Core Material for Composite Market

Core Material for Composite Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704325 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

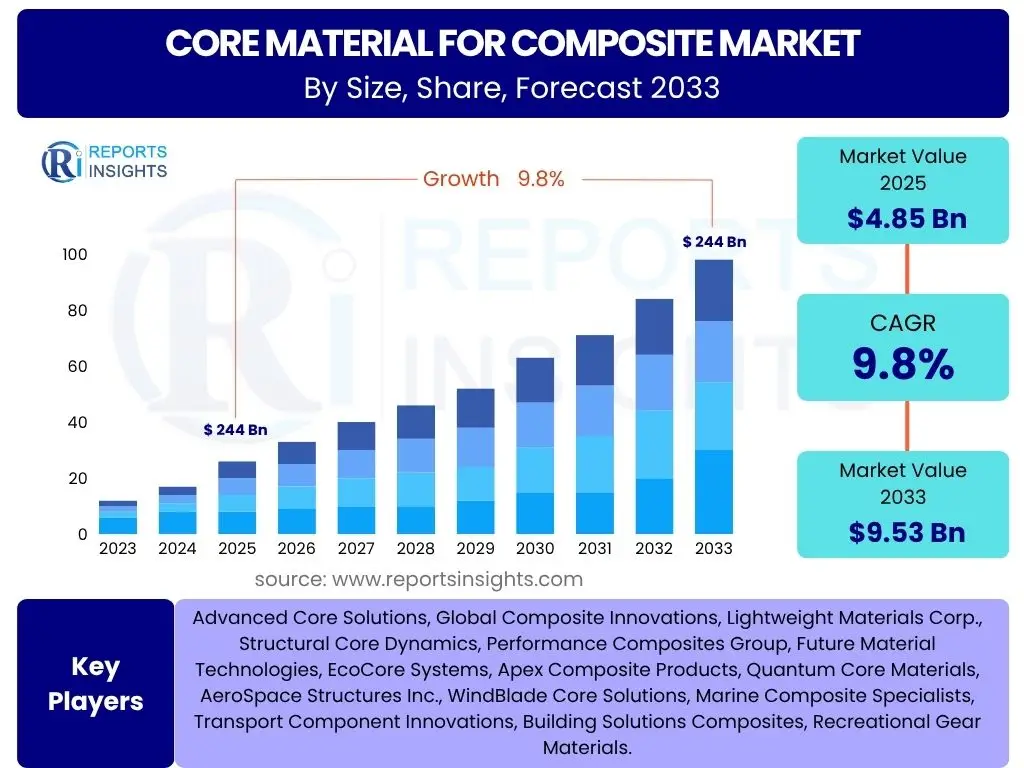

Core Material for Composite Market Size

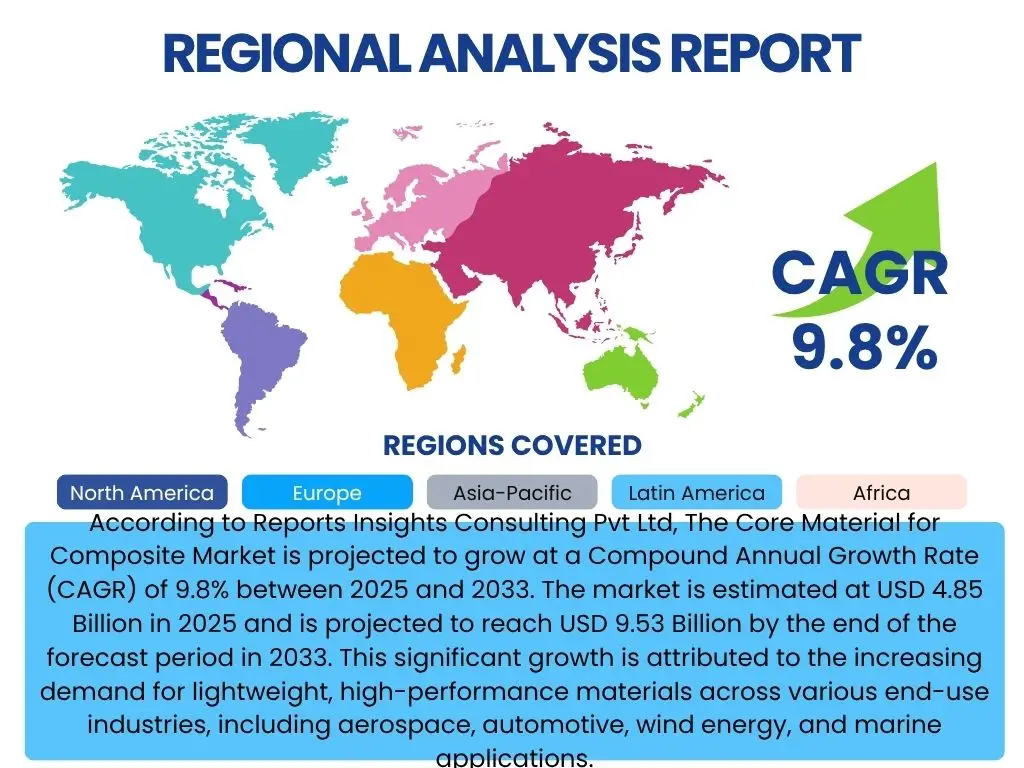

According to Reports Insights Consulting Pvt Ltd, The Core Material for Composite Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. The market is estimated at USD 4.85 Billion in 2025 and is projected to reach USD 9.53 Billion by the end of the forecast period in 2033. This significant growth is attributed to the increasing demand for lightweight, high-performance materials across various end-use industries, including aerospace, automotive, wind energy, and marine applications.

The expansion of the core material for composite market is driven by technological advancements in material science, leading to the development of more sustainable and cost-effective core materials. Innovations in manufacturing processes, such as additive manufacturing for complex geometries and automation in composite production, are further accelerating market growth. These developments enable manufacturers to produce composites with improved strength-to-weight ratios and enhanced durability, meeting the stringent performance requirements of modern applications.

Furthermore, the global emphasis on fuel efficiency and emission reduction, particularly in the transportation sector, is a key factor propelling the adoption of composite materials. Core materials play a crucial role in creating sandwich structures that offer superior stiffness and strength at minimal weight, making them indispensable for electric vehicles, aircraft, and high-speed trains. The rising demand for renewable energy infrastructure, especially wind turbine blades, also significantly contributes to the market's upward trajectory.

Key Core Material for Composite Market Trends & Insights

The Core Material for Composite market is witnessing transformative trends driven by evolving industry demands and technological advancements. Users frequently inquire about the shift towards sustainable materials, the integration of advanced manufacturing techniques, and the increasing adoption of composites in emerging applications. There is also significant interest in how performance requirements, such as enhanced fire resistance and improved mechanical properties, are shaping material development. Furthermore, the market is characterized by a drive towards cost reduction through process optimization and material innovation, alongside a focus on supply chain resilience in response to global disruptions.

The industry is actively exploring bio-based and recyclable core materials to address environmental concerns and comply with stricter regulations, marking a significant move towards a circular economy. Concurrently, the proliferation of automation and digital technologies in composite manufacturing is improving efficiency and precision. These developments collectively indicate a market moving towards more intelligent, efficient, and environmentally responsible composite solutions, with a continuous push for materials that offer superior performance characteristics while being economically viable for large-scale production across diverse sectors.

- Increased adoption of sustainable and bio-based core materials.

- Growing demand for lightweight solutions in electric vehicles and urban air mobility.

- Integration of automation and robotic technologies in composite manufacturing.

- Development of multi-functional core materials with enhanced properties (e.g., acoustic dampening, thermal insulation).

- Expansion of core material applications in construction and infrastructure.

- Focus on supply chain optimization and localized production to enhance resilience.

AI Impact Analysis on Core Material for Composite

User inquiries regarding the impact of Artificial Intelligence (AI) on the Core Material for Composite sector frequently revolve around its potential to revolutionize material design, optimize manufacturing processes, and enhance product quality and performance. There is considerable interest in how AI can accelerate the discovery of new core materials with desired properties, streamline complex simulation and testing phases, and predict material behavior under various conditions. Users also express curiosity about AI's role in predictive maintenance for composite structures and improving overall supply chain efficiency within the industry.

AI is set to significantly transform the Core Material for Composite market by enabling data-driven decision-making throughout the entire product lifecycle. From generative design and topological optimization of core structures to real-time process control in composite layup and curing, AI algorithms can identify efficiencies and improvements that are otherwise difficult for human analysis. This leads to reduced material waste, shorter development cycles, and higher-quality end products, addressing critical industry challenges related to cost, performance, and sustainability. The ability of AI to analyze vast datasets pertaining to material properties and manufacturing parameters will unlock new levels of precision and innovation in the sector.

- Accelerated material discovery and optimization through AI-driven simulations.

- Enhanced design and topological optimization for complex core geometries.

- Predictive quality control and defect detection in composite manufacturing processes.

- Optimization of production parameters and automation of manufacturing lines.

- Improved supply chain management and demand forecasting for raw materials.

- Development of smart composites with embedded sensors and AI for real-time monitoring.

Key Takeaways Core Material for Composite Market Size & Forecast

Analysis of user questions concerning the Core Material for Composite market size and forecast highlights a strong interest in understanding the primary growth catalysts, the long-term sustainability of demand, and potential investment areas. Users are keen to grasp which industries will drive the most significant demand, the role of sustainability initiatives in market expansion, and the impact of technological advancements on future market trajectories. Furthermore, there is a focus on identifying key regions poised for substantial growth and the overarching economic factors that could influence market stability and expansion over the forecast period.

The market is poised for robust expansion, primarily fueled by the imperative for lightweighting across aerospace, automotive, and renewable energy sectors to enhance performance and meet environmental regulations. Continuous innovation in material science, particularly in developing high-performance and sustainable core solutions, will be critical to sustaining this growth. Strategic investments in research and development, coupled with an agile approach to supply chain management, will enable stakeholders to capitalize on emerging opportunities and navigate potential challenges, positioning the industry for sustained profitability and increased adoption in novel applications.

- Significant market expansion driven by demand from aerospace, automotive, and wind energy.

- Strong emphasis on sustainable and recyclable core material development.

- Technological advancements in manufacturing processes enhancing market viability.

- Asia Pacific and North America poised for substantial growth.

- Increased adoption in emerging applications such as electric vehicles and urban air mobility.

Core Material for Composite Market Drivers Analysis

The Core Material for Composite market is primarily propelled by the escalating global demand for lightweight and high-strength materials, critical for enhancing fuel efficiency and reducing emissions across various industries. The aerospace and defense sectors are significant contributors, requiring advanced composites for structural components that offer superior performance characteristics at reduced weight. Similarly, the automotive industry, particularly with the rise of electric vehicles, heavily relies on core materials to optimize vehicle range and structural integrity without compromising safety.

The rapid expansion of the renewable energy sector, especially the wind energy segment, also serves as a major driver. Core materials are indispensable for manufacturing longer, more efficient wind turbine blades that can withstand extreme environmental conditions. Furthermore, advancements in composite manufacturing technologies, such as automated fiber placement and resin infusion, are making composite production more cost-effective and scalable, thereby increasing their adoption in traditional and emerging applications like infrastructure and marine vessels.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Lightweight Materials in Aerospace and Defense | +2.5% | North America, Europe, Asia Pacific | Short- to Mid-term |

| Growth in Electric Vehicle (EV) Production | +2.0% | China, Europe, North America | Mid- to Long-term |

| Expansion of Wind Energy Sector | +1.8% | Europe, Asia Pacific, North America | Mid- to Long-term |

| Advancements in Composite Manufacturing Technologies | +1.5% | Global | Short- to Mid-term |

| Rising Infrastructure and Construction Projects | +1.0% | Asia Pacific, North America | Mid-term |

Core Material for Composite Market Restraints Analysis

Despite its significant growth potential, the Core Material for Composite market faces several restraints, primarily revolving around the high initial cost of raw materials and complex manufacturing processes. The specialized nature of these materials and their production often translates into higher expenses compared to traditional materials like steel or aluminum, which can deter adoption in cost-sensitive applications. Furthermore, the variability in raw material prices, often linked to petrochemical derivatives, introduces an element of unpredictability into the production costs.

Another notable restraint is the challenge associated with the recyclability and disposal of composite materials. Unlike metals, composites are difficult to recycle economically and efficiently at their end-of-life, leading to environmental concerns and increased waste management costs. This issue is particularly relevant as industries increasingly prioritize sustainability and circular economy principles. The extensive lead times for qualification and certification processes, especially in highly regulated sectors like aerospace, can also impede faster market penetration and product innovation, creating significant barriers to entry for new market players.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Raw Material Costs | -1.8% | Global | Short- to Mid-term |

| Complex Manufacturing Processes | -1.5% | Global | Short- to Mid-term |

| Challenges in Recycling and Disposal | -1.2% | Europe, North America | Mid- to Long-term |

| Volatility in Raw Material Prices | -1.0% | Global | Short-term |

| Strict Regulatory and Certification Requirements | -0.8% | Europe, North America | Long-term |

Core Material for Composite Market Opportunities Analysis

The Core Material for Composite market presents substantial opportunities driven by the growing emphasis on sustainability and the emergence of advanced manufacturing techniques. The development of bio-based core materials, derived from renewable resources like balsa wood or recycled plastics, offers a promising avenue for market growth by addressing environmental concerns and catering to eco-conscious industries. This shift aligns with global sustainability goals and opens new market segments for environmentally friendly composite solutions. Additionally, advancements in additive manufacturing (3D printing) are creating opportunities for producing complex, customized core structures with minimal material waste, thereby expanding design possibilities and reducing production lead times.

The increasing adoption of composites in nascent applications, such as urban air mobility (UAM) vehicles, high-speed rail, and advanced infrastructure projects, represents significant growth opportunities. These sectors demand high-performance, lightweight materials that traditional alternatives cannot adequately provide. Furthermore, the potential for market expansion in developing economies, driven by rapid industrialization and infrastructure development, offers new avenues for core material manufacturers. Strategic partnerships and collaborations across the value chain can also unlock innovation and accelerate market penetration, leveraging combined expertise and resources to develop novel solutions and address specific industry needs efficiently.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Bio-based and Recycled Core Materials | +2.2% | Europe, North America, Asia Pacific | Mid- to Long-term |

| Growth in Emerging Applications (e.g., UAM, Advanced Infrastructure) | +1.9% | Global | Mid- to Long-term |

| Advancements in Additive Manufacturing for Composites | +1.7% | North America, Europe | Short- to Mid-term |

| Expansion into Developing Economies | +1.4% | Asia Pacific, Latin America | Mid-term |

| Strategic Collaborations and Partnerships | +1.0% | Global | Short- to Mid-term |

Core Material for Composite Market Challenges Impact Analysis

The Core Material for Composite market encounters several challenges that can impede its growth trajectory, notably the volatility of raw material prices and the complexities associated with establishing efficient and resilient supply chains. Disruptions in the global supply chain, exacerbated by geopolitical events or natural disasters, can lead to material shortages and significant cost fluctuations, impacting production schedules and profitability. Furthermore, the specialized manufacturing techniques required for composites often necessitate substantial capital investment and a highly skilled workforce, posing barriers to entry and expansion for many companies.

Another critical challenge is the intense competition from traditional materials like metals and advanced plastics, which continue to evolve in performance and cost-effectiveness. While composites offer superior properties, their higher initial cost and complex processing can make them less attractive for certain applications unless significant performance benefits outweigh these factors. Moreover, the industry faces ongoing pressure to develop more sustainable and recyclable solutions, which requires considerable research and development investment without immediate guarantees of commercial viability. Adhering to diverse and evolving regulatory standards across different regions also adds a layer of complexity for manufacturers operating on a global scale.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions and Raw Material Volatility | -1.7% | Global | Short-term |

| High Initial Investment and Manufacturing Complexity | -1.4% | Global | Mid-term |

| Competition from Traditional Materials | -1.1% | Global | Mid- to Long-term |

| Regulatory Hurdles and Environmental Compliance | -0.9% | Europe, North America | Long-term |

| Shortage of Skilled Labor | -0.7% | Global | Mid-term |

Core Material for Composite Market - Updated Report Scope

This report provides a detailed analysis of the Core Material for Composite market, encompassing historical data, current market dynamics, and future projections. It offers an in-depth understanding of market size, growth drivers, restraints, opportunities, and challenges. The scope includes a comprehensive segmentation analysis by material type, application, and region, providing granular insights into market trends and competitive landscapes. The report aims to equip stakeholders with actionable intelligence for strategic decision-making and market positioning over the forecast period.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.85 Billion |

| Market Forecast in 2033 | USD 9.53 Billion |

| Growth Rate | 9.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Advanced Core Solutions, Global Composite Innovations, Lightweight Materials Corp., Structural Core Dynamics, Performance Composites Group, Future Material Technologies, EcoCore Systems, Apex Composite Products, Quantum Core Materials, AeroSpace Structures Inc., WindBlade Core Solutions, Marine Composite Specialists, Transport Component Innovations, Building Solutions Composites, Recreational Gear Materials. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Core Material for Composite market is comprehensively segmented to provide granular insights into its diverse applications and material types. This segmentation allows for a detailed understanding of market dynamics across various sectors, identifying high-growth areas and specific material preferences. The primary segmentation includes analysis by material type, which covers different forms of core materials, each with unique properties and suitable for distinct applications. Furthermore, the market is segmented by end-use industry, reflecting the diverse sectors that increasingly adopt composite structures for their performance benefits.

The classification by material type encompasses widely used core materials such as foam cores, known for their versatility and cost-effectiveness, and honeycomb cores, prized for their high strength-to-weight ratio and rigidity. Balsa wood cores, a natural and sustainable option, also form a significant segment. Each material type caters to specific requirements related to density, stiffness, impact resistance, and cost. The segmentation by end-use industry highlights the critical role of core materials in aerospace and defense, wind energy, marine, automotive, and construction, among others, showcasing the broad utility and growing adoption of composites across global industrial landscapes.

- By Material Type:

- Foam Cores (PVC Foam, PET Foam, PMI Foam, PU Foam, Styrene Acrylonitrile (SAN) Foam)

- Honeycomb Cores (Aluminum Honeycomb, Nomex Honeycomb, Fiber Reinforced Plastic Honeycomb, Polycarbonate Honeycomb)

- Balsa Wood Cores

- Other Core Materials (e.g., Syntactic Foams, Thermoplastic Cores)

- By End-Use Industry:

- Aerospace and Defense

- Wind Energy

- Marine

- Automotive and Transportation

- Construction and Infrastructure

- Sporting Goods

- Others (e.g., Medical, Electronics)

Regional Highlights

- North America: A leading region driven by high demand from the aerospace and defense sectors, coupled with significant investments in research and development for advanced composites. The growth of electric vehicle manufacturing also contributes substantially to market expansion.

- Europe: Characterized by strong growth in the wind energy sector and stringent environmental regulations promoting the adoption of lightweight and sustainable materials. Germany and the Nordic countries are at the forefront of composite innovation and application.

- Asia Pacific (APAC): Expected to be the fastest-growing region, fueled by rapid industrialization, increasing automotive production (including EVs), and massive infrastructure development projects. China, India, and Japan are key contributors to this regional growth.

- Latin America: Showing gradual growth, primarily in the construction and marine sectors, with increasing awareness and adoption of composite materials for cost-efficiency and durability.

- Middle East and Africa (MEA): Emerging market with potential in infrastructure and construction projects, alongside nascent aerospace and defense industry development, albeit starting from a smaller base.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Core Material for Composite Market.- Advanced Core Solutions

- Global Composite Innovations

- Lightweight Materials Corp.

- Structural Core Dynamics

- Performance Composites Group

- Future Material Technologies

- EcoCore Systems

- Apex Composite Products

- Quantum Core Materials

- AeroSpace Structures Inc.

- WindBlade Core Solutions

- Marine Composite Specialists

- Transport Component Innovations

- Building Solutions Composites

- Recreational Gear Materials

Frequently Asked Questions

Analyze common user questions about the Core Material for Composite market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are core materials in composites?

Core materials are lightweight materials used to create sandwich structures in composites, providing high stiffness and strength with minimal weight. They are typically placed between two thin, strong composite skins.

Which industries primarily use core materials for composites?

Core materials are extensively used in industries demanding high strength-to-weight ratios, including aerospace and defense, wind energy, marine, automotive, construction, and sporting goods.

What types of core materials are available?

Common types include foam cores (e.g., PVC, PET, PMI), honeycomb cores (e.g., aluminum, Nomex), and natural materials like balsa wood, each offering distinct properties for various applications.

What are the main drivers for the Core Material for Composite market?

Key drivers include the increasing demand for lightweight vehicles and aircraft, growth in renewable energy (especially wind power), and advancements in composite manufacturing technologies.

What challenges does the Core Material for Composite market face?

Challenges include high raw material costs, complex manufacturing processes, difficulties in recycling, and volatility in supply chains, impacting broader adoption and cost-effectiveness.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted