Mobile Phone Battery Anode Material Market

Mobile Phone Battery Anode Material Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701081 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

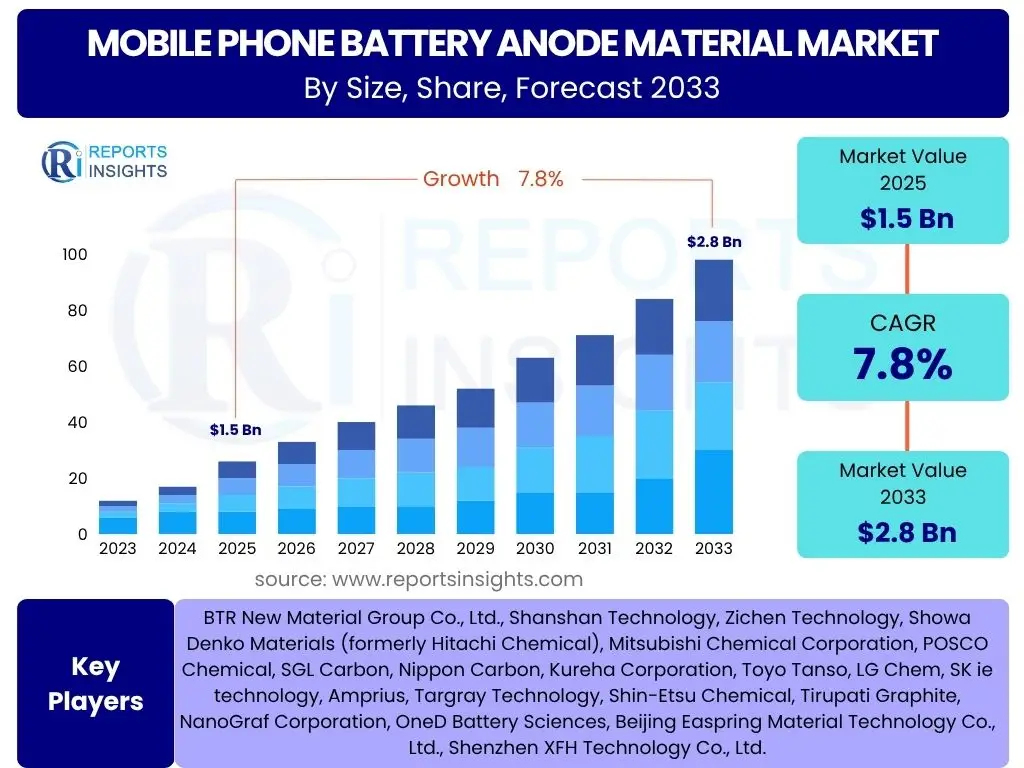

Mobile Phone Battery Anode Material Market Size

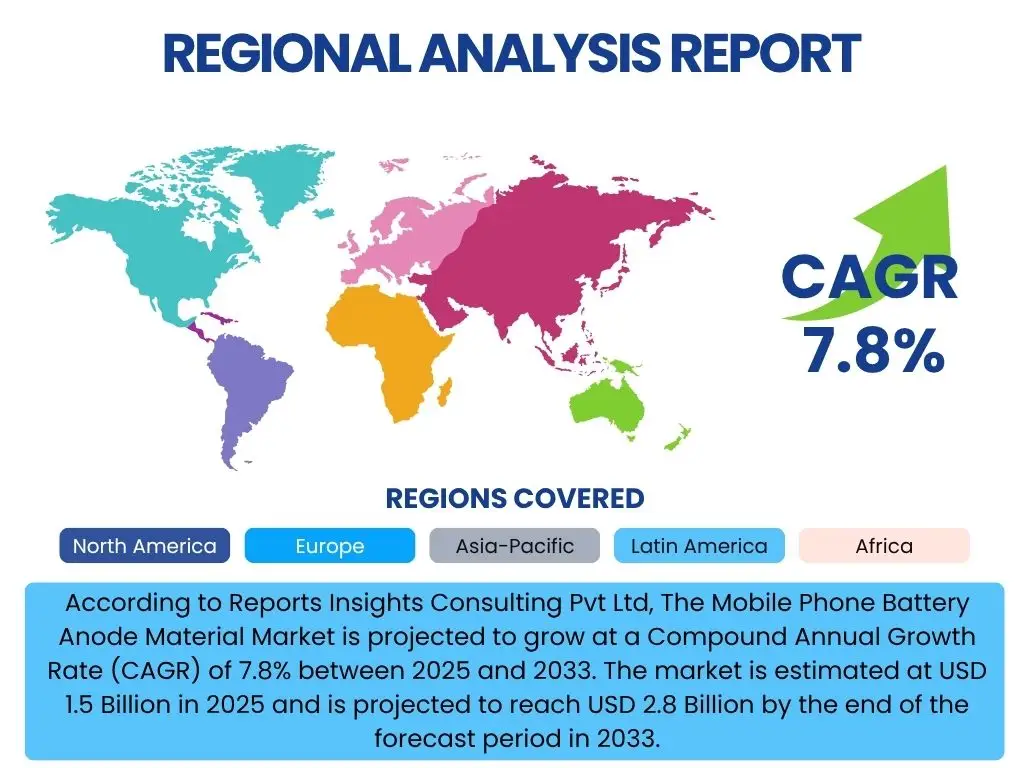

According to Reports Insights Consulting Pvt Ltd, The Mobile Phone Battery Anode Material Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 1.5 Billion in 2025 and is projected to reach USD 2.8 Billion by the end of the forecast period in 2033.

Key Mobile Phone Battery Anode Material Market Trends & Insights

The Mobile Phone Battery Anode Material market is witnessing transformative trends driven by the relentless pursuit of higher energy density, faster charging capabilities, and enhanced safety. User queries frequently revolve around the adoption of next-generation materials and their impact on battery performance and longevity. There is a clear interest in understanding how sustainable practices and supply chain resilience are shaping the material landscape, alongside the technological advancements in anode chemistry. The market is moving towards more sophisticated material compositions to meet the evolving demands of modern smartphones and other mobile devices, emphasizing performance and environmental responsibility.

Key insights indicate a significant shift from traditional graphite towards advanced materials like silicon-based composites, which offer superior energy storage capacity. Furthermore, the integration of innovative manufacturing processes and the exploration of novel material structures are critical for achieving breakthroughs in fast charging and cycle life. The industry is also increasingly focused on optimizing material costs and securing diverse supply chains to mitigate geopolitical risks and ensure stable production. This comprehensive evolution underscores a dynamic market poised for substantial innovation and growth.

- Shift Towards Silicon-Based Anodes: Significant research and development are focused on silicon-carbon composite anodes due to their higher theoretical specific capacity compared to traditional graphite, promising extended battery life and smaller form factors for mobile devices. This trend addresses consumer demand for longer-lasting charges and thinner device profiles.

- Demand for Fast Charging Compatibility: The rising consumer expectation for rapid charging capabilities is driving the development of anode materials that can withstand high current densities without degradation. This leads to innovations in material morphology and surface coatings, ensuring battery integrity even with rapid power delivery.

- Enhanced Safety Features: Ongoing efforts to improve battery safety, including thermal stability and prevention of dendrite formation, are influencing anode material design and selection. As energy densities increase, the imperative for safer battery operation becomes even more critical for widespread adoption.

- Sustainable Sourcing and Recycling Initiatives: Increasing environmental awareness and regulatory pressures are prompting manufacturers to explore more sustainable sourcing of raw materials and to invest in recycling technologies for end-of-life battery components, including anode materials. This ensures environmental responsibility throughout the product lifecycle.

- Integration with Advanced Battery Architectures: Research into solid-state batteries and other next-generation battery designs is influencing the long-term material roadmap for anodes. This focuses on ensuring compatibility and optimal performance within these novel systems, which could revolutionize battery technology in the coming decade.

AI Impact Analysis on Mobile Phone Battery Anode Material

The impact of Artificial Intelligence (AI) on the Mobile Phone Battery Anode Material market is a topic of growing interest among users, with common questions centering on how AI can accelerate material discovery, optimize manufacturing processes, and enhance quality control. Users are keen to understand if AI can reduce the time and cost associated with developing new anode chemistries and how it might lead to more efficient production of these critical components. The consensus suggests AI's potential to revolutionize various stages of the anode material lifecycle, from initial research to large-scale deployment.

AI's role extends beyond just research and development, influencing supply chain resilience and predictive maintenance for manufacturing equipment. By analyzing vast datasets, AI algorithms can identify optimal material compositions, predict performance characteristics, and detect manufacturing anomalies with high precision, thereby improving product consistency and reducing waste. Furthermore, AI can aid in the simulation of material behavior under various operating conditions, accelerating the validation process and ensuring the reliability of new anode designs before physical prototyping. This integration of AI promises to drive significant efficiencies and innovation within the sector, shortening development cycles and enhancing product quality.

- Accelerated Material Discovery and Design: AI algorithms can rapidly screen millions of potential material candidates and predict their properties, significantly reducing the time and cost associated with discovering novel anode materials with superior performance characteristics. This computational approach allows for faster iteration and identification of promising chemistries.

- Optimized Manufacturing Processes: AI-driven process control systems can monitor and adjust parameters in real-time during anode material production, leading to improved yield rates, reduced energy consumption, and enhanced material consistency and quality. This minimizes defects and maximizes output efficiency.

- Enhanced Quality Control and Defect Detection: Machine learning models can analyze imaging data from production lines to identify microscopic defects or inconsistencies in anode materials that might be missed by human inspection. This ensures higher product reliability and safety by catching flaws early in the manufacturing process.

- Predictive Maintenance for Production Equipment: AI can predict equipment failures in anode material manufacturing facilities by analyzing operational data, enabling proactive maintenance. This minimizes downtime, extends equipment lifespan, and ensures uninterrupted production lines.

- Supply Chain Optimization and Risk Management: AI tools can analyze complex global supply chain data to optimize logistics, predict potential disruptions, and identify alternative sourcing options for critical raw materials used in anode production. This enhances overall supply chain resilience and reduces vulnerability to external shocks.

Key Takeaways Mobile Phone Battery Anode Material Market Size & Forecast

Answering common user questions about the Mobile Phone Battery Anode Material market forecast reveals a strong consensus on sustained growth, primarily fueled by the continuous evolution of smartphone technology and increasing global adoption rates. Users are particularly interested in understanding the primary drivers behind this expansion, the emerging material innovations that will define future batteries, and the overall market trajectory. The insights underscore a dynamic market where performance enhancements and sustainability considerations are paramount to long-term success.

The market is poised for robust expansion, driven by the persistent demand for longer battery life and faster charging capabilities in mobile devices. Furthermore, the transition towards advanced anode materials like silicon-carbon composites is a critical factor influencing market valuation and growth projections. The forecast indicates that while traditional graphite will maintain a significant share, the incremental adoption of next-generation materials will be key to unlocking new levels of battery performance and market value. Overall, the market is characterized by technological innovation, strategic material shifts, and a strong commitment to meeting evolving consumer demands and environmental responsibilities.

- Strong Growth Trajectory: The market is projected to exhibit a healthy Compound Annual Growth Rate (CAGR), indicating a robust expansion driven by global smartphone proliferation and the continuous upgrade cycle for mobile devices, especially in emerging economies.

- Material Innovation as a Core Driver: The transition from conventional graphite to high-capacity silicon-based and composite anode materials is a fundamental growth propeller. These innovations enable enhanced energy density, faster charging, and improved overall battery performance.

- Increasing Investment in Research & Development: Significant investments in research and development for novel anode chemistries and advanced manufacturing processes are expected to accelerate market innovation and diversify product offerings, fostering a competitive landscape.

- Sustainability and Supply Chain Focus: Growing emphasis on environmentally responsible sourcing, production, and recycling practices for anode materials will increasingly influence market dynamics and strategic partnerships. This ensures a greener footprint throughout the value chain.

- Global Market Expansion: Emerging economies and increasing smartphone penetration in developing regions will contribute significantly to the overall market size and demand for mobile phone battery anode materials. This geographical expansion provides new avenues for market growth.

Mobile Phone Battery Anode Material Market Drivers Analysis

The Mobile Phone Battery Anode Material market is primarily propelled by several key factors that collectively foster its expansion. These drivers are rooted in the ever-evolving landscape of consumer electronics, particularly the smartphone industry, which consistently demands higher performance and greater efficiency from its power sources. Innovations in battery technology, coupled with the relentless pursuit of superior user experience, directly influence the demand for advanced anode materials.

Beyond direct consumer demand, broader technological advancements and strategic industrial shifts also play a pivotal role. The drive towards faster charging, longer battery life, and enhanced safety features in mobile devices necessitates continuous improvement and material innovation in anode components. This strong demand-side pull, combined with technological pushes from material science, creates a robust environment for market growth, encouraging both established players and new entrants to invest in next-generation anode solutions that can meet future performance benchmarks.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Smartphone Adoption | +2.1% | Asia Pacific (China, India), Latin America, Africa | 2025-2033 |

| Demand for Higher Energy Density Batteries | +1.8% | Global, particularly developed markets (North America, Europe, East Asia) | 2025-2033 |

| Technological Advancements in Anode Materials (e.g., Silicon-based) | +1.5% | Global, especially R&D hubs (USA, Japan, South Korea, Germany, China) | 2025-2033 |

| Consumer Preference for Faster Charging Solutions | +1.2% | Global | 2025-2030 |

| Growing Miniaturization of Electronic Devices | +0.8% | Global | 2025-2033 |

Mobile Phone Battery Anode Material Market Restraints Analysis

Despite significant growth prospects, the Mobile Phone Battery Anode Material market faces several notable restraints that could temper its expansion. These challenges often stem from the complex interplay of raw material availability, manufacturing sophistication, and the inherent safety considerations associated with high-performance battery components. Addressing these limitations is crucial for sustained market development and the widespread adoption of advanced anode technologies, ensuring their practical viability.

The high costs associated with research, development, and scaling up of novel materials pose a considerable barrier, particularly for smaller players lacking substantial capital. Furthermore, the global supply chain for critical raw materials remains susceptible to geopolitical tensions and price volatility, impacting production stability and overall material costs. Overcoming these restraints will require strategic investments in R&D, diversification of supply chains, and continuous innovation in manufacturing processes to ensure both cost-effectiveness and performance reliability of anode materials, mitigating potential slowdowns in market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Research and Development Costs for Novel Materials | -1.3% | Global | 2025-2033 |

| Volatility in Raw Material Prices (e.g., Graphite, Silicon) | -1.0% | Global, especially China, Brazil, Australia (key graphite sources) | 2025-2033 |

| Challenges in Scaling Up Production of Advanced Anodes | -0.9% | Global | 2025-2030 |

| Safety Concerns (e.g., Thermal Runaway, Dendrite Formation) | -0.7% | Global | 2025-2033 |

| Intense Competition from Established Graphite Suppliers | -0.5% | Asia Pacific | 2025-2033 |

Mobile Phone Battery Anode Material Market Opportunities Analysis

The Mobile Phone Battery Anode Material market presents numerous compelling opportunities for growth and innovation, driven by emerging technological advancements and evolving market demands. These opportunities are not only confined to material science breakthroughs but also extend to strategic market penetration and the adoption of sustainable practices. Capitalizing on these avenues will be crucial for market players aiming to gain a competitive edge and expand their global footprint, ensuring long-term profitability and relevance.

Significant potential lies in the continued development and commercialization of next-generation anode materials that promise superior performance characteristics, such as higher energy density and faster charging capabilities, which directly address core consumer needs. Furthermore, the increasing global emphasis on environmental sustainability opens doors for companies investing in green manufacturing processes and circular economy principles. Exploring strategic collaborations and new application areas beyond traditional mobile phones also represents a significant growth vector for the market, diversifying revenue streams and reducing reliance on a single end-use sector.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Next-Generation Anode Materials (e.g., Lithium Metal, Solid-State Anodes) | +1.9% | Global, particularly North America, Europe, East Asia | 2028-2033 |

| Expansion into New Applications Beyond Smartphones (e.g., Wearables, IoT devices) | +1.5% | Global | 2025-2033 |

| Increasing Focus on Sustainable and Eco-friendly Material Production | +1.2% | Europe, North America, Japan | 2025-2033 |

| Strategic Partnerships and Collaborations for R&D and Commercialization | +1.0% | Global | 2025-2033 |

| Untapped Markets in Developing Economies | +0.8% | Africa, Southeast Asia, South America | 2025-2033 |

Mobile Phone Battery Anode Material Market Challenges Impact Analysis

The Mobile Phone Battery Anode Material market faces several inherent challenges that demand careful navigation by industry participants. These obstacles often relate to the complex technical requirements for material performance, intense market competition, and the necessity of adhering to stringent safety and environmental standards. Successfully addressing these challenges is paramount for companies seeking to maintain competitiveness and achieve sustainable growth in this rapidly evolving sector, ensuring long-term viability.

One significant hurdle involves the intricate balance between achieving high energy density, long cycle life, and acceptable safety profiles for new anode materials, as these properties can often be mutually exclusive. Furthermore, the intellectual property landscape is highly complex, with numerous patents potentially limiting new entrants or innovations without significant licensing agreements. Ensuring cost-effective production while maintaining rigorous quality control standards also presents a continuous challenge, requiring advanced manufacturing techniques and robust testing protocols. Navigating these complexities requires robust R&D, strong supply chain management, and a deep understanding of global regulatory frameworks.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving a Balance Between Energy Density, Cycle Life, and Safety | -1.2% | Global | 2025-2033 |

| Complex Intellectual Property Landscape and Patent Barriers | -1.0% | Global, particularly key innovation hubs | 2025-2033 |

| Stringent Regulatory and Environmental Compliance Requirements | -0.8% | Europe, North America, Japan | 2025-2033 |

| Maintaining Cost-Effectiveness Amidst Material Innovations | -0.7% | Global | 2025-2033 |

| Technological Obsolescence Due to Rapid Innovation Cycle | -0.5% | Global | 2025-2033 |

Mobile Phone Battery Anode Material Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Mobile Phone Battery Anode Material market, segmenting it by material type, application, manufacturing process, purity level, and end-user. It offers detailed insights into market dynamics, including drivers, restraints, opportunities, and challenges, along with a thorough regional analysis. The report covers historical data from 2019 to 2023 and provides forecasts up to 2033, enabling stakeholders to make informed strategic decisions and understand the evolving landscape of anode materials for mobile phone batteries. This scope ensures a holistic understanding of the market's past performance, current state, and future potential.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.5 Billion |

| Market Forecast in 2033 | USD 2.8 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | BTR New Material Group Co., Ltd., Shanshan Technology, Zichen Technology, Showa Denko Materials (formerly Hitachi Chemical), Mitsubishi Chemical Corporation, POSCO Chemical, SGL Carbon, Nippon Carbon, Kureha Corporation, Toyo Tanso, LG Chem, SK ie technology, Amprius, Targray Technology, Shin-Etsu Chemical, Tirupati Graphite, NanoGraf Corporation, OneD Battery Sciences, Beijing Easpring Material Technology Co., Ltd., Shenzhen XFH Technology Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Mobile Phone Battery Anode Material market is comprehensively segmented to provide a granular view of its diverse components, offering insights into various material types, applications, and manufacturing processes. This detailed segmentation allows stakeholders to identify specific growth areas and understand the evolving preferences within the industry. By dissecting the market into these categories, the report highlights key sub-segments that are driving innovation and market share shifts, from the foundational material compositions to their end-use applications in a wide array of mobile devices.

Each segment holds unique dynamics influenced by technological advancements, regulatory environments, and consumer demands. For instance, the transition towards silicon-based anodes signifies a major shift in material composition, while the proliferation of smartwatches and other wearables expands the application landscape beyond traditional smartphones. Understanding these segment-specific trends is crucial for market participants to tailor their strategies, invest in promising technologies, and effectively penetrate niche markets within the broader mobile phone battery ecosystem, ultimately driving market growth and competitive advantage.

- By Material Type: This segment examines the various chemistries used for anode materials, including established graphite (natural and synthetic) and emerging high-capacity materials like silicon-based composites (e.g., silicon-carbon, silicon nanowires, silicon oxide) and lithium titanate (LTO). It also includes other experimental materials that are under development for future applications.

- By Application: This segmentation covers the end-use devices for which these anode materials are primarily designed, encompassing the core segments of smartphones, feature phones, and tablets. Furthermore, it includes the rapidly growing categories of wearable devices (such as smartwatches and fitness trackers) and other portable electronic devices like laptops and portable gaming consoles.

- By Manufacturing Process: This segment focuses on the different techniques employed in the production of anode materials, such as carbonization and graphitization for graphite-based materials, and various coating technologies (e.g., carbon coating, metal oxide coating) used to enhance the performance and stability of both traditional and novel materials. It also includes sintering and mechanical alloying processes for specialized anode compounds.

- By Purity Level: Anode materials are categorized based on their purity, which directly impacts battery performance and cost. This includes high purity materials, typically used in premium and high-performance batteries where stringent quality and maximum efficiency are required, and standard purity materials for general and cost-sensitive applications.

- By End-User: This segment distinguishes between original equipment manufacturers (OEMs) who integrate these materials directly into new battery cells for their devices during initial production, and the aftermarket, which includes replacement battery manufacturers and repair services catering to consumer needs after initial purchase.

Regional Highlights

- Asia Pacific (APAC): This region unequivocally dominates the Mobile Phone Battery Anode Material market, primarily driven by the presence of major smartphone manufacturers and battery cell producers in countries like China, South Korea, and Japan. India and Southeast Asian nations are also experiencing significant growth in smartphone adoption and manufacturing, further fueling demand. The region benefits from robust manufacturing infrastructure, extensive supply chains, and substantial investments in battery R&D, particularly in next-generation anode materials. China, in particular, is a global leader in both production and consumption of anode materials, especially synthetic graphite and increasingly, silicon-based anodes.

- North America: Characterized by strong innovation and a focus on advanced battery technologies, North America is a significant market for high-performance anode materials, including silicon-based solutions. The region has a strong research and development ecosystem, with numerous startups and academic institutions working on next-generation battery chemistries aimed at improving energy density and safety. Demand is driven by premium smartphone segments and the increasing adoption of wearable devices, alongside a growing emphasis on domestic battery manufacturing and supply chain resilience to reduce reliance on foreign imports.

- Europe: This region is increasingly focused on sustainable and ethically sourced anode materials, driven by stringent environmental regulations and a growing commitment to circular economy principles. Countries like Germany, France, and the Scandinavian nations are investing heavily in battery gigafactories and related material research, aiming to build a strong domestic battery value chain. While not a primary mobile phone manufacturing hub, Europe plays a critical role in advanced material development, particularly for higher-value, specialized anode applications and cutting-edge recycling technologies for battery components.

- Latin America: This region presents a growing market opportunity, largely due to increasing smartphone penetration and improving economic conditions in countries like Brazil, Mexico, and Argentina. While local manufacturing of anode materials and battery cells is currently limited, the rising demand for mobile phone batteries, and consequently their components, is steadily increasing. The market here is primarily driven by consumer electronics consumption and relies heavily on imports from Asia Pacific, indicating potential for future localized investment.

- Middle East and Africa (MEA): The MEA region is an emerging market for mobile phone battery anode materials, propelled by rapid urbanization and rising smartphone adoption rates across various countries, particularly in densely populated areas. Economic diversification efforts and improving digital infrastructure are contributing to increased demand for mobile devices. Although the market is currently smaller compared to developed regions, it holds substantial long-term growth potential as mobile connectivity continues to expand across the continent, leading to higher consumption of portable electronic devices.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Mobile Phone Battery Anode Material Market.- BTR New Material Group Co., Ltd.

- Shanshan Technology

- Zichen Technology

- Showa Denko Materials (formerly Hitachi Chemical)

- Mitsubishi Chemical Corporation

- POSCO Chemical

- SGL Carbon

- Nippon Carbon

- Kureha Corporation

- Toyo Tanso

- LG Chem

- SK ie technology

- Amprius

- Targray Technology

- Shin-Etsu Chemical

- Tirupati Graphite

- NanoGraf Corporation

- OneD Battery Sciences

- Beijing Easpring Material Technology Co., Ltd.

- Shenzhen XFH Technology Co., Ltd.

Frequently Asked Questions

Analyze common user questions about the Mobile Phone Battery Anode Material market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a mobile phone battery anode material?

A mobile phone battery anode material is a key component within lithium-ion batteries that serves as the negative electrode. During discharge, lithium ions are released from the anode and travel to the cathode, creating an electric current. Conversely, during charging, lithium ions re-enter and are stored within the anode's porous structure. The material's specific properties, such as its structure and composition, directly influence the battery's overall capacity, charging speed, and long-term lifespan.

Why is anode material important for mobile phone batteries?

The anode material is crucial because it largely dictates several critical performance parameters of the battery, including its energy density (how much charge it can hold), power output (how quickly it can deliver energy), and cycle life (how many charge-discharge cycles it can withstand). Superior anode materials enable the design of smaller, lighter batteries that offer longer operational times and faster charging capabilities, which are indispensable features for modern mobile devices and meet increasing consumer demands for performance.

What are the primary types of anode materials used in mobile phone batteries?

Historically, graphite, in both its natural and synthetic forms, has been the predominant anode material due to its stable performance, cost-effectiveness, and reliable safety profile. However, there's a significant and growing trend towards next-generation materials like silicon-based anodes, which include silicon-carbon composites and silicon oxide. These emerging materials offer significantly higher theoretical energy storage capacity compared to graphite, promising breakthroughs in battery performance, though they present unique challenges related to volume expansion during charging and cycling.

How do advancements in anode materials impact battery life and charging speed?

Advancements in anode materials directly translate to improved battery performance across key metrics. Materials with higher energy density, such as silicon-based anodes, enable batteries to store more charge in the same physical volume, thereby extending usage time between charges. Furthermore, anode materials designed with optimized structures can facilitate faster lithium-ion intercalation and deintercalation processes, leading to significantly quicker charging times without critically compromising battery degradation or overall lifespan. These innovations are fundamental for enhancing the mobile device user experience.

What is the future outlook for mobile phone battery anode materials?

The future outlook for mobile phone battery anode materials is characterized by continued intense innovation aimed at maximizing energy density, enhancing safety features, and improving overall cost-efficiency. Research and development efforts are intensely focused on advancing silicon-dominant materials, exploring the potential of lithium metal anodes, and developing materials specifically compatible with solid-state battery technology. Moreover, sustainability, encompassing responsible sourcing, eco-friendly production, and advanced recycling techniques, will play an increasingly critical role in shaping the market, ensuring both superior performance and environmental responsibility across the entire battery lifecycle.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted