Battery Electric Truck Market

Battery Electric Truck Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702244 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

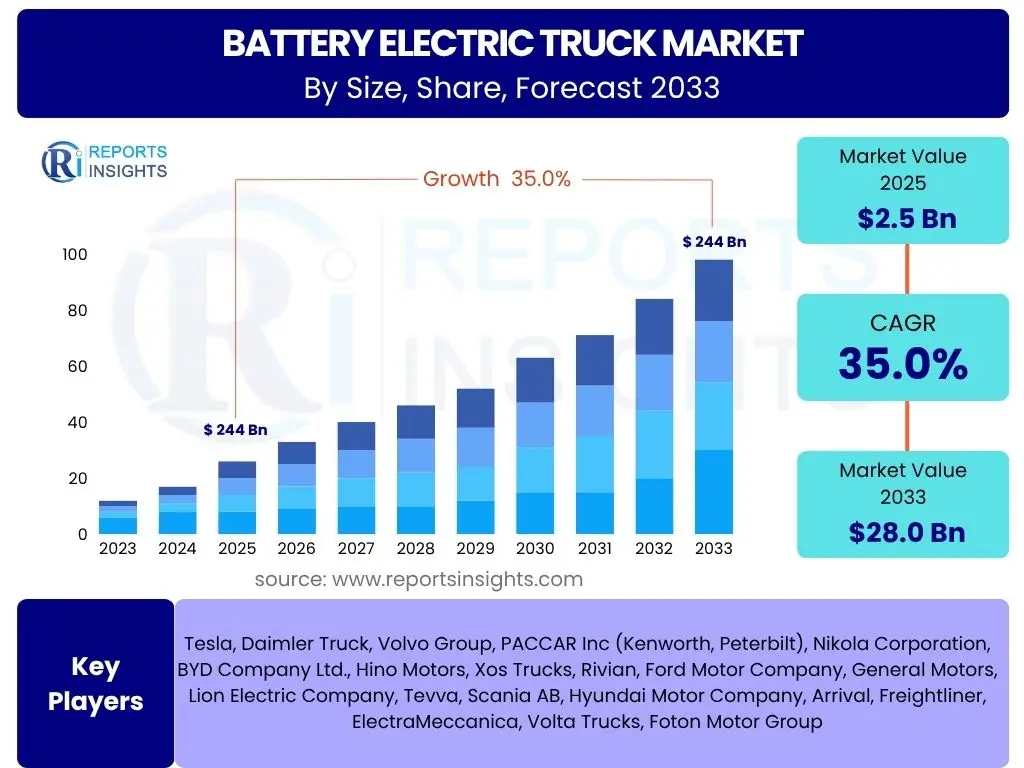

Battery Electric Truck Market Size

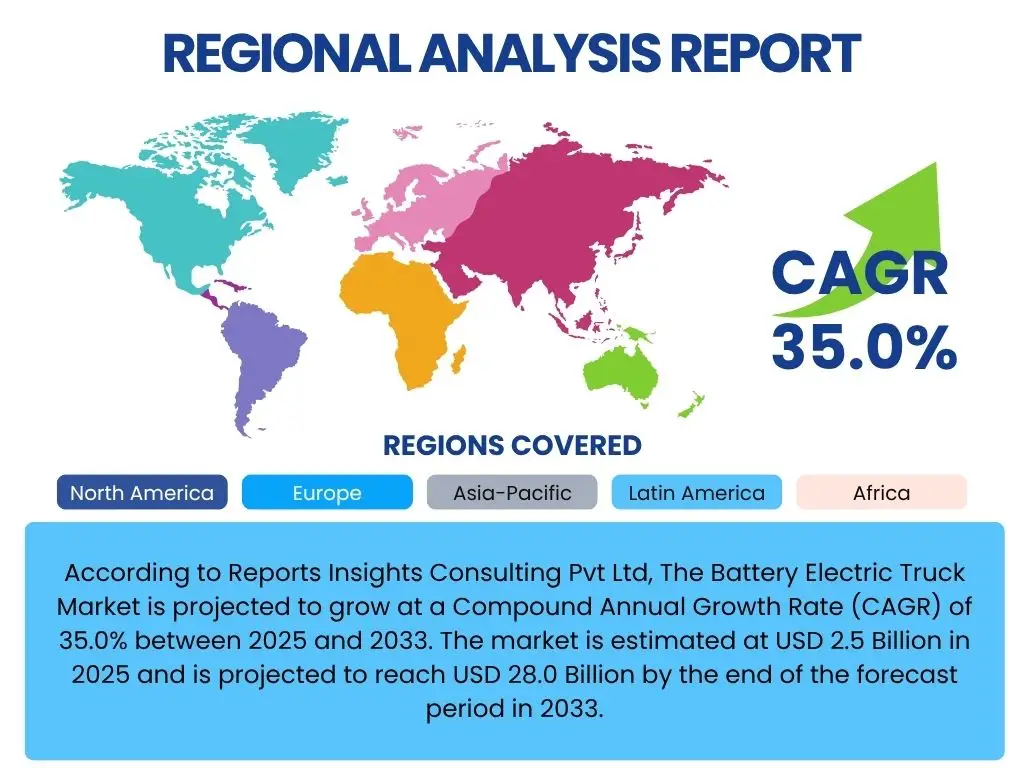

According to Reports Insights Consulting Pvt Ltd, The Battery Electric Truck Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 35.0% between 2025 and 2033. The market is estimated at USD 2.5 Billion in 2025 and is projected to reach USD 28.0 Billion by the end of the forecast period in 2033.

Key Battery Electric Truck Market Trends & Insights

The Battery Electric Truck market is currently experiencing a rapid transformation driven by a convergence of technological advancements, stringent environmental regulations, and evolving corporate sustainability goals. A significant trend involves the development of higher energy density battery packs, which are extending the range capabilities of these vehicles, addressing a critical concern for long-haul applications. This progress is complemented by innovations in charging infrastructure, including the deployment of megawatt charging systems (MCS) designed to significantly reduce charging times for heavy-duty electric trucks.

Furthermore, there is a growing emphasis on modular and scalable electric powertrain architectures, allowing manufacturers to optimize vehicle performance for various duty cycles, from urban delivery to regional haul. Fleet operators are increasingly adopting electric trucks not only for emissions reduction but also for lower operational costs, driven by reduced fuel and maintenance expenses. The integration of advanced telematics and predictive maintenance systems is also gaining traction, enhancing the efficiency and reliability of electric truck fleets.

- Advancements in battery technology extending range and reducing charging times.

- Development of high-power charging infrastructure, including Megawatt Charging Systems (MCS).

- Increasing corporate sustainability initiatives and environmental, social, and governance (ESG) mandates driving fleet electrification.

- Government incentives and favorable policies promoting electric vehicle adoption globally.

- Rising fuel costs and total cost of ownership (TCO) advantages favoring electric trucks.

- Integration of smart logistics and fleet management solutions enhancing operational efficiency.

AI Impact Analysis on Battery Electric Truck

Artificial intelligence is poised to profoundly transform the Battery Electric Truck market, addressing key operational challenges and enhancing vehicle performance, safety, and efficiency. AI-powered battery management systems (BMS) are becoming increasingly sophisticated, capable of predicting battery degradation, optimizing charging cycles to extend battery life, and dynamically managing power distribution to maximize range. This predictive capability significantly improves the reliability and longevity of the most critical and expensive component of an electric truck.

Beyond battery optimization, AI is central to the development of advanced driver-assistance systems (ADAS) and autonomous driving capabilities in electric trucks. These systems leverage AI for real-time traffic analysis, route optimization to minimize energy consumption, predictive cruise control, and enhanced safety features such as collision avoidance. AI also plays a crucial role in smart fleet management platforms, enabling predictive maintenance, optimizing delivery routes based on real-time data and energy consumption patterns, and facilitating efficient charge scheduling across large fleets, thereby reducing downtime and operational costs. The continuous data feedback loops enabled by AI will allow for ongoing improvements in vehicle design and operational strategies.

- Predictive Battery Management: AI optimizes battery health, extends lifespan, and maximizes range through intelligent charging and discharge patterns.

- Route Optimization: AI algorithms analyze traffic, topography, and charging infrastructure to recommend the most energy-efficient routes.

- Predictive Maintenance: AI monitors vehicle components in real-time to anticipate failures, reducing downtime and maintenance costs.

- Autonomous Driving Capabilities: AI is foundational for developing self-driving electric trucks, enhancing safety and operational efficiency, especially in logistics hubs and long-haul scenarios.

- Energy Management: AI dynamically adjusts power consumption across various vehicle systems to conserve energy and improve overall efficiency.

Key Takeaways Battery Electric Truck Market Size & Forecast

The Battery Electric Truck market is on the cusp of exponential growth, driven by a confluence of regulatory pressures, technological maturation, and economic imperatives. The significant projected Compound Annual Growth Rate (CAGR) underscores a fundamental shift in commercial transportation towards electrification. This growth is not uniform across all segments or regions, with specific vehicle types and geographical areas showing higher adoption rates initially, primarily influenced by policy support and the feasibility of charging infrastructure deployment.

A crucial insight is the accelerating pace of battery technology development, which is directly addressing previous limitations such as range anxiety and payload capacity, making electric trucks increasingly viable for a broader array of applications. Furthermore, the total cost of ownership (TCO) argument for electric trucks is strengthening, as battery costs decrease and the operational savings from lower fuel and maintenance expenses become more pronounced. This economic advantage, coupled with environmental benefits, positions electric trucks as a strategic investment for logistics companies and fleet operators aiming for long-term sustainability and profitability.

- The market is poised for significant expansion, with a projected tenfold increase in market value by 2033.

- Technological advancements in battery density and charging infrastructure are key enablers of this growth.

- Total Cost of Ownership (TCO) for electric trucks is becoming increasingly competitive, driving adoption over conventional diesel trucks.

- Policy support and regulatory mandates for emissions reduction are critical accelerators for market penetration across key regions.

- Urban and regional delivery segments are expected to lead initial adoption, followed by medium and heavy-duty long-haul applications as technology matures.

Battery Electric Truck Market Drivers Analysis

The global shift towards reducing carbon emissions and achieving sustainability targets is a primary driver for the Battery Electric Truck market. Governments worldwide are implementing stringent emission standards and offering substantial incentives, including tax credits, subsidies, and infrastructure development grants, to encourage the adoption of electric vehicles in commercial fleets. These policy frameworks create a favorable environment for manufacturers and fleet operators to invest in electric trucks, making them an economically viable and environmentally responsible choice. The increasing global focus on climate change mitigation has compelled industries to seek cleaner transportation alternatives, with electric trucks emerging as a leading solution for freight and logistics.

Beyond environmental mandates, the compelling economics of battery electric trucks are significantly influencing their market growth. While the initial purchase price of an electric truck may be higher than its diesel counterpart, the substantial savings in fuel and maintenance costs over the vehicle's lifespan offer a lower Total Cost of Ownership (TCO). Electricity prices are generally more stable and often lower than diesel, and electric powertrains have fewer moving parts, leading to reduced maintenance requirements and less downtime. This economic advantage, combined with corporate social responsibility initiatives and the public image benefits of operating a green fleet, is increasingly motivating companies to electrify their trucking operations.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Strict Emission Regulations & Government Incentives | +4.5% | Europe, North America, China | Short to Mid-Term (2025-2029) |

| Decreasing Battery Costs & Improving Energy Density | +3.8% | Global | Mid to Long-Term (2027-2033) |

| Growing Demand for Logistics & E-commerce Delivery | +3.0% | Global | Short to Mid-Term (2025-2030) |

| Corporate Sustainability Goals & ESG Mandates | +2.5% | North America, Europe, Developed Asia Pacific | Mid-Term (2026-2031) |

| Technological Advancements in Charging Infrastructure | +2.0% | Global, particularly urban centers | Mid to Long-Term (2027-2033) |

Battery Electric Truck Market Restraints Analysis

Despite the strong growth trajectory, the Battery Electric Truck market faces significant restraints that could impede its widespread adoption, primarily revolving around high upfront costs and the nascent charging infrastructure. The initial purchase price of a battery electric truck remains considerably higher than that of a comparable diesel truck, largely due to the high cost of battery packs. While battery costs are declining, this capital expenditure represents a substantial barrier for many fleet operators, especially small and medium-sized enterprises (SMEs) that may have limited access to financing or government incentives. This cost differential creates a significant hurdle for market penetration, requiring robust financial support mechanisms to bridge the gap.

Another major restraint is the lack of extensive and robust charging infrastructure, particularly for heavy-duty electric trucks requiring high-power charging. While urban areas might see more development, long-haul routes and remote logistics hubs often lack the necessary charging points with sufficient power output. The deployment of megawatt charging stations (MCS) is still in its early stages, and the grid capacity in many regions may not be adequate to support widespread high-power charging demands without significant upgrades. Furthermore, range anxiety remains a concern for operators, as the available range of electric trucks can be limited by battery capacity, payload, and environmental conditions, requiring careful route planning and access to reliable charging. The weight of heavy battery packs also impacts payload capacity, which can be a critical factor for certain freight operations, further restraining adoption in specific heavy-duty segments.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Upfront Purchase Cost | -3.5% | Global, particularly emerging economies | Short to Mid-Term (2025-2029) |

| Limited Charging Infrastructure & Range Anxiety | -3.0% | Global, especially long-haul routes | Short to Mid-Term (2025-2030) |

| Battery Weight & Payload Capacity Limitations | -2.2% | Global, specifically heavy-duty segments | Mid-Term (2026-2031) |

| Grid Infrastructure Readiness & Power Availability | -1.8% | North America, Europe (certain areas), Developing Asia | Mid to Long-Term (2027-2033) |

| Lack of Standardization in Charging Technology | -1.5% | Global | Short-Term (2025-2027) |

Battery Electric Truck Market Opportunities Analysis

The Battery Electric Truck market presents substantial opportunities for innovation and growth, particularly through the development of advanced battery technologies and the expansion of charging solutions. Breakthroughs in solid-state batteries, lithium-sulfur batteries, and other next-generation chemistries promise higher energy density, faster charging capabilities, and improved safety, which will directly address current limitations such as range anxiety and battery weight. These technological advancements will make electric trucks more competitive for long-haul applications and broader commercial use, opening up new market segments previously dominated by diesel vehicles. Furthermore, advancements in vehicle-to-grid (V2G) and vehicle-to-everything (V2X) technologies offer opportunities for electric trucks to serve as mobile energy storage units, providing grid stability services and generating additional revenue streams for fleet operators.

Another significant opportunity lies in the burgeoning market for specialized electric trucks tailored for specific applications, such as construction, refuse collection, and port operations. These niche markets often operate on fixed routes with predictable schedules, making them ideal candidates for electrification due to easier charging management and a strong emphasis on localized emissions reduction. The expansion of public and private charging networks, including fast-charging corridors along major freight routes and depot charging solutions, will further accelerate adoption. Moreover, the increasing integration of digital solutions like fleet management software, telematics, and predictive analytics offers opportunities to optimize electric truck operations, enhance efficiency, and provide value-added services, fostering a more connected and intelligent logistics ecosystem.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advancements in Battery Technology (e.g., Solid-State) | +4.0% | Global | Mid to Long-Term (2028-2033) |

| Expansion of Public & Private Charging Networks | +3.5% | North America, Europe, China | Mid-Term (2026-2031) |

| Development of Specialized Electric Trucks for Niche Applications | +3.0% | Global, particularly urban centers | Short to Mid-Term (2025-2029) |

| Fleet Electrification as a Service (EaaS) Models | +2.5% | Europe, North America | Mid-Term (2026-2030) |

| Integration with Smart Logistics & Autonomous Technologies | +2.0% | Global, developed markets | Mid to Long-Term (2027-2033) |

Battery Electric Truck Market Challenges Impact Analysis

The Battery Electric Truck market faces significant challenges, primarily related to the substantial investment required for developing and deploying robust charging infrastructure, particularly for heavy-duty vehicles. The current grid infrastructure in many regions is not adequately prepared to handle the large-scale, high-power demands of multiple electric trucks charging simultaneously, leading to potential issues with grid stability, power availability, and the need for expensive upgrades. This infrastructure gap can result in longer charging times or limited access to necessary charging capabilities, directly impacting fleet operational efficiency and feasibility, especially for long-haul routes where charging stops must be strategically planned and guaranteed.

Another critical challenge lies in managing battery degradation and ensuring long-term vehicle performance and residual value. Batteries are the most expensive component of an electric truck, and their performance degrades over time, affecting range and charging capabilities. Developing effective battery recycling programs and ensuring the responsible disposal of end-of-life batteries also present a significant environmental and logistical challenge. Furthermore, the specialized skills required for manufacturing, maintaining, and repairing complex electric powertrains pose a challenge for the workforce. There is a pressing need for upskilling and reskilling programs to ensure a sufficient pool of qualified technicians and engineers, as the talent gap can hinder both production scalability and service network expansion, ultimately impacting fleet readiness and uptime.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Infrastructure & Grid Readiness for High-Power Charging | -4.0% | Global, developing nations | Short to Mid-Term (2025-2030) |

| Battery Raw Material Supply Chain Volatility & Costs | -3.2% | Global | Short to Mid-Term (2025-2029) |

| Standardization of Charging Protocols & Connectors | -2.5% | Global | Short to Mid-Term (2025-2028) |

| Workforce Skill Gap for EV Manufacturing & Maintenance | -2.0% | Global | Mid-Term (2026-2031) |

| Residual Value & Battery Lifespan Concerns | -1.8% | Global | Mid to Long-Term (2027-2033) |

Battery Electric Truck Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Battery Electric Truck market, encompassing current trends, growth drivers, restraints, opportunities, and challenges influencing its trajectory from 2025 to 2033. The scope includes a detailed market size estimation, segmentation analysis by vehicle type, battery type, application, and range, as well as a thorough regional outlook. The report also highlights the competitive landscape, profiling key market players and their strategic initiatives, alongside an impact analysis of artificial intelligence on the industry. It aims to deliver actionable insights for stakeholders to navigate the evolving market dynamics effectively.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.5 Billion |

| Market Forecast in 2033 | USD 28.0 Billion |

| Growth Rate | 35.0% |

| Number of Pages | 250 |

| Key Trends | |

| Segments Covered | |

| Key Companies Covered | Tesla, Daimler Truck, Volvo Group, PACCAR Inc (Kenworth, Peterbilt), Nikola Corporation, BYD Company Ltd., Hino Motors, Xos Trucks, Rivian, Ford Motor Company, General Motors, Lion Electric Company, Tevva, Scania AB, Hyundai Motor Company, Arrival, Freightliner, ElectraMeccanica, Volta Trucks, Foton Motor Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Battery Electric Truck market is segmented to provide a granular understanding of its diverse applications and technological evolution. Key segmentation criteria include vehicle type, differentiating between light-duty, medium-duty, and heavy-duty trucks, each serving distinct logistical and operational needs. This categorization is crucial as the technological requirements and market readiness vary significantly across these segments, with light-duty trucks often leading in adoption due to their suitability for urban deliveries and simpler charging demands. The battery type segmentation explores the prevalence and advancements of various battery chemistries, such as lithium-ion, and emerging technologies like solid-state, which are pivotal for performance enhancements and cost reductions.

Further segmentation by application highlights the diverse end-use sectors leveraging electric trucks, ranging from traditional logistics and parcel delivery to more specialized fields like construction, mining, and waste management. Each application presents unique operational demands, influencing factors such as required range, payload capacity, and charging infrastructure needs. The range segmentation categorizes trucks based on their operational distance capabilities, crucial for understanding suitability for short-haul urban distribution versus long-haul freight transport. Understanding these segmentations allows for targeted market strategies, product development, and infrastructure planning, ensuring that solutions align with specific industry requirements and user expectations.

- Vehicle Type:

- Light-Duty Electric Trucks (LDET)

- Medium-Duty Electric Trucks (MDET)

- Heavy-Duty Electric Trucks (HDET)

- Battery Type:

- Lithium-ion

- Solid-State

- Others (e.g., LFP, NMC)

- Application:

- Logistics & Delivery

- Construction

- Mining

- Waste Management

- Agriculture

- Ports

- Others

- Range:

- Short Range (0-150 Miles)

- Medium Range (151-300 Miles)

- Long Range (300+ Miles)

- Propulsion:

- Battery Electric Vehicle (BEV)

- Plug-in Hybrid Electric Vehicle (PHEV)

- Fuel Cell Electric Vehicle (FCEV)

Regional Highlights

- North America: Strong policy support, increasing corporate fleet electrification goals, and significant investments in charging infrastructure are driving robust growth. Countries like the United States and Canada are seeing major commitments from large logistics companies and manufacturers, particularly for last-mile delivery and regional haul.

- Europe: Leading the global transition with stringent emission regulations, substantial government incentives, and a well-established commitment to decarbonization. Nations such as Germany, Norway, and the Netherlands are at the forefront of electric truck adoption, emphasizing urban logistics and heavy-duty regional transport.

- Asia Pacific (APAC): Emerges as a key growth region due to rapid urbanization, increasing e-commerce activities, and strong government backing for electric mobility, especially in China. China dominates the market with massive domestic production and favorable policies, while India and Japan are also making strides in electric commercial vehicle development.

- Latin America: Exhibits emerging potential with growing interest in sustainable logistics and urban delivery solutions. While infrastructure development is still in early stages, increasing environmental awareness and pilot projects in countries like Brazil and Mexico indicate future growth.

- Middle East and Africa (MEA): Represents nascent markets with opportunities driven by sustainability goals and diversification away from fossil fuels in certain regions. Limited but growing investments in smart city initiatives and logistics infrastructure are laying groundwork for future electric truck adoption.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Battery Electric Truck Market.- Tesla

- Daimler Truck

- Volvo Group

- PACCAR Inc (Kenworth, Peterbilt)

- Nikola Corporation

- BYD Company Ltd.

- Hino Motors

- Xos Trucks

- Rivian

- Ford Motor Company

- General Motors

- Lion Electric Company

- Tevva

- Scania AB

- Hyundai Motor Company

- Arrival

- Freightliner

- ElectraMeccanica

- Volta Trucks

- Foton Motor Group

Frequently Asked Questions

Analyze common user questions about the Battery Electric Truck market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate for the Battery Electric Truck Market?

The Battery Electric Truck Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 35.0% between 2025 and 2033, demonstrating a significant shift towards electrification in the commercial vehicle sector.

What are the primary drivers of the Battery Electric Truck Market?

Key drivers include stringent global emission regulations, substantial government incentives and subsidies, the decreasing cost of battery technology, and the compelling total cost of ownership (TCO) advantages for fleet operators.

What are the main challenges facing the Battery Electric Truck Market?

Major challenges include the high upfront purchase cost of electric trucks, the need for extensive and high-power charging infrastructure development, concerns regarding battery weight impacting payload, and the volatility in raw material supply chains for batteries.

How is AI impacting the Battery Electric Truck industry?

AI is transforming the industry through advanced battery management systems for optimized performance and longevity, AI-powered route optimization for energy efficiency, predictive maintenance, and the development of autonomous driving capabilities for enhanced safety and operational efficiency.

Which regions are leading the adoption of Battery Electric Trucks?

North America and Europe are leading due to strong policy support and environmental mandates, while Asia Pacific, particularly China, is a dominant market driven by rapid urbanization, significant domestic production, and government backing for electric mobility.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted