AD ECU Market

AD ECU Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701024 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

AD ECU Market Size

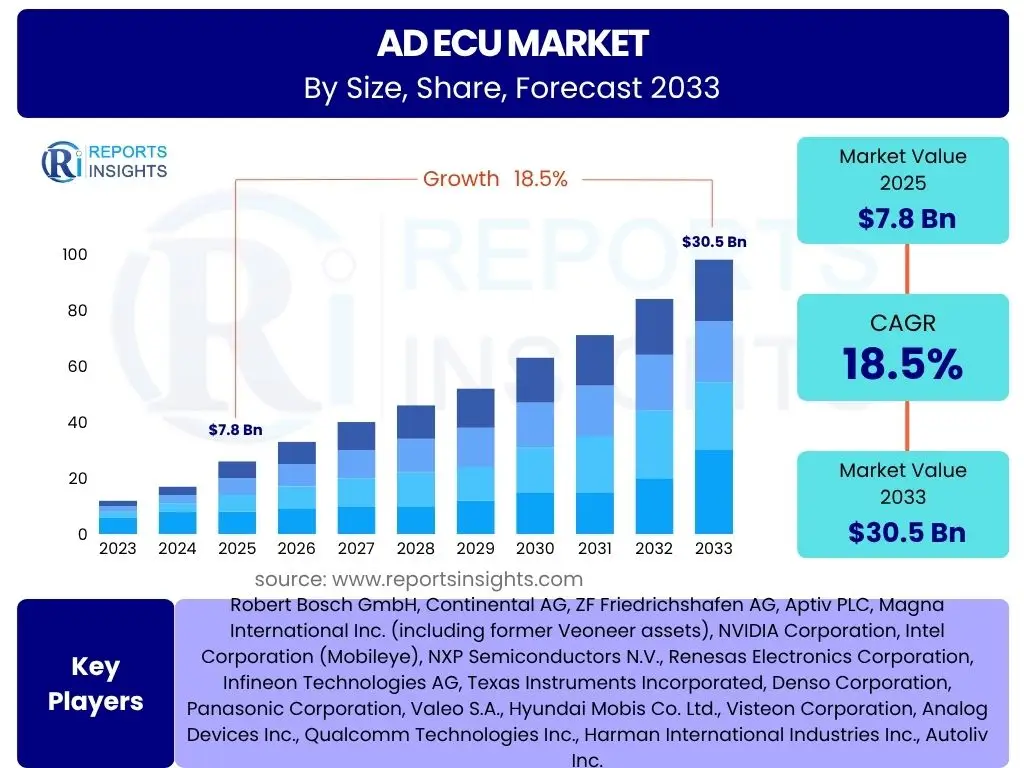

According to Reports Insights Consulting Pvt Ltd, The AD ECU Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 7.8 billion in 2025 and is projected to reach USD 30.5 billion by the end of the forecast period in 2033.

Key AD ECU Market Trends & Insights

The AD ECU market is undergoing a transformative period, driven by the accelerating development of autonomous vehicles and advanced driver-assistance systems. Common user inquiries often revolve around the technological shifts and their implications. Key trends highlight a move towards higher computational power, enhanced sensor fusion capabilities, and the integration of artificial intelligence for more sophisticated decision-making processes. There is a strong emphasis on functional safety and cybersecurity, as these systems become increasingly critical for vehicle operation and passenger protection. Furthermore, the evolving vehicle architecture, from distributed ECUs to more centralized domain controllers and even zonal architectures, is a significant trend impacting design and integration strategies within the automotive industry.

Another prominent trend is the increasing demand for over-the-air (OTA) updates, enabling continuous improvement and feature deployment without physical vehicle intervention. This capability is crucial for software-defined vehicles and supports the iterative development cycles of autonomous driving features. The convergence of automotive and consumer electronics technologies is also fostering innovation, bringing advanced computing platforms and connectivity solutions into the vehicle. As regulatory frameworks evolve globally, the market is responding with AD ECU solutions that can adapt to varying safety standards and legal requirements, driving further investment in robust and flexible architectures.

- Shift towards centralized domain controllers and zonal architectures for simplified wiring and enhanced computational efficiency.

- Integration of advanced sensor fusion techniques, combining data from radar, lidar, cameras, and ultrasonic sensors for comprehensive environmental perception.

- Increased adoption of Artificial Intelligence and Machine Learning algorithms for improved object detection, prediction, and decision-making.

- Emphasis on functional safety (ISO 26262 compliance) and robust cybersecurity measures to protect critical vehicle systems from external threats.

- Development of high-performance computing (HPC) platforms capable of processing massive amounts of data in real-time.

- Growth in the implementation of over-the-air (OTA) update capabilities for software and firmware enhancements, enabling continuous vehicle improvement.

- Standardization efforts for communication protocols and software interfaces to promote interoperability and accelerate development.

- Focus on energy efficiency for AD ECUs, especially in electric and hybrid vehicles, to minimize power consumption.

AI Impact Analysis on AD ECU

Common user questions regarding AI's impact on AD ECUs frequently address its role in enabling autonomous functions, the complexity it introduces, and its implications for system safety and performance. Artificial intelligence is unequivocally the cornerstone of modern AD ECU functionality, transforming these units from mere control interfaces into intelligent decision-making hubs. AI algorithms, particularly deep learning and machine learning, empower AD ECUs to process vast amounts of sensor data, interpret complex driving scenarios, and execute precise control commands in real-time. This includes advanced perception capabilities like object recognition, classification, and tracking, as well as predictive analytics for anticipating the behavior of other road users and optimizing vehicle maneuvers.

The integration of AI necessitates significantly more powerful and specialized processing units within AD ECUs, often incorporating dedicated AI accelerators, GPUs, and high-performance CPUs. This also introduces challenges related to data management, model validation, and the explainability of AI decisions, which are critical for safety-critical applications. Users are concerned about the reliability and robustness of AI in unforeseen circumstances, leading to a strong focus on extensive testing, simulation, and real-world validation. Despite these complexities, AI's continuous evolution promises to unlock higher levels of automation, enabling vehicles to navigate increasingly intricate environments and handle dynamic situations with greater autonomy and safety, fundamentally redefining the capabilities of AD ECUs.

- Enables sophisticated perception through advanced object detection, classification, and tracking from multiple sensor inputs.

- Facilitates intelligent decision-making and path planning for autonomous driving, optimizing vehicle responses in dynamic environments.

- Requires high-performance computing architectures, including GPUs and dedicated AI accelerators, to manage complex computations in real-time.

- Drives the need for robust machine learning models that can handle diverse and unpredictable road conditions.

- Introduces challenges in data management, model training, validation, and ensuring the explainability and safety of AI-driven decisions.

- Supports predictive analytics for anticipating traffic flow, pedestrian movement, and potential hazards, enhancing proactive safety features.

- Enables continuous learning and adaptation capabilities, allowing AD ECUs to improve performance over time through software updates and collected data.

Key Takeaways AD ECU Market Size & Forecast

User inquiries about the AD ECU market size and forecast consistently seek clarity on growth drivers, future outlook, and sustainability. A primary takeaway is the market's robust growth trajectory, fueled by an escalating global demand for enhanced vehicle safety features and the rapid progression towards higher levels of autonomous driving. Regulatory mandates, particularly in developed economies, are significantly influencing this growth by requiring advanced driver-assistance systems in new vehicles. The forecast indicates sustained expansion, underpinned by continuous technological innovation in sensor technology, AI integration, and high-performance computing, which are critical for the functionality and reliability of AD ECUs.

Furthermore, the market's long-term sustainability is reinforced by increasing consumer willingness to pay for advanced safety and convenience features, coupled with the automotive industry's strategic shift towards software-defined vehicles. This transformation positions AD ECUs as central components in future mobility solutions, extending beyond traditional vehicle control to comprehensive environmental understanding and proactive decision-making. The substantial projected increase in market valuation underscores strong investor confidence and continued research and development investments aimed at overcoming existing technical and regulatory hurdles, ensuring the AD ECU market remains a pivotal segment within the broader automotive electronics landscape.

- The AD ECU market is projected for substantial growth, driven by increasing ADAS adoption and autonomous driving development.

- Significant investment in research and development is expected to continue, pushing technological boundaries and enhancing system capabilities.

- Regulatory bodies worldwide are playing a crucial role in accelerating market growth through stricter safety mandates.

- The evolution towards higher levels of vehicle autonomy will be a primary demand driver for more complex and powerful AD ECUs.

- Market expansion is supported by the automotive industry's shift towards software-defined vehicles and connected ecosystems.

AD ECU Market Drivers Analysis

The AD ECU market is experiencing significant momentum, propelled by a confluence of powerful drivers. One of the foremost catalysts is the increasing global emphasis on road safety and the subsequent implementation of stringent safety regulations by governments and automotive bodies. These regulations often mandate the inclusion of advanced driver-assistance systems (ADAS) such as Automatic Emergency Braking (AEB), Lane Keeping Assist (LKA), and Blind Spot Detection (BSD) as standard features in new vehicles. Such mandates directly stimulate the demand for sophisticated AD ECUs capable of processing data from various sensors and executing critical safety functions, thereby reducing accidents and fatalities.

Another pivotal driver is the accelerating consumer demand for advanced convenience and safety features in vehicles. As awareness of ADAS benefits grows, consumers are increasingly prioritizing vehicles equipped with features that enhance driving comfort and provide an added layer of protection. This shift in consumer preference, combined with the competitive landscape among automotive manufacturers to differentiate their offerings, is prompting widespread integration of ADAS technologies across various vehicle segments, from economy cars to luxury models. This pervasive adoption naturally translates into higher demand for the underlying AD ECU hardware and software.

Furthermore, the rapid advancements in autonomous driving technology, from Level 2+ partial automation to future Level 4 and Level 5 fully autonomous vehicles, are fundamentally transforming the AD ECU landscape. Higher levels of autonomy necessitate more powerful, complex, and redundant AD ECUs capable of real-time sensor fusion, complex decision-making, and fail-operational capabilities. The ongoing development and eventual commercialization of self-driving cars, robotaxis, and autonomous logistics solutions are creating entirely new application areas and pushing the boundaries of AD ECU capabilities, driving innovation and market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stricter Global Safety Regulations and Mandates (e.g., Euro NCAP, NHTSA) | +6.0% | Global, particularly Europe, North America, China | Short to Mid-term (2025-2029) |

| Increasing Consumer Demand for ADAS Features and Vehicle Safety | +5.5% | North America, Europe, Asia Pacific (APAC) | Long-term (2025-2033) |

| Accelerated Development and Adoption of Autonomous Driving Technologies (L2+ to L5) | +4.5% | Global, led by North America, China, Germany | Mid to Long-term (2027-2033) |

| Technological Advancements in AI, Sensors (Lidar, Radar, Camera), and High-Performance Computing | +3.0% | Global | Continuous |

| Growth in Electric Vehicle (EV) Production and Integration of Advanced Electronics | +2.5% | Global, especially China, Europe, USA | Long-term (2025-2033) |

AD ECU Market Restraints Analysis

Despite its robust growth potential, the AD ECU market faces several significant restraints that could temper its expansion. One primary challenge is the inherently high cost associated with the research, development, and integration of sophisticated AD ECU systems. These units require advanced processors, intricate software algorithms, and rigorous testing for functional safety and reliability, all of which contribute to substantial upfront investments. The complexity further increases with the adoption of higher autonomy levels, where redundant systems and fail-operational capabilities are crucial, making the technology expensive to implement across all vehicle segments, particularly in cost-sensitive emerging markets.

Another major restraint is the intricate complexity involved in integrating various hardware and software components within the AD ECU ecosystem. Ensuring seamless interoperability between diverse sensors (cameras, radar, lidar), processing units, communication modules, and control algorithms from multiple suppliers poses significant technical hurdles. This integration challenge extends to the need for robust software validation and verification processes, which are time-consuming and resource-intensive, often leading to prolonged development cycles. Furthermore, the rapid pace of technological innovation in this domain means that hardware and software can become obsolete quickly, necessitating continuous updates and re-engineering, which adds to the overall cost and complexity for manufacturers.

Finally, cybersecurity vulnerabilities represent a growing concern and a significant restraint for the AD ECU market. As vehicles become increasingly connected and reliant on external data sources and software updates, they become potential targets for cyberattacks. A compromised AD ECU could lead to severe consequences, including vehicle hijacking, data breaches, or critical system failures, posing immense safety risks. Developing and implementing robust cybersecurity measures, including encryption, secure boot processes, and intrusion detection systems, requires substantial investment and ongoing vigilance. The potential for such threats can erode consumer trust and slow down the adoption of advanced autonomous features, thereby impacting market growth if not adequately addressed.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Development, Manufacturing, and Integration Costs of AD ECU Systems | -4.0% | Global, particularly affecting mass-market adoption | Long-term |

| Complexity of Software and Hardware Integration, Validation, and Verification | -3.5% | Global | Mid to Long-term |

| Cybersecurity Vulnerabilities and the Need for Robust Protection Measures | -2.5% | Global | Continuous |

| Limited Availability of Highly Skilled Workforce in AI, Software, and Automotive Electronics | -2.0% | Global | Mid-term |

| Public Acceptance and Trust Issues Regarding Autonomous Driving Technologies | -1.5% | Global, varying by region | Long-term |

AD ECU Market Opportunities Analysis

The AD ECU market is replete with significant opportunities, driven by ongoing technological advancements and evolving automotive architectures. A prime opportunity lies in the continued advancement towards higher levels of autonomous driving, specifically Level 3 (conditional automation) and beyond. As vehicles move towards more self-sufficient operation, the demand for highly sophisticated, redundant, and fail-operational AD ECUs will surge. This shift requires not only increased processing power but also novel architectures, such as domain and zonal controllers, which consolidate processing and simplify wiring harnesses, presenting a substantial market for advanced, integrated solutions.

Another compelling opportunity stems from the increasing integration of Vehicle-to-Everything (V2X) communication technologies. V2X enables vehicles to communicate with other vehicles (V2V), infrastructure (V2I), pedestrians (V2P), and the network (V2N), providing an unprecedented level of contextual awareness for AD ECUs. This external data vastly enhances the AD ECU's perception capabilities, allowing for more informed decision-making, improved safety features like accident prevention, and optimized traffic flow. The rollout of 5G networks further amplifies this opportunity by providing the necessary low-latency, high-bandwidth communication infrastructure to support real-time V2X interactions, thereby expanding the functional scope and value proposition of AD ECUs.

Furthermore, the rapid growth of the electric vehicle (EV) market presents a unique opportunity for AD ECU manufacturers. EVs, by their very nature, are designed with advanced electronic architectures, making them ideal platforms for integrating sophisticated ADAS and autonomous driving systems. The shift away from traditional internal combustion engine vehicles reduces complexity in certain areas, allowing for greater focus on and investment in advanced electronics like AD ECUs. This transition creates a symbiotic relationship where EVs demand advanced ECUs for energy management and ADAS features, while AD ECU advancements make EVs safer and more appealing, thereby accelerating the adoption of both technologies globally.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advancement towards Higher Levels of Autonomous Driving (Level 3, 4, and 5) | +5.0% | Global, particularly developed automotive markets | Long-term |

| Integration with Vehicle-to-Everything (V2X) Communication and 5G Networks | +4.0% | North America, Europe, China | Mid to Long-term |

| Emergence of Domain Centralized and Zonal Architectures in Vehicle E/E Systems | +3.5% | Global | Mid-term |

| Expansion into Commercial Vehicles (Trucks, Buses) and Logistics Automation | +3.0% | Global | Long-term |

| Development of Software-Defined Vehicles and Over-the-Air (OTA) Updates Capabilities | +2.5% | Global | Continuous |

AD ECU Market Challenges Impact Analysis

The AD ECU market, while promising, grapples with several formidable challenges that require innovative solutions and strategic partnerships. A significant challenge lies in managing the immense volume and velocity of data generated by multiple high-resolution sensors in real-time. AD ECUs must process gigabytes of data per second from cameras, lidar, radar, and ultrasonic sensors, requiring highly optimized data pipelines and powerful processing capabilities to ensure real-time performance and low latency for critical safety functions. Any delay in processing can lead to unsafe conditions, making efficient data handling a paramount concern that stresses current hardware and software architectures.

Another critical challenge is ensuring the functional safety and reliability of AD ECUs, especially as systems move towards higher autonomy levels where human intervention is minimal or absent. This necessitates adherence to rigorous functional safety standards like ISO 26262, which demand extensive validation, fault tolerance, and redundancy in both hardware and software. Developing and certifying such systems is immensely complex and time-consuming, requiring robust testing methodologies, including hardware-in-the-loop (HIL) and software-in-the-loop (SIL) simulations, as well as vast amounts of real-world testing. The potential for systematic or random failures in safety-critical components poses a constant challenge for manufacturers.

Furthermore, the AD ECU market faces the challenge of a fragmented and evolving regulatory landscape globally. Different countries and regions are developing their own specific regulations and legal frameworks for autonomous driving, leading to a lack of harmonization. This divergence can complicate product development, as AD ECUs must be designed to meet various regional requirements, increasing complexity and cost. Achieving standardized testing protocols and certification processes across borders is crucial but remains an ongoing challenge. Lastly, public perception and trust in autonomous systems pose a considerable hurdle; high-profile accidents involving autonomous vehicles can severely impact consumer confidence and slow down widespread adoption, underscoring the need for unwavering safety and transparency in development and deployment.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Managing Large Volumes of Sensor Data and Ensuring Real-time Performance | -3.0% | Global | Continuous |

| Ensuring Functional Safety, Reliability, and Redundancy for Safety-Critical Applications | -2.5% | Global | Continuous |

| Lack of Standardized Global Regulatory Frameworks and Legal Liability Issues | -2.0% | Global | Long-term |

| High Power Consumption and Thermal Management Requirements for High-Performance AD ECUs | -1.5% | Global | Mid-term |

| Interoperability and Compatibility Issues Among Different OEM and Supplier Systems | -1.0% | Global | Mid-term |

AD ECU Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the AD ECU market, covering its historical performance, current dynamics, and future projections. The scope includes a detailed examination of market size, growth drivers, restraints, opportunities, and challenges, offering a holistic view for stakeholders. Key market trends, including technological advancements and evolving regulatory landscapes, are thoroughly analyzed to provide actionable insights. The report further segments the market by various criteria such as type, autonomy level, application, vehicle type, and component, providing granular understanding of the market structure and potential growth areas. Regional analysis offers specific insights into market dynamics across major geographic segments, highlighting key country-level developments and competitive landscapes.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 7.8 billion |

| Market Forecast in 2033 | USD 30.5 billion |

| Growth Rate | 18.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG, Aptiv PLC, Magna International Inc. (including former Veoneer assets), NVIDIA Corporation, Intel Corporation (Mobileye), NXP Semiconductors N.V., Renesas Electronics Corporation, Infineon Technologies AG, Texas Instruments Incorporated, Denso Corporation, Panasonic Corporation, Valeo S.A., Hyundai Mobis Co. Ltd., Visteon Corporation, Analog Devices Inc., Qualcomm Technologies Inc., Harman International Industries Inc., Autoliv Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The AD ECU market is intricately segmented to provide a granular understanding of its diverse components and evolving applications. This segmentation is crucial for stakeholders to identify specific growth areas, understand competitive dynamics within niches, and tailor strategies effectively. The market can be dissected based on several key criteria, reflecting the technological complexity and varied requirements across the automotive industry. Analyzing these segments helps in comprehending how different aspects of AD ECU technology contribute to the overall market growth, from fundamental components to advanced autonomous functions, and their adoption across different vehicle types and geographical regions.

The segmentation by type illustrates the architectural shift in vehicle electronics, moving from numerous distributed ECUs to integrated domain controllers and eventually towards centralized computing platforms, each demanding different AD ECU capabilities. Autonomy level segmentation highlights the progressive sophistication of ADAS and autonomous driving features, directly correlating with the computational power and functional safety requirements of AD ECUs. Furthermore, segmenting by application clarifies the specific ADAS features that are driving demand, while vehicle type segmentation differentiates between the needs of passenger cars versus commercial vehicles. Component-level analysis provides insights into the underlying hardware and software technologies that form the core of every AD ECU, crucial for suppliers and technology developers.

- By Type: This segment includes Centralized ECU, representing the consolidation of multiple functions into a single powerful unit; Domain Controller ECU, which manages a specific domain like ADAS/AD functions; and Distributed ECU, the traditional architecture where each function has its own dedicated ECU.

- By Autonomy Level: Categorizes AD ECUs based on the level of autonomous driving they enable, from Level 1 (ADAS features like adaptive cruise control) through Level 2 (partial automation), Level 3 (conditional automation), Level 4 (high automation), to Level 5 (full automation).

- By Application: Focuses on the specific ADAS and AD features that AD ECUs power, such as Adaptive Cruise Control (ACC), Lane Keeping Assist (LKA), Automatic Emergency Braking (AEB), Parking Assist, Traffic Jam Assist (TJA), Blind Spot Detection (BSD), and Driver Monitoring System (DMS), among others.

- By Vehicle Type: Differentiates the market based on the type of vehicle integrating AD ECUs, primarily Passenger Vehicles and Commercial Vehicles, which are further sub-segmented into Light Commercial Vehicles and Heavy Commercial Vehicles, each with distinct requirements and adoption rates.

- By Component: Breaks down the AD ECU into its fundamental hardware and software constituents, including Microcontrollers (MCUs), Microprocessors (MPUs), Memory units, various Communication Modules (e.g., Ethernet, CAN, FlexRay), and the specific types of Sensors (Radar, Lidar, Camera, Ultrasonic) that feed data into the ECU.

Regional Highlights

- North America: This region stands as a significant market for AD ECUs, largely driven by strong innovation, a proactive approach to autonomous vehicle testing and deployment, and increasing consumer demand for advanced vehicle safety features. Countries like the United States and Canada are home to numerous technology companies and automotive OEMs investing heavily in AD/ADAS R&D, fostering a competitive ecosystem. Favorable regulatory environments in some states and provinces for autonomous vehicle testing further accelerate market growth and technological advancements.

- Europe: Characterized by stringent safety regulations from bodies like Euro NCAP, Europe is a leading market for the adoption of ADAS features, which directly translates to demand for AD ECUs. The region's focus on premium vehicle segments and luxury brands often means higher integration rates of sophisticated AD ECU-driven systems. Germany, with its strong automotive engineering heritage, along with France and the UK, are at the forefront of developing and deploying advanced AD ECU technologies.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing market, primarily fueled by rapid urbanization, increasing vehicle production (especially in China and India), and growing awareness about vehicle safety. China is a particularly dominant player, with significant government support for electric vehicles and autonomous driving initiatives, making it a hotbed for AD ECU innovation and adoption. Japan and South Korea also contribute significantly due to their advanced automotive manufacturing capabilities and technological leadership in electronics.

- Latin America: This region represents an emerging market for AD ECUs, with increasing penetration of ADAS features driven by rising disposable incomes and growing awareness of vehicle safety. While adoption rates may lag behind developed markets, the long-term potential is substantial as automotive manufacturers introduce more technologically advanced and safer vehicle models into the region. Brazil and Mexico are key countries, seeing increased local production and integration of ADAS technologies.

- Middle East and Africa (MEA): The AD ECU market in MEA is currently nascent but shows promising growth potential, particularly in the Gulf Cooperation Council (GCC) countries. Growth is primarily driven by the luxury and high-end vehicle segments, which are early adopters of advanced safety and autonomous features. Government initiatives aimed at modernizing infrastructure and promoting smart city concepts could further stimulate the demand for AD ECUs in the long term, though widespread adoption faces economic and infrastructural challenges.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the AD ECU Market.- Robert Bosch GmbH

- Continental AG

- ZF Friedrichshafen AG

- Aptiv PLC

- Magna International Inc.

- NVIDIA Corporation

- Intel Corporation (Mobileye)

- NXP Semiconductors N.V.

- Renesas Electronics Corporation

- Infineon Technologies AG

- Texas Instruments Incorporated

- Denso Corporation

- Panasonic Corporation

- Valeo S.A.

- Hyundai Mobis Co. Ltd.

- Visteon Corporation

- Analog Devices Inc.

- Qualcomm Technologies Inc.

- Harman International Industries Inc.

- Autoliv Inc.

Frequently Asked Questions

Analyze common user questions about the AD ECU market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is an AD ECU?

An AD ECU, or Advanced Driver-Assistance Systems Electronic Control Unit, is a dedicated computer within a vehicle responsible for processing sensor data and executing commands related to ADAS and autonomous driving functionalities. It acts as the brain for features like automatic emergency braking, lane keeping assist, and adaptive cruise control, enabling the vehicle to perceive its environment, make decisions, and control various actuators for safer and more automated driving.

Why is the AD ECU market growing?

The AD ECU market is experiencing robust growth primarily due to increasing global emphasis on road safety, leading to stricter regulatory mandates for ADAS features in new vehicles. Additionally, growing consumer demand for advanced safety and convenience features, coupled with the rapid progression towards higher levels of autonomous driving, are significant drivers. Continuous technological advancements in AI, sensors, and high-performance computing also fuel this expansion.

How does AI impact AD ECUs?

AI significantly impacts AD ECUs by enabling enhanced perception (object detection, classification), intelligent decision-making, and predictive capabilities crucial for autonomous driving. It allows AD ECUs to process complex sensor data in real-time, anticipate scenarios, and optimize vehicle responses. While demanding powerful processors and robust validation, AI integration is key to unlocking higher levels of automation and improving overall system performance and safety.

What are the main challenges for the AD ECU market?

Key challenges for the AD ECU market include managing vast volumes of real-time sensor data, ensuring the functional safety and reliability of complex systems (adhering to standards like ISO 26262), and navigating a fragmented global regulatory landscape. Additionally, high development and integration costs, cybersecurity vulnerabilities, and the need for a highly skilled workforce also pose significant hurdles for market players.

What are the future trends in AD ECU architecture?

Future trends in AD ECU architecture point towards a significant shift from distributed ECUs to more centralized domain controllers and ultimately, zonal architectures. This evolution aims to consolidate processing power, simplify wiring harnesses, and enable more efficient data management and software updates. The integration of high-performance computing platforms and seamless V2X communication capabilities will also be crucial for supporting higher levels of autonomous driving.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted