects, oil and gas exploration (requiring robust industrial MEMS), and improving healthcare infrastructure. As digitalization accelerates, the demand for MEMS in various applications is expected to increase steadily.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the MEM Device, Equipment, and Material Market.- MicroFab Technologies

- Sensor Dynamics Inc.

- Precision MEMS Solutions

- Advanced Wafer Systems

- NanoTech Materials

- Global Sensor Innovations

- Integrated Microsystems

- Apex Microdevices

- Silicon Frontiers

- Digital Fluidics Corp.

- BioMEMS Innovations

- Quantum Sensorics

- PicoScale Devices

- Electro-Optical Microsystems

- Intelligent Actuators

- Connective MEMS

- Strategic Materials Group

- Visionary Microelectronics

- OmniSense Technologies

- MicroSense Innovations

Frequently Asked Questions

Analyze common user questions about the MEM Device, Equipment, and Material market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the MEM Device, Equipment, and Material Market?

The MEM Device, Equipment, and Material Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2025 and 2033, reaching an estimated USD 91.2 Billion by the end of the forecast period.

Which factors are primarily driving the MEM Device, Equipment, and Material Market?

The market is primarily driven by increasing demand for miniaturized and smart devices in consumer electronics, significant growth in automotive electronics and ADAS, advancements in healthcare and medical devices, and the expansion of industrial IoT and automation applications.

What are the main challenges faced by the MEM Device, Equipment, and Material Market?

Key challenges include high capital expenditure for fabrication facilities, complex and lengthy R&D cycles, vulnerabilities in the supply chain for critical materials, intense cost pressure from end-user industries, and a shortage of skilled labor in MEMS engineering.

How is Artificial Intelligence (AI) impacting the MEM Device, Equipment, and Material Market?

AI is significantly impacting the market by optimizing MEMS design and simulation, enhancing predictive maintenance in manufacturing, improving quality control, enabling the development of smart and adaptive MEMS devices, and accelerating R&D through machine learning.

Which region is expected to lead the MEM Device, Equipment, and Material Market growth?

The Asia Pacific region is expected to lead market growth, driven by its robust consumer electronics manufacturing capabilities, rapid expansion of the automotive sector, and increasing adoption of smart devices and industrial automation across countries like China, South Korea, and Japan.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted