HSR Composite Market

HSR Composite Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710400 | Last Updated : January 05, 2026 |

Format : ![]()

![]()

![]()

![]()

HSR Composite Market Size

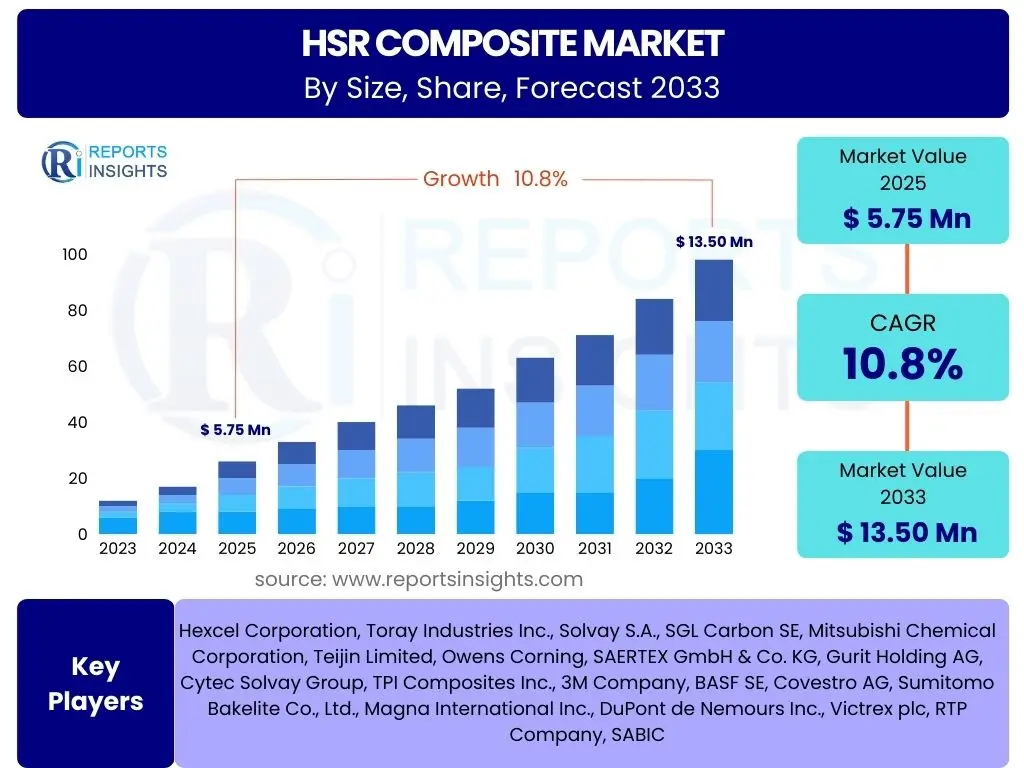

According to Reports Insights Consulting Pvt Ltd, The HSR Composite Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.8% between 2025 and 2033. The market is estimated at USD 5.75 Billion in 2025 and is projected to reach USD 13.50 Billion by the end of the forecast period in 2033.

Key HSR Composite Market Trends & Insights

The HSR Composite market is undergoing significant transformation driven by a confluence of technological advancements, evolving application demands, and a heightened focus on sustainability. Industry stakeholders are keenly observing shifts towards advanced material formulations that offer enhanced performance characteristics, alongside the integration of smart manufacturing processes. A key trend involves the relentless pursuit of lightweighting solutions across sectors like aerospace, automotive, and wind energy, where superior strength-to-weight ratios are critical for efficiency and operational performance. This drive is further augmented by innovations in fiber and resin technologies, pushing the boundaries of material properties.

Another prominent insight is the growing emphasis on sustainable and circular economy practices within the composite industry. Manufacturers are increasingly investing in research and development for bio-based resins, recycled fibers, and more efficient manufacturing techniques that reduce waste and energy consumption. This not only aligns with global environmental goals but also addresses regulatory pressures and consumer preferences for greener products. Furthermore, the market is witnessing an uptick in the adoption of automation and digitalization across the production lifecycle, from design and simulation to fabrication and quality control, leading to improved consistency, reduced costs, and faster time-to-market for complex composite structures.

- Increased adoption of advanced thermoplastic composites for enhanced recyclability and repairability.

- Growing demand for multi-material hybrid composite structures to optimize performance and cost.

- Integration of smart manufacturing processes, including automation and digital twins, for improved production efficiency.

- Development of sustainable and bio-based composite materials to meet environmental regulations and consumer preferences.

- Expansion of additive manufacturing (3D printing) for complex HSR composite geometries and rapid prototyping.

AI Impact Analysis on HSR Composite

The advent of Artificial Intelligence (AI) is poised to revolutionize the HSR Composite market, addressing complex challenges in material design, manufacturing, and operational maintenance. Users frequently inquire about how AI can optimize the typically intricate and resource-intensive processes associated with high-strength, high-stiffness resin composites. AI's capabilities in data analysis and pattern recognition are particularly valuable for predicting material performance, simulating manufacturing defects, and streamlining design iterations. This translates into faster development cycles, reduced material waste, and the creation of novel composite structures with previously unattainable properties, directly responding to the demand for innovation and efficiency.

Beyond design and manufacturing, AI is also anticipated to significantly enhance the in-service performance and longevity of HSR Composite components. Predictive maintenance, powered by AI algorithms, allows for the early detection of structural anomalies or wear, enabling timely interventions that prevent catastrophic failures and extend the operational life of assets in critical applications such as aerospace or high-speed rail. Furthermore, AI-driven quality control systems can monitor production lines in real-time, identifying deviations and ensuring consistent product quality, which is paramount for safety-critical composite applications. While the integration presents opportunities for substantial cost savings and performance gains, concerns regarding data privacy, algorithm bias, and the need for specialized AI expertise within the composite sector remain areas of focus for industry stakeholders.

- AI-driven generative design for optimized composite structures and material layups.

- Predictive maintenance analytics for HSR composite components, extending asset lifespan.

- Enhanced quality control and defect detection through AI-powered visual inspection systems.

- Supply chain optimization for raw materials and finished composite products using machine learning.

- Development of smart composites with integrated sensors and AI for real-time performance monitoring.

Key Takeaways HSR Composite Market Size & Forecast

The HSR Composite market is on a robust growth trajectory, demonstrating its critical role in advanced industrial applications where performance, lightweighting, and durability are paramount. A primary takeaway is the consistent demand from high-growth sectors such as aerospace & defense, automotive, and wind energy, which are continually seeking materials that offer superior strength-to-weight ratios and enhanced fatigue resistance. This sustained demand underpins the market's significant Compound Annual Growth Rate, indicating a strong positive outlook for investments and innovation within the industry. The forecast underscores the strategic importance of composites in enabling next-generation technologies and infrastructure.

Another crucial insight derived from the market size and forecast is the increasing geographical diversification of production and consumption. While established markets in North America and Europe continue to drive innovation and high-value applications, the Asia Pacific region is rapidly emerging as a dominant force in both manufacturing capacity and end-use demand, particularly in automotive and construction. This shift necessitates a global strategic approach for market participants, focusing on localized supply chains and understanding regional regulatory landscapes. The projected market value by 2033 highlights the long-term potential for advanced composites to displace traditional materials across an expanding array of applications, reinforcing their status as a foundational element of modern engineering.

- The HSR Composite market is poised for significant expansion, driven by high-performance material demand across key industries.

- Aerospace & Defense and Automotive sectors remain primary growth engines due to stringent lightweighting and performance requirements.

- Sustainability and recyclability initiatives are increasingly influencing material selection and manufacturing processes, presenting both challenges and opportunities.

- Technological advancements in manufacturing processes, including automation and AI, are crucial for cost reduction and scalability.

- Asia Pacific is projected to be a key growth region, offering substantial market opportunities due to rapid industrialization and infrastructure development.

HSR Composite Market Drivers Analysis

The HSR Composite market is propelled by several robust drivers, fundamentally rooted in the intrinsic advantages that composite materials offer over conventional ones. The increasing demand for lightweight and high-strength materials across various industries is arguably the most significant catalyst. Sectors like aerospace and automotive are under constant pressure to improve fuel efficiency, reduce emissions, and enhance performance, which directly benefits from the superior strength-to-weight ratio of composites. This not only aids in meeting stringent regulatory standards but also contributes to better operational dynamics and reduced lifetime costs for end-products.

Furthermore, the rapid advancements in manufacturing technologies, including automation, additive manufacturing, and advanced process controls, are making HSR Composites more cost-effective and scalable. These innovations address historical challenges related to production complexity and high initial investment, thereby broadening the application scope of composites. The expanding application base in emerging areas such as urban air mobility, renewable energy (specifically larger and more efficient wind turbine blades), and advanced sporting goods also significantly contributes to market expansion. The continuous push for material innovation, leading to composites with improved durability, fatigue resistance, and functional integration, ensures their competitive edge and sustained market penetration.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Lightweight Materials | +3.2% | Global, particularly North America, Europe, Asia Pacific | Short to Long-term |

| Technological Advancements in Manufacturing Processes | +2.8% | Global, strong in developed economies | Mid-term |

| Growing Adoption in Aerospace & Defense | +2.5% | North America, Europe, China | Long-term |

| Expansion in Wind Energy Sector | +2.1% | Europe, Asia Pacific, North America | Mid to Long-term |

| Strict Environmental Regulations for Fuel Efficiency | +1.5% | Europe, North America, Japan | Short to Mid-term |

HSR Composite Market Restraints Analysis

Despite its significant growth potential, the HSR Composite market faces several inherent restraints that temper its expansion. One of the primary challenges is the relatively high manufacturing cost associated with advanced composites. The raw materials, such as carbon fibers and specialized resins, are often more expensive than traditional materials like steel or aluminum. Furthermore, the specialized processing techniques required, including complex layup procedures, curing cycles, and stringent quality control, demand significant capital investment in machinery and skilled labor, which can be a barrier to entry for new players and can inflate the final product cost, especially for high-volume applications.

Another significant restraint is the complexity and cost associated with recycling HSR Composites. Unlike metals that can be easily melted and reused, thermoset composites are difficult to separate into their constituent fibers and resins, making circular economy initiatives challenging. While advancements are being made in mechanical and chemical recycling, these processes are often energy-intensive and not yet fully economically viable on a large scale. Additionally, the long qualification and certification processes, particularly in safety-critical sectors like aerospace, can delay the adoption of new composite materials and designs, hindering innovation and market penetration. Supply chain volatility for key raw materials also poses a risk, impacting production schedules and material costs.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing and Raw Material Costs | -2.8% | Global | Short to Mid-term |

| Challenges in Recycling and Disposal | -2.0% | Europe, North America | Mid to Long-term |

| Complexity of Manufacturing Processes | -1.7% | Global | Short-term |

| Lengthy Qualification and Certification Procedures | -1.5% | Aerospace & Defense-focused regions (NA, EU) | Long-term |

| Volatility in Raw Material Supply Chain | -1.0% | Global | Short-term |

HSR Composite Market Opportunities Analysis

The HSR Composite market is rich with opportunities stemming from an evolving technological landscape and expanding application horizons. One significant opportunity lies in the burgeoning demand from new and emerging applications beyond traditional aerospace and automotive sectors. Areas such as urban air mobility (UAM), advanced defense systems, and highly specialized industrial machinery are increasingly recognizing the unparalleled performance benefits of composites, opening up new revenue streams and market segments. These applications often require materials that can withstand extreme conditions while remaining exceptionally lightweight, a niche perfectly served by HSR Composites.

Furthermore, the continuous innovation in material science presents another substantial opportunity. Developments in thermoplastic composites, bio-based resins, and smart composites with integrated functionalities are expanding the capabilities and appeal of these materials. Thermoplastics, for instance, offer advantages in recyclability and faster processing times, addressing some of the key restraints of traditional thermosets. Additionally, the increasing focus on automation and digitalization in manufacturing processes, including the adoption of Industry 4.0 principles, promises to enhance production efficiency, reduce costs, and enable higher-volume production, making composites more competitive against conventional materials in a wider range of applications. Strategic partnerships and collaborations across the value chain, from raw material suppliers to end-use manufacturers, also offer significant growth avenues by pooling expertise and resources for product development and market penetration.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emerging Applications in Urban Air Mobility and Defense | +3.5% | North America, Europe, Asia Pacific | Mid to Long-term |

| Advancements in Thermoplastic Composites | +2.7% | Global | Mid-term |

| Development of Sustainable and Bio-based Composites | +2.2% | Europe, North America | Long-term |

| Increased Automation and Digitalization in Manufacturing | +1.9% | Developed Economies | Short to Mid-term |

| Expansion into New Regional Markets (e.g., Southeast Asia, Latin America) | +1.6% | Asia Pacific, Latin America, MEA | Mid to Long-term |

HSR Composite Market Challenges Impact Analysis

The HSR Composite market, while dynamic, encounters several challenges that can impede its optimal growth and widespread adoption. One significant challenge is the lack of standardized testing methods and regulatory frameworks across different regions and applications. This fragmented approach can lead to inconsistencies in material performance specifications, prolonged certification processes, and increased costs for manufacturers operating globally. Establishing universal standards is crucial for instilling greater confidence in composite materials and accelerating their integration into new designs and critical infrastructure projects.

Another substantial challenge relates to the shortage of skilled labor proficient in composite design, manufacturing, and repair. The specialized nature of composite production demands a workforce with expertise in material science, advanced engineering, and complex fabrication techniques. This skill gap can lead to production bottlenecks, quality control issues, and delays in project execution. Addressing this requires significant investment in education, training programs, and talent development initiatives. Furthermore, the high capital expenditure required for setting up advanced composite manufacturing facilities, coupled with the long return on investment cycles, presents a barrier for smaller enterprises and new entrants, limiting market competitiveness and innovation. Economic uncertainties and global supply chain disruptions also pose ongoing challenges, impacting raw material availability and pricing.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Lack of Standardization and Regulatory Harmonization | -2.5% | Global | Long-term |

| Shortage of Skilled Workforce | -1.8% | Global, particularly developed regions | Mid to Long-term |

| High Capital Investment for Manufacturing Facilities | -1.5% | Global | Short to Mid-term |

| Competition from Traditional Materials (Metals) | -1.2% | Global | Short to Mid-term |

| Disruptions in Global Supply Chains | -0.9% | Global | Short-term |

HSR Composite Market - Updated Report Scope

This comprehensive market report delves into the intricate dynamics of the HSR Composite market, providing an in-depth analysis of its current size, historical performance, and future growth projections from 2025 to 2033. The scope encompasses detailed segmentation by material type, manufacturing process, end-use application, and geographical regions, offering granular insights into the market's evolving landscape. It further explores critical market drivers, restraints, opportunities, and challenges, alongside an impact assessment of AI technologies on the industry. The report identifies key trends shaping the market and profiles leading companies, offering a holistic view for strategic decision-making and investment planning within the advanced composites sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 5.75 Billion |

| Market Forecast in 2033 | USD 13.50 Billion |

| Growth Rate | 10.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Hexcel Corporation, Toray Industries Inc., Solvay S.A., SGL Carbon SE, Mitsubishi Chemical Corporation, Teijin Limited, Owens Corning, SAERTEX GmbH & Co. KG, Gurit Holding AG, Cytec Solvay Group, TPI Composites Inc., 3M Company, BASF SE, Covestro AG, Sumitomo Bakelite Co., Ltd., Magna International Inc., DuPont de Nemours Inc., Victrex plc, RTP Company, SABIC |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The HSR Composite market is meticulously segmented to provide a granular understanding of its diverse components and dynamics. This segmentation facilitates a detailed analysis of market performance across different material types, manufacturing technologies, and end-use industries, enabling stakeholders to identify specific growth areas and tailor strategies effectively. The market's complexity necessitates a multi-faceted approach to categorization, reflecting the wide array of materials and processes involved in producing high-strength and high-stiffness composite structures.

Key segmentations by fiber type, such as carbon, glass, and aramid, highlight the varying performance characteristics and cost profiles influencing material selection for specific applications. Similarly, the distinction between thermoset and thermoplastic resins addresses differences in processability, repairability, and recyclability. Furthermore, the segmentation by manufacturing process, encompassing methods like lay-up, filament winding, and advanced additive manufacturing, reveals the technological sophistication and automation levels prevalent in the industry. Ultimately, the end-use application segmentation—ranging from aerospace and defense to automotive, wind energy, and construction—underscores the broad utility and critical importance of HSR Composites across modern industrial landscapes.

- By Fiber Type: Carbon Fiber, Glass Fiber, Aramid Fiber, Other Fibers

- By Resin Type: Thermoset (Epoxy, Polyester, Vinyl Ester, Phenolic, Other Thermosets), Thermoplastic (PEEK, PPS, PAEK, Polypropylene, Polyamide, Other Thermoplastics)

- By Manufacturing Process: Lay-up (Hand Lay-up, Spray Lay-up, Automated Fiber Placement/Tape Laying), Filament Winding, Pultrusion, Resin Transfer Molding (RTM)/Vacuum Assisted RTM (VaRTM), Compression Molding, Additive Manufacturing, Other Processes

- By Application: Aerospace & Defense (Commercial Aviation, Military Aviation, Space), Automotive (Passenger Vehicles, Commercial Vehicles, Electric Vehicles), Wind Energy (Blades, Nacelles), Construction (Infrastructure, Architectural), Marine (Leisure Boats, Commercial Vessels), Sporting Goods, Electrical & Electronics, Others

Regional Highlights

- North America: This region is a leading market for HSR Composites, primarily driven by the robust aerospace and defense sector, which demands high-performance, lightweight materials for aircraft and military equipment. The automotive industry, especially with the growing emphasis on electric vehicles and fuel efficiency, also contributes significantly. Strong R&D investments and the presence of major composite manufacturers and research institutions further solidify its position.

- Europe: Europe represents a mature and highly innovative market, characterized by stringent environmental regulations and a strong focus on renewable energy, particularly wind power. The region's advanced automotive manufacturing base and a thriving aerospace sector, along with a proactive approach to developing sustainable and recyclable composite solutions, drive consistent demand.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, fueled by rapid industrialization, increasing infrastructure development, and expanding manufacturing capabilities in countries like China, India, and Japan. The burgeoning automotive and wind energy sectors, coupled with growing investments in aerospace and defense, make it a pivotal market for HSR Composites. Localized production and a vast consumer base contribute to its accelerated growth.

- Latin America: This region shows promising growth potential, albeit from a smaller base, driven by increasing foreign investment in manufacturing and infrastructure projects. The expansion of automotive production and the nascent development of renewable energy projects present significant opportunities for HSR Composites.

- Middle East and Africa (MEA): The MEA region is emerging as a market for HSR Composites, mainly due to diversification efforts away from oil economies, leading to investments in infrastructure, aerospace, and renewable energy. Government initiatives to develop local manufacturing capabilities are also creating new avenues for composite adoption.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the HSR Composite Market.- Hexcel Corporation

- Toray Industries Inc.

- Solvay S.A.

- SGL Carbon SE

- Mitsubishi Chemical Corporation

- Teijin Limited

- Owens Corning

- SAERTEX GmbH & Co. KG

- Gurit Holding AG

- TPI Composites Inc.

- 3M Company

- BASF SE

- Covestro AG

- Sumitomo Bakelite Co., Ltd.

- Magna International Inc.

- DuPont de Nemours Inc.

- Victrex plc

- RTP Company

- SABIC

Frequently Asked Questions

What is the projected growth rate for the HSR Composite Market?

The HSR Composite Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.8% between 2025 and 2033, reaching USD 13.50 Billion by 2033.

Which applications primarily drive the demand for HSR Composites?

Demand for HSR Composites is primarily driven by applications in Aerospace & Defense, Automotive (especially electric vehicles), and the Wind Energy sectors due to their superior strength-to-weight ratio and durability requirements.

What are the key challenges facing the HSR Composite Market?

Key challenges include high manufacturing costs, complexities in recycling and disposal, a shortage of skilled labor, and the lack of comprehensive standardization across the industry.

How is AI impacting the HSR Composite industry?

AI is significantly impacting the HSR Composite industry through generative design for optimization, predictive maintenance for extended asset life, enhanced quality control, and supply chain optimization.

Which region is expected to lead market growth for HSR Composites?

The Asia Pacific (APAC) region is expected to exhibit the fastest growth, driven by rapid industrialization, expanding manufacturing, and increasing investments in key end-use industries like automotive and wind energy.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted