Green Hydrogen Market

Green Hydrogen Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703618 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

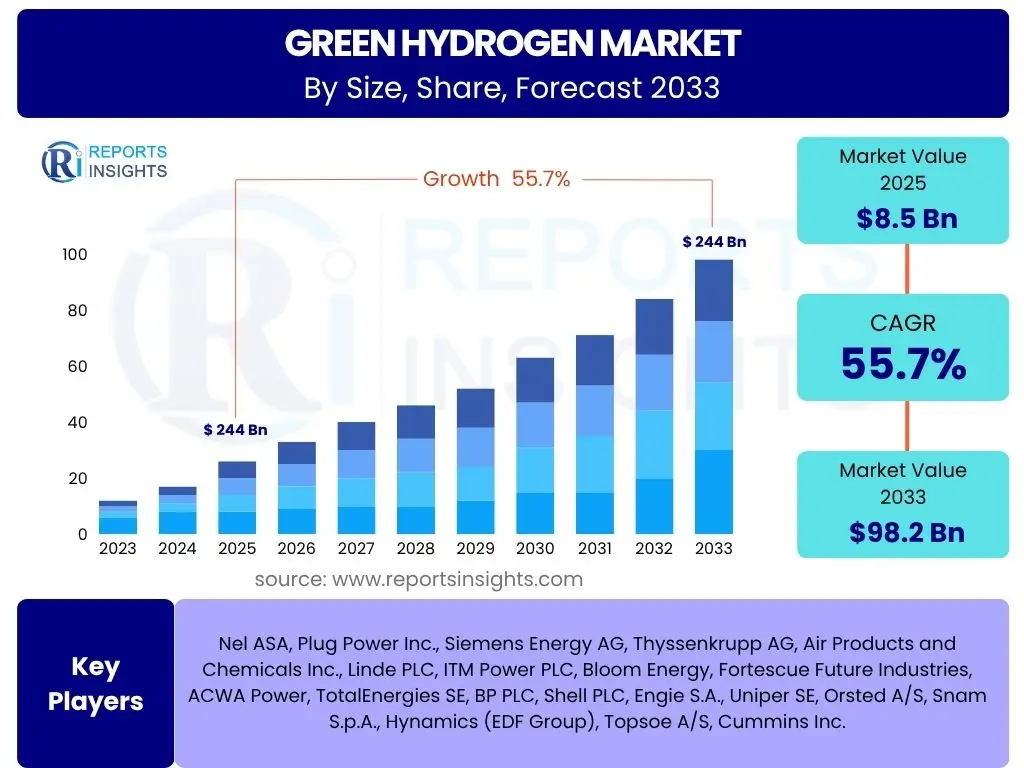

Green Hydrogen Market Size

According to Reports Insights Consulting Pvt Ltd, The Green Hydrogen Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 55.7% between 2025 and 2033. The market is estimated at USD 8.5 Billion in 2025 and is projected to reach USD 98.2 Billion by the end of the forecast period in 2033.

Key Green Hydrogen Market Trends & Insights

The Green Hydrogen market is experiencing dynamic shifts driven by a global commitment to decarbonization and energy transition. Significant trends indicate a rapid expansion fueled by supportive policy frameworks, advancements in renewable energy technologies, and increasing corporate sustainability initiatives. There is a growing emphasis on developing large-scale electrolyzer manufacturing capabilities and integrating green hydrogen into diverse industrial and energy sectors to replace fossil fuels. This evolving landscape highlights a collective push towards achieving net-zero emissions through sustainable hydrogen production.

Market insights suggest a strong focus on reducing the levelized cost of hydrogen (LCOH) through economies of scale and technological innovations. Investment in hydrogen infrastructure, including pipelines, storage, and refueling stations, is accelerating across key regions. Furthermore, strategic collaborations between energy companies, industrial players, and technology providers are becoming prevalent, aiming to establish comprehensive green hydrogen ecosystems. The market is also witnessing a trend towards regional hydrogen hubs, optimizing production and consumption within specific industrial clusters.

- Increasing government support and policy incentives for clean hydrogen production.

- Significant reduction in renewable energy costs, making green hydrogen more competitive.

- Rapid scaling up of electrolyzer manufacturing capacities globally.

- Growing corporate demand for decarbonization solutions in hard-to-abate sectors.

- Development of international trade routes and supply chains for green hydrogen.

- Emergence of large-scale green hydrogen projects and dedicated production facilities.

- Integration of green hydrogen into existing energy grids and industrial processes.

- Focus on innovation in hydrogen storage and transportation technologies.

AI Impact Analysis on Green Hydrogen

Artificial intelligence is poised to significantly optimize various aspects of the green hydrogen value chain, addressing common user questions related to efficiency, cost reduction, and operational complexity. AI algorithms can enhance the efficiency of electrolyzers by monitoring operational parameters in real-time and predicting maintenance needs, thereby reducing downtime and extending equipment lifespan. Furthermore, AI can optimize the integration of intermittent renewable energy sources, such as wind and solar, with electrolyzers to ensure a stable and cost-effective hydrogen supply, directly impacting the economic viability of green hydrogen production.

The application of AI extends to improving the design and scalability of green hydrogen plants, leveraging data analytics for site selection, resource assessment, and process optimization. Users are keen on how AI can streamline supply chain management, from hydrogen production to distribution and end-use, by forecasting demand, managing logistics, and optimizing transportation routes. Moreover, AI-driven simulations can accelerate research and development efforts, enabling faster innovation in materials science for electrolyzers and fuel cells, ultimately contributing to a more robust and cost-efficient green hydrogen economy.

- Enhanced electrolyzer efficiency and predictive maintenance through real-time data analysis.

- Optimized integration of renewable energy sources for stable hydrogen production.

- Improved plant design and operational efficiency through AI-driven simulations.

- Streamlined supply chain management and logistics for hydrogen distribution.

- Accelerated research and development in materials and processes for hydrogen technologies.

- Better demand forecasting and energy management for hydrogen applications.

- Reduced operational costs through autonomous control systems and smart automation.

- Advanced safety monitoring and risk management in hydrogen infrastructure.

Key Takeaways Green Hydrogen Market Size & Forecast

The Green Hydrogen market is on a trajectory of unprecedented growth, driven by a confluence of global decarbonization targets, supportive governmental policies, and significant advancements in renewable energy technologies. The substantial projected CAGR from 2025 to 2033 underscores the market's emergence as a cornerstone of the future energy landscape. This rapid expansion is not merely speculative but is grounded in tangible investments, expanding production capacities, and increasing cross-sectoral adoption, highlighting its critical role in achieving net-zero emissions.

Key insights reveal that while initial capital expenditures remain a challenge, the declining costs of renewable energy and the scaling of electrolyzer technologies are rapidly improving the economic viability of green hydrogen. The market forecast indicates a strong shift towards hydrogen as a versatile energy carrier, particularly in hard-to-abate sectors like heavy industry, long-haul transportation, and chemical production. This growth signifies a global commitment to sustainable energy solutions, positioning green hydrogen as a pivotal component of the global energy transition strategy.

- The market is poised for exponential growth, reflecting strong global commitment to decarbonization.

- Significant investments in renewable energy infrastructure are underpinning green hydrogen expansion.

- Technological advancements in electrolyzers are driving down production costs and increasing efficiency.

- Policy support and incentive programs are crucial catalysts for market acceleration.

- Green hydrogen is becoming indispensable for decarbonizing heavy industries and transportation.

- Regional hydrogen hubs and international collaborations are fostering ecosystem development.

- The long-term outlook for green hydrogen is highly positive, driven by sustained demand for clean energy.

Green Hydrogen Market Drivers Analysis

The significant growth in the Green Hydrogen market is primarily propelled by escalating global pressure to reduce carbon emissions and achieve climate targets. Governments worldwide are implementing ambitious decarbonization strategies, recognizing green hydrogen as a key enabler for transitioning away from fossil fuels in challenging sectors. This has led to the introduction of various supportive policies, subsidies, and incentives aimed at accelerating the production, adoption, and infrastructure development for green hydrogen, creating a favorable investment climate for project developers and technology providers.

Furthermore, the decreasing costs of renewable energy sources, particularly solar and wind power, are making the production of green hydrogen more economically viable. As the primary input for green hydrogen, affordable renewable electricity is directly lowering production costs, enhancing its competitiveness against conventional gray hydrogen. Coupled with growing corporate sustainability commitments and increasing demand from industries seeking to reduce their carbon footprint, these factors collectively drive significant investment and innovation across the green hydrogen value chain.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Government Policies and Incentives | +1.8% | Europe, North America, Asia Pacific | Short to Mid-term (2025-2030) |

| Declining Renewable Energy Costs | +1.5% | Global | Mid-term (2025-2030) |

| Increasing Demand for Decarbonization | +1.2% | Global, particularly Industrial Hubs | Mid to Long-term (2028-2033) |

| Technological Advancements in Electrolyzers | +1.0% | Global (with R&D concentration in developed regions) | Short to Mid-term (2025-2030) |

| Growth in Corporate ESG Initiatives | +0.8% | North America, Europe | Mid to Long-term (2028-2033) |

Green Hydrogen Market Restraints Analysis

Despite its significant potential, the Green Hydrogen market faces several key restraints that could impede its rapid expansion. One of the primary barriers is the high initial capital expenditure required for green hydrogen production facilities, including electrolyzers and dedicated renewable energy infrastructure. The substantial upfront investment, coupled with operational costs related to electricity consumption and maintenance, makes green hydrogen less cost-competitive compared to established fossil fuel alternatives or even other forms of hydrogen production in certain applications.

Another significant restraint is the underdeveloped infrastructure for hydrogen storage, transportation, and distribution. Current pipeline networks are limited, and alternative methods like cryogenic liquefaction or chemical carriers are energy-intensive and expensive. Furthermore, the intermittent nature of renewable energy sources necessitates robust energy storage solutions or flexible electrolyzer operations, adding to the complexity and cost of ensuring a consistent green hydrogen supply. Regulatory uncertainties and the lack of standardized certification schemes across different regions also pose challenges for international trade and market harmonization.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Production Costs (CAPEX and OPEX) | -1.5% | Global | Short to Mid-term (2025-2030) |

| Limited Hydrogen Infrastructure | -1.3% | Global (particularly emerging markets) | Short to Mid-term (2025-2030) |

| Competition from Conventional Hydrogen | -1.0% | Global (industrial sectors) | Short to Mid-term (2025-2030) |

| Regulatory and Permitting Complexities | -0.8% | North America, Europe | Short-term (2025-2027) |

| Water Availability and Management | -0.5% | Arid regions, high-stress water areas | Mid to Long-term (2028-2033) |

Green Hydrogen Market Opportunities Analysis

The Green Hydrogen market presents substantial opportunities stemming from the global imperative for deep decarbonization across various sectors. The most significant opportunity lies in replacing fossil fuels in hard-to-abate industries such as steel, chemicals, ammonia, and cement production, where electrification is challenging or not feasible. Green hydrogen can serve as a clean feedstock or fuel, enabling these industries to achieve significant emission reductions and comply with stricter environmental regulations, opening up vast new markets for its application.

Another major opportunity is the development of a robust international trade market for green hydrogen and its derivatives (e.g., green ammonia, green methanol). Regions with abundant renewable energy resources can become major exporters, supplying energy-poor but demand-rich industrial centers globally. Furthermore, the increasing integration of green hydrogen into power grids, serving as a long-duration energy storage solution or a flexible power source, presents a significant avenue for market expansion. The development of hydrogen-powered mobility solutions, especially for heavy-duty transport, shipping, and aviation, also offers considerable growth prospects as these sectors seek alternatives to conventional fuels.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Decarbonization of Heavy Industry | +1.2% | Europe, Asia Pacific, North America | Mid to Long-term (2028-2033) |

| Development of Hydrogen Export Markets | +1.0% | Middle East, Australia, Latin America, North Africa | Long-term (2030-2033) |

| Integration into Energy Storage and Grid Balancing | +0.9% | Europe, North America, Asia Pacific | Mid to Long-term (2028-2033) |

| Expansion of Hydrogen Mobility (Heavy-Duty) | +0.8% | North America, Europe, China, Japan, Korea | Mid-term (2025-2030) |

| Power-to-X Applications (e.g., Synfuels) | +0.7% | Europe, Asia Pacific | Long-term (2030-2033) |

Green Hydrogen Market Challenges Impact Analysis

The Green Hydrogen market faces several significant challenges that necessitate concerted efforts from stakeholders to overcome. A primary concern is the scalability of green hydrogen production to meet future demand, which requires a massive build-out of renewable energy capacity and electrolyzer manufacturing. Ensuring the availability of sufficient renewable electricity at competitive prices, especially for large-scale projects, remains a considerable hurdle. The intermittency of renewable sources also demands sophisticated grid integration and energy management solutions to ensure stable hydrogen output.

Another critical challenge revolves around the safety aspects of hydrogen, including its storage, handling, and transportation. Developing and implementing stringent safety standards and protocols across the entire value chain is essential to gain public acceptance and facilitate widespread adoption. Furthermore, the current lack of a global, harmonized regulatory framework and certification schemes for green hydrogen can hinder cross-border trade and investment. Securing adequate financing for large, capital-intensive projects and navigating complex permitting processes also presents notable barriers for project developers in an emerging industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Scalability and Project Financing | -1.0% | Global | Short to Mid-term (2025-2030) |

| Infrastructure Development Bottlenecks | -0.9% | Global | Short to Mid-term (2025-2030) |

| Safety Concerns and Public Perception | -0.7% | Global (particularly urban areas) | Short to Mid-term (2025-2030) |

| Lack of Harmonized Regulatory Frameworks | -0.6% | International Trade | Short to Mid-term (2025-2030) |

| Efficient Storage and Transport Solutions | -0.5% | Global | Mid-term (2025-2030) |

Green Hydrogen Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Green Hydrogen market, encompassing historical data, current market dynamics, and future growth projections from 2025 to 2033. It offers detailed insights into market size, segmentation across various technologies and end-use applications, regional trends, and the competitive landscape. The scope includes a thorough examination of market drivers, restraints, opportunities, and challenges, providing stakeholders with a holistic understanding of the market's potential and complexities. The report also highlights the impact of emerging technologies and policy developments on market evolution, offering strategic foresight for industry participants.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 8.5 Billion |

| Market Forecast in 2033 | USD 98.2 Billion |

| Growth Rate | 55.7% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Nel ASA, Plug Power Inc., Siemens Energy AG, Thyssenkrupp AG, Air Products and Chemicals Inc., Linde PLC, ITM Power PLC, Bloom Energy, Fortescue Future Industries, ACWA Power, TotalEnergies SE, BP PLC, Shell PLC, Engie S.A., Uniper SE, Orsted A/S, Snam S.p.A., Hynamics (EDF Group), Topsoe A/S, Cummins Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Green Hydrogen market is meticulously segmented to provide a granular understanding of its diverse components and growth opportunities. This segmentation considers various aspects, including the underlying production technologies, specific end-use applications, and the methodologies employed for hydrogen generation. Such a detailed breakdown enables stakeholders to identify niche markets, assess technological preferences, and strategically position themselves within the rapidly evolving green hydrogen ecosystem, reflecting the complexity and multi-faceted nature of the industry.

- By Technology: Identifies the prevalent electrolyzer types shaping production.

- Alkaline Electrolyzer: Mature technology, lower CAPEX, larger scale.

- PEM Electrolyzer: High efficiency, flexible operation, faster response time.

- Solid Oxide Electrolyzer (SOEC): High efficiency at high temperatures, potential for co-production.

- Anion Exchange Membrane (AEM) Electrolyzer: Emerging technology, combines benefits of Alkaline and PEM.

- Other Electrolyzer Technologies: Includes various pilot and experimental technologies.

- By Application: Categorizes demand based on where green hydrogen is utilized.

- Power Generation: For energy storage, grid balancing, and direct power production.

- Transportation: Fuel for heavy-duty vehicles, maritime vessels, and potential aviation.

- Industrial Feedstock: Replacement for gray hydrogen in ammonia, methanol, steel, and refinery processes.

- Building Heating and Power: For heating residential and commercial buildings.

- Other Applications: Includes various niche and emerging uses.

- By End Use: Further refines application areas by final consumption sector.

- Mobility: Direct use in fuel cell electric vehicles and other transport modes.

- Power: Conversion back to electricity, energy storage solutions.

- Industrial: Process heat, chemical feedstock, reducing agent.

- Grid Injection: Blending hydrogen into natural gas pipelines.

- By Production Method: Distinguishes hydrogen generation based on the renewable energy source.

- Solar Electrolysis: Using solar PV power for water electrolysis.

- Wind Electrolysis: Using wind power for water electrolysis.

- Hydro Electrolysis: Utilizing hydropower for green hydrogen production.

- Geothermal Electrolysis: Leveraging geothermal energy as a power source.

- Biomass Electrolysis: Using biomass-derived electricity for electrolysis.

Regional Highlights

- North America: Driven by significant policy support, particularly the Inflation Reduction Act (IRA) in the United States, which offers substantial tax credits for clean hydrogen production. Focus on developing regional hydrogen hubs and decarbonizing industrial sectors and heavy-duty transport. Canada also has ambitious hydrogen strategies and abundant renewable resources.

- Europe: A leading region with ambitious hydrogen strategies (e.g., REPowerEU, European Green Deal). Strong focus on industrial decarbonization, hydrogen valley development, and cross-border infrastructure. Germany, Netherlands, France, and Spain are at the forefront of project development and policy implementation, aiming to reduce reliance on fossil fuel imports.

- Asia Pacific (APAC): Emerging as a major demand and supply hub. Countries like Japan, South Korea, China, and Australia are investing heavily in green hydrogen for industrial applications, power generation, and export. Australia and India have significant renewable energy potential, positioning them as future major exporters. China's scale of renewable deployment is expected to drive down costs.

- Middle East and Africa (MEA): Possessing vast untapped renewable energy resources (solar and wind), this region is poised to become a significant global exporter of green hydrogen and its derivatives. Countries like Saudi Arabia, UAE, and Oman are investing billions in large-scale green hydrogen projects targeting international markets. Africa's potential, particularly in North and Southern Africa, is immense for domestic use and export to Europe.

- Latin America: Countries like Chile and Brazil are rapidly advancing their green hydrogen strategies due to abundant renewable energy resources (solar, wind, hydropower). Chile aims to become a leading exporter, leveraging its exceptional Patagonia wind resources. The region is focusing on industrial applications and potential export to global markets.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Green Hydrogen Market.- Leading Electrolyzer Manufacturers

- Integrated Energy Developers

- Industrial Gas Suppliers

- Renewable Energy Project Developers

- Engineering and Construction Firms

- Fuel Cell Technology Providers

- Oil and Gas Majors (transitioning to clean energy)

- Utilities and Power Generators

- Chemical and Manufacturing Companies

- Specialized Hydrogen Infrastructure Developers

- Heavy Industry Enterprises

- Maritime and Logistics Companies

- Automotive and Transport Solution Providers

- Research and Development Institutions

- Government-backed Energy Initiatives

Frequently Asked Questions

What is Green Hydrogen?

Green hydrogen is hydrogen produced through electrolysis of water, powered by electricity generated from renewable energy sources such as solar, wind, or hydropower, resulting in near-zero carbon emissions during production.

How is Green Hydrogen Produced?

Green hydrogen is produced by passing an electric current through water (H2O) in an electrolyzer. This process, called electrolysis, splits water into hydrogen (H2) and oxygen (O2). The electricity used for this process must come exclusively from renewable energy sources to be classified as green hydrogen.

What are the primary uses of Green Hydrogen?

Green hydrogen is primarily used for decarbonizing hard-to-abate sectors like heavy industry (steel, chemicals, ammonia), long-haul transportation (trucks, ships, aviation), power generation (energy storage, grid balancing), and as a clean fuel for heating and power generation in buildings.

What are the main challenges for the Green Hydrogen market?

The main challenges include high initial production costs, the need for extensive infrastructure development for storage and transportation, ensuring scalability to meet demand, developing clear regulatory frameworks, and addressing safety concerns associated with hydrogen handling.

What is the outlook for the Green Hydrogen market?

The outlook for the green hydrogen market is highly positive, driven by strong global decarbonization targets, increasing government support, declining renewable energy costs, and technological advancements. The market is projected for exponential growth, becoming a crucial component of the global energy transition strategy.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted