Steam Turbine Market

Steam Turbine Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705385 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

Steam Turbine Market Size

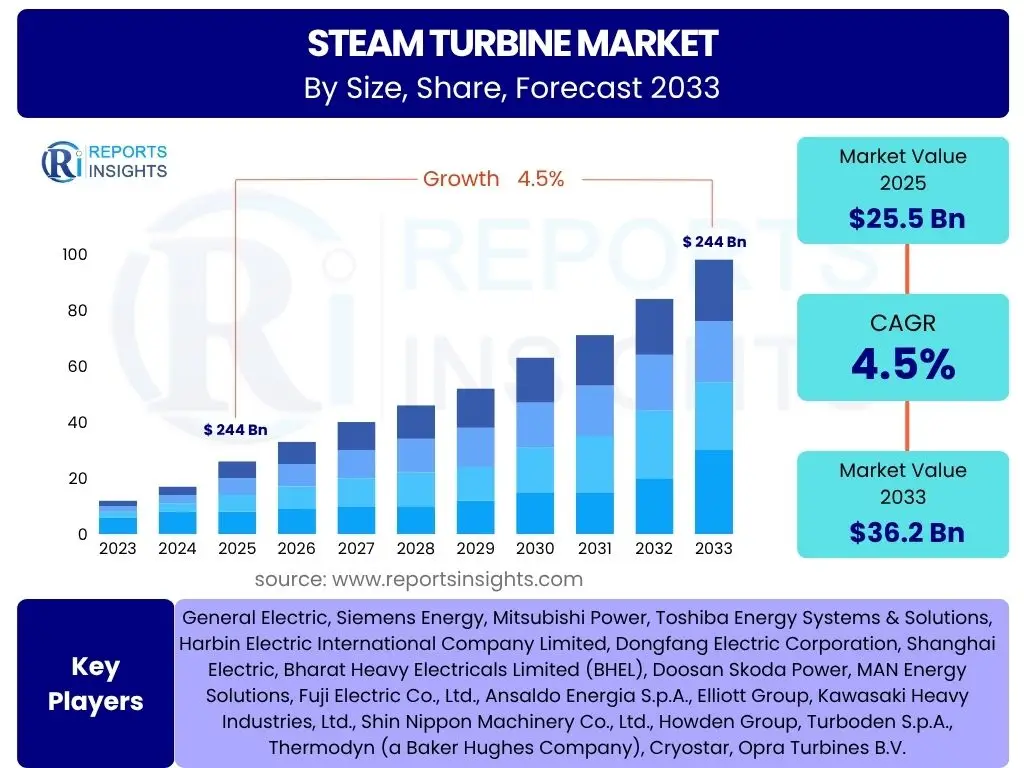

According to Reports Insights Consulting Pvt Ltd, The Steam Turbine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2033. The market is estimated at USD 25.5 Billion in 2025 and is projected to reach USD 36.2 Billion by the end of the forecast period in 2033.

Key Steam Turbine Market Trends & Insights

The Steam Turbine market is undergoing significant transformations driven by global energy transition efforts, increased focus on operational efficiency, and the integration of advanced digital technologies. User inquiries frequently highlight the shift towards cleaner energy sources, the demand for more flexible and reliable power generation solutions, and the ongoing modernization of existing power infrastructure. These trends collectively underscore an industry adapting to evolving environmental mandates and technological advancements while striving to meet continuous global energy demand.

There is a pronounced trend towards enhancing the efficiency of steam turbines to reduce fuel consumption and lower carbon emissions, making them more competitive in a decarbonizing energy landscape. Furthermore, the increasing integration of steam turbines with renewable energy sources, such as Concentrated Solar Power (CSP) and biomass, signifies their crucial role in hybrid power generation systems. This adaptability ensures their continued relevance amidst the growing share of intermittent renewables in the energy mix, providing stable base-load or flexible power as needed.

- Decarbonization and Net-Zero Targets: Growing pressure for cleaner energy generation drives demand for high-efficiency turbines and those compatible with carbon capture technologies or sustainable fuel sources.

- Digitalization and Industry 4.0 Integration: Adoption of IoT, AI, and predictive analytics for enhanced operational efficiency, predictive maintenance, and remote monitoring.

- Focus on Operational Flexibility: Increasing demand for turbines capable of faster ramp-up and ramp-down times to complement intermittent renewable energy sources.

- Modernization and Retrofitting of Existing Plants: Investment in upgrading older turbine fleets to improve efficiency, extend lifespan, and comply with stricter environmental regulations.

- Emergence of Small Modular Reactors (SMRs): Development of smaller, more flexible nuclear power solutions that utilize steam turbines, opening new market segments.

AI Impact Analysis on Steam Turbine

The integration of Artificial Intelligence (AI) is set to significantly revolutionize the Steam Turbine market, addressing common user concerns regarding operational efficiency, maintenance costs, and reliability. Users frequently inquire about AI's potential to optimize performance, predict failures, and automate complex processes within power generation. This indicates a strong interest in how AI can move beyond traditional operational models to create more resilient, efficient, and intelligent steam turbine systems.

AI's influence is primarily manifested through advanced data analytics capabilities, enabling real-time monitoring and anomaly detection that far surpasses human capabilities. This leads to more precise predictive maintenance schedules, reducing unplanned downtime and extending the operational lifespan of critical components. Furthermore, AI-powered algorithms can optimize turbine operation parameters based on fluctuating demand, fuel costs, and environmental conditions, leading to significant fuel savings and reduced emissions. The capacity for AI to learn from vast datasets allows for continuous improvement in turbine performance and responsiveness, making a tangible impact on overall plant economics and environmental footprint.

- Predictive Maintenance: AI algorithms analyze sensor data to predict equipment failures, enabling proactive maintenance and reducing unplanned downtime.

- Operational Optimization: AI-driven controls optimize turbine parameters for maximum efficiency, considering factors like fuel consumption, load demand, and environmental conditions.

- Remote Monitoring and Diagnostics: AI enhances remote capabilities, allowing experts to diagnose issues and provide solutions without on-site presence.

- Design and Engineering Enhancement: AI assists in simulating complex fluid dynamics and thermal properties, leading to more efficient and durable turbine designs.

- Energy Management and Grid Integration: AI-powered systems facilitate seamless integration of steam turbines with smart grids, optimizing power dispatch and balancing supply with demand.

Key Takeaways Steam Turbine Market Size & Forecast

The Steam Turbine market is poised for steady growth, driven by fundamental energy demand and a global shift towards enhancing energy infrastructure efficiency. Common user inquiries often center on the long-term viability of steam turbines amidst renewable energy expansion, and the forecast clearly indicates their enduring importance. The projected market expansion underscores the continued reliance on steam-based power generation in various sectors, even as the energy mix diversifies. This growth is largely influenced by technological advancements improving efficiency and adaptability, alongside strategic investments in both new capacity and modernization of existing plants.

The significant market valuation by 2033 reflects a sustained need for reliable base-load and flexible power generation, where steam turbines excel. While the energy transition is accelerating, steam turbines remain critical for industries and nations requiring consistent and high-capacity power, particularly from sources like nuclear, coal (with carbon capture), natural gas, and biomass. The anticipated Compound Annual Growth Rate (CAGR) further emphasizes the incremental but consistent expansion, highlighting areas of opportunity in efficiency upgrades, new plant constructions in emerging economies, and specialized applications.

- Sustained Growth Trajectory: The market is projected to grow consistently through 2033, indicating continued relevance of steam turbine technology.

- Efficiency as a Primary Driver: Advancements in turbine efficiency are crucial for market competitiveness and meeting environmental targets.

- Diverse Application Portfolio: Steam turbines will continue to be vital across various power generation methods including thermal, nuclear, and concentrated solar power.

- Asia Pacific Dominance: This region is expected to remain a significant growth hub due to ongoing industrialization and power infrastructure development.

- Resilience Amidst Energy Transition: Despite the rise of renewables, steam turbines will maintain a critical role for base-load power and grid stability.

Steam Turbine Market Drivers Analysis

The Steam Turbine market is primarily propelled by the ever-increasing global demand for electricity, particularly from industrial expansion and growing populations in developing economies. As urbanization accelerates and industrial activities intensify, the need for reliable and high-capacity power generation solutions becomes paramount. This fundamental demand underpins new power plant constructions and the expansion of existing facilities, where steam turbines are often the core component due to their proven reliability and scale.

Furthermore, the imperative to replace aging power infrastructure in developed regions significantly drives market growth. Many operational power plants, particularly coal-fired ones, are nearing the end of their design life, necessitating either complete replacement or significant modernization. The pursuit of enhanced energy efficiency across all sectors also contributes positively, as modern steam turbines offer improved heat rates, leading to lower fuel consumption and reduced operational costs. Lastly, favorable government policies promoting industrial growth, electrification, and, in some cases, sustained use of thermal power sources, further stimulate investments in steam turbine technology.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Global Electricity Demand | +1.5% - +2.0% | Asia Pacific, Middle East & Africa | Long-term (2025-2033) |

| Industrial Expansion and Urbanization | +1.0% - +1.5% | China, India, Southeast Asia | Medium-term (2025-2029) |

| Replacement of Aging Power Infrastructure | +0.8% - +1.2% | North America, Europe | Long-term (2025-2033) |

| Increasing Focus on Energy Efficiency | +0.7% - +1.0% | Global, particularly developed economies | Ongoing (2025-2033) |

| Development of Nuclear Power Projects (SMRs) | +0.5% - +0.8% | North America, Europe, East Asia | Long-term (2028-2033) |

| Investment in Concentrated Solar Power (CSP) | +0.3% - +0.6% | MEA, Southwest US, Australia | Medium-term (2026-2031) |

| Rise in Waste-to-Energy Plants | +0.2% - +0.4% | Europe, Asia Pacific | Short-to-Medium term (2025-2028) |

Steam Turbine Market Restraints Analysis

The Steam Turbine market faces significant restraints primarily due to the global energy transition away from fossil fuels, particularly coal, which has historically been a major application area for steam turbines. The rapid proliferation of renewable energy sources such as solar and wind power, which offer lower operational costs and reduced environmental impact, poses a direct competitive threat. This shift often results in the decommissioning of thermal power plants or a reduced investment in new ones, thereby limiting the demand for new steam turbines.

Furthermore, the substantial upfront capital investment required for constructing steam turbine-based power plants, coupled with the long project development cycles, acts as a deterrent for potential investors. Environmental regulations, increasingly stringent emissions standards, and carbon pricing mechanisms also add to the operational costs and regulatory burden for fossil fuel-fired steam turbine plants, making them less attractive. Public opposition to certain types of power generation, such as coal or large-scale nuclear, also contributes to delays or cancellations of projects, impacting market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Penetration of Renewable Energy | -1.5% - -2.0% | Global, especially Europe, North America | Long-term (2025-2033) |

| High Capital Investment Costs | -1.0% - -1.5% | Global | Ongoing (2025-2033) |

| Stringent Environmental Regulations and Policies | -0.8% - -1.2% | Europe, North America, parts of Asia | Ongoing (2025-2033) |

| Long Project Development and Construction Timelines | -0.7% - -1.0% | Global | Ongoing (2025-2033) |

| Public Opposition to Traditional Thermal Power | -0.5% - -0.8% | Developed countries | Medium-term (2025-2029) |

| Fluctuations in Raw Material Prices | -0.3% - -0.6% | Global | Short-term (2025-2027) |

| Geopolitical Instability Affecting Project Funding | -0.2% - -0.4% | Specific conflict zones | Short-to-Medium term (2025-2028) |

Steam Turbine Market Opportunities Analysis

Despite the challenges, significant opportunities exist for the Steam Turbine market, primarily stemming from the global push for energy efficiency and the need for stable base-load power. The modernization and retrofitting of existing power plants represent a substantial segment, as utilities seek to extend asset lifespans, improve efficiency, and reduce emissions without constructing entirely new facilities. This involves upgrading turbine components, controls, and materials to meet contemporary performance standards and regulatory requirements.

The burgeoning interest in Small Modular Reactors (SMRs) and other advanced nuclear technologies presents a compelling new growth avenue. SMRs, due to their smaller footprint, modular construction, and enhanced safety features, are gaining traction globally, and each unit requires highly specialized steam turbines. Furthermore, the growing adoption of industrial co-generation (Combined Heat and Power - CHP) and waste-to-energy facilities offers niche but expanding markets for smaller to medium-sized steam turbines, as industries seek to optimize their energy consumption and manage waste efficiently, leveraging the inherent flexibility of steam cycle power generation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Modernization and Retrofitting of Existing Plants | +1.2% - +1.8% | North America, Europe, China | Long-term (2025-2033) |

| Growth in Small Modular Reactor (SMR) Development | +1.0% - +1.5% | North America, Europe, East Asia | Medium-to-Long term (2027-2033) |

| Increased Adoption of Industrial Co-generation (CHP) | +0.8% - +1.2% | Global, particularly industrial clusters | Ongoing (2025-2033) |

| Development of Waste-to-Energy (WtE) Plants | +0.7% - +1.0% | Europe, Asia Pacific, rapidly urbanizing areas | Medium-term (2025-2030) |

| Expansion of Concentrated Solar Power (CSP) | +0.5% - +0.8% | MEA, Southwest US, Australia, Spain | Medium-term (2026-2031) |

| Applications in Geothermal and Biomass Power | +0.4% - +0.7% | Indonesia, Philippines, Turkey (Geothermal); Europe (Biomass) | Ongoing (2025-2033) |

| Emerging Markets for New Power Capacity | +0.3% - +0.6% | Southeast Asia, Sub-Saharan Africa | Long-term (2028-2033) |

Steam Turbine Market Challenges Impact Analysis

The Steam Turbine market faces several inherent challenges that can impede its growth and widespread adoption. A primary concern is the relatively high upfront cost of manufacturing and installing steam turbines, coupled with the extensive infrastructure requirements for associated power plants. This significant capital outlay can be a barrier to entry, particularly for developing economies or projects with limited access to financing. Furthermore, the long lead times associated with the design, manufacturing, and commissioning of large-scale steam turbines and power plants can create delays and increase project risks, impacting investment decisions.

Another significant challenge stems from the increasing stringency of environmental regulations, particularly concerning greenhouse gas emissions. While steam turbines can be integrated with cleaner fuels or carbon capture technologies, the regulatory landscape often favors renewable energy sources, which do not produce direct emissions. The intermittency of renewable energy also poses a challenge for grid stability, and while steam turbines can offer base-load power, integrating them efficiently with variable renewable output requires sophisticated grid management systems. Lastly, the global supply chain for complex components and specialized materials can be vulnerable to disruptions, impacting production schedules and costs.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure and Project Complexity | -1.2% - -1.8% | Global | Ongoing (2025-2033) |

| Increasingly Stringent Environmental Regulations | -1.0% - -1.5% | Europe, North America, emerging Asian economies | Ongoing (2025-2033) |

| Long Lead Times and Complex Supply Chains | -0.8% - -1.2% | Global | Ongoing (2025-2033) |

| Competition from Decentralized Energy Solutions | -0.7% - -1.0% | Developed markets | Medium-term (2025-2030) |

| Integration Challenges with Intermittent Renewables | -0.5% - -0.8% | Regions with high renewable penetration | Ongoing (2025-2033) |

| Skilled Labor Shortages for Installation and Maintenance | -0.4% - -0.7% | Global | Long-term (2025-2033) |

| Technological Advancements in Competitor Technologies | -0.3% - -0.6% | Global | Ongoing (2025-2033) |

Steam Turbine Market - Updated Report Scope

This market research report provides an in-depth analysis of the global Steam Turbine market, offering a comprehensive overview of its current size, historical performance, and future growth projections. The scope includes a detailed examination of market drivers, restraints, opportunities, and challenges, along with an impact analysis of artificial intelligence on the industry. The report segments the market by type, capacity, application, and provides a thorough regional analysis, identifying key growth areas and competitive landscapes. It aims to furnish stakeholders with actionable insights for strategic decision-making in the dynamic energy sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 25.5 Billion |

| Market Forecast in 2033 | USD 36.2 Billion |

| Growth Rate | 4.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | General Electric, Siemens Energy, Mitsubishi Power, Toshiba Energy Systems & Solutions, Harbin Electric International Company Limited, Dongfang Electric Corporation, Shanghai Electric, Bharat Heavy Electricals Limited (BHEL), Doosan Skoda Power, MAN Energy Solutions, Fuji Electric Co., Ltd., Ansaldo Energia S.p.A., Elliott Group, Kawasaki Heavy Industries, Ltd., Shin Nippon Machinery Co., Ltd., Howden Group, Turboden S.p.A., Thermodyn (a Baker Hughes Company), Cryostar, Opra Turbines B.V. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Steam Turbine market is comprehensively segmented across various dimensions to provide granular insights into its structure and growth drivers. These segmentations are critical for understanding specific market dynamics, identifying niche opportunities, and tailoring strategic approaches. The primary categorizations include type, capacity, and application, each revealing distinct trends and competitive landscapes within the broader market.

By type, steam turbines are categorized based on their exhaust conditions and operational mechanisms, influencing their suitability for different power generation and industrial processes. Capacity segmentation highlights the demand for turbines ranging from small industrial units to large utility-scale power plant components, reflecting diverse energy needs. Application-wise, the market is broadly divided between dedicated power generation for national grids and industrial power generation, encompassing a wide array of heavy industries that utilize steam for process heat and electricity production. These detailed segments allow for a precise analysis of market movements and future potential.

- By Type:

- Condensing Steam Turbine: Predominantly used in large utility-scale power plants for maximizing electricity generation.

- Back-pressure Steam Turbine: Utilized in industrial applications where process heat is needed after power generation, optimizing energy efficiency.

- Extraction Steam Turbine: Offers flexibility by allowing steam to be extracted at intermediate stages for process heat while the remaining steam continues to generate power.

- Others: Includes specific designs like impulse and reaction turbines catering to specialized requirements.

- By Capacity:

- Small (Below 100 MW): Typically for industrial co-generation, distributed power, or smaller renewable energy projects.

- Medium (100 MW - 500 MW): Common in mid-sized power plants, industrial complexes, and some nuclear or concentrated solar power (CSP) facilities.

- Large (Above 500 MW): Primarily deployed in large-scale thermal (coal, gas) and nuclear power plants for base-load electricity supply.

- By Application:

- Power Generation:

- Coal Power Plants: Traditional largest segment, though facing decline in some regions.

- Nuclear Power Plants: Essential for stable, high-capacity base-load power.

- Natural Gas Power Plants: Increasingly used for flexible power generation, often combined cycle.

- Geothermal Power Plants: Utilizing earth's heat for continuous clean energy.

- Biomass Power Plants: Converting organic matter into electricity and heat.

- Concentrated Solar Power (CSP) Plants: Using solar thermal energy to drive steam turbines.

- Industrial Power Generation:

- Oil and Gas: For refinery operations and platform power.

- Chemicals and Petrochemicals: Essential for process heat and electricity.

- Metals and Mining: Providing power for heavy machinery and smelting.

- Pulp and Paper: Energy for paper production and associated processes.

- Sugar: Utilizing bagasse for co-generation.

- Food and Beverage: For various heating and sterilization processes.

- Others: Diverse industrial applications requiring steam.

- Power Generation:

Regional Highlights

- North America: This region demonstrates a mature market with a significant focus on modernizing existing power infrastructure and investing in advanced nuclear technologies like Small Modular Reactors (SMRs). While coal-fired power plants are being phased out, demand for steam turbines in natural gas combined cycle plants, industrial co-generation, and emerging geothermal projects remains stable. The U.S. and Canada are leading in efficiency upgrades and smart grid integration.

- Europe: Characterized by stringent environmental regulations and aggressive decarbonization targets, Europe's steam turbine market is driven by retrofitting for higher efficiency, biomass-fired power plants, and waste-to-energy initiatives. There is also a growing interest in new nuclear builds in some countries and the application of steam turbines in industrial process heating and power generation.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, fueled by rapid industrialization, increasing urbanization, and expanding electricity demand, particularly in China, India, and Southeast Asian nations. Significant investments in new coal-fired power plants (though declining in some areas), nuclear power development, and various industrial applications, including petrochemicals and metals, drive this growth. The region also sees a rise in Concentrated Solar Power (CSP) projects in sun-rich areas.

- Latin America: This region presents a mix of opportunities, with countries like Brazil showing demand for biomass-based power generation and industrial applications. New power capacity additions, including natural gas and some geothermal projects, contribute to the steam turbine market here, alongside ongoing efforts to enhance energy access and reliability.

- Middle East and Africa (MEA): The Middle East is a key market due to substantial investments in new natural gas-fired power plants and large-scale Concentrated Solar Power (CSP) projects. Africa, particularly Sub-Saharan Africa, represents a long-term growth opportunity driven by increasing electrification efforts, industrial development, and the need for diverse energy sources, including new coal and gas power plants, where applicable.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Steam Turbine Market.- General Electric

- Siemens Energy

- Mitsubishi Power

- Toshiba Energy Systems & Solutions

- Harbin Electric International Company Limited

- Dongfang Electric Corporation

- Shanghai Electric

- Bharat Heavy Electricals Limited (BHEL)

- Doosan Skoda Power

- MAN Energy Solutions

- Fuji Electric Co., Ltd.

- Ansaldo Energia S.p.A.

- Elliott Group

- Kawasaki Heavy Industries, Ltd.

- Shin Nippon Machinery Co., Ltd.

- Howden Group

- Turboden S.p.A.

- Thermodyn (a Baker Hughes Company)

- Cryostar

- Opra Turbines B.V.

Frequently Asked Questions

Analyze common user questions about the Steam Turbine market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate for the Steam Turbine Market?

The Steam Turbine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2033, indicating steady expansion.

Which factors are primarily driving the Steam Turbine Market growth?

Key drivers include increasing global electricity demand, industrial expansion, the need for replacing aging power infrastructure, and a continuous focus on enhancing energy efficiency in power generation.

How is AI impacting the Steam Turbine industry?

AI is transforming the industry through predictive maintenance, operational optimization for efficiency, remote monitoring and diagnostics, and aiding in the design of more advanced turbine systems.

What are the main applications of steam turbines?

Steam turbines are primarily used in large-scale power generation (coal, nuclear, natural gas, geothermal, biomass, CSP) and various industrial applications such as oil & gas, chemicals, metals, and pulp & paper for combined heat and power (CHP).

Which region is expected to lead the Steam Turbine Market?

The Asia Pacific (APAC) region is anticipated to be the largest and fastest-growing market due to rapid industrialization, urbanization, and significant investments in new power capacity.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted