Commercial Aircraft Turbine Blade and Vane Market

Commercial Aircraft Turbine Blade and Vane Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705174 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

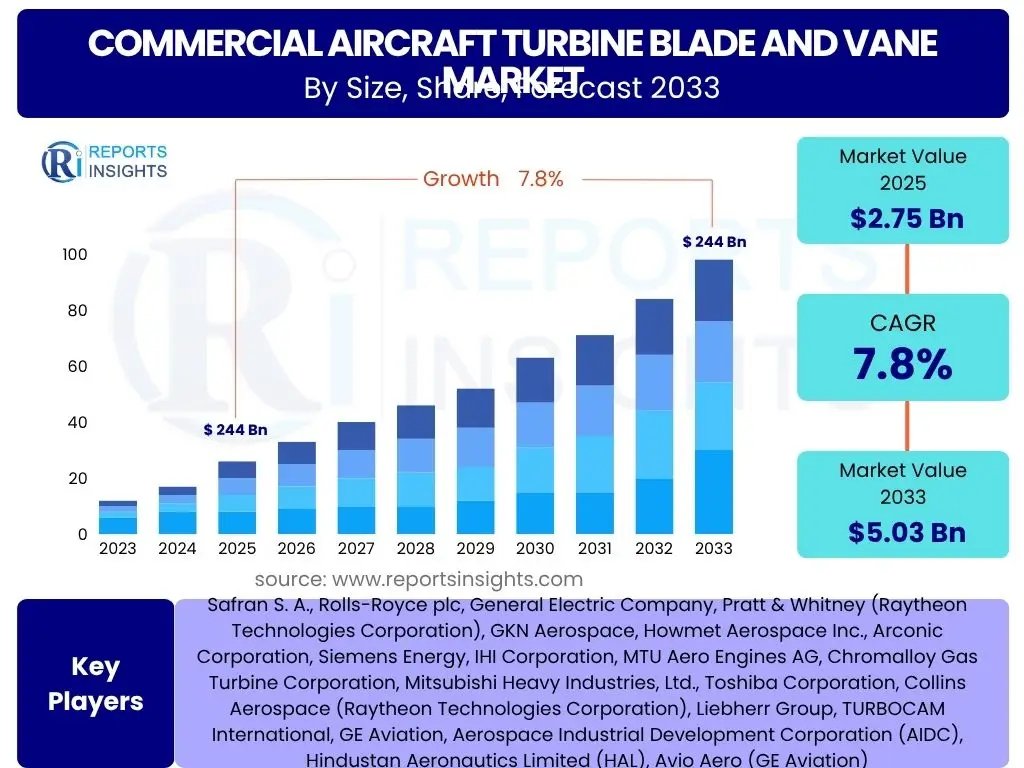

Commercial Aircraft Turbine Blade and Vane Market Size

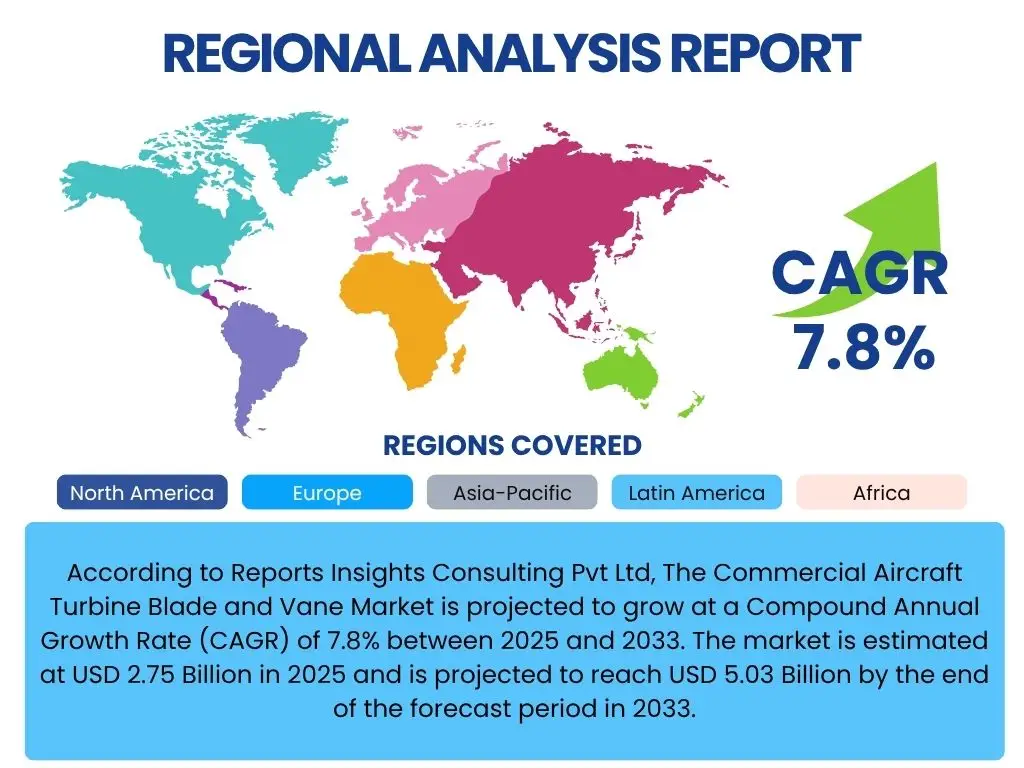

According to Reports Insights Consulting Pvt Ltd, The Commercial Aircraft Turbine Blade and Vane Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 2.75 Billion in 2025 and is projected to reach USD 5.03 Billion by the end of the forecast period in 2033.

Key Commercial Aircraft Turbine Blade and Vane Market Trends & Insights

The Commercial Aircraft Turbine Blade and Vane market is experiencing significant transformation driven by the aerospace industry's pursuit of enhanced engine efficiency, reduced operational costs, and environmental sustainability. A primary trend involves the increasing adoption of advanced materials such as Ceramic Matrix Composites (CMCs) and advanced nickel-based superalloys. These materials offer superior temperature resistance and lighter weight, directly contributing to improved fuel efficiency and extended component lifespan. The drive for lighter, stronger components capable of withstanding extreme conditions is paramount as engine designs push the boundaries of thermal efficiency.

Another prominent trend is the growing integration of advanced manufacturing techniques, most notably additive manufacturing (3D printing). This technology allows for the creation of complex geometries that are difficult or impossible to achieve with traditional methods, leading to optimized designs that improve airflow, reduce weight, and enhance overall engine performance. Additionally, the aftermarket segment, particularly Maintenance, Repair, and Overhaul (MRO) services, is witnessing steady growth as the global commercial aircraft fleet expands and ages. This creates a continuous demand for replacement blades and vanes, as well as repair and refurbishment services to extend the operational life of existing components.

- Increased adoption of Ceramic Matrix Composites (CMCs) and advanced superalloys for enhanced thermal performance and weight reduction.

- Growing integration of additive manufacturing (3D printing) for complex, optimized blade and vane geometries.

- Rising demand for Maintenance, Repair, and Overhaul (MRO) services driven by fleet expansion and aging aircraft.

- Focus on lightweighting technologies to improve fuel efficiency and reduce emissions.

- Development of advanced coating technologies for improved durability and erosion resistance.

AI Impact Analysis on Commercial Aircraft Turbine Blade and Vane

Artificial Intelligence (AI) is set to significantly impact the Commercial Aircraft Turbine Blade and Vane market by revolutionizing design, manufacturing, and maintenance processes. In the design phase, AI-driven generative design tools can rapidly explore thousands of design iterations, optimizing blade and vane geometries for maximum aerodynamic efficiency, structural integrity, and material usage. This capability drastically reduces design cycles and leads to innovative, high-performing components that were previously unattainable through traditional human-led design methods. Furthermore, AI algorithms can analyze vast datasets from simulations and real-world performance, identifying optimal material compositions and manufacturing parameters to enhance component durability and performance under extreme operational conditions.

In manufacturing, AI-powered systems are enhancing precision and efficiency, particularly in quality control and process optimization. Machine learning algorithms analyze sensor data from manufacturing equipment to detect anomalies, predict equipment failures, and ensure consistent product quality, minimizing defects and waste. This leads to higher yield rates and reduced production costs. For maintenance, AI is transforming predictive capabilities. By analyzing flight data, engine performance metrics, and historical maintenance records, AI models can accurately predict when turbine blades and vanes are likely to degrade or fail, enabling proactive maintenance schedules. This predictive approach minimizes unscheduled downtime, reduces maintenance costs, and significantly enhances aircraft safety and operational reliability.

- Generative design for optimized blade and vane geometries, accelerating design cycles.

- Predictive maintenance for turbine components, reducing unscheduled downtime and MRO costs.

- AI-driven quality control in manufacturing processes, minimizing defects and improving yield.

- Optimization of material selection and manufacturing parameters for enhanced durability.

- Supply chain optimization and demand forecasting for raw materials and finished components.

Key Takeaways Commercial Aircraft Turbine Blade and Vane Market Size & Forecast

The Commercial Aircraft Turbine Blade and Vane market is poised for robust growth through 2033, primarily fueled by the sustained expansion of global air travel and the continuous demand for new, more fuel-efficient aircraft. The aerospace industry's relentless pursuit of operational efficiency mandates engines that are lighter, more powerful, and consume less fuel, directly impacting the demand for advanced turbine components. This necessitates ongoing innovation in material science and manufacturing processes, with a particular emphasis on components that can withstand higher temperatures and pressures within the engine core, thereby improving overall engine performance and reducing emissions.

A significant driver of market expansion is the increasing investment in research and development for next-generation engine programs, which heavily rely on cutting-edge blade and vane technologies. Concurrently, the aftermarket segment for maintenance, repair, and overhaul (MRO) services will continue to be a substantial revenue generator, supporting the longevity and operational reliability of the existing global aircraft fleet. Manufacturers are increasingly focusing on strategic partnerships and technological advancements, including additive manufacturing and advanced coatings, to maintain competitiveness and meet the evolving demands of the aerospace sector, ensuring continuous market relevance and growth.

- Market growth is significantly driven by increasing global air travel and new aircraft deliveries.

- Strong emphasis on fuel efficiency and emission reduction is propelling demand for advanced turbine components.

- Innovations in material science, particularly CMCs and advanced superalloys, are critical for performance enhancement.

- Aftermarket MRO services represent a substantial and growing segment due to fleet aging.

- Technological advancements like additive manufacturing are key to future market development and component optimization.

Commercial Aircraft Turbine Blade and Vane Market Drivers Analysis

The growth of the Commercial Aircraft Turbine Blade and Vane Market is propelled by several fundamental drivers within the global aerospace sector. One primary driver is the significant increase in global air passenger traffic and freight volumes. As more people travel and goods are transported by air, the demand for new commercial aircraft rises, directly translating into a greater need for advanced, high-performance turbine blades and vanes in newly manufactured engines. This continuous expansion of the global commercial fleet forms a foundational demand for original equipment components.

Another crucial driver is the aerospace industry's relentless focus on fuel efficiency and emissions reduction. Regulatory pressures and airline operational cost concerns necessitate engines that consume less fuel and produce fewer harmful emissions. This drives engine manufacturers to develop next-generation designs featuring hotter, more efficient combustion processes, which, in turn, requires turbine blades and vanes made from advanced materials capable of withstanding extreme temperatures and pressures, such as Ceramic Matrix Composites (CMCs) and improved superalloys. Furthermore, the robust activity in the Maintenance, Repair, and Overhaul (MRO) sector, driven by an aging global aircraft fleet, ensures a consistent aftermarket demand for replacement and repair of these critical components.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Air Traffic and Aircraft Deliveries | +2.1% | Global, particularly Asia Pacific, North America | 2025-2033 (Long-term) |

| Growing Demand for Fuel-Efficient Aircraft Engines | +1.8% | Global, especially developed economies | 2025-2033 (Long-term) |

| Advancements in Material Science and Manufacturing Technologies | +1.5% | North America, Europe, parts of Asia Pacific (Japan, South Korea) | 2025-2033 (Mid to Long-term) |

| Expansion of Maintenance, Repair, and Overhaul (MRO) Activities | +1.2% | Global, prominent in established aviation hubs | 2025-2033 (Continuous) |

Commercial Aircraft Turbine Blade and Vane Market Restraints Analysis

Despite significant growth prospects, the Commercial Aircraft Turbine Blade and Vane Market faces several notable restraints that could impact its expansion. One significant challenge is the high cost associated with advanced materials like nickel-based superalloys and Ceramic Matrix Composites (CMCs), which are essential for high-performance turbine components. The manufacturing processes for these materials are complex and energy-intensive, directly contributing to elevated production costs. This material expense can increase the overall cost of engine production and MRO activities, potentially limiting widespread adoption, particularly for older aircraft or regional jet segments.

Another critical restraint is the stringent regulatory environment and the extensive certification processes required for aerospace components. Turbine blades and vanes are critical safety components, necessitating rigorous testing, validation, and certification by aviation authorities such as the FAA and EASA. This process is time-consuming and expensive, extending product development cycles and increasing time-to-market for new innovations. Furthermore, geopolitical uncertainties and trade disputes can disrupt global supply chains for raw materials and specialized manufacturing equipment, leading to price volatility and potential delays in production, thereby impacting market stability and growth projections.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Advanced Materials and Manufacturing Processes | -1.3% | Global | 2025-2033 (Ongoing) |

| Stringent Regulatory and Certification Processes | -1.0% | Global, especially North America, Europe | 2025-2033 (Long-term) |

| Supply Chain Vulnerabilities and Geopolitical Instability | -0.8% | Global | 2025-2033 (Short to Mid-term volatility) |

| Skilled Labor Shortage in Aerospace Manufacturing | -0.5% | North America, Europe | 2025-2033 (Ongoing) |

Commercial Aircraft Turbine Blade and Vane Market Opportunities Analysis

The Commercial Aircraft Turbine Blade and Vane Market presents several significant opportunities for growth and innovation. A key opportunity lies in the continuous research and development of next-generation engine architectures, particularly those designed for increased fuel efficiency and reduced environmental impact. These new engine programs will drive demand for innovative blade and vane designs, leveraging advanced materials like Ceramic Matrix Composites (CMCs) and advanced manufacturing techniques such as additive manufacturing. Investments in these areas will yield significant competitive advantages and market share for leading component manufacturers, fostering a new era of component design and performance.

Another substantial opportunity resides in the expansion of aftermarket services, especially for maintenance, repair, and overhaul (MRO) solutions for the vast global commercial aircraft fleet. As aircraft age, the need for replacement and repair of turbine components intensifies, creating a consistent revenue stream for MRO providers. Furthermore, the increasing adoption of sustainable aviation fuels (SAFs) and the development of engines compatible with these fuels could create new design and material requirements for turbine components, opening avenues for specialized solutions. The potential for market expansion into emerging economies with growing aviation sectors, particularly in Asia Pacific and Latin America, also offers considerable long-term growth prospects for component suppliers and MRO providers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Next-Generation Engine Programs | +1.9% | Global, focusing on OEM strongholds | 2027-2033 (Long-term) |

| Advancements and Adoption of Additive Manufacturing | +1.6% | North America, Europe, selected APAC countries | 2025-2033 (Mid to Long-term) |

| Growth in Aftermarket Services and MRO Innovations | +1.4% | Global | 2025-2033 (Continuous) |

| Expansion into Emerging Aviation Markets (APAC, Latin America) | +1.1% | Asia Pacific, Latin America, Middle East | 2026-2033 (Long-term) |

Commercial Aircraft Turbine Blade and Vane Market Challenges Impact Analysis

The Commercial Aircraft Turbine Blade and Vane Market faces several complex challenges that demand strategic responses from industry participants. A primary challenge is the intense competition among established players and emerging entrants, particularly in an industry characterized by high capital investment and stringent performance requirements. This competitive landscape puts pressure on pricing and necessitates continuous innovation to maintain market share, compelling companies to invest heavily in research and development while optimizing production costs, which can impact profitability margins across the value chain.

Another significant challenge is managing the volatility of raw material prices, particularly for critical elements like nickel, cobalt, and titanium, which are essential components of high-performance superalloys. Fluctuations in commodity markets can directly impact production costs and profit margins for manufacturers of turbine blades and vanes. Furthermore, ensuring the long-term reliability and integrity of advanced materials, such as Ceramic Matrix Composites (CMCs), under extreme operating conditions, alongside the complex process of integrating new manufacturing technologies like additive manufacturing into existing production lines, poses substantial technical and operational hurdles. Meeting evolving environmental regulations related to engine noise and emissions also adds complexity to component design and manufacturing processes.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition and Pricing Pressures | -1.1% | Global | 2025-2033 (Ongoing) |

| Volatility in Raw Material Prices | -0.9% | Global | 2025-2033 (Short to Mid-term) |

| Technological Integration and Reliability of New Materials/Processes | -0.7% | Global, particularly R&D hubs | 2025-2030 (Mid-term) |

| Intellectual Property Protection and Counterfeit Parts | -0.4% | Global | 2025-2033 (Ongoing) |

Commercial Aircraft Turbine Blade and Vane Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Commercial Aircraft Turbine Blade and Vane market, offering detailed insights into its size, growth trajectory, key trends, and future outlook from 2025 to 2033. The report meticulously examines the factors influencing market dynamics, including drivers, restraints, opportunities, and challenges, providing a holistic understanding of the industry's landscape. It covers critical market segmentations by material, aircraft type, engine type, application, and manufacturing process, enabling a granular view of market performance across various dimensions. Furthermore, the report features a robust competitive analysis, profiling key market players and their strategic initiatives, alongside regional market assessments to identify growth hotspots and emerging opportunities.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.75 Billion |

| Market Forecast in 2033 | USD 5.03 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Safran S. A., Rolls-Royce plc, General Electric Company, Pratt & Whitney (Raytheon Technologies Corporation), GKN Aerospace, Howmet Aerospace Inc., Arconic Corporation, Siemens Energy, IHI Corporation, MTU Aero Engines AG, Chromalloy Gas Turbine Corporation, Mitsubishi Heavy Industries, Ltd., Toshiba Corporation, Collins Aerospace (Raytheon Technologies Corporation), Liebherr Group, TURBOCAM International, GE Aviation, Aerospace Industrial Development Corporation (AIDC), Hindustan Aeronautics Limited (HAL), Avio Aero (GE Aviation) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Commercial Aircraft Turbine Blade and Vane market is extensively segmented to provide a detailed understanding of its various facets and dynamics. This segmentation allows for precise analysis of market trends, growth drivers, and opportunities across different material types, aircraft categories, engine technologies, application areas, and manufacturing processes. Each segment presents unique characteristics and growth trajectories influenced by technological advancements, regulatory requirements, and shifts in global aviation demand. Understanding these distinct segments is crucial for stakeholders to identify lucrative avenues for investment and strategic development.

The market is primarily segmented by the material composition of the blades and vanes, reflecting the continuous innovation in material science aimed at improving performance and durability under extreme conditions. Further segmentation by aircraft type, including narrow-body, wide-body, and regional jets, highlights the varying demands across commercial aviation sectors. Segmentation by engine type, such as turbofan and turboprop, illustrates the specific design and material requirements for different propulsion systems. The division into OEM and MRO applications distinguishes between initial component supply and aftermarket services, both crucial to the market's overall health. Lastly, segmentation by manufacturing process underscores the growing adoption of advanced techniques like additive manufacturing, which are reshaping the production landscape for these critical components.

- By Material: Nickel-based Superalloys, Cobalt-based Superalloys, Titanium Alloys, Ceramic Matrix Composites (CMCs), Others

- By Aircraft Type: Narrow-body Aircraft, Wide-body Aircraft, Regional Jets, Business Jets, General Aviation

- By Engine Type: Turbofan, Turboprop, Turbojet

- By Application: Original Equipment Manufacturer (OEM), Maintenance, Repair, and Overhaul (MRO)

- By Manufacturing Process: Forging, Casting, Machining, Additive Manufacturing, Others

Regional Highlights

- North America: This region dominates the Commercial Aircraft Turbine Blade and Vane market due to the presence of major aircraft and engine manufacturers, a robust aerospace MRO industry, and significant defense spending that drives technological advancements in turbine components. The U.S. remains a global leader in aerospace research, development, and production.

- Europe: A key hub for aerospace innovation, Europe hosts several leading engine manufacturers and component suppliers. The region benefits from strong governmental support for aerospace R&D and a mature aviation market, contributing significantly to both OEM and MRO segments. Countries like the UK, France, and Germany are at the forefront of advanced material development and manufacturing techniques.

- Asia Pacific (APAC): Expected to exhibit the highest growth rate, driven by surging air passenger traffic, massive fleet expansion initiatives by airlines, and increasing investment in aerospace manufacturing capabilities, particularly in China, India, and Japan. This region represents the largest market for new aircraft deliveries and a rapidly expanding MRO sector.

- Latin America: This region demonstrates steady growth, primarily influenced by fleet modernization efforts and increasing air travel within and to the region. While smaller than other major regions, it presents opportunities for MRO services and new aircraft component demand as commercial fleets expand.

- Middle East and Africa (MEA): Characterized by the rapid expansion of major airlines and strategic investments in aviation infrastructure, particularly in the UAE and Qatar. This growth fuels demand for new aircraft and, consequently, turbine components, alongside a growing need for localized MRO capabilities to support the expanding fleets.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Commercial Aircraft Turbine Blade and Vane Market.- Safran S. A.

- Rolls-Royce plc

- General Electric Company

- Pratt & Whitney (Raytheon Technologies Corporation)

- GKN Aerospace

- Howmet Aerospace Inc.

- Arconic Corporation

- Siemens Energy

- IHI Corporation

- MTU Aero Engines AG

- Chromalloy Gas Turbine Corporation

- Mitsubishi Heavy Industries, Ltd.

- Toshiba Corporation

- Collins Aerospace (Raytheon Technologies Corporation)

- Liebherr Group

- TURBOCAM International

- GE Aviation

- Aerospace Industrial Development Corporation (AIDC)

- Hindustan Aeronautics Limited (HAL)

- Avio Aero (GE Aviation)

Frequently Asked Questions

Analyze common user questions about the Commercial Aircraft Turbine Blade and Vane market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are the primary drivers of growth for the Commercial Aircraft Turbine Blade and Vane market?

The primary growth drivers include the continuous increase in global air passenger traffic and freight volumes, leading to higher demand for new aircraft. Additionally, the aerospace industry's focus on developing more fuel-efficient and environmentally friendly engines, requiring advanced turbine components, significantly propels market expansion.

How is additive manufacturing impacting the production of turbine blades and vanes?

Additive manufacturing, or 3D printing, is revolutionizing production by enabling the creation of highly complex and optimized blade and vane geometries that are difficult to achieve with traditional methods. This technology improves design flexibility, reduces material waste, and can accelerate manufacturing lead times.

What role do advanced materials like CMCs play in this market?

Advanced materials such as Ceramic Matrix Composites (CMCs) are critical for next-generation turbine blades and vanes because they offer superior temperature resistance, lighter weight, and enhanced durability compared to traditional superalloys. Their use allows engines to operate at higher temperatures, improving fuel efficiency and reducing emissions.

Which regions are expected to show the most significant growth in the Commercial Aircraft Turbine Blade and Vane market?

The Asia Pacific (APAC) region is projected to exhibit the most significant growth due to substantial investments in fleet expansion by airlines, rising air travel demand, and the development of indigenous aerospace manufacturing capabilities in countries like China and India.

What are the main challenges faced by manufacturers in this market?

Manufacturers face challenges such as the high cost and volatility of raw materials, stringent regulatory requirements and lengthy certification processes, intense market competition leading to pricing pressures, and the need to integrate and ensure the reliability of new manufacturing technologies and materials.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted