Heavy Fuel Oil Generator Market

Heavy Fuel Oil Generator Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704411 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

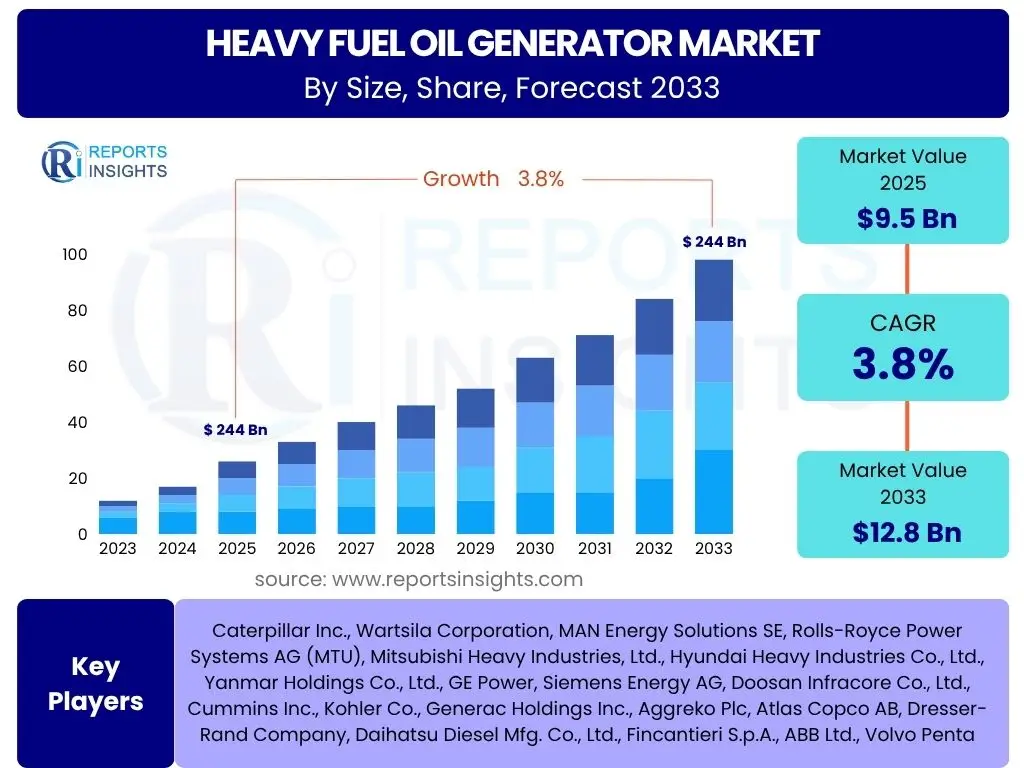

Heavy Fuel Oil Generator Market Size

According to Reports Insights Consulting Pvt Ltd, The Heavy Fuel Oil Generator Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 3.8% between 2025 and 2033. The market is estimated at USD 9.5 billion in 2025 and is projected to reach USD 12.8 billion by the end of the forecast period in 2033.

Key Heavy Fuel Oil Generator Market Trends & Insights

The Heavy Fuel Oil (HFO) generator market is experiencing a complex interplay of evolving energy policies, technological advancements, and shifting demand dynamics across various industrial and commercial sectors. A prominent trend involves the increasing demand for reliable backup power solutions in regions with unstable grid infrastructure, particularly in developing economies where rapid industrialization and urbanization necessitate robust energy supply. Despite the global push towards renewable energy sources, HFO generators continue to play a crucial role in ensuring energy security for critical operations, providing a resilient and cost-effective power generation option in specific contexts.

Another significant trend is the focus on improving the operational efficiency and emissions profile of HFO generators. Manufacturers are investing in research and development to enhance fuel combustion efficiency, reduce maintenance requirements, and integrate advanced emission control technologies to comply with increasingly stringent environmental regulations. This includes the development of more sophisticated engine management systems and exhaust gas treatment solutions, aiming to mitigate the environmental impact while retaining the operational benefits of HFO as a fuel source. The market also observes a trend towards hybrid power solutions, where HFO generators are combined with renewable energy sources like solar or wind power to create more sustainable and versatile energy systems, especially in remote or off-grid applications.

Furthermore, the maritime industry remains a significant driver for HFO generator demand, as HFO is a widely used fuel for propulsion and auxiliary power generation on large vessels. Compliance with the International Maritime Organization (IMO) 2020 regulations, which limit sulfur content in marine fuels, has led to a dual trend of adopting low-sulfur fuels or investing in exhaust gas cleaning systems (scrubbers), which in turn, impacts the operational landscape for HFO-powered marine generators. The market is also seeing a diversification of applications, with HFO generators finding utility in data centers, mining operations, and large-scale industrial plants that require continuous, high-capacity power generation independent of the main grid.

- Growing demand for reliable backup and prime power in regions with unreliable grid infrastructure.

- Increased focus on improving fuel efficiency and reducing emissions through technological advancements.

- Integration of advanced emission control systems and engine management technologies.

- Development and adoption of hybrid power solutions combining HFO with renewables.

- Continued strong demand from the maritime industry for propulsion and auxiliary power.

- Compliance with evolving international and regional environmental regulations (e.g., IMO 2020).

- Expansion of applications in energy-intensive sectors such as data centers, mining, and heavy manufacturing.

AI Impact Analysis on Heavy Fuel Oil Generator

Artificial intelligence (AI) is poised to significantly transform the heavy fuel oil generator market by enhancing operational efficiency, predictive maintenance capabilities, and overall asset management. User inquiries frequently center on how AI can reduce downtime, optimize fuel consumption, and improve the environmental footprint of these generators. AI-powered diagnostic systems can analyze vast amounts of operational data, identifying subtle anomalies that indicate potential equipment failures before they occur, thereby enabling proactive maintenance and minimizing costly unscheduled shutdowns. This shift from reactive to predictive maintenance is a key area of interest, as it directly addresses common concerns about operational reliability and maintenance costs associated with HFO generators.

Furthermore, AI algorithms can optimize fuel consumption by continuously monitoring various operational parameters such as load demand, ambient conditions, and fuel quality. By intelligently adjusting engine settings, AI can ensure that HFO generators operate at peak efficiency, leading to substantial reductions in fuel expenditure and, consequently, lower carbon emissions per unit of energy generated. Users are keen to understand how such optimization translates into tangible cost savings and improved environmental performance, especially given the volatility of HFO prices and increasing regulatory pressures regarding emissions. AI also facilitates better integration of HFO generators into microgrids and hybrid power systems, allowing for seamless energy management and load balancing, which is crucial for maximizing the benefits of diverse energy sources.

The application of AI extends to supply chain management and inventory optimization for spare parts, ensuring that critical components are available when needed, further reducing maintenance lead times. From a broader perspective, AI can contribute to more intelligent decision-making regarding generator deployment and utilization based on predicted energy demand patterns, grid stability forecasts, and fuel price trends. This strategic application of AI is vital for maximizing the return on investment for HFO generator assets and aligning their operation with evolving energy landscapes, addressing user expectations for future-proof and resilient power solutions. The ability of AI to process and interpret complex data sets offers an unprecedented level of insight into generator performance and longevity.

- Enhanced predictive maintenance: AI analyzes sensor data to forecast failures, reducing unscheduled downtime and maintenance costs.

- Optimized fuel efficiency: AI algorithms adjust engine parameters in real-time based on load and environmental conditions, leading to significant fuel savings.

- Improved operational control: AI enables remote monitoring and control, facilitating more efficient and responsive generator management.

- Smarter fault diagnosis: Rapid identification of operational issues through AI-driven analytics, minimizing diagnostic time.

- Integration with hybrid systems: AI facilitates seamless coordination between HFO generators and renewable energy sources for optimized power delivery.

- Supply chain optimization: AI assists in managing spare parts inventory and logistics, ensuring availability and reducing lead times.

- Emissions reduction: Through optimized combustion and operational efficiency, AI indirectly contributes to lower pollutant output.

Key Takeaways Heavy Fuel Oil Generator Market Size & Forecast

The Heavy Fuel Oil Generator market demonstrates a steady growth trajectory driven by the persistent global demand for reliable and continuous power, especially in regions characterized by insufficient grid infrastructure or critical industrial operations. User interest frequently revolves around the balance between the cost-effectiveness and robustness of HFO generators against the backdrop of increasing environmental scrutiny and the rise of cleaner energy alternatives. The market's projected growth indicates that despite these challenges, HFO generators retain a vital role in the global energy mix, particularly for specific niche applications where their attributes, such as high power output and ability to operate independently for extended periods, are indispensable.

A significant takeaway is the ongoing innovation within the sector, focusing on enhancing the environmental performance and operational efficiency of HFO generators. This includes advancements in fuel consumption optimization, emission control technologies, and the development of hybrid power solutions that integrate HFO generators with renewable energy sources. Such developments are crucial for the market's sustainability and future growth, addressing regulatory pressures and user concerns regarding environmental impact. The forecast reflects an expectation that strategic investments in these areas will enable HFO generators to maintain their relevance by offering a more sustainable and compliant power generation option while continuing to meet demanding industrial and commercial requirements.

Furthermore, the market's resilience is underscored by its integral role in critical infrastructure, remote locations, and the maritime sector, where the unique properties of HFO generators provide distinct advantages. The forecast suggests that while the overall growth rate might be moderate compared to some emerging renewable technologies, the consistent demand from these essential sectors will ensure a stable and predictable market expansion. This underscores the perception of HFO generators as reliable workhorses in specific power generation scenarios, a key consideration for stakeholders seeking long-term stability and assured power supply in diverse operational environments.

- Market size is projected to grow from USD 9.5 billion in 2025 to USD 12.8 billion by 2033, indicating steady expansion.

- Compound Annual Growth Rate (CAGR) of 3.8% reflects a sustained demand in specific applications and regions.

- Technological advancements in efficiency and emissions control are critical for market sustainability and growth.

- Strategic importance in remote power generation, critical infrastructure, and the maritime industry drives continued demand.

- Hybrid power solutions combining HFO with renewables represent a significant future growth avenue.

- Regulatory compliance and environmental considerations are increasingly shaping product development and market dynamics.

Heavy Fuel Oil Generator Market Drivers Analysis

The Heavy Fuel Oil Generator market is primarily driven by the escalating global demand for reliable and continuous power supply, particularly in regions with underdeveloped or unreliable grid infrastructure. Rapid industrialization, urbanization, and population growth in emerging economies necessitate robust power solutions, and HFO generators offer a proven, high-capacity option for prime or backup power. Their ability to operate independently for extended periods makes them invaluable for critical facilities such as hospitals, data centers, manufacturing plants, and mining operations, where power interruptions can result in significant economic losses or safety hazards. This fundamental requirement for energy security underpins a substantial portion of the market's demand.

Another significant driver is the cost-effectiveness of HFO as a fuel source compared to diesel in certain large-scale applications, coupled with its ready availability in many parts of the world. While HFO prices can be volatile, its lower cost per unit of energy relative to lighter distillates often makes it an economically attractive choice for high-power, continuous operation scenarios, especially in marine transport and remote industrial sites. Furthermore, the established infrastructure for HFO storage and distribution globally contributes to its widespread adoption. The flexibility of HFO generators to handle various load conditions and provide immediate power adds to their appeal in diverse industrial settings.

The continuous expansion of the maritime industry, including shipping, cruise lines, and offshore operations, acts as a consistent and substantial driver for HFO generator demand. Heavy fuel oil remains a primary fuel for marine engines and auxiliary power units due to its energy density and historical cost advantages. Despite evolving environmental regulations in the maritime sector, HFO generators, especially when paired with exhaust gas cleaning systems, continue to be a viable and widely used power solution. This enduring demand from the global shipping fleet significantly contributes to the market's stability and growth, as new vessel constructions and existing fleet upgrades necessitate reliable power generation systems.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Reliable Power in Grid-Deficient Regions | +1.5% | Africa, Southeast Asia, Latin America | Mid to Long-term (2025-2033) |

| Cost-effectiveness of HFO for High-Capacity & Continuous Operation | +0.8% | Global, particularly Industrial & Marine Sectors | Mid to Long-term (2025-2033) |

| Growth of the Global Maritime Industry and Offshore Operations | +0.7% | Global, Coastal Regions, Shipping Lanes | Mid to Long-term (2025-2033) |

| Backup Power Needs for Critical Infrastructure & Data Centers | +0.5% | North America, Europe, Asia Pacific | Short to Mid-term (2025-2029) |

Heavy Fuel Oil Generator Market Restraints Analysis

The primary restraint impacting the Heavy Fuel Oil Generator market is the increasing stringency of global environmental regulations aimed at reducing air pollutant emissions. Governments and international bodies are imposing stricter limits on sulfur oxides (SOx), nitrogen oxides (NOx), and particulate matter (PM) from HFO combustion. Compliance with these regulations often requires significant investments in exhaust gas treatment systems, such as scrubbers and selective catalytic reduction (SCR) units, or a switch to more expensive, lower-sulfur fuels. This directly increases the operational and capital expenditure for HFO generator owners, making alternative power solutions more competitive and potentially slowing down new installations or replacements.

Another significant restraint is the global push towards renewable energy sources and cleaner fuel alternatives. The rapid advancements in solar, wind, and battery storage technologies, coupled with declining costs, are making these options increasingly attractive for both grid-tied and off-grid applications. Government incentives and subsidies for renewable energy deployment further accelerate this transition, leading to a reduced reliance on traditional fossil fuel-based generation, including HFO. This competitive pressure from renewables and natural gas-fired generators, which typically have lower emissions and better public perception, limits the expansion opportunities for HFO generators, particularly in developed economies and areas with strong environmental advocacy.

Furthermore, the volatility of global crude oil prices directly impacts the cost of heavy fuel oil, introducing significant uncertainty into the operational expenses of HFO generators. Fluctuating fuel costs can erode profitability for businesses reliant on HFO for power generation, making long-term financial planning challenging. Additionally, the intensive maintenance requirements and higher operational complexities associated with HFO engines, due to the fuel's viscosity and impurities, present an ongoing operational burden. These factors, combined with concerns about public perception regarding the environmental impact of HFO, contribute to a cautious approach by potential new adopters and encourage existing users to explore alternatives where feasible.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations (SOx, NOx, PM) | -1.2% | Global, particularly Europe, North America, key Asian ports | Long-term (2025-2033) |

| Increasing Adoption of Renewable Energy Sources & Cleaner Fuels | -1.0% | Global, particularly Developed Economies | Long-term (2025-2033) |

| Volatile HFO Prices & High Operating Costs | -0.8% | Global | Mid-term (2025-2029) |

| Negative Public Perception & ESG Pressures | -0.5% | Global | Long-term (2025-2033) |

Heavy Fuel Oil Generator Market Opportunities Analysis

Despite existing challenges, significant opportunities are emerging for the Heavy Fuel Oil Generator market, primarily stemming from the demand for hybrid power solutions. Integrating HFO generators with renewable energy sources such as solar photovoltaic systems and wind turbines, coupled with battery energy storage systems (BESS), creates robust and efficient microgrids. This hybrid approach allows for reduced HFO consumption and emissions while maintaining the reliability and high power output capabilities of the HFO generator as a dispatchable power source. These solutions are particularly attractive for remote communities, islands, and off-grid industrial operations where a stable, reliable, and increasingly sustainable power supply is crucial.

Technological advancements aimed at enhancing fuel efficiency and reducing emissions present another substantial opportunity. Continuous investment in engine design improvements, advanced combustion technologies, and sophisticated exhaust gas after-treatment systems can make HFO generators more environmentally compliant and operationally competitive. For instance, the development of dual-fuel or multi-fuel engines that can seamlessly switch between HFO and cleaner fuels like LNG or even bio-fuels, offers flexibility and future-proofing against evolving regulations. These innovations cater to the growing demand for solutions that balance operational cost-effectiveness with environmental responsibility, opening new market segments and extending the lifecycle of existing HFO assets.

Furthermore, the persistent need for emergency and standby power in critical infrastructure, such as hospitals, data centers, and telecommunication hubs, provides a stable and expanding market segment. In these applications, the high power density, rapid start-up, and long run-time capabilities of HFO generators are often superior to other solutions, ensuring uninterrupted operation during grid failures. Opportunities also exist in expanding industrial sectors in developing nations, particularly mining, oil & gas, and manufacturing, which require substantial and continuous power where grid infrastructure is nascent or unreliable. Customization of HFO generator solutions to meet specific industry needs, including robust designs for harsh environments, can unlock new market potential and strengthen the market position of HFO generators.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Hybrid Power Solutions (HFO + Renewables) | +1.0% | Global, particularly Remote Areas, Islands, Developing Economies | Mid to Long-term (2025-2033) |

| Technological Advancements in Efficiency & Emissions Reduction | +0.9% | Global | Mid to Long-term (2025-2033) |

| Increasing Demand for Emergency & Standby Power in Critical Infrastructure | +0.6% | North America, Europe, Asia Pacific | Short to Mid-term (2025-2029) |

| Expansion in Underserved and Resource-Rich Developing Regions | +0.5% | Africa, Latin America, Southeast Asia | Long-term (2025-2033) |

Heavy Fuel Oil Generator Market Challenges Impact Analysis

The Heavy Fuel Oil Generator market faces significant challenges, primarily from the escalating global focus on decarbonization and the transition to cleaner energy sources. The pervasive negative perception of fossil fuels, particularly HFO due to its higher emissions profile compared to natural gas or renewables, places considerable pressure on the industry. This societal and political shift towards sustainability translates into stricter environmental policies and reduced financial incentives for HFO-based power generation. As a result, businesses and governments are increasingly hesitant to invest in new HFO generator installations, favoring greener alternatives to meet their carbon reduction commitments and improve public image. This fundamental shift in energy philosophy poses a long-term existential challenge to the market.

Compliance with rapidly evolving and increasingly stringent environmental regulations poses a continuous operational and financial challenge. Regulations like the International Maritime Organization's (IMO) 2020 sulfur cap have already forced significant changes in the marine sector, leading to increased adoption of scrubbers or a switch to more expensive low-sulfur fuels. Similar regulatory pressures are emerging for land-based HFO generator operations, mandating costly emission control technologies or even outright bans in certain urban or environmentally sensitive areas. The complexity and cost of maintaining regulatory compliance, coupled with the risk of non-compliance penalties, significantly elevate the operational burden and limit the attractiveness of HFO generators, especially for smaller operators.

Moreover, the competition from rapidly advancing and increasingly cost-effective renewable energy technologies, such as utility-scale solar and wind power, along with enhanced battery storage solutions, presents a formidable market challenge. These alternatives offer increasingly competitive levelized costs of electricity (LCOE) and a superior environmental profile. In many regions, grid-scale renewable projects are becoming the preferred choice for new power generation capacity, displacing the need for conventional fossil fuel plants. This technological displacement, combined with the inherent volatility of global oil prices which directly impacts HFO fuel costs, creates an unpredictable economic environment for HFO generator operators, making long-term planning and investment decisions precarious.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Strict Environmental Regulations and Decarbonization Pressures | -1.5% | Global | Long-term (2025-2033) |

| Intense Competition from Renewable Energy Sources and Cleaner Fuels | -1.3% | Global, particularly Developed Markets | Long-term (2025-2033) |

| Volatile Fuel Costs and Operational Complexity | -0.7% | Global | Mid-term (2025-2029) |

| Negative Public Perception and Brand Image Issues | -0.4% | Global | Long-term (2025-2033) |

Heavy Fuel Oil Generator Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Heavy Fuel Oil Generator market, detailing its current size, historical performance, and future growth projections. It encapsulates critical market dynamics, including drivers, restraints, opportunities, and challenges that shape the industry landscape. The report also highlights the impact of emerging technologies like AI on market evolution and outlines key trends, providing a strategic overview for stakeholders seeking to understand market potential and make informed investment decisions across various segments and regions globally.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 9.5 Billion |

| Market Forecast in 2033 | USD 12.8 Billion |

| Growth Rate | 3.8% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Caterpillar Inc., Wartsila Corporation, MAN Energy Solutions SE, Rolls-Royce Power Systems AG (MTU), Mitsubishi Heavy Industries, Ltd., Hyundai Heavy Industries Co., Ltd., Yanmar Holdings Co., Ltd., GE Power, Siemens Energy AG, Doosan Infracore Co., Ltd., Cummins Inc., Kohler Co., Generac Holdings Inc., Aggreko Plc, Atlas Copco AB, Dresser-Rand Company, Daihatsu Diesel Mfg. Co., Ltd., Fincantieri S.p.A., ABB Ltd., Volvo Penta |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Heavy Fuel Oil Generator market is comprehensively segmented to provide a detailed understanding of its diverse applications and operational scales. This segmentation allows for precise market analysis, identifying the specific sub-markets driving demand and revealing unique growth opportunities. By categorizing generators based on power output, application type, and end-use industry, the report offers a granular view of market dynamics and competitive landscapes across different sectors, enabling stakeholders to tailor their strategies effectively and address specific market needs. This structured approach highlights the varied roles HFO generators play in providing power across industrial, commercial, and critical infrastructure settings.

- By Power Output:

- 500 kW - 2 MW: Primarily for medium-scale industrial facilities, commercial buildings, and smaller marine vessels.

- 2 MW - 5 MW: Suited for larger industrial plants, data centers, and mid-sized power plants for prime or standby power.

- Above 5 MW: Utilized for utility-scale power generation, large industrial complexes, and very large marine vessels or offshore platforms.

- By Application:

- Prime Power: Generators serving as the primary source of electricity for continuous operation, particularly in off-grid locations.

- Standby Power: Used as an emergency power source during grid outages for critical facilities.

- Peak Shaving: Employed to reduce electricity consumption from the grid during peak demand periods, optimizing energy costs.

- By End-Use Industry:

- Marine: Powering propulsion and auxiliary systems for cargo ships, cruise liners, oil tankers, and offshore vessels.

- Industrial & Manufacturing: Providing reliable power for factories, processing plants, and heavy machinery.

- Oil & Gas: Essential for drilling operations, refineries, and offshore platforms where continuous power is critical.

- Mining: Supporting heavy machinery, ventilation systems, and infrastructure in remote mining sites.

- Commercial: Backup or prime power for large commercial complexes, shopping malls, and institutional buildings.

- Data Centers: Ensuring uninterrupted power supply for critical data storageand processing facilities.

- Others: Including applications in agriculture, construction, and remote telecommunication sites.

Regional Highlights

- Asia Pacific (APAC): Expected to be the largest and fastest-growing market due to rapid industrialization, urbanization, and a significant number of grid-deficient areas requiring reliable power solutions. Countries like India, Indonesia, Vietnam, and parts of China are witnessing substantial investments in industrial infrastructure and maritime activities, driving demand for HFO generators for prime and backup power.

- Africa: A substantial growth region for HFO generators, driven by vast energy deficits, underdeveloped power grids, and burgeoning mining and industrial sectors. The need for independent and reliable power sources in remote locations makes HFO generators a viable option across various African countries.

- Latin America: Demonstrates steady demand, particularly in countries with significant mining operations, oil & gas exploration, and a need for stable power grids. Brazil, Mexico, and Chile represent key markets where HFO generators serve critical industrial and commercial applications.

- Middle East and Africa (MEA): While oil-producing nations may have abundant natural gas, the broader MEA region, particularly parts of Africa and regions with less developed infrastructure, relies on HFO generators for industrial growth and energy security. The maritime trade routes through the Middle East also contribute to regional demand.

- North America: The market for HFO generators is more mature, with demand primarily driven by emergency standby power for critical infrastructure, data centers, and some legacy industrial applications. Stringent environmental regulations and a focus on cleaner energy alternatives moderate growth, but reliability remains a key driver.

- Europe: A mature market with a strong emphasis on environmental compliance and a rapid transition towards renewable energy. Demand for HFO generators is largely concentrated in the maritime sector (ports, shipping) and specific industrial applications where HFO is still a viable option, often accompanied by advanced emission control technologies.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Heavy Fuel Oil Generator Market.- Caterpillar Inc.

- Wartsila Corporation

- MAN Energy Solutions SE

- Rolls-Royce Power Systems AG (MTU)

- Mitsubishi Heavy Industries, Ltd.

- Hyundai Heavy Industries Co., Ltd.

- Yanmar Holdings Co., Ltd.

- GE Power

- Siemens Energy AG

- Doosan Infracore Co., Ltd.

- Cummins Inc.

- Kohler Co.

- Generac Holdings Inc.

- Aggreko Plc

- Atlas Copco AB

- Dresser-Rand Company

- Daihatsu Diesel Mfg. Co., Ltd.

- Fincantieri S.p.A.

- ABB Ltd.

- Volvo Penta

Frequently Asked Questions

What is the Heavy Fuel Oil Generator market size and its projected growth?

The Heavy Fuel Oil Generator market is estimated at USD 9.5 billion in 2025 and is projected to reach USD 12.8 billion by 2033, growing at a Compound Annual Growth Rate (CAGR) of 3.8% from 2025 to 2033.

What are the primary drivers for the Heavy Fuel Oil Generator market?

Key drivers include the increasing demand for reliable power in regions with unstable grids, the cost-effectiveness of HFO for high-capacity and continuous operations, and the sustained growth of the global maritime industry.

What are the main restraints affecting the Heavy Fuel Oil Generator market?

Major restraints include stringent global environmental regulations, the increasing adoption of renewable energy sources, volatile HFO prices, and the negative public perception associated with fossil fuels.

How does AI impact the Heavy Fuel Oil Generator market?

AI significantly impacts the market through enhanced predictive maintenance, optimized fuel efficiency, improved operational control, and smarter fault diagnosis, leading to reduced downtime and operational costs.

Which regions are key for the Heavy Fuel Oil Generator market?

Asia Pacific is expected to be the largest and fastest-growing market, with significant demand also coming from Africa, Latin America, and the Middle East, driven by industrialization and grid infrastructure needs.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted