Hydrogen Market

Hydrogen Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703901 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Hydrogen Market Size

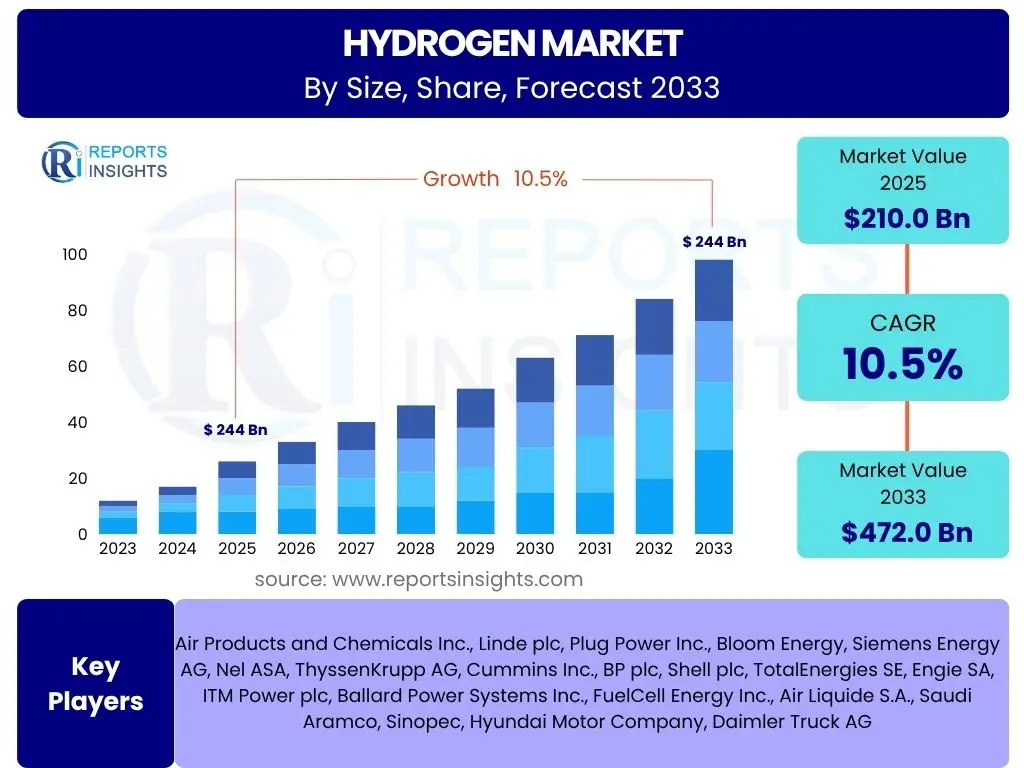

According to Reports Insights Consulting Pvt Ltd, The Hydrogen Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2033. The market is estimated at USD 210.0 Billion in 2025 and is projected to reach USD 472.0 Billion by the end of the forecast period in 2033.

Key Hydrogen Market Trends & Insights

User inquiries frequently highlight the escalating global commitment to decarbonization as a primary driver for hydrogen market expansion. Stakeholders are keen to understand how policy frameworks, technological advancements, and shifting energy paradigms are shaping the industry. The focus is particularly strong on the transition from conventional hydrogen production methods to cleaner alternatives like green and blue hydrogen, alongside the development of robust infrastructure for storage, distribution, and widespread end-use applications across various sectors.

A key area of interest revolves around the economic viability and scalability of green hydrogen, produced via renewable energy-powered electrolysis, and the role of carbon capture technologies in making blue hydrogen a transitional solution. Users are also exploring the potential for hydrogen in heavy-duty transportation, industrial processes such as steelmaking and chemicals, and power generation, seeking insights into the timelines and investment required to realize these applications. The market is witnessing a significant influx of private and public investment, signaling strong confidence in hydrogen's role in the future energy mix, prompting questions about emerging investment hotspots and collaborative ventures.

- Accelerated adoption of green hydrogen production pathways.

- Significant investments in hydrogen infrastructure development.

- Integration of hydrogen into diverse industrial and transportation applications.

- Increasing government support and policy incentives for clean hydrogen.

- Technological advancements in electrolysis and fuel cell efficiency.

AI Impact Analysis on Hydrogen

Common user questions regarding AI's impact on the hydrogen sector reveal a strong interest in how artificial intelligence can optimize production, enhance efficiency, and accelerate innovation. Users frequently inquire about AI's role in improving the electrolysis process, predicting equipment failures, and managing complex supply chains for hydrogen. There is a clear expectation that AI will be instrumental in making hydrogen production more cost-effective and environmentally friendly, addressing critical scalability challenges.

The discussions often center on AI's potential in predictive maintenance for electrolyzers and fuel cells, leading to reduced downtime and operational costs. Furthermore, users are keen to understand how AI algorithms can optimize renewable energy integration for green hydrogen production, balancing grid stability with hydrogen output. Concerns also exist about the data requirements and computational power needed for effective AI deployment, alongside the need for specialized skills within the workforce to leverage these advanced technologies. Overall, the prevailing sentiment is that AI will serve as a transformative tool, unlocking new levels of efficiency and capability across the hydrogen value chain.

- Optimization of green hydrogen production processes and energy efficiency.

- Predictive maintenance for hydrogen infrastructure and equipment.

- Enhanced demand forecasting and supply chain management for hydrogen distribution.

- Acceleration of research and development for new hydrogen materials and catalysts.

- Improved safety monitoring and risk management in hydrogen operations.

Key Takeaways Hydrogen Market Size & Forecast

User queries regarding key takeaways from the Hydrogen market size and forecast consistently highlight the market's robust growth trajectory and its pivotal role in global decarbonization efforts. There is a pervasive interest in understanding the primary drivers behind this expansion, particularly the interplay between policy support, technological innovation, and increasing industrial demand. Stakeholders are keen to discern the long-term investment opportunities and the potential for hydrogen to transform various energy-intensive sectors, offering insights into its projected market value and compound annual growth rate.

A significant aspect of user interest focuses on the anticipated shifts in the hydrogen production mix, with a strong emphasis on the scaling of green and blue hydrogen. Questions often arise about the key milestones and critical inflection points that will shape the market's evolution, including cost reductions, infrastructure build-out, and the emergence of new end-use applications. The discussions underscore the market's dynamic nature, driven by both environmental imperatives and economic incentives, indicating a collective recognition of hydrogen as a fundamental component of future sustainable energy systems.

- The hydrogen market is poised for substantial growth, driven by global decarbonization targets.

- Green hydrogen production is a central focus for future market expansion.

- Significant investments in infrastructure and technology are critical for realizing market potential.

- Policy and regulatory frameworks play a crucial role in shaping market development.

- Diversification of hydrogen applications across industrial, transportation, and power sectors is expected.

Hydrogen Market Drivers Analysis

The hydrogen market's growth is fundamentally propelled by the urgent global imperative to achieve net-zero emissions and transition to sustainable energy systems. Governments worldwide are increasingly implementing stringent environmental regulations and offering substantial incentives for clean hydrogen production and deployment. This legislative support, combined with growing corporate commitments to decarbonization, is fostering a robust demand for hydrogen across diverse industrial, transportation, and energy sectors, seeking a clean alternative to fossil fuels. The expanding recognition of hydrogen as a versatile energy carrier, capable of addressing hard-to-abate emissions in heavy industries, further strengthens its market position.

Technological advancements, particularly in electrolysis efficiency and renewable energy integration, are progressively reducing the cost of green hydrogen production, making it more competitive. Furthermore, the development of hydrogen fuel cell technologies for vehicles, power generation, and specialized industrial applications is creating new revenue streams and expanding the market's addressable opportunities. The convergence of these factors — environmental necessity, supportive policies, technological innovation, and diversifying end-uses — establishes a powerful foundation for sustained market expansion, attracting significant investment and fostering a collaborative ecosystem for hydrogen development.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Decarbonization Targets & Net-Zero Ambitions | +2.5% | Global, particularly Europe, North America, Asia Pacific | Short to Long Term (2025-2033) |

| Increasing Government Support & Policy Incentives | +2.0% | Europe (EU Hydrogen Strategy), North America (IRA, Bipartisan Infrastructure Law), Asia Pacific (Japan, South Korea, China) | Short to Mid Term (2025-2029) |

| Technological Advancements & Cost Reductions in Production | +1.8% | Global | Mid to Long Term (2027-2033) |

| Growing Demand for Hydrogen in Industrial & Transportation Sectors | +1.5% | Global, particularly heavy industry hubs & logistics corridors | Short to Long Term (2025-2033) |

| Development of Hydrogen Infrastructure for Storage & Distribution | +1.2% | Key industrial clusters & energy transition zones | Mid to Long Term (2027-2033) |

Hydrogen Market Restraints Analysis

Despite its significant potential, the hydrogen market faces several substantial restraints that could impede its rapid expansion. A primary challenge remains the high cost of production, particularly for green hydrogen, which currently often exceeds the cost of fossil fuel-based hydrogen or other energy alternatives. This cost disparity makes it difficult for green hydrogen to compete purely on an economic basis without significant subsidies or carbon pricing mechanisms, limiting its immediate widespread adoption. Furthermore, the energy intensity of hydrogen production, especially through electrolysis, can put pressure on electricity grids and requires substantial renewable energy generation capacity to ensure truly green credentials.

Another major restraint is the underdeveloped state of hydrogen infrastructure for storage, transportation, and refueling. Building out pipelines, liquefaction plants, and robust distribution networks requires massive capital investment and long lead times, creating bottlenecks for scalable deployment. Safety concerns associated with hydrogen's flammability and specific handling requirements also contribute to public apprehension and regulatory hurdles, necessitating comprehensive safety protocols and public education campaigns. These combined factors present significant barriers to achieving the scale and cost-competitiveness required for hydrogen to become a dominant energy vector.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Production Costs (Especially Green Hydrogen) | -1.5% | Global | Short to Mid Term (2025-2030) |

| Lack of Extensive Infrastructure for Storage and Distribution | -1.2% | Global, particularly emerging hydrogen economies | Short to Long Term (2025-2033) |

| Energy Intensity and Supply Chain Challenges | -0.8% | Global | Short to Mid Term (2025-2030) |

| Safety Concerns and Public Perception | -0.5% | Global, especially urban areas for refueling stations | Short to Mid Term (2025-2029) |

Hydrogen Market Opportunities Analysis

The hydrogen market presents numerous compelling opportunities driven by the global energy transition and technological innovation. A significant opportunity lies in the rapid expansion of green hydrogen production, powered by the increasing availability and decreasing cost of renewable energy. This enables the decarbonization of hard-to-abate sectors like heavy industry (steel, cement, chemicals) and long-haul transportation (shipping, aviation, heavy-duty vehicles), where direct electrification is challenging. The development of new end-use applications, such as hydrogen-fired power plants for grid balancing and hydrogen-based ammonia for agricultural fertilizers, further broadens the market scope and creates diversified revenue streams.

Furthermore, the establishment of international clean hydrogen trade corridors, facilitated by declining shipping costs for ammonia and other hydrogen carriers, represents a substantial long-term opportunity, allowing regions with abundant renewable resources to export energy. Collaboration across the value chain, from renewable energy developers and electrolyzer manufacturers to industrial consumers and infrastructure providers, is fostering innovative business models and accelerating project deployment. Government funding and international partnerships are also opening up new markets and incentivizing private sector investment, positioning hydrogen as a central component of future sustainable economic development and energy security strategies.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Green Hydrogen Production via Renewable Energy | +2.0% | Global, strong in Europe, APAC, Middle East, North America | Short to Long Term (2025-2033) |

| Decarbonization of Heavy Industry (Steel, Chemicals, Cement) | +1.8% | Europe, Asia Pacific, North America | Mid to Long Term (2028-2033) |

| Development of International Clean Hydrogen Trade Corridors | +1.5% | Global (between resource-rich and energy-importing regions) | Mid to Long Term (2030-2033) |

| New Applications in Transportation (Shipping, Aviation, Rail) | +1.0% | Global, particularly major transport hubs | Mid to Long Term (2028-2033) |

Hydrogen Market Challenges Impact Analysis

The hydrogen market faces several complex challenges that require concerted efforts for resolution. One significant hurdle is the cost competitiveness of clean hydrogen compared to established fossil fuel alternatives, particularly in the absence of robust carbon pricing or direct subsidies. Achieving significant cost reductions for green hydrogen production necessitates further technological breakthroughs in electrolyzer efficiency and durability, alongside substantial reductions in renewable energy costs and grid integration challenges. The sheer scale of investment required for deploying widespread hydrogen infrastructure, including pipelines, storage facilities, and refueling stations, poses a considerable financial and logistical challenge that demands large-scale public-private partnerships.

Another critical challenge lies in ensuring the long-term energy efficiency of the entire hydrogen value chain, from production to end-use, to minimize energy losses. Furthermore, regulatory uncertainty and the lack of harmonized international standards for hydrogen purity, safety, and certification create barriers to cross-border trade and large-scale project development. Addressing public perception and safety concerns through rigorous safety protocols, comprehensive training, and transparent communication is also vital for broad market acceptance. Successfully navigating these challenges will be crucial for the hydrogen market to realize its full potential as a key enabler of global decarbonization.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cost Competitiveness Against Conventional Fuels | -1.5% | Global | Short to Mid Term (2025-2030) |

| Scaling Up Production and Infrastructure Simultaneously | -1.3% | Global, particularly developing economies | Short to Long Term (2025-2033) |

| Ensuring Energy Efficiency Across the Value Chain | -0.9% | Global | Short to Mid Term (2025-2029) |

| Regulatory Uncertainty and Lack of Standardized Frameworks | -0.7% | Global, particularly for international trade | Short to Mid Term (2025-2029) |

Hydrogen Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the global hydrogen market, offering detailed insights into market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. The scope encompasses a thorough examination of production methods, end-use applications, and strategic developments shaping the industry, presenting a forward-looking perspective on market dynamics and future growth prospects to aid strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 210.0 Billion |

| Market Forecast in 2033 | USD 472.0 Billion |

| Growth Rate | 10.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Air Products and Chemicals Inc., Linde plc, Plug Power Inc., Bloom Energy, Siemens Energy AG, Nel ASA, ThyssenKrupp AG, Cummins Inc., BP plc, Shell plc, TotalEnergies SE, Engie SA, ITM Power plc, Ballard Power Systems Inc., FuelCell Energy Inc., Air Liquide S.A., Saudi Aramco, Sinopec, Hyundai Motor Company, Daimler Truck AG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The hydrogen market is segmented based on critical factors that influence its production, distribution, and end-use, providing a granular view of market dynamics. These segmentations are crucial for understanding the diverse pathways and applications that contribute to the market's overall growth and evolution. The primary segmentations include analysis by production method, which differentiates between traditional fossil fuel-based hydrogen and emerging clean hydrogen varieties; by application, detailing its use across various sectors from industrial feedstock to energy generation and transportation; by end-use industry, identifying specific sectors that are adopting hydrogen; and by storage and distribution, highlighting the infrastructure developments necessary for its widespread adoption. This multi-dimensional segmentation offers a comprehensive framework for assessing market opportunities and challenges across the value chain.

- By Production Method: Grey Hydrogen, Blue Hydrogen, Green Hydrogen (Alkaline Electrolyzer, PEM Electrolyzer, SOEC Electrolyzer), Other Production Methods

- By Application: Energy (Power Generation, Fuel Cells), Industrial Feedstock (Ammonia Production, Methanol Production, Refining, Steel & Iron Manufacturing, Other Industrial Applications), Transportation (Fuel Cell Electric Vehicles - FCEV, Shipping, Aviation, Rail), Building Heating & Power

- By End-Use Industry: Chemical, Refineries, Metal Processing, Glass, Electronics, Food & Beverage, Automotive, Power Generation, Others

- By Storage and Distribution: Compression, Liquefaction, Pipeline Transport, Storage Tanks

- By Region: North America, Europe, Asia Pacific, Latin America, Middle East, and Africa

Regional Highlights

- North America: Driven by significant policy support, particularly in the United States through the Inflation Reduction Act, fostering investments in clean hydrogen production and infrastructure development. Canada is also emerging as a key player with abundant renewable resources.

- Europe: Leading the global charge for green hydrogen, propelled by ambitious decarbonization targets, comprehensive hydrogen strategies from the European Union and individual member states, and substantial public and private funding for electrolysis and fuel cell projects.

- Asia Pacific (APAC): Expected to witness robust growth due to rising industrial demand, government initiatives (e.g., in Japan, South Korea, China, and Australia), and increasing efforts to reduce carbon emissions from energy-intensive industries and transportation.

- Middle East & Africa (MEA): Positioning itself as a future global hub for green hydrogen exports, leveraging abundant solar resources and significant capital investment from energy companies and sovereign wealth funds to develop large-scale production facilities.

- Latin America: Holds significant potential for green hydrogen production, especially in countries with vast renewable energy resources like Chile and Brazil, attracting international investments for export-oriented projects.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Hydrogen Market.- Air Products and Chemicals Inc.

- Linde plc

- Plug Power Inc.

- Bloom Energy

- Siemens Energy AG

- Nel ASA

- ThyssenKrupp AG

- Cummins Inc.

- BP plc

- Shell plc

- TotalEnergies SE

- Engie SA

- ITM Power plc

- Ballard Power Systems Inc.

- FuelCell Energy Inc.

- Air Liquide S.A.

- Saudi Aramco

- Sinopec

- Hyundai Motor Company

- Daimler Truck AG

Frequently Asked Questions

What is green hydrogen and why is it important?

Green hydrogen is produced by splitting water molecules into hydrogen and oxygen using electrolysis powered by renewable electricity sources, such as solar or wind. Its importance stems from its near-zero carbon emissions during production, making it a critical component for decarbonizing hard-to-abate sectors like heavy industry, long-haul transportation, and power generation, significantly contributing to global net-zero targets.

What are the main applications of hydrogen in the market?

Hydrogen has diverse applications across various sectors. In industry, it is a crucial feedstock for ammonia and methanol production, oil refining, and emerging green steel manufacturing. In transportation, it fuels fuel cell electric vehicles (FCEVs), and is being explored for shipping, aviation, and rail. It also serves as an energy carrier for power generation, grid balancing, and can be used for building heating.

What factors are primarily driving the growth of the hydrogen market?

The hydrogen market's growth is primarily driven by escalating global decarbonization efforts, increasing government support through policies and incentives, significant technological advancements reducing production costs, and rising demand from energy-intensive industrial and transportation sectors seeking cleaner alternatives. Expanding infrastructure for storage and distribution also plays a vital role.

What are the biggest challenges facing the widespread adoption of hydrogen?

Key challenges include the high production costs of clean hydrogen, particularly green hydrogen, compared to fossil fuel alternatives. Other significant hurdles are the underdeveloped infrastructure for storage and distribution, energy efficiency losses across the value chain, and the need for harmonized regulatory frameworks and safety standards to facilitate large-scale deployment and public acceptance.

What role do governments and policies play in the hydrogen market's development?

Governments and their policies play a pivotal role in accelerating the hydrogen market's development by providing substantial financial incentives, grants, and tax credits for clean hydrogen production and infrastructure. They also establish national hydrogen strategies, set emissions targets, and implement regulatory frameworks that foster investment, stimulate demand, and create a conducive environment for innovation and market growth.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted