Floating Wind Turbine Market

Floating Wind Turbine Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700949 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

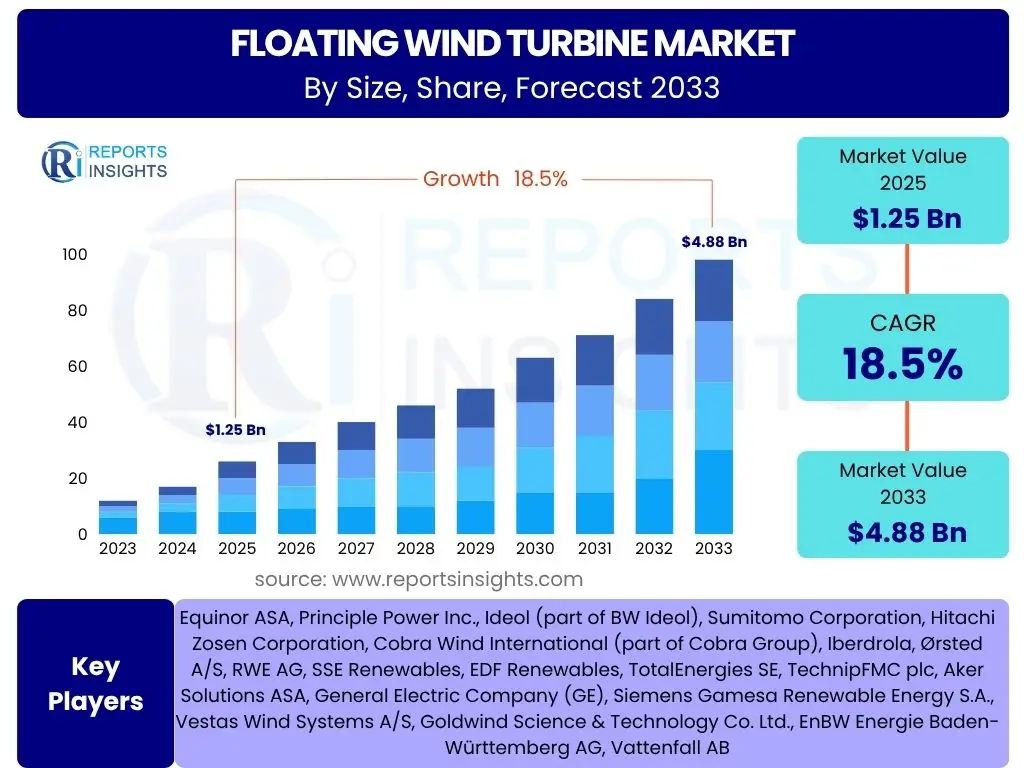

Floating Wind Turbine Market Size

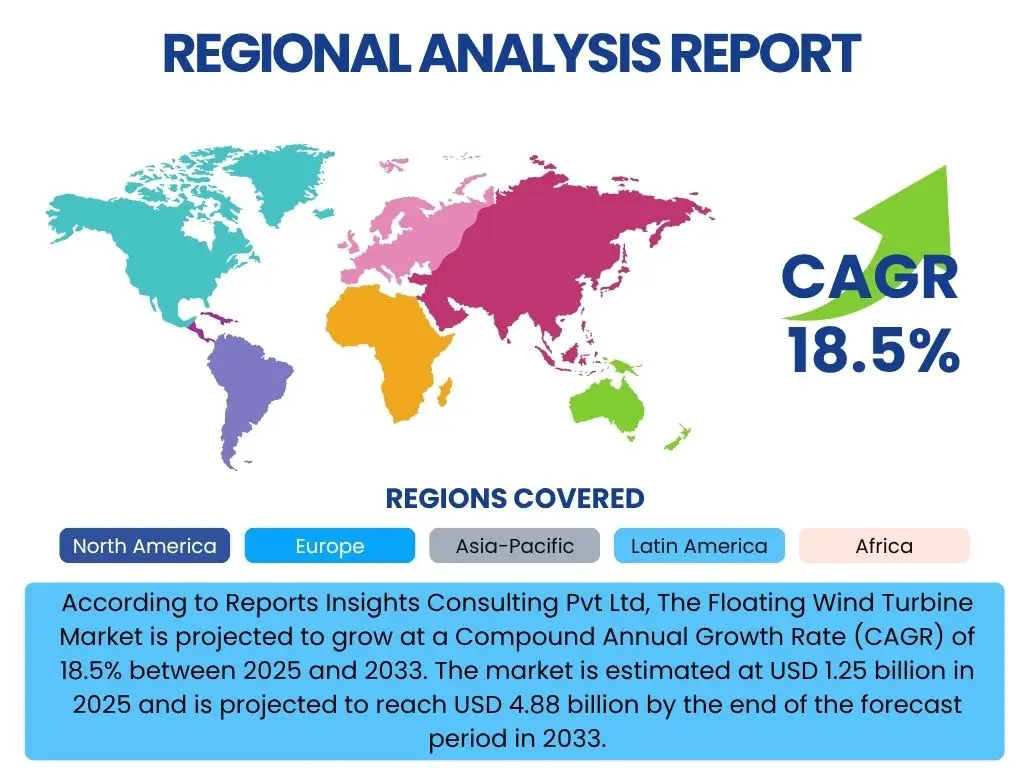

According to Reports Insights Consulting Pvt Ltd, The Floating Wind Turbine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 1.25 billion in 2025 and is projected to reach USD 4.88 billion by the end of the forecast period in 2033.

Key Floating Wind Turbine Market Trends & Insights

The floating wind turbine market is undergoing a rapid evolution, driven by advancements in technology, increasing global commitment to renewable energy, and the necessity to exploit deeper offshore wind resources. Common user inquiries often focus on the commercial viability of these projects, the specific technological breakthroughs enabling their deployment, and the evolving regulatory landscapes that support or hinder their growth. There is significant interest in understanding how cost reductions are being achieved and the role of international collaboration in accelerating market adoption. The emphasis is shifting from pilot projects to large-scale commercial deployments, highlighting a maturation in the industry's approach and capabilities.

Key trends indicate a strong move towards industrialization and standardization of floating substructure designs, aiming to lower manufacturing and installation costs. Furthermore, the integration of energy storage solutions and green hydrogen production with floating wind farms is emerging as a critical trend, enhancing grid stability and offering new revenue streams. The increasing focus on local supply chain development and port infrastructure upgrades also signifies a strategic move to optimize project logistics and reduce overall project timelines. These trends collectively underscore a market poised for exponential growth, driven by both technological readiness and supportive policy frameworks.

- Standardization of floating substructure designs for mass production.

- Integration of energy storage and green hydrogen production.

- Development of advanced mooring and anchoring systems.

- Expansion of dedicated port infrastructure for assembly and deployment.

- Increasing project scale and move towards commercial-scale arrays.

AI Impact Analysis on Floating Wind Turbine

User inquiries regarding the impact of Artificial Intelligence (AI) on the floating wind turbine sector frequently revolve around its potential to optimize operations, enhance predictive maintenance, and improve overall project economics. Stakeholders are particularly interested in how AI can address the unique challenges of deep-water installations, such as complex environmental monitoring, remote asset management, and the unpredictable nature of marine conditions. Expectations are high that AI will contribute significantly to reducing operational expenditures and increasing the efficiency and reliability of these nascent technologies. There is also curiosity about AI's role in the design phase, particularly for hydrodynamic modeling and structural integrity analysis, which are critical for innovative floating platforms.

AI's influence extends across the entire lifecycle of floating wind turbines, from initial site selection and design optimization to real-time operational management and post-deployment maintenance. By leveraging vast datasets on wind patterns, ocean currents, and structural performance, AI algorithms can predict potential failures, optimize turbine yaw and pitch for maximum energy capture, and manage grid integration more effectively. This intelligent automation not only enhances performance but also significantly improves safety protocols and extends the lifespan of critical components. The adoption of AI is therefore seen as a transformative force, enabling greater scalability and economic viability for floating offshore wind projects.

- Predictive maintenance and fault detection using AI algorithms.

- Optimization of turbine performance and energy yield through AI-driven controls.

- Enhanced site assessment and environmental impact modeling.

- Automated monitoring and remote diagnostics for operational efficiency.

- Improved structural health monitoring and integrity assessment.

Key Takeaways Floating Wind Turbine Market Size & Forecast

Common user questions regarding key takeaways from the Floating Wind Turbine market size and forecast data often focus on understanding the primary growth catalysts, the long-term investment potential, and the critical factors that will shape the market's trajectory. Users seek clear insights into which technological advancements are most impactful, what regional markets are poised for significant expansion, and the overarching implications for energy transition and decarbonization efforts. There is a strong desire to identify the tipping points that could accelerate or decelerate market adoption, particularly concerning cost reduction targets and policy stability.

The market is poised for substantial growth, driven by global net-zero targets and the increasing technical maturity of floating foundation technologies. The forecast indicates that while upfront capital costs remain a challenge, ongoing innovation and economies of scale will progressively lower the Levelized Cost of Energy (LCOE) for floating wind, making it competitive with other forms of renewable energy. Key takeaways emphasize the strategic importance of early mover advantage in technology development and deployment, the necessity of robust policy support, and the critical role of international collaboration in de-risking large-scale projects. The market's potential for unlocking vast deep-water resources worldwide underscores its pivotal role in the future global energy mix.

- Significant market growth anticipated, driven by global decarbonization goals.

- Continued reduction in Levelized Cost of Energy (LCOE) through technological advancements and economies of scale.

- Strong potential for deep-water resource exploitation, expanding addressable market.

- Policy support and regulatory frameworks are crucial for accelerated deployment.

- Increased investment and collaboration are essential for de-risking large-scale projects.

Floating Wind Turbine Market Drivers Analysis

The floating wind turbine market is propelled by a confluence of powerful drivers rooted in global energy transition imperatives and technological advancements. A primary driver is the urgent need to address climate change and reduce carbon emissions, which necessitates a rapid expansion of renewable energy sources. Conventional fixed-bottom offshore wind installations are limited by water depth, often capping out at around 60 meters. Floating technology removes this constraint, enabling access to vast deep-water areas with higher and more consistent wind speeds, thereby unlocking immense untapped energy potential globally.

Government policies and escalating renewable energy targets across major economies also serve as significant market drivers. Countries are increasingly setting ambitious offshore wind capacity goals, with specific allocations for floating wind given its strategic importance. Financial incentives, such as subsidies, tax credits, and feed-in tariffs, are designed to de-risk early projects and stimulate investment in this nascent but promising sector. Furthermore, the continuous decline in the Levelized Cost of Energy (LCOE) for offshore wind, including projections for floating wind, makes these projects increasingly competitive with traditional fossil fuel-based power generation, enhancing their attractiveness to investors and developers.

Technological maturation and innovation contribute substantially. Ongoing research and development are leading to more efficient, robust, and cost-effective floating platform designs, advanced mooring systems, and improved installation techniques. This technological evolution reduces technical risks and enhances project viability. Coupled with the growing global energy demand, especially in coastal and island nations with limited land for onshore renewables, floating wind offers a scalable and sustainable solution for future energy security.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Decarbonization & Energy Transition Targets | +5.5% | Global, particularly Europe, Asia Pacific, North America | Long-term (2025-2033) |

| Access to Deeper Waters & Higher Wind Speeds | +4.8% | Europe (Norway, UK, Scotland), Asia Pacific (Japan, Korea), North America (West Coast) | Mid-to-Long term (2027-2033) |

| Supportive Government Policies & Incentives | +4.2% | Europe, UK, France, Norway, Japan, South Korea, US, Scotland | Short-to-Mid term (2025-2030) |

| Falling Levelized Cost of Energy (LCOE) | +3.0% | Global | Mid-to-Long term (2028-2033) |

| Technological Advancements & Design Optimization | +1.0% | Global | Ongoing (2025-2033) |

Floating Wind Turbine Market Restraints Analysis

Despite its significant growth potential, the floating wind turbine market faces several considerable restraints that could impede its rapid expansion. A primary barrier is the exceptionally high upfront capital expenditure required for developing and deploying floating wind projects. These costs are significantly higher than those for fixed-bottom offshore wind, driven by the complexity of manufacturing specialized floating platforms, advanced mooring systems, and the need for sophisticated installation vessels capable of handling immense structures in challenging offshore environments. This elevated cost base makes projects less attractive to investors seeking quicker returns or lower financial risks, thereby slowing down the pace of commercialization and scale-up.

Another critical restraint is the immaturity of the supply chain and port infrastructure specifically tailored for floating wind projects. Unlike fixed-bottom offshore wind, which has benefited from decades of industrialization, the floating sector requires specialized fabrication facilities, heavy-lift capabilities, and deepwater port access for the assembly and deployment of large floating structures. The current lack of fully developed infrastructure and a mature supply chain leads to bottlenecks, increased logistics costs, and extended project timelines. This challenge is particularly acute in regions attempting to establish their floating wind industry from scratch, necessitating substantial upfront public and private investment in infrastructure development.

Furthermore, regulatory and permitting complexities pose significant hurdles. Floating wind projects often operate in deeper, more remote waters, impacting marine ecosystems and requiring extensive environmental impact assessments. Navigating diverse national and international maritime laws, obtaining multiple permits from various agencies, and addressing potential conflicts with other ocean users (e.g., fishing, shipping, defense) can result in prolonged approval processes and increased project risks. These complexities, combined with the technical challenges of operating and maintaining assets in harsh marine environments, contribute to the cautious approach of some developers and investors, acting as a brake on the market's otherwise promising growth trajectory.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Upfront Capital Costs | -4.0% | Global | Short-to-Mid term (2025-2030) |

| Immature Supply Chain & Port Infrastructure | -3.5% | Europe (developing ports), Asia Pacific (nascent infrastructure), North America (early stage) | Mid-term (2026-2031) |

| Grid Connection & Transmission Limitations | -2.8% | Global, particularly remote deep-water sites | Mid-to-Long term (2028-2033) |

| Environmental Concerns & Permitting Complexities | -2.0% | Global, especially sensitive marine areas | Ongoing (2025-2033) |

| Operation & Maintenance (O&M) Challenges in Deep Waters | -1.5% | Global | Long-term (2029-2033) |

Floating Wind Turbine Market Opportunities Analysis

The floating wind turbine market presents substantial opportunities driven by its capacity to unlock vast, previously inaccessible offshore wind resources. Unlike fixed-bottom foundations, floating platforms can be deployed in water depths exceeding 60 meters, which constitutes the majority of the world's best wind resources. This opens up entirely new geographies, including regions with narrow continental shelves or steep seabed gradients, such as Japan, South Korea, Portugal, the US West Coast, and parts of the Mediterranean. The ability to harness stronger and more consistent winds in deeper waters translates into higher capacity factors and greater electricity generation, making these projects highly attractive for future energy security and supply.

Another significant opportunity lies in the potential for innovation and industrialization, leading to substantial cost reductions. As the technology scales from demonstration projects to commercial arrays, economies of scale in manufacturing, standardized designs, and optimized installation procedures are expected to drive down the Levelized Cost of Energy (LCOE). This pathway to cost competitiveness will broaden the market appeal of floating wind, attracting larger investments and enabling more widespread adoption. Furthermore, the development of integrated energy solutions, such as co-locating floating wind farms with green hydrogen production facilities or advanced battery storage, presents an opportunity to enhance grid stability and create new value chains for renewable energy beyond direct power generation.

The global push for decarbonization and energy independence creates a strong policy-driven demand for floating wind. Many nations are setting ambitious targets for offshore wind deployment, with floating technology being critical to achieving these goals where shallow-water sites are limited. This policy support, combined with growing investor confidence in renewable infrastructure, attracts significant capital flows into the sector. Additionally, the development of a specialized floating wind supply chain, including advanced materials, fabrication techniques, and novel maritime logistics, represents an opportunity for job creation and economic growth in coastal regions, fostering local industrial development and creating a robust ecosystem for future expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Accessing Deep-Water, High-Resource Sites | +6.0% | Global (esp. Japan, South Korea, US West Coast, Portugal, UK, Norway) | Long-term (2026-2033) |

| Cost Reduction through Industrialization & Scale | +5.0% | Global | Mid-to-Long term (2028-2033) |

| Development of Green Hydrogen & Hybrid Projects | +4.5% | Europe, Asia Pacific | Mid-to-Long term (2027-2033) |

| Policy Support & Auction Mechanisms | +3.5% | Europe (UK, France), Asia Pacific (Japan, Korea), US | Short-to-Mid term (2025-2030) |

| Emergence of New Market Entrants & Investors | +2.0% | Global | Mid-term (2026-2031) |

Floating Wind Turbine Market Challenges Impact Analysis

The floating wind turbine market, while promising, faces significant challenges that necessitate innovative solutions and strategic planning. One major challenge is the inherent complexity of designing and manufacturing robust floating structures capable of withstanding extreme marine conditions, including high waves, strong currents, and corrosive saltwater environments. Ensuring the long-term structural integrity and stability of these platforms, along with their intricate mooring and anchoring systems, demands advanced engineering and materials science expertise. The sheer scale and weight of these components also pose considerable logistical challenges during fabrication, transport, and installation, often requiring specialized vessels and port facilities that are not yet widely available or standardized globally.

Another critical challenge lies in the operation and maintenance (O&M) of floating wind farms, particularly in remote, deep-water locations. Accessing these offshore assets for routine maintenance, repairs, or component replacements is significantly more complex and costly than for fixed-bottom turbines. The dynamic movement of the floating platforms adds another layer of complexity to maintenance procedures, requiring specialized tools and highly trained personnel. Furthermore, the subsea cable infrastructure needed to transmit power from distant floating wind farms to the grid presents its own set of challenges, including protection against damage, efficient power transfer over long distances, and reliable grid integration, all of which add to project complexity and cost.

Finally, securing adequate financing for large-scale floating wind projects remains a substantial hurdle. Given the novelty of the technology at a commercial scale, the higher capital costs, and perceived risks compared to mature renewable technologies, attracting sufficient investment can be difficult. Project developers often struggle to achieve financial close due to a lack of long-term revenue certainty, fluctuating policy landscapes, and limited availability of specialized insurance. Addressing these financing challenges will require innovative funding models, stronger government guarantees, and a clear demonstration of the technology's long-term reliability and economic viability to build investor confidence and accelerate market adoption.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technical Complexity & Design Optimization | -3.0% | Global | Short-to-Mid term (2025-2029) |

| Logistics & Installation of Large Structures | -2.5% | Global, particularly regions with limited heavy-lift infrastructure | Mid-term (2026-2030) |

| High O&M Costs & Remote Accessibility | -2.0% | Global | Long-term (2028-2033) |

| Grid Integration & Transmission Infrastructure | -1.8% | Global, especially for large-scale remote projects | Mid-to-Long term (2027-2032) |

| Securing Project Financing & Insurance | -1.5% | Global | Short-to-Mid term (2025-2029) |

Floating Wind Turbine Market - Updated Report Scope

This comprehensive report provides a detailed analysis of the Floating Wind Turbine Market, segmenting it by foundation type, location, and application, while offering in-depth regional insights. It covers historical data from 2019 to 2023 and provides forecasts from 2025 to 2033, including market size, growth rates, key trends, drivers, restraints, opportunities, and challenges. The report profiles leading market players and identifies strategic developments shaping the industry landscape, aiming to deliver actionable intelligence for stakeholders navigating this evolving sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.25 billion |

| Market Forecast in 2033 | USD 4.88 billion |

| Growth Rate | 18.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Equinor ASA, Principle Power Inc., Ideol (part of BW Ideol), Sumitomo Corporation, Hitachi Zosen Corporation, Cobra Wind International (part of Cobra Group), Iberdrola, Ørsted A/S, RWE AG, SSE Renewables, EDF Renewables, TotalEnergies SE, TechnipFMC plc, Aker Solutions ASA, General Electric Company (GE), Siemens Gamesa Renewable Energy S.A., Vestas Wind Systems A/S, Goldwind Science & Technology Co. Ltd., EnBW Energie Baden-Württemberg AG, Vattenfall AB |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The floating wind turbine market is analyzed across several critical segments to provide a granular understanding of its dynamics and growth trajectories. These segmentations allow for a detailed examination of technological preferences, deployment strategies, and end-user applications, highlighting the diverse facets of this rapidly evolving industry. Understanding these segments is crucial for stakeholders to identify niche opportunities, allocate resources effectively, and develop targeted market strategies that align with specific regional demands and technological advancements.

The segmentation by foundation type is particularly vital, as each design offers distinct advantages in terms of stability, cost, and suitability for varying water depths and seabed conditions. Location-based segmentation distinguishes between shallow and deep-water applications, reflecting the core value proposition of floating technology in accessing vast deep-water resources. Application-based segmentation categorizes the end-use of floating wind power, providing insights into its role in utility-scale power generation, industrial processes, and commercial energy supply, thus offering a holistic view of market demand and future potential.

- By Foundation Type:

- Semi-submersible: Known for stability and ease of assembly at port.

- Spar: Requires deep water for deployment due to its long, slender design.

- Tension Leg Platform (TLP): Offers excellent stability and requires minimal seabed footprint.

- Barge: Simple design, potentially lower cost for shallower floating applications.

- Others: Emerging and hybrid concepts.

- By Location:

- Shallow Water: Transition zones where fixed-bottom is becoming less feasible but floating offers advantages.

- Deep Water: Core application area, beyond 60-meter depth, for harnessing high-resource wind.

- By Application:

- Utility: Large-scale power generation for national grids.

- Industrial: Powering industrial facilities, potentially through direct supply or green hydrogen production.

- Commercial: Smaller scale applications for specific commercial needs.

Regional Highlights

- Europe: Leading the global market, particularly the UK, Norway, France, and Spain, driven by ambitious offshore wind targets, supportive policies, and extensive research and development in floating technology. Scotland is a prominent hub for floating wind deployment.

- Asia Pacific (APAC): Emerging as a critical growth region with significant potential, led by Japan, South Korea, Taiwan, and China, due to their limited shallow-water areas and strong renewable energy commitments. These nations are heavily investing in floating wind R&D and pilot projects.

- North America: The U.S. West Coast and East Coast (Maine, California, Oregon) are poised for substantial growth, given their deep-water resources and state-level renewable energy mandates. California has particularly aggressive targets for floating offshore wind.

- Latin America: Nascent but promising, with countries like Brazil showing interest in exploring their deep-water offshore wind potential, though market development is still in very early stages.

- Middle East and Africa (MEA): Limited current activity but holds long-term potential, especially in regions with suitable deep-water profiles and growing energy demands, contingent on strong policy support and foreign investment.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Floating Wind Turbine Market.- Equinor ASA

- Principle Power Inc.

- Ideol (part of BW Ideol)

- Sumitomo Corporation

- Hitachi Zosen Corporation

- Cobra Wind International (part of Cobra Group)

- Iberdrola

- Ørsted A/S

- RWE AG

- SSE Renewables

- EDF Renewables

- TotalEnergies SE

- TechnipFMC plc

- Aker Solutions ASA

- General Electric Company (GE)

- Siemens Gamesa Renewable Energy S.A.

- Vestas Wind Systems A/S

- Goldwind Science & Technology Co. Ltd.

- EnBW Energie Baden-Württemberg AG

- Vattenfall AB

Frequently Asked Questions

Analyze common user questions about the Floating Wind Turbine market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a floating wind turbine?

A floating wind turbine is an offshore wind turbine mounted on a floating platform that is anchored to the seabed, rather than being fixed directly to the ocean floor. This design allows for deployment in deeper waters where traditional fixed-bottom turbines are not feasible.

Why is floating wind energy important?

Floating wind energy is crucial because it unlocks access to vast deep-water areas with stronger and more consistent winds, significantly expanding the global potential for offshore wind power. This technology is vital for achieving ambitious renewable energy targets and decarbonization goals, especially for countries with limited shallow-water coastlines.

What are the main types of floating foundations?

The primary types of floating foundations for wind turbines include semi-submersible (most common), spar, tension leg platform (TLP), and barge. Each design offers different stability characteristics, fabrication methods, and suitability for varying water depths and environmental conditions.

What are the biggest challenges for floating wind turbines?

Key challenges for floating wind turbines include high upfront capital costs, the immaturity of the supply chain and port infrastructure, complexities in installation and maintenance in harsh marine environments, and securing long-term project financing and grid integration solutions.

What is the market outlook for floating wind turbines?

The market outlook for floating wind turbines is highly positive, projected to experience significant growth between 2025 and 2033. This growth is driven by increasing global demand for renewable energy, technological advancements leading to cost reductions, and supportive government policies aimed at deep-water offshore wind deployment.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted