Material Processing Equipment Market

Material Processing Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703822 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

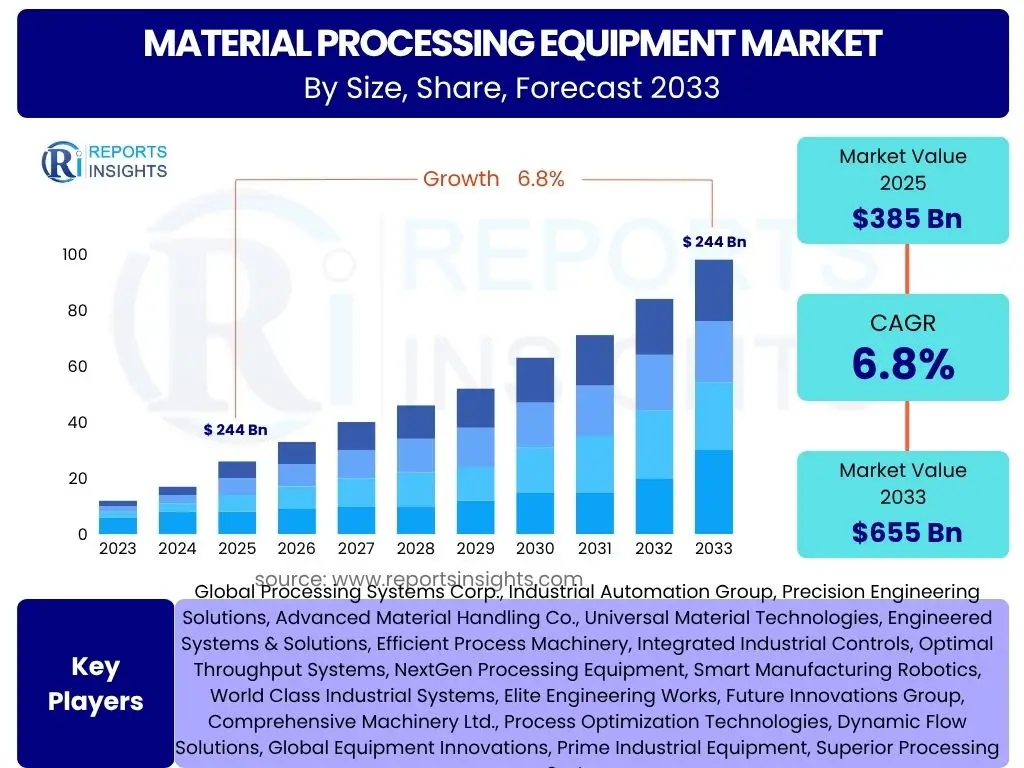

Material Processing Equipment Market Size

According to Reports Insights Consulting Pvt Ltd, The Material Processing Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 385 billion in 2025 and is projected to reach USD 655 billion by the end of the forecast period in 2033.

Key Material Processing Equipment Market Trends & Insights

User inquiries frequently center on the transformative trends shaping the Material Processing Equipment market, highlighting a keen interest in technological advancements, sustainability initiatives, and evolving operational paradigms. Stakeholders are particularly focused on understanding how digitalization, automation, and the integration of smart technologies are enhancing efficiency, precision, and safety across various industrial applications. Furthermore, there is significant attention on the adoption of energy-efficient and environmentally responsible equipment, driven by global mandates and corporate sustainability goals.

The increasing complexity of materials and production processes necessitates more sophisticated and adaptable processing solutions. This includes demand for equipment capable of handling diverse material properties, from high-strength alloys to delicate composites, with minimal waste and maximum yield. The drive for optimized supply chains and localized production also influences equipment design, favoring modular, scalable, and versatile systems that can adapt to fluctuating market demands and regional specifications.

Moreover, the market is witnessing a shift towards service-oriented business models, where equipment manufacturers provide comprehensive solutions beyond mere product sales, including predictive maintenance, operational analytics, and remote diagnostics. This trend is fueled by the desire for improved uptime, reduced operational costs, and enhanced overall equipment effectiveness (OEE). The integration of Internet of Things (IoT) devices within processing equipment is a pivotal enabler of these service models, offering real-time data for performance monitoring and proactive interventions, thereby extending equipment lifespan and optimizing throughput.

- Increasing integration of automation and robotics for enhanced operational efficiency and safety.

- Rising adoption of Industrial IoT (IIoT) for real-time monitoring, predictive maintenance, and data analytics.

- Growing demand for energy-efficient and sustainable processing solutions across industries.

- Emphasis on modular and flexible equipment designs to adapt to diverse production needs.

- Advancements in material science driving the need for specialized and precise processing technologies.

- Shift towards subscription-based and equipment-as-a-service (EaaS) business models.

- Digitization of workflows leading to enhanced process control and traceability.

AI Impact Analysis on Material Processing Equipment

Common user questions regarding Artificial Intelligence (AI) in Material Processing Equipment revolve around its practical applications, perceived benefits, and potential challenges. Users are keen to understand how AI algorithms can optimize operational parameters, predict equipment failures, and enhance quality control in real-time. There is a strong interest in AI's role in improving energy consumption, reducing material waste, and facilitating autonomous operations within complex processing lines, thereby addressing key industry pain points.

The integration of AI is increasingly seen as a critical differentiator, enabling equipment to learn from operational data, adapt to changing conditions, and make intelligent decisions without human intervention. This translates into capabilities such as adaptive process control, where AI fine-tunes parameters to achieve optimal output for varying material inputs, or AI-powered vision systems that detect defects with unprecedented accuracy. These advancements are instrumental in moving towards more resilient, self-optimizing manufacturing environments.

However, concerns are also frequently raised about data security, the complexity of AI system implementation, and the need for a skilled workforce capable of managing and maintaining AI-driven equipment. Users seek clarity on the return on investment for AI integration and strategies to overcome the initial capital expenditure and training requirements. Despite these challenges, the overwhelming sentiment points towards AI as a fundamental technology poised to revolutionize the Material Processing Equipment sector by driving significant improvements in productivity, efficiency, and sustainability.

- Optimized process control through AI-driven algorithms for improved efficiency and yield.

- Predictive maintenance enabled by machine learning to reduce downtime and maintenance costs.

- Enhanced quality control and defect detection using AI-powered vision systems.

- Autonomous operation capabilities for material handling and processing tasks.

- Energy consumption optimization and waste reduction through intelligent resource management.

- Data-driven decision-making for equipment upgrades and operational improvements.

- Simulation and digital twin technologies leveraging AI for process design and optimization.

Key Takeaways Material Processing Equipment Market Size & Forecast

User inquiries concerning key takeaways from the Material Processing Equipment market size and forecast consistently highlight the robust growth trajectory driven by industrial expansion and technological advancements. A primary insight is the market's resilience and its deep linkage to global manufacturing output and infrastructure development. The sustained demand for high-quality, efficiently processed materials across diverse sectors, including mining, construction, manufacturing, and food processing, underpins the positive forecast for the coming decade.

Another significant takeaway is the increasing emphasis on smart, connected, and sustainable equipment. The forecast indicates that investments will increasingly flow towards solutions incorporating automation, digitalization, and energy efficiency, reflecting a broader industry commitment to operational excellence and environmental stewardship. This shift is not merely a trend but a fundamental reorientation of market priorities, with long-term implications for product development and competitive strategies.

Furthermore, the regional dynamics reveal a strong growth impetus from emerging economies, particularly in Asia Pacific, where industrialization and urbanization are accelerating. While established markets in North America and Europe continue to innovate and adopt advanced technologies, the sheer scale of development in newer industrial hubs presents substantial opportunities. Overall, the market is poised for significant expansion, characterized by a confluence of technological innovation, sustainability imperatives, and expanding industrial bases globally.

- Significant market expansion anticipated due to global industrialization and infrastructure projects.

- Technological innovation, particularly in automation and AI, will be a primary growth accelerator.

- Sustainability and energy efficiency are critical drivers influencing equipment design and adoption.

- Asia Pacific is projected to be the fastest-growing region, fueled by rapid manufacturing growth.

- The market is shifting towards integrated solutions offering enhanced data insights and operational flexibility.

- High capital expenditure requirements remain a notable barrier, driving interest in financing and service models.

- Continuous demand for customized processing solutions tailored to specific industry needs.

Material Processing Equipment Market Drivers Analysis

The Material Processing Equipment market is significantly propelled by several macro and microeconomic factors, creating a robust demand environment. Rapid industrialization and urbanization across emerging economies, particularly in the Asia Pacific region, necessitate substantial investments in manufacturing, construction, and mining sectors, which are primary consumers of material processing equipment. This growth is complemented by the ongoing global push for advanced infrastructure development, including roads, bridges, and commercial facilities, all requiring extensive material preparation and handling capabilities. The increasing complexity and diversity of materials used in modern manufacturing, such as composites, specialized alloys, and recycled content, also drive demand for sophisticated and precise processing machinery capable of handling varied material properties.

Furthermore, technological advancements, especially in automation, robotics, and digitalization, are revolutionizing the efficiency and safety of material processing operations. The integration of these technologies allows for higher throughput, reduced labor costs, and improved quality control, making advanced equipment a compelling investment for industries striving for competitive advantage. The growing emphasis on environmental sustainability and resource efficiency also acts as a significant driver. Industries are increasingly seeking equipment that minimizes waste, reduces energy consumption, and facilitates the recycling and reuse of materials, aligning with global circular economy initiatives and stringent regulatory frameworks.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Industrial Growth & Infrastructure Development | +1.5-2.0% | Asia Pacific, North America, Middle East | Short to Long-term (2025-2033) |

| Increasing Automation & Digitalization Adoption | +1.0-1.5% | Europe, North America, Developed APAC | Mid to Long-term (2027-2033) |

| Rising Demand for Advanced & Specialized Materials | +0.8-1.2% | Global, particularly high-tech manufacturing hubs | Short to Mid-term (2025-2030) |

| Growing Focus on Sustainability & Resource Efficiency | +0.7-1.0% | Europe, North America, Select APAC | Mid to Long-term (2027-2033) |

| Expansion of Mining and Construction Sectors | +1.2-1.8% | Africa, Latin America, Asia Pacific | Short to Mid-term (2025-2030) |

Material Processing Equipment Market Restraints Analysis

Despite the positive growth trajectory, the Material Processing Equipment market faces significant restraints that can impede its expansion. One primary restraint is the substantial capital expenditure required for acquiring advanced processing equipment. The high upfront investment can be prohibitive for small and medium-sized enterprises (SMEs) and even large corporations, particularly in economically volatile periods. This high cost often necessitates long payback periods, making companies cautious about new investments and potentially delaying modernization efforts. Furthermore, the complexities associated with financing large-scale equipment purchases, including securing loans and managing interest rates, can add to the financial burden and act as a deterrent for market entry or expansion.

Another critical restraint is the increasingly stringent environmental regulations and safety standards. While driving innovation towards sustainable solutions, these regulations often lead to higher manufacturing costs for equipment producers and increased operational costs for end-users, as compliance requires specialized technology, process adjustments, and ongoing monitoring. Adapting existing equipment to meet new standards can also be expensive and complex, potentially leading to obsolescence. Additionally, the shortage of skilled labor capable of operating, maintaining, and troubleshooting advanced material processing equipment poses a significant challenge. The complexity of modern machinery requires specialized training and expertise, and the global dearth of such skilled professionals can lead to operational inefficiencies, increased downtime, and higher labor costs, thereby limiting the adoption rate of advanced systems.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure & Investment Costs | -1.0-1.5% | Global, particularly emerging economies | Short to Mid-term (2025-2030) |

| Stringent Environmental & Safety Regulations | -0.8-1.2% | Europe, North America, Developed APAC | Mid to Long-term (2027-2033) |

| Shortage of Skilled Labor & Technical Expertise | -0.7-1.0% | Global, particularly highly industrialized regions | Short to Long-term (2025-2033) |

| Economic Volatility & Geopolitical Instability | -0.5-0.8% | Global, varying by specific regions | Short-term (2025-2027) |

| Complexity of Equipment Integration & Maintenance | -0.4-0.6% | Global, affecting smaller enterprises | Mid-term (2027-2030) |

Material Processing Equipment Market Opportunities Analysis

Significant opportunities exist within the Material Processing Equipment market, driven by the increasing demand for customized solutions and the ongoing digitalization of industrial processes. The trend towards mass customization and personalized products across various consumer goods sectors translates directly into a need for flexible and adaptable processing equipment capable of rapid changeovers and small-batch production. This presents an opportunity for manufacturers to develop modular and reconfigurable systems that can efficiently handle diverse material types and product specifications, moving away from rigid, high-volume production lines. Furthermore, the expansion of e-commerce and logistics sectors globally creates new avenues for material handling and processing equipment, as these industries require sophisticated sorting, packaging, and distribution systems to manage vast volumes of goods efficiently.

The global push for circular economy principles and sustainable industrial practices offers another substantial growth opportunity. This involves developing and deploying equipment specifically designed for recycling, waste reduction, and the processing of secondary raw materials. Technologies that enable efficient material separation, purification, and transformation of waste into valuable resources are in high demand. Companies that can innovate in these areas, offering solutions that minimize environmental impact while maintaining economic viability, are poised for significant market gains. This includes advancements in energy-efficient machinery, systems for carbon capture, and equipment that facilitates the use of bio-based or recycled content in production processes.

Moreover, the untapped potential in emerging markets provides immense opportunities for market penetration and expansion. As these regions continue to industrialize, the demand for foundational material processing infrastructure grows exponentially. While cost-effectiveness remains a crucial factor, there is also a rising appreciation for quality, reliability, and modern technological integration. Offering scalable, robust, and technologically appropriate solutions tailored to the specific needs and economic conditions of these markets can unlock substantial revenue streams and foster long-term partnerships. The development of localized manufacturing capabilities and after-sales support networks in these regions further enhances market penetration strategies.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Circular Economy & Recycling Initiatives | +1.0-1.5% | Europe, Asia Pacific, North America | Mid to Long-term (2027-2033) |

| Demand for Smart & Connected Equipment (IIoT, AI) | +0.9-1.3% | Global, particularly developed economies | Short to Long-term (2025-2033) |

| Expansion into Emerging Industrial Markets | +1.2-1.7% | Asia Pacific, Latin America, Africa | Short to Mid-term (2025-2030) |

| Customization & Flexibility in Manufacturing | +0.8-1.1% | Global, especially high-value manufacturing | Mid-term (2027-2030) |

| Development of Advanced Material Processing Technologies | +0.7-1.0% | Global, R&D intensive regions | Long-term (2030-2033) |

Material Processing Equipment Market Challenges Impact Analysis

The Material Processing Equipment market faces several significant challenges that can impact its growth and operational stability. One prominent challenge is the increasing volatility in global supply chains, exacerbated by geopolitical tensions, natural disasters, and economic protectionism. This volatility leads to unpredictable costs for raw materials, components, and logistics, making it difficult for manufacturers to forecast production costs and delivery times accurately. Disruptions can cause delays in equipment manufacturing and deployment, affecting project timelines for end-users and potentially eroding profit margins for equipment suppliers. Furthermore, the reliance on specialized components and materials from a limited number of suppliers makes the industry particularly vulnerable to supply chain shocks.

Another critical challenge is the intense competitive landscape, characterized by the presence of numerous global and regional players. This high level of competition often leads to pricing pressures, forcing manufacturers to innovate constantly while maintaining competitive pricing, which can squeeze profit margins. Differentiation becomes key, requiring significant investment in research and development to introduce new technologies and features that provide a clear advantage. Additionally, the rapid pace of technological obsolescence poses a continuous challenge. As new innovations emerge, existing equipment can quickly become outdated, necessitating frequent upgrades or replacements, which can be a significant cost burden for both manufacturers in terms of R&D and end-users in terms of investment cycles.

The imperative to meet increasingly stringent sustainability standards and reduce environmental footprint represents both an opportunity and a significant challenge. While driving innovation, it requires substantial investment in redesigning equipment for greater energy efficiency, lower emissions, and the ability to process recycled materials. This transition demands not only technological shifts but also changes in operational practices and significant financial outlay, potentially impacting short-term profitability. Moreover, adapting to diverse regional regulations and achieving global compliance adds complexity to product development and market entry strategies, requiring manufacturers to navigate a fragmented regulatory landscape.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions & Volatility | -1.0-1.5% | Global, particularly manufacturing hubs | Short to Mid-term (2025-2028) |

| Intense Competition & Pricing Pressures | -0.8-1.2% | Global, especially mature markets | Short to Long-term (2025-2033) |

| Rapid Technological Obsolescence | -0.7-1.0% | Global, affecting all technology adopters | Mid-term (2027-2030) |

| Meeting Evolving Sustainability & Emission Standards | -0.6-0.9% | Europe, North America, Developed APAC | Mid to Long-term (2027-2033) |

| Cybersecurity Risks for Connected Equipment | -0.4-0.6% | Global, particularly for IIoT integrated systems | Short to Long-term (2025-2033) |

Material Processing Equipment Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the Material Processing Equipment market, providing a detailed analysis of its size, growth projections, key trends, and influential factors. It offers an in-depth examination of market segmentation by equipment type, application, and end-user industries, alongside a thorough regional analysis to highlight geographical growth opportunities and challenges. The scope encompasses an assessment of the competitive landscape, profiling leading players and evaluating their strategic initiatives. Furthermore, the report provides critical insights into the impact of emerging technologies like Artificial Intelligence (AI) and the Internet of Things (IoT) on the market's evolution, alongside an analysis of sustainability imperatives shaping future developments.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 385 Billion |

| Market Forecast in 2033 | USD 655 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Processing Systems Corp., Industrial Automation Group, Precision Engineering Solutions, Advanced Material Handling Co., Universal Material Technologies, Engineered Systems & Solutions, Efficient Process Machinery, Integrated Industrial Controls, Optimal Throughput Systems, NextGen Processing Equipment, Smart Manufacturing Robotics, World Class Industrial Systems, Elite Engineering Works, Future Innovations Group, Comprehensive Machinery Ltd., Process Optimization Technologies, Dynamic Flow Solutions, Global Equipment Innovations, Prime Industrial Equipment, Superior Processing Systems. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Material Processing Equipment market is comprehensively segmented to provide granular insights into its diverse components, facilitating a deeper understanding of market dynamics and investment opportunities. Key segmentation areas include equipment type, application, and end-user, each revealing unique market demands and technological preferences. The equipment type segmentation encompasses a broad range of machinery vital for transforming raw materials into usable forms, such as crushing, screening, conveying, mixing, separation, grinding, drying, and agglomeration equipment. Each type addresses specific stages of material processing, from initial size reduction to final product formation, and their individual market trajectories are influenced by specific industrial requirements and technological advancements.

Application-based segmentation highlights the primary industries consuming material processing equipment, including vital sectors like mining and metallurgy, construction and infrastructure, food and beverage processing, chemical and petrochemical, and waste management and recycling. The distinct material characteristics and process requirements of each application dictate the demand for specialized equipment. For instance, the mining sector requires robust, high-capacity crushing and conveying systems, while the pharmaceutical industry demands precision mixing and separation equipment with stringent hygiene standards. Understanding these application-specific needs is crucial for manufacturers to tailor their product offerings and market strategies effectively.

Finally, end-user segmentation differentiates between heavy industry, light industry, and commercial applications, reflecting varying scales of operation and investment capacities. Heavy industries, such as large-scale mining or infrastructure projects, typically demand large, custom-engineered, and high-capacity equipment with significant capital investment. Light industries and commercial sectors, conversely, might require more flexible, smaller-scale, and often more automated solutions. This multi-faceted segmentation allows for a nuanced analysis of market demand drivers, technological adoption patterns, and competitive dynamics across the entire value chain of material processing.

- By Equipment Type:

- Crushing Equipment: Used for primary and secondary size reduction of large materials.

- Screening Equipment: Separates materials by size and removes impurities.

- Conveying Equipment: Transports materials within a processing facility.

- Mixing and Blending Equipment: Combines different materials to achieve homogeneity.

- Separation Equipment: Isolates specific components from a mixture (e.g., magnetic, gravity, optical).

- Grinding Equipment: Further reduces particle size for fine processing.

- Drying and Cooling Equipment: Removes moisture or regulates temperature of materials.

- Agglomeration Equipment: Forms larger particles from fine powders.

- Other Equipment Types: Includes filtering, granulating, and specialized compacting machinery.

- By Application:

- Mining & Metallurgy: Extraction and processing of ores and minerals.

- Construction & Infrastructure: Preparation of aggregates, concrete, and asphalt.

- Food & Beverage Processing: Handling raw ingredients, mixing, and packaging.

- Chemical & Petrochemical: Processing of chemicals, polymers, and fuels.

- Pharmaceutical & Biotechnology: Sterile processing and precise material handling.

- Waste Management & Recycling: Sorting, crushing, and processing waste materials for reuse.

- Manufacturing & Industrial (General): Diverse applications in various manufacturing processes.

- Agriculture: Processing of grains, feeds, and other agricultural products.

- By End-User:

- Heavy Industry: Large-scale operations with high throughput requirements.

- Light Industry: Smaller-scale manufacturing and processing.

- Commercial: Applications in smaller businesses or specialized services.

Regional Highlights

The Material Processing Equipment market exhibits distinct regional dynamics driven by varying levels of industrialization, infrastructure development, and technological adoption. North America, characterized by its mature industrial base and strong emphasis on automation and smart manufacturing, continues to be a significant market. The region benefits from substantial investments in infrastructure upgrades, advanced manufacturing, and the adoption of cutting-edge technologies to enhance efficiency and productivity. While growth may be more moderate compared to emerging markets, the demand for high-value, digitally integrated, and sustainable processing solutions remains robust, driven by innovation and strict regulatory frameworks.

Europe stands as a frontrunner in adopting highly automated and environmentally compliant material processing solutions. The region's strong focus on circular economy principles, energy efficiency, and stringent environmental regulations drives innovation in green processing technologies and advanced recycling equipment. Countries like Germany and the Nordic nations lead in developing and implementing sophisticated, energy-efficient machinery. The market here is also characterized by a demand for precision engineering, customized solutions, and lifecycle services, reflecting a mature industrial landscape committed to sustainable and high-quality production.

Asia Pacific (APAC) emerges as the fastest-growing region in the Material Processing Equipment market, propelled by rapid industrialization, burgeoning manufacturing sectors, and extensive infrastructure development, particularly in China, India, and Southeast Asian countries. The sheer scale of construction, mining, and industrial projects in this region creates immense demand for a wide range of processing equipment, from basic crushing units to advanced automation systems. While cost-effectiveness remains a key consideration, there is a growing trend towards adopting advanced and energy-efficient technologies to meet increasing production demands and global quality standards.

Latin America, with its rich natural resources and developing industrial base, presents substantial opportunities, especially in the mining, construction, and agricultural sectors. Investments in infrastructure and resource extraction drive the demand for material processing equipment, though the market can be influenced by commodity price fluctuations and economic stability. Countries like Brazil, Mexico, and Chile are key contributors, focusing on modernizing existing facilities and expanding production capacities. The Middle East and Africa (MEA) region also shows significant promise, fueled by large-scale construction projects, diversification efforts away from oil economies, and growing mining activities. Government initiatives to develop manufacturing capabilities and improve infrastructure are creating new avenues for material processing equipment, albeit with unique challenges related to climate and logistics.

- North America: Stable demand driven by infrastructure upgrades, advanced manufacturing, and high technology adoption. Emphasis on automation, digitalization, and productivity enhancements.

- Europe: Leader in sustainable and energy-efficient processing solutions due to stringent environmental regulations and circular economy initiatives. Focus on precision, customization, and advanced engineering.

- Asia Pacific (APAC): Fastest-growing market due to rapid industrialization, robust manufacturing expansion, and extensive infrastructure development in countries like China and India. High volume demand across various applications.

- Latin America: Growing market primarily driven by mining, construction, and agriculture sectors. Demand influenced by commodity prices and economic stability.

- Middle East and Africa (MEA): Emerging market with significant potential due to large-scale construction projects, industrial diversification, and resource extraction activities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Material Processing Equipment Market.- Global Processing Systems Corp.

- Industrial Automation Group

- Precision Engineering Solutions

- Advanced Material Handling Co.

- Universal Material Technologies

- Engineered Systems & Solutions

- Efficient Process Machinery

- Integrated Industrial Controls

- Optimal Throughput Systems

- NextGen Processing Equipment

- Smart Manufacturing Robotics

- World Class Industrial Systems

- Elite Engineering Works

- Future Innovations Group

- Comprehensive Machinery Ltd.

- Process Optimization Technologies

- Dynamic Flow Solutions

- Global Equipment Innovations

- Prime Industrial Equipment

- Superior Processing Systems

Frequently Asked Questions

Analyze common user questions about the Material Processing Equipment market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Material Processing Equipment Market?

The Material Processing Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, reaching an estimated USD 655 billion by 2033 from USD 385 billion in 2025.

Which key trends are driving the Material Processing Equipment Market?

Key trends include increasing automation and robotics integration, rising adoption of Industrial IoT (IIoT) for real-time monitoring, a growing emphasis on energy-efficient and sustainable solutions, and a shift towards modular and flexible equipment designs.

How is AI impacting the Material Processing Equipment sector?

AI is significantly impacting the sector by enabling optimized process control, predictive maintenance, enhanced quality control, and autonomous operation capabilities, leading to improved efficiency, reduced downtime, and resource optimization.

What are the primary challenges faced by the Material Processing Equipment Market?

The market faces challenges such as volatile global supply chains, intense competition leading to pricing pressures, rapid technological obsolescence, the need to meet evolving sustainability standards, and cybersecurity risks for connected systems.

Which regions are key contributors to the Material Processing Equipment Market?

Asia Pacific is the fastest-growing region, driven by rapid industrialization, while North America and Europe maintain stable demand for advanced, high-value, and sustainable processing solutions due to their mature industrial bases and strong regulatory frameworks.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted