Permanent Magnet Material Market

Permanent Magnet Material Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704404 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Permanent Magnet Material Market Size

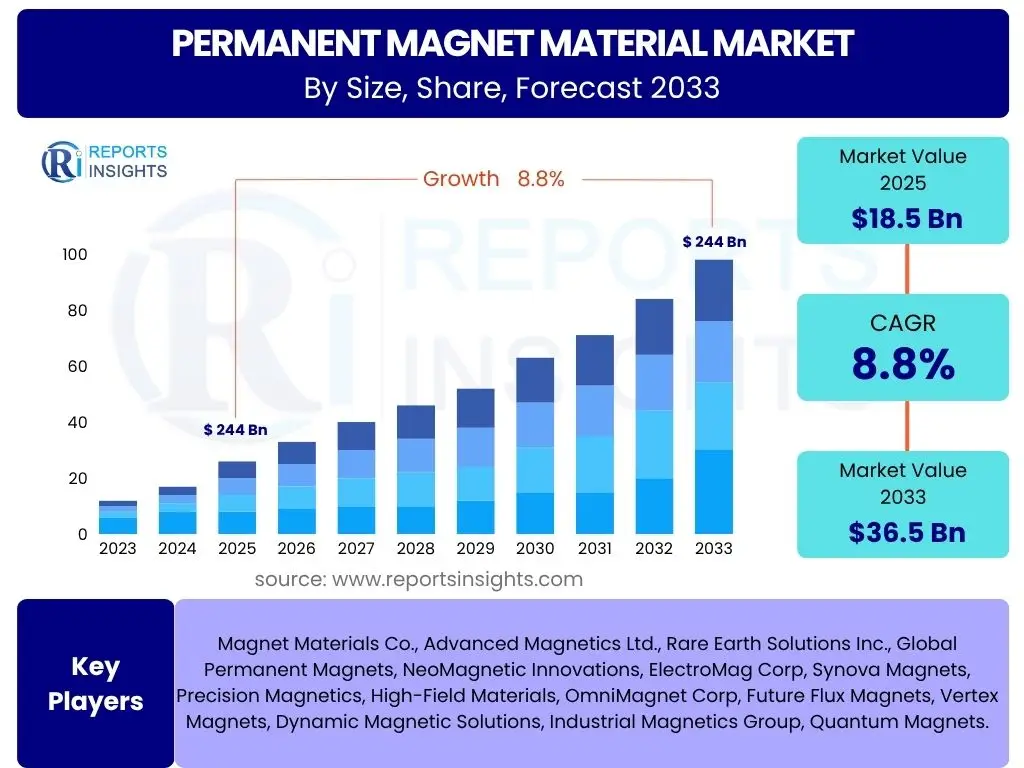

According to Reports Insights Consulting Pvt Ltd, The Permanent Magnet Material Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.8% between 2025 and 2033. The market is estimated at USD 18.5 billion in 2025 and is projected to reach USD 36.5 billion by the end of the forecast period in 2033.

Key Permanent Magnet Material Market Trends & Insights

The permanent magnet material market is experiencing dynamic shifts driven by global advancements in technology and increasing environmental consciousness. A primary trend involves the sustained surge in demand for high-performance magnets, particularly Neodymium Iron Boron (NdFeB), fueled by the accelerated adoption of electric vehicles (EVs) and renewable energy systems. Consumers and industries alike are seeking more efficient and compact power solutions, directly impacting material specifications and manufacturing processes. Furthermore, there is a growing emphasis on material sustainability, prompting research into recycling rare earth elements and developing magnets with reduced environmental footprints.

Another significant insight pertains to the ongoing innovation in magnet design and composition. Manufacturers are increasingly exploring alternatives to traditional rare earth-based magnets, such as ferrite magnets, for specific applications where cost-effectiveness and temperature stability are prioritized over peak magnetic strength. This diversification of material use helps mitigate risks associated with raw material supply chain volatility and geopolitical dependencies. The trend towards miniaturization in electronics and medical devices also necessitates the development of smaller, yet equally powerful, magnetic solutions, driving advancements in material science and precision manufacturing techniques.

Moreover, the market is witnessing increased regionalization of supply chains, with countries aiming to establish domestic production capabilities for strategic materials. This trend is a response to recent global supply disruptions and geopolitical tensions, fostering investment in local mining, refining, and manufacturing facilities. The integration of advanced manufacturing technologies, including additive manufacturing and advanced sintering processes, is also gaining traction, promising to enhance production efficiency, reduce waste, and enable more complex magnet geometries tailored to specific industrial requirements.

- Accelerated adoption of electric vehicles and hybrid electric vehicles.

- Expansion of renewable energy infrastructure, particularly wind turbines.

- Miniaturization and increasing sophistication of consumer electronics.

- Growing emphasis on sustainable sourcing and recycling of rare earth elements.

- Advancements in magnetic material research and development, including non-rare earth alternatives.

- Increasing application in industrial automation and robotics.

- Development of regionalized and resilient supply chains.

AI Impact Analysis on Permanent Magnet Material

The integration of Artificial Intelligence (AI) and Machine Learning (ML) is poised to significantly revolutionize the permanent magnet material sector by enhancing various stages of the value chain. Users frequently inquire about AI's potential to optimize material discovery, improve manufacturing efficiency, and streamline supply chain management. AI algorithms can rapidly analyze vast datasets of material properties, accelerating the identification of novel compositions with superior magnetic characteristics. This capability reduces the time and cost associated with traditional trial-and-error experimentation, enabling faster innovation cycles and the development of next-generation magnetic materials tailored for specific high-performance applications, such as advanced motors and sensors.

In manufacturing, AI-driven predictive analytics can optimize production parameters, leading to improved yield rates and reduced waste. For instance, machine learning models can monitor real-time sensor data from sintering processes to predict defects or deviations, allowing for proactive adjustments and ensuring consistent product quality. This level of precision and control is critical for producing high-grade permanent magnets, which require stringent material purity and structural integrity. Furthermore, AI can assist in automating complex quality control procedures, identifying microscopic flaws that might be missed by human inspection, thereby enhancing overall product reliability.

Beyond material science and production, AI offers substantial benefits in demand forecasting and supply chain resilience. By analyzing market trends, economic indicators, and geopolitical developments, AI models can provide more accurate predictions of future demand for various permanent magnet types, helping manufacturers optimize inventory levels and production schedules. This predictive capability is particularly valuable in a market often susceptible to raw material price volatility and supply chain disruptions. AI can also facilitate better resource allocation and logistics, ensuring a more efficient and responsive global supply network for critical permanent magnet materials, addressing user concerns about market stability and material availability.

- Accelerated material discovery and optimization through AI-driven simulations.

- Enhanced manufacturing precision and efficiency via predictive analytics and process control.

- Improved demand forecasting and inventory management for raw materials and finished products.

- Optimization of supply chain logistics and increased resilience against disruptions.

- Automated quality control and defect detection systems for higher product reliability.

Key Takeaways Permanent Magnet Material Market Size & Forecast

The permanent magnet material market is set for robust expansion, primarily propelled by global electrification trends and advancements in high-tech industries. A key takeaway from the market size and forecast is the undeniable impact of the electric vehicle sector, which acts as a foundational driver for growth, particularly for high-energy density magnets like NdFeB. Stakeholders need to recognize that sustained investment in EV infrastructure and manufacturing directly translates into increased demand for these specialized materials. Furthermore, the burgeoning renewable energy sector, especially wind power, continues to underpin market expansion, necessitating reliable and efficient magnetic solutions for turbine generators.

Another crucial insight is the growing imperative for supply chain diversification and resilience. Users and industry participants frequently inquire about the stability of raw material supply, given the geopolitical concentration of rare earth element mining and processing. This concern highlights a strategic shift towards exploring alternative material compositions and developing localized processing capabilities to mitigate risks. The forecast indicates that companies capable of ensuring a stable and ethical supply of materials, potentially through recycling initiatives or diversified sourcing, will gain a significant competitive advantage and address a core market vulnerability.

Finally, the market's future growth is not solely dependent on volume but also on technological innovation. The forecast emphasizes the increasing sophistication of applications, from miniaturized electronics to advanced medical devices, demanding magnets with superior performance characteristics, including higher temperature resistance and improved corrosion resistance. This suggests that market players focusing on research and development, particularly in areas like additive manufacturing for complex magnet geometries and novel non-rare earth magnet formulations, are well-positioned for long-term success. The market is evolving towards a more technologically driven and sustainably oriented landscape, requiring strategic foresight from all participants.

- Significant growth driven by Electric Vehicle (EV) adoption and renewable energy expansion.

- Increasing focus on supply chain diversification and raw material security.

- Technological advancements in magnet materials and manufacturing processes are critical for future demand.

- Asia Pacific will remain the largest market, but other regions are showing accelerated growth due to localization efforts.

- Sustainability and recycling initiatives are becoming increasingly important for industry players.

Permanent Magnet Material Market Drivers Analysis

The permanent magnet material market's expansion is fundamentally propelled by several potent macro and microeconomic factors. A primary driver is the accelerating global shift towards electrification across various sectors, most notably in automotive with the widespread adoption of electric and hybrid vehicles. These vehicles rely heavily on high-performance permanent magnets for their motors, which demand significant magnetic strength and efficiency to achieve extended range and superior performance. This automotive transformation alone accounts for a substantial portion of the demand surge, pushing manufacturers to innovate and scale production.

Concurrently, the global push for renewable energy sources, particularly wind power generation, represents another critical growth catalyst. Wind turbines utilize large, powerful permanent magnets in their generators to efficiently convert wind energy into electricity. As countries commit to reducing carbon emissions and increasing their renewable energy capacity, the deployment of wind farms, both onshore and offshore, is expanding rapidly, thereby escalating the demand for high-grade permanent magnet materials. This environmental imperative combined with energy security concerns ensures sustained investment in this sector, directly benefiting the magnet market.

Furthermore, the continuous evolution and expansion of consumer electronics, industrial automation, and medical devices contribute significantly to market growth. From smartphones and laptops to robotics and MRI machines, miniaturization and enhanced functionality often necessitate compact yet powerful magnetic components. The integration of permanent magnets into these diverse applications underscores their indispensable role in modern technology, driving consistent demand across a broad spectrum of industries. These drivers collectively create a robust growth environment for the permanent magnet material market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Electric Vehicle (EV) Adoption | +1.8% | Global, particularly China, Europe, North America | 2025-2033 |

| Growth in Wind Energy Sector | +1.5% | Europe, Asia Pacific, North America | 2025-2033 |

| Industrial Automation & Robotics | +1.2% | Global, especially developed economies | 2025-2033 |

| Consumer Electronics Miniaturization | +1.0% | Asia Pacific, North America, Europe | 2025-2033 |

| Advancements in Medical Devices | +0.8% | North America, Europe, Developed Asia Pacific | 2025-2033 |

Permanent Magnet Material Market Restraints Analysis

Despite its significant growth trajectory, the permanent magnet material market faces several notable restraints that could temper its expansion. A paramount concern is the volatility and scarcity of raw materials, particularly rare earth elements like Neodymium and Dysprosium, which are crucial for high-performance magnets. The highly concentrated nature of rare earth mining and processing, predominantly in specific geopolitical regions, creates supply chain vulnerabilities and subjects prices to significant fluctuations. This dependency poses considerable risk to manufacturers, impacting production costs and long-term strategic planning, and leading to increased material costs that can be passed on to end-users.

Another significant restraint involves the stringent environmental regulations and high energy consumption associated with the mining and processing of rare earth elements. The extraction and refining processes often generate toxic waste and have substantial carbon footprints, leading to increased scrutiny from environmental agencies and public advocacy groups. Compliance with evolving environmental standards necessitates costly investments in cleaner technologies and waste management, which can impede production capacity and raise operational expenses for magnet manufacturers. These regulatory pressures could slow down the expansion of existing facilities and deter new entrants.

Furthermore, the development of alternative magnet technologies that reduce or eliminate the reliance on rare earth elements, while offering a long-term solution, can also act as a short-to-medium term restraint on the traditional market. As research progresses into ferrite magnets, alnico magnets, and other non-rare earth options, there is a potential for some market cannibalization, particularly in applications where cost or specific performance parameters allow for substitutes. The high upfront capital investment required for new production facilities, coupled with the complex intellectual property landscape surrounding advanced magnet technologies, also acts as a barrier, limiting rapid market entry and expansion for many potential players.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Price Volatility & Scarcity | -1.3% | Global, particularly Asia Pacific | 2025-2033 |

| Geopolitical Supply Chain Risks | -1.0% | Global | 2025-2033 |

| Environmental Regulations & Energy Costs | -0.8% | Europe, North America, China | 2025-2033 |

| High Research & Development Costs for Alternatives | -0.6% | Global | 2025-2030 |

Permanent Magnet Material Market Opportunities Analysis

The permanent magnet material market is rich with strategic opportunities driven by emerging technological frontiers and evolving industrial demands. A significant opportunity lies in the burgeoning field of advanced manufacturing technologies, particularly additive manufacturing (3D printing) for magnetic materials. This technology allows for the creation of complex, customized magnet geometries with enhanced magnetic properties that are difficult or impossible to achieve with traditional methods. Such precision manufacturing opens new avenues for optimized magnet performance in specialized applications like micro-robotics, high-efficiency motors, and compact sensor systems, presenting a pathway for market differentiation and premium product development.

Another key opportunity stems from the increasing global focus on circular economy principles and resource sustainability. The development and commercialization of efficient recycling technologies for rare earth elements from end-of-life products, especially from spent EV batteries and wind turbines, represent a massive untapped resource. Investing in these recycling capabilities not only provides a more stable and environmentally friendly supply of critical materials but also reduces dependence on primary mining, mitigating geopolitical risks and raw material price volatility. Companies that establish robust recycling infrastructure are poised to gain a competitive edge and appeal to environmentally conscious consumers and industries.

Furthermore, the expansion into new and niche applications offers substantial growth potential. Beyond the established automotive and wind energy sectors, permanent magnets are finding increasing utility in emerging areas such as magnetic refrigeration, maglev transportation systems, advanced medical imaging beyond MRI (e.g., targeted drug delivery), and specialized aerospace components. These high-value applications often demand custom-engineered magnets with specific performance attributes, providing opportunities for specialized manufacturers to carve out lucrative market segments. The ongoing innovation in these diverse sectors creates a fertile ground for the sustained demand and technological advancement of permanent magnet materials.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advanced Manufacturing Technologies (e.g., Additive Manufacturing) | +1.4% | Global, especially North America, Europe, Asia Pacific | 2027-2033 |

| Development of Rare Earth Recycling Technologies | +1.1% | Europe, Asia Pacific, North America | 2028-2033 |

| Emerging Applications (e.g., Magnetic Refrigeration, Maglev) | +0.9% | Global | 2026-2033 |

| Strategic Stockpiling and Diversification of Supply Chains | +0.7% | North America, Europe, Japan | 2025-2033 |

Permanent Magnet Material Market Challenges Impact Analysis

The permanent magnet material market faces distinct challenges that require strategic navigation for sustained growth and stability. A prominent challenge is the increasing geopolitical instability and trade tensions that can disrupt the global supply chain for critical rare earth elements. Given the concentrated nature of rare earth mining and processing, any geopolitical friction or trade policy shifts between key producing and consuming nations can lead to significant supply bottlenecks, price spikes, and an inability for manufacturers to meet demand. This uncertainty forces companies to seek costly and time-consuming supply diversification strategies, impacting immediate operational efficiency.

Another significant hurdle is the continuous need for research and development to address performance gaps and sustainability concerns. While advancements are being made, developing new magnet materials that match or exceed the performance of rare earth magnets while being more environmentally friendly and cost-effective remains a formidable scientific and engineering challenge. This includes improving temperature stability, corrosion resistance, and reducing the heavy rare earth content in existing high-performance magnets. The high capital expenditure and long lead times associated with such R&D efforts can strain company resources and delay market readiness of new solutions.

Furthermore, intellectual property (IP) disputes and the high cost of licensing patented technologies pose a barrier to innovation and market entry, particularly for smaller players. The complex landscape of magnet material patents can restrict the adoption of new manufacturing processes or material compositions, limiting competitive dynamics and potentially slowing down overall market progress. Additionally, the availability of a skilled workforce, specifically in advanced material science, chemical engineering, and precision manufacturing, is becoming a growing concern. The specialized nature of permanent magnet production necessitates highly trained professionals, and a shortage of such talent can hinder expansion plans and technological absorption within the industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Geopolitical Instability & Trade Restrictions | -1.5% | Global | Ongoing |

| High R&D Costs & Long Development Cycles for New Materials | -1.0% | Global | 2025-2033 |

| Intellectual Property (IP) Barriers & Licensing | -0.7% | Global | Ongoing |

| Shortage of Skilled Labor and Expertise | -0.5% | North America, Europe, Developed Asia Pacific | 2025-2033 |

Permanent Magnet Material Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Permanent Magnet Material Market, encompassing detailed market sizing, growth forecasts, and a thorough examination of key trends, drivers, restraints, and opportunities. The report segments the market by material type, application, and geographic region, offering granular insights into market dynamics across various sectors and global landscapes. It also includes an extensive competitive landscape analysis, profiling leading companies and their strategic initiatives, alongside an impact assessment of AI on the industry, providing a holistic view of the market's current state and future potential.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 36.5 Billion |

| Growth Rate | 8.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Magnet Materials Co., Advanced Magnetics Ltd., Rare Earth Solutions Inc., Global Permanent Magnets, NeoMagnetic Innovations, ElectroMag Corp, Synova Magnets, Precision Magnetics, High-Field Materials, OmniMagnet Corp, Future Flux Magnets, Vertex Magnets, Dynamic Magnetic Solutions, Industrial Magnetics Group, Quantum Magnets. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The permanent magnet material market is comprehensively segmented to provide granular insights into its diverse components and drivers. This segmentation allows for a detailed analysis of specific material types, their applications across various industries, and their regional demand patterns. Understanding these distinct segments is crucial for identifying market niches, forecasting demand, and developing targeted strategies for growth and innovation within the industry.

- By Material Type: Neodymium Iron Boron (NdFeB), Samarium Cobalt (SmCo), Ferrite, Alnico, Other Permanent Magnets.

- By Application: Automotive (EV/HEV, Conventional Vehicles), Electronics (Consumer Electronics, Industrial Electronics), Wind Energy, Medical (MRI, Medical Devices), Industrial Automation, Aerospace & Defense, Others (Consumer Goods, Research & Development).

- By Region: North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA).

Regional Highlights

- Asia Pacific (APAC): The Asia Pacific region stands as the dominant market for permanent magnet materials, primarily driven by robust manufacturing sectors in China, Japan, and South Korea. This region benefits from significant investments in electric vehicle production, expansion of renewable energy projects (especially wind power), and a booming consumer electronics industry. China, in particular, is a global leader in both the production and consumption of rare earth permanent magnets, influencing global supply chains and price dynamics. The region's extensive industrial base and rapid urbanization fuel continuous demand for high-performance magnets across various applications.

- North America: North America demonstrates substantial growth in the permanent magnet market, largely propelled by increasing electric vehicle adoption and significant investments in industrial automation and aerospace & defense sectors. The United States is a key market, focusing on developing domestic rare earth processing capabilities and fostering innovation in advanced magnet technologies. The region's emphasis on high-efficiency industrial motors and medical imaging equipment also contributes significantly to market demand for specialized magnetic materials, driven by stringent energy efficiency standards and technological advancements.

- Europe: Europe is a vital market for permanent magnet materials, driven by its strong commitment to renewable energy targets and the rapidly expanding European electric vehicle market. Countries like Germany, France, and the UK are major consumers due to their advanced automotive manufacturing, wind turbine production, and industrial machinery sectors. The region also actively pursues research into sustainable magnet materials and recycling technologies, aiming to reduce its reliance on external rare earth supplies and bolster its circular economy initiatives, often driven by strict environmental regulations.

- Latin America: The Latin American market for permanent magnets is experiencing steady growth, influenced by increasing industrialization and infrastructure development. Key sectors contributing to demand include automotive, particularly in Brazil and Mexico, and industrial machinery. While smaller in comparison to other major regions, opportunities exist for market penetration as local manufacturing capabilities expand and regional governments promote sustainable energy projects and industrial modernization, leading to increased demand for efficient magnetic components.

- Middle East and Africa (MEA): The MEA region is an emerging market for permanent magnet materials, with growth driven by diversification efforts away from oil-dependent economies and increasing investments in renewable energy projects. Countries like UAE and Saudi Arabia are investing heavily in smart city initiatives, industrial automation, and renewable energy infrastructure, creating new avenues for magnet applications. While currently a smaller share of the global market, the region's long-term development plans suggest promising growth potential for specialized magnetic materials in various industrial and infrastructural projects.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Permanent Magnet Material Market.- Magnet Materials Co.

- Advanced Magnetics Ltd.

- Rare Earth Solutions Inc.

- Global Permanent Magnets

- NeoMagnetic Innovations

- ElectroMag Corp

- Synova Magnets

- Precision Magnetics

- High-Field Materials

- OmniMagnet Corp

- Future Flux Magnets

- Vertex Magnets

- Dynamic Magnetic Solutions

- Industrial Magnetics Group

- Quantum Magnets

- CoreForce Magnets

- Apex Magnetic Technologies

- Eon Magnets

- Prime Magnetics

- Zenith Magnetic Solutions

Frequently Asked Questions

What are the primary types of permanent magnet materials?

The primary types of permanent magnet materials include Neodymium Iron Boron (NdFeB), Samarium Cobalt (SmCo), Ferrite (ceramic) magnets, and Alnico magnets. Each type possesses distinct magnetic properties, temperature resistances, and cost profiles, making them suitable for various applications.

Which industry is the largest consumer of permanent magnets?

The automotive industry, particularly the electric vehicle (EV) and hybrid electric vehicle (HEV) segments, is currently the largest and fastest-growing consumer of high-performance permanent magnets, primarily due to their critical role in electric motors.

How do geopolitical factors impact the permanent magnet market?

Geopolitical factors significantly impact the market due to the highly concentrated mining and processing of rare earth elements in specific regions. Trade disputes, supply chain disruptions, and export policies can lead to price volatility and supply instability for critical magnet materials.

What role does sustainability play in the permanent magnet industry?

Sustainability is increasingly crucial, focusing on reducing the environmental impact of mining, developing more energy-efficient production processes, and establishing robust recycling programs for rare earth elements from end-of-life products. This shift aims to create a more circular economy for magnet materials.

What are the emerging applications for permanent magnet materials?

Emerging applications include magnetic refrigeration, advanced medical imaging beyond traditional MRI, maglev transportation systems, sophisticated industrial robotics, and highly efficient micro-motors for precision instrumentation, driving demand for specialized and high-performance magnetic solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted