Hydrogen Fuel Cell Train Market

Hydrogen Fuel Cell Train Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704389 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

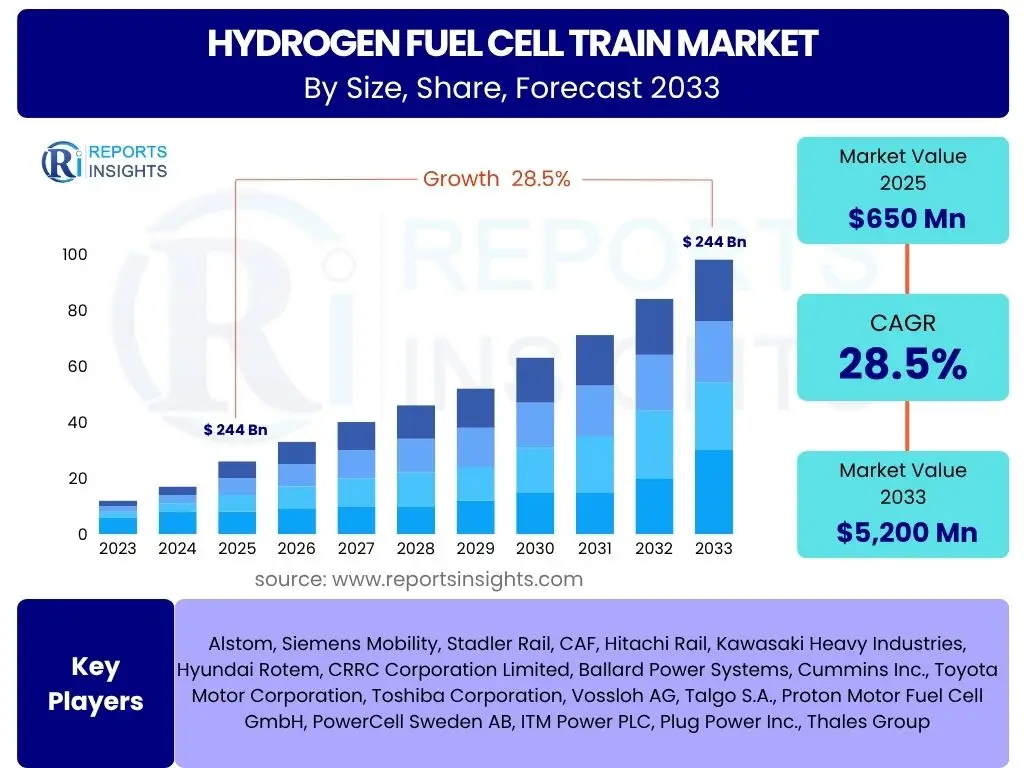

Hydrogen Fuel Cell Train Market Size

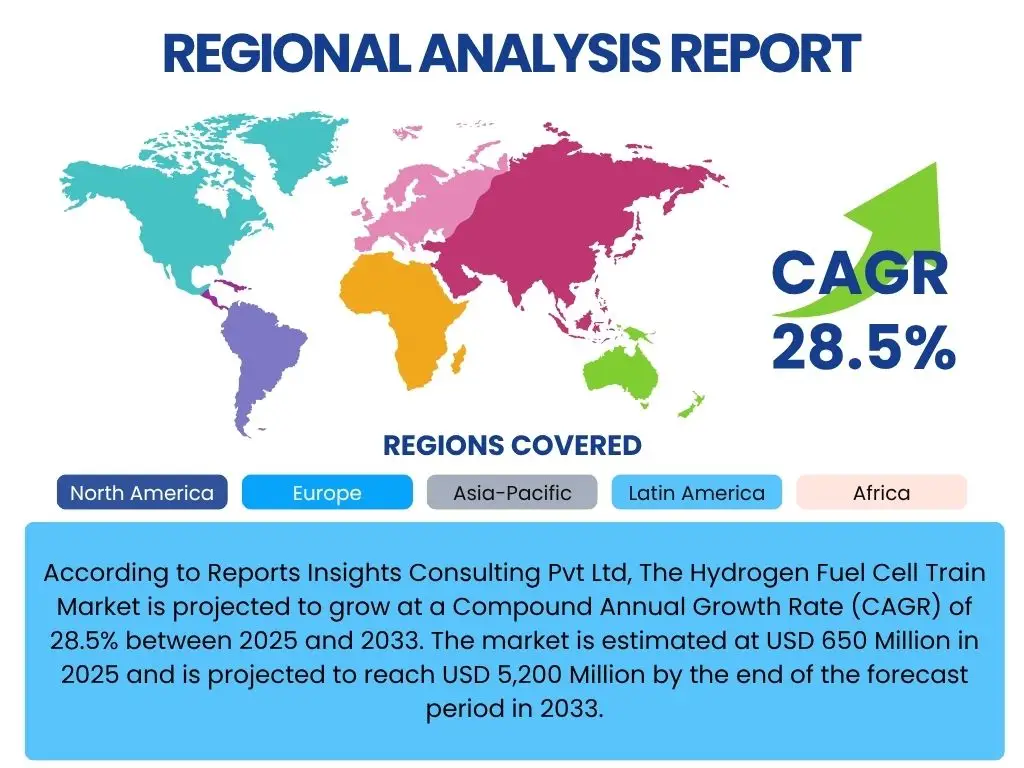

According to Reports Insights Consulting Pvt Ltd, The Hydrogen Fuel Cell Train Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 28.5% between 2025 and 2033. The market is estimated at USD 650 Million in 2025 and is projected to reach USD 5,200 Million by the end of the forecast period in 2033.

Key Hydrogen Fuel Cell Train Market Trends & Insights

The Hydrogen Fuel Cell Train market is experiencing a significant transformation driven by a global imperative for decarbonization and sustainable transportation solutions. Key trends indicate a robust shift towards cleaner energy sources in the railway sector, with hydrogen fuel cell technology emerging as a frontrunner for non-electrified routes. Growing public and private investments in hydrogen infrastructure, coupled with stringent environmental regulations, are accelerating the adoption of these innovative trains. Furthermore, advancements in fuel cell efficiency and hydrogen storage solutions are enhancing the operational viability and economic attractiveness of these systems, making them competitive alternatives to traditional diesel locomotives.

Technological innovation is a pivotal trend, encompassing not only the fuel cell stacks themselves but also advanced materials for lightweight train design and sophisticated energy management systems that optimize power usage. There is also a notable trend towards collaborative ventures between train manufacturers, hydrogen technology providers, and railway operators, facilitating knowledge transfer and accelerating commercial deployment. The market is witnessing the expansion of pilot projects into full-scale commercial routes, particularly in European countries, which are setting precedents for other regions. This proactive approach by various stakeholders underscores a collective commitment to establishing a resilient and environmentally friendly railway ecosystem powered by hydrogen.

- Accelerated decarbonization initiatives within the global transportation sector.

- Increased government funding and policy support for hydrogen infrastructure development.

- Technological advancements in fuel cell efficiency, hydrogen storage, and energy management.

- Growing collaboration between railway operators, train manufacturers, and hydrogen suppliers.

- Expansion of hydrogen train pilot projects into commercial operational routes.

- Emphasis on green hydrogen production to ensure a fully sustainable lifecycle.

AI Impact Analysis on Hydrogen Fuel Cell Train

The integration of Artificial Intelligence (AI) is poised to revolutionize the Hydrogen Fuel Cell Train market by significantly enhancing operational efficiency, predictive maintenance, and overall safety. Users frequently inquire about how AI can optimize energy consumption, given the critical importance of hydrogen fuel management. AI algorithms can analyze vast datasets from sensors on trains, including fuel cell performance, battery status, and route topography, to predict optimal power delivery and regeneration strategies, thereby extending range and reducing operational costs. Furthermore, AI-driven predictive maintenance systems can monitor the health of critical components like fuel cells, traction motors, and hydrogen storage tanks, identifying potential failures before they occur and minimizing downtime, a major concern for railway operators seeking reliable service.

Beyond operational enhancements, AI is expected to play a crucial role in route optimization and scheduling, leveraging real-time data on weather, traffic, and infrastructure availability to ensure punctual and efficient services. For safety, AI can power advanced driver assistance systems, defect detection on tracks, and intelligent surveillance within train carriages, addressing user concerns about the safety protocols for hydrogen-powered vehicles. Moreover, AI's analytical capabilities will be instrumental in the design and development phases of new hydrogen fuel cell train models, enabling simulations for aerodynamic efficiency, structural integrity, and hydrogen system integration. The synergistic combination of AI with hydrogen technology is therefore viewed as a pathway to smarter, safer, and more sustainable rail transport systems.

- Predictive maintenance optimization, reducing unscheduled downtime and operational costs.

- Enhanced energy management and route optimization through real-time data analysis.

- Improved safety features via AI-powered monitoring and anomaly detection systems.

- Automated diagnostics for fuel cell performance and hydrogen system integrity.

- Support for autonomous operation capabilities in shunting yards and designated routes.

- Data-driven design and simulation for new train models, accelerating development cycles.

Key Takeaways Hydrogen Fuel Cell Train Market Size & Forecast

The Hydrogen Fuel Cell Train market is on an accelerated growth trajectory, signifying a critical shift towards sustainable railway transportation. The market's projected expansion from USD 650 Million in 2025 to USD 5,200 Million by 2033, at a robust CAGR of 28.5%, underscores the increasing global commitment to decarbonization and the viability of hydrogen as a primary fuel source for trains. This substantial growth is primarily driven by supportive government policies, escalating environmental concerns, and continuous technological breakthroughs that enhance the efficiency and reliability of fuel cell systems. Stakeholders across the value chain, from component manufacturers to railway operators, are poised to benefit from this expansion, with significant opportunities for investment and innovation in both train technology and hydrogen infrastructure.

A key insight from the forecast is the emerging competitive landscape, where established rail manufacturers are actively investing in hydrogen capabilities, and new players focusing on fuel cell technology are entering the market. This dynamic environment is fostering rapid innovation and bringing down costs, making hydrogen fuel cell trains increasingly attractive compared to conventional diesel locomotives, especially on non-electrified lines. Furthermore, the forecast highlights the critical need for a synchronized development of green hydrogen production and refueling infrastructure to support widespread adoption. The market's future will largely depend on overcoming initial capital expenditure barriers and ensuring a stable, cost-effective supply of hydrogen, positioning the market as a long-term growth area for sustainable mobility.

- Significant market expansion driven by global decarbonization efforts.

- High Compound Annual Growth Rate (CAGR) indicating strong investor confidence and technological maturity.

- Increasing government support and regulatory frameworks are key accelerators.

- Technological advancements are continuously improving system efficiency and reducing costs.

- Critical importance of synchronized development of green hydrogen production and refueling infrastructure.

- Emerging opportunities for both established players and new entrants across the value chain.

Hydrogen Fuel Cell Train Market Drivers Analysis

The market for Hydrogen Fuel Cell Trains is propelled by a confluence of powerful drivers rooted in environmental sustainability, energy independence, and technological innovation. Global efforts to mitigate climate change and reduce carbon emissions are paramount, pushing governments and railway operators to seek alternatives to diesel-powered trains. Hydrogen fuel cell technology offers a zero-emission solution at the point of use, aligning perfectly with ambitious national and international decarbonization targets. Furthermore, the rising cost volatility of fossil fuels and the desire for greater energy security are compelling factors, as hydrogen, especially when produced from renewable sources (green hydrogen), offers a stable and domestically available energy supply, reducing reliance on imported fuels and enhancing economic resilience.

Technological advancements in fuel cell efficiency, hydrogen storage density, and overall system integration have significantly improved the performance and feasibility of hydrogen trains, making them more attractive for railway applications. These improvements translate into longer ranges, faster refueling times, and reduced operational complexities, addressing previous limitations. Additionally, the increasing availability of incentives, subsidies, and favorable policies from governments and international bodies are playing a crucial role in de-risking initial investments and stimulating market adoption. These financial mechanisms help bridge the cost gap between hydrogen solutions and traditional systems, encouraging research, development, and deployment of hydrogen fuel cell trains across diverse railway networks.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Decarbonization Goals and Strict Emission Regulations | +3.0% | Europe, Asia Pacific, North America | Mid-term to Long-term |

| Government Subsidies and Incentives for Green Technologies | +2.5% | Germany, France, Japan, South Korea | Short-term to Mid-term |

| Advancements in Fuel Cell Technology and Hydrogen Storage | +2.0% | Global | Mid-term |

| Rising Cost and Volatility of Diesel Fuel | +1.8% | Global | Short-term to Mid-term |

| Demand for Energy Independence and Security | +1.5% | Europe, North America | Mid-term to Long-term |

Hydrogen Fuel Cell Train Market Restraints Analysis

Despite the promising growth trajectory, the Hydrogen Fuel Cell Train market faces several significant restraints that could impede its widespread adoption. One of the primary barriers is the high initial capital expenditure associated with hydrogen fuel cell trains compared to conventional diesel or even electrified alternatives. The sophisticated technology involved in fuel cells, hydrogen storage tanks, and associated power electronics contributes to higher manufacturing costs, which can deter railway operators, especially those with limited budgets. Furthermore, the development of a comprehensive hydrogen refueling infrastructure is still in its nascent stages globally. The lack of readily available and widespread refueling stations poses a significant logistical challenge, limiting the operational flexibility and scalability of hydrogen train fleets and necessitating substantial infrastructure investment.

Another crucial restraint pertains to the current high cost and energy intensity of producing green hydrogen, which is essential for ensuring the entire lifecycle of hydrogen trains is carbon-neutral. While production costs are expected to decrease with technological advancements and economies of scale, they currently impact the overall economic viability. Public perception and safety concerns regarding hydrogen, particularly its flammability and storage under high pressure, also represent a psychological barrier, though extensive safety measures are integrated into train design and operation. Additionally, competition from established electrification projects, which benefit from existing infrastructure and proven reliability, presents a formidable alternative, especially for high-traffic routes where electrification remains a preferred solution, potentially slowing the uptake of hydrogen solutions in certain segments.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Expenditure | -2.8% | Global, particularly Developing Regions | Short-term to Mid-term |

| Lack of Widespread Hydrogen Refueling Infrastructure | -2.5% | Global | Short-term to Mid-term |

| High Cost of Green Hydrogen Production | -1.9% | Global | Short-term |

| Perceived Safety Concerns and Public Acceptance | -1.5% | Global | Mid-term |

| Competition from Railway Electrification | -1.2% | Europe, Asia Pacific | Mid-term to Long-term |

Hydrogen Fuel Cell Train Market Opportunities Analysis

The Hydrogen Fuel Cell Train market is rich with opportunities stemming from the ongoing global energy transition and the growing demand for sustainable transportation. A significant opportunity lies in the development and deployment of green hydrogen production at scale, utilizing renewable energy sources such as solar and wind power. As green hydrogen becomes more cost-effective and readily available, it will directly enhance the environmental credentials and economic viability of hydrogen fuel cell trains, making them a truly sustainable alternative. This presents immense investment opportunities in electrolysis technology and renewable energy projects specifically aimed at supplying the transportation sector. Furthermore, the substantial network of non-electrified railway lines globally, particularly in North America, parts of Europe, and emerging economies, offers a vast addressable market for hydrogen trains, as electrification of these routes is often prohibitively expensive or geographically challenging.

Another promising opportunity involves the retrofitting of existing diesel train fleets with hydrogen fuel cell technology. This approach allows railway operators to extend the lifespan of their assets while transitioning to cleaner energy, potentially at a lower cost than purchasing entirely new hydrogen trains. This incremental shift can accelerate adoption and reduce the overall carbon footprint of national railway systems. Strategic partnerships and collaborations between train manufacturers, hydrogen producers, energy companies, and local governments are also creating new business models and fostering innovation. These alliances facilitate knowledge sharing, overcome infrastructure challenges, and pool resources for large-scale projects, thereby unlocking new geographical markets and operational segments. The burgeoning focus on circular economy principles within the industry also presents opportunities for hydrogen train components to be recycled or reused, further enhancing sustainability and long-term cost efficiency.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Green Hydrogen Production and Infrastructure | +4.0% | Global | Mid-term to Long-term |

| Untapped Market of Non-Electrified Railway Lines | +3.5% | North America, Eastern Europe, Developing Asia | Mid-term to Long-term |

| Retrofitting of Existing Diesel Locomotive Fleets | +3.0% | Europe, North America, India, China | Short-term to Mid-term |

| Strategic Partnerships and Cross-Sector Collaborations | +2.5% | Global | Short-term to Mid-term |

| Development of Standardized Technologies and Regulations | +2.0% | Global | Mid-term |

Hydrogen Fuel Cell Train Market Challenges Impact Analysis

The Hydrogen Fuel Cell Train market, while promising, grapples with several formidable challenges that require concerted efforts for resolution. One significant hurdle is the complexity and nascent stage of the hydrogen supply chain. Ensuring a consistent, reliable, and cost-effective supply of hydrogen, especially green hydrogen, from production facilities to various refueling points across extensive railway networks, presents considerable logistical and infrastructural challenges. This includes the storage, transportation, and safe handling of hydrogen, which differ substantially from conventional fuels and demand specialized infrastructure and trained personnel. The scalability of hydrogen production, particularly green hydrogen, is also a challenge, as current capacities are insufficient to meet the potential large-scale demand from a fully transitioned rail sector.

Another major challenge lies in overcoming the high initial investment costs for both the trains themselves and the required hydrogen infrastructure. This financial barrier can deter potential adopters, especially in regions with tighter budgets or where traditional diesel infrastructure is deeply entrenched. Furthermore, regulatory frameworks and standardization are still evolving for hydrogen-powered rail transport. The absence of universally accepted safety standards, operational guidelines, and certification processes can slow down deployment and restrict cross-border operations. Building public confidence and addressing safety perceptions surrounding hydrogen technology are also critical, as any incident, however minor, could significantly impede market acceptance. Lastly, the energy density of hydrogen, while superior to batteries for longer distances, still presents challenges in terms of onboard storage volume and weight, which can impact train design and payload capacity, particularly for freight applications requiring substantial power and range.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Developing and Scaling Hydrogen Supply Chain & Infrastructure | -2.0% | Global | Short-term to Mid-term |

| High Initial Investment and Operating Costs | -1.8% | Global | Short-term to Mid-term |

| Evolving Regulatory Landscape and Lack of Standardized Norms | -1.5% | Global, particularly Europe for cross-border | Mid-term |

| Public Perception and Safety Acceptance of Hydrogen | -1.0% | Global | Mid-term to Long-term |

| Energy Density and Onboard Storage Limitations | -0.8% | Global | Long-term (R&D focus) |

Hydrogen Fuel Cell Train Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the Hydrogen Fuel Cell Train market, offering an in-depth analysis of market size, growth drivers, restraints, opportunities, and challenges. It provides a strategic outlook on the market's trajectory from 2025 to 2033, incorporating insights from historical trends and future projections. The report segments the market by various parameters including type, application, component, and geography, offering granular insights into each segment's performance and potential. Furthermore, it delivers a detailed competitive landscape, profiling key players and assessing their strategic initiatives, product portfolios, and market positioning to provide a holistic understanding of the industry structure. The scope is designed to equip stakeholders with actionable intelligence for informed decision-making and strategic planning within the rapidly evolving hydrogen railway sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 650 Million |

| Market Forecast in 2033 | USD 5,200 Million |

| Growth Rate | 28.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Alstom, Siemens Mobility, Stadler Rail, CAF, Hitachi Rail, Kawasaki Heavy Industries, Hyundai Rotem, CRRC Corporation Limited, Ballard Power Systems, Cummins Inc., Toyota Motor Corporation, Toshiba Corporation, Vossloh AG, Talgo S.A., Proton Motor Fuel Cell GmbH, PowerCell Sweden AB, ITM Power PLC, Plug Power Inc., Thales Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Hydrogen Fuel Cell Train market is segmented to provide a granular understanding of its diverse applications and technological components, enabling targeted analysis and strategic development. The segmentation by type distinguishes between passenger and freight trains, recognizing the differing requirements for speed, capacity, and operational cycles in each category. This differentiation is crucial as passenger trains often prioritize comfort and lower noise levels, while freight trains demand high power output and robust performance for heavy loads over long distances. Analyzing these segments helps identify specific technological innovations and market opportunities tailored to their unique operational demands and regulatory landscapes, which vary significantly across regions and railway networks.

Further segmentation by application categorizes trains for mainline operation versus shunting duties, highlighting the variations in power demands, range requirements, and operational environments. Mainline trains require sustained high power and significant hydrogen storage for intercity or long-distance routes, whereas shunting locomotives, operating primarily within rail yards, prioritize maneuverability and frequent starts/stops with potentially smaller hydrogen systems. The component segmentation, encompassing fuel cell modules, hydrogen storage systems, power control units, and traction motors, offers insights into the core technological elements driving the market. Understanding the growth and innovation within each component segment is vital for suppliers and manufacturers to focus R&D efforts and optimize their product portfolios, ensuring the continuous improvement and cost reduction of hydrogen train technologies.

- By Type:

- Passenger Train

- Freight Train

- By Application:

- Mainline

- Shunting

- By Component:

- Fuel Cell Module

- Hydrogen Storage System

- Power Control Unit

- Traction Motor

- Cooling System

- Others

- By Region:

- North America

- Europe

- Asia Pacific (APAC)

- Latin America

- Middle East, and Africa (MEA)

Regional Highlights

- Europe: Leading the global market due to aggressive decarbonization targets, substantial government subsidies, and early adoption of hydrogen train pilot projects in countries like Germany, France, and the United Kingdom. Strong policy support and investment in hydrogen infrastructure are driving rapid commercial deployment.

- Asia Pacific (APAC): Emerging as a significant growth region, propelled by large railway networks in countries such as Japan, South Korea, and China. Extensive R&D investments, increasing environmental awareness, and government initiatives aimed at reducing emissions from the vast railway sector are fostering market expansion.

- North America: Demonstrating growing interest, particularly for freight rail applications across its extensive non-electrified networks in the United States and Canada. Federal funding and state-level incentives for clean transportation are creating opportunities for hydrogen train development and deployment.

- Latin America: A nascent market with developing interest in hydrogen fuel cell trains as a solution for modernizing aging rail infrastructure and addressing environmental concerns. Early-stage pilot projects and exploratory discussions are beginning to emerge.

- Middle East and Africa (MEA): Showing potential for future growth, driven by ambitious national visions for sustainable development and diversification of energy sources. Investments in green hydrogen production facilities could pave the way for hydrogen rail adoption in the long term, particularly in countries with significant renewable energy potential.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Hydrogen Fuel Cell Train Market.- Alstom

- Siemens Mobility

- Stadler Rail

- CAF

- Hitachi Rail

- Kawasaki Heavy Industries

- Hyundai Rotem

- CRRC Corporation Limited

- Ballard Power Systems

- Cummins Inc.

- Toyota Motor Corporation

- Toshiba Corporation

- Vossloh AG

- Talgo S.A.

- Proton Motor Fuel Cell GmbH

- PowerCell Sweden AB

- ITM Power PLC

- Plug Power Inc.

- Thales Group

Frequently Asked Questions

What are hydrogen fuel cell trains?

Hydrogen fuel cell trains are railway vehicles that use hydrogen as their primary fuel source to generate electricity, powering the train's electric motors. They combine hydrogen from onboard tanks with oxygen from the air in a fuel cell, producing electricity and water as the only byproduct, resulting in zero harmful emissions at the point of use.

What are the key benefits of hydrogen fuel cell trains?

The primary benefits include zero direct emissions, reduced noise pollution compared to diesel trains, potential for energy independence, and the ability to operate on non-electrified lines without the need for costly overhead catenary systems. They offer a sustainable solution for decarbonizing the rail sector.

What are the main challenges facing the hydrogen fuel cell train market?

Key challenges include the high initial capital expenditure for both trains and supporting infrastructure, the current limited availability of hydrogen refueling stations, the cost and scalability of green hydrogen production, and the need for evolving safety regulations and public acceptance of hydrogen technology.

How does the cost of hydrogen fuel cell trains compare to traditional trains?

Currently, hydrogen fuel cell trains have a higher upfront cost than traditional diesel trains due to the specialized technology and nascent supply chain. However, their operational costs can be competitive, especially when considering the rising cost of diesel and potential carbon taxes, along with government incentives and the long-term cost reduction from green hydrogen production at scale.

What is the future outlook for the hydrogen fuel cell train market?

The future outlook is highly positive, driven by strong global decarbonization mandates, increasing investments in hydrogen infrastructure, and continuous technological advancements. The market is projected for significant growth, with hydrogen trains becoming a viable and increasingly adopted solution for sustainable railway transportation, particularly on non-electrified routes.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted