Wind Turbine Component Market

Wind Turbine Component Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704354 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

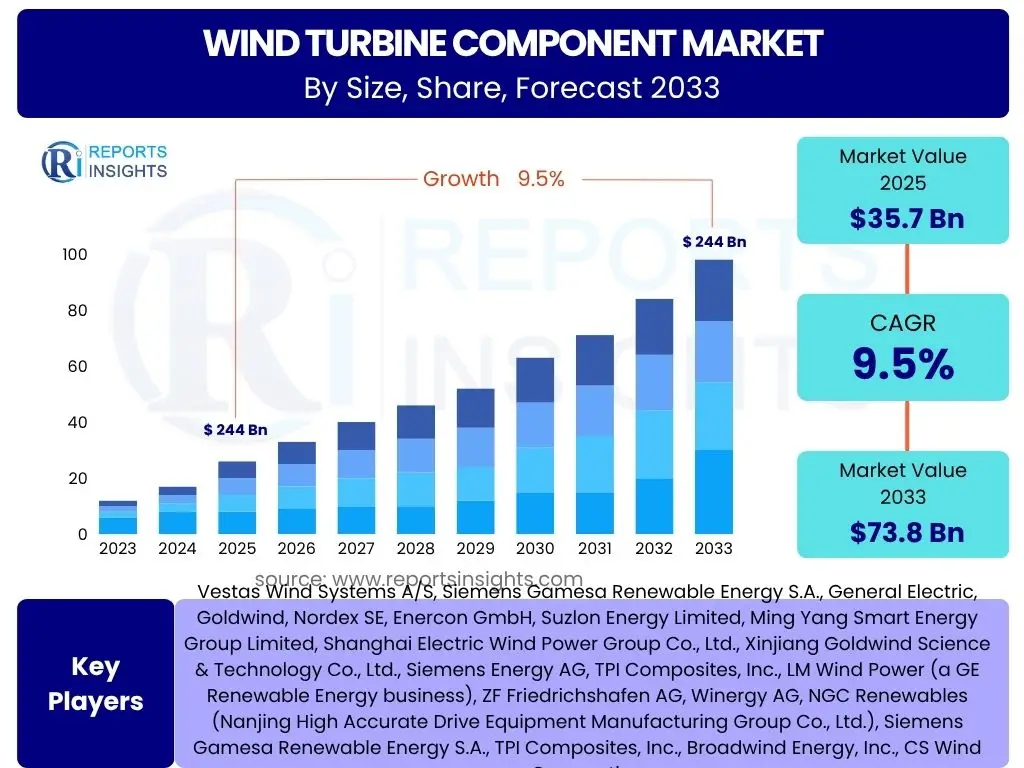

Wind Turbine Component Market Size

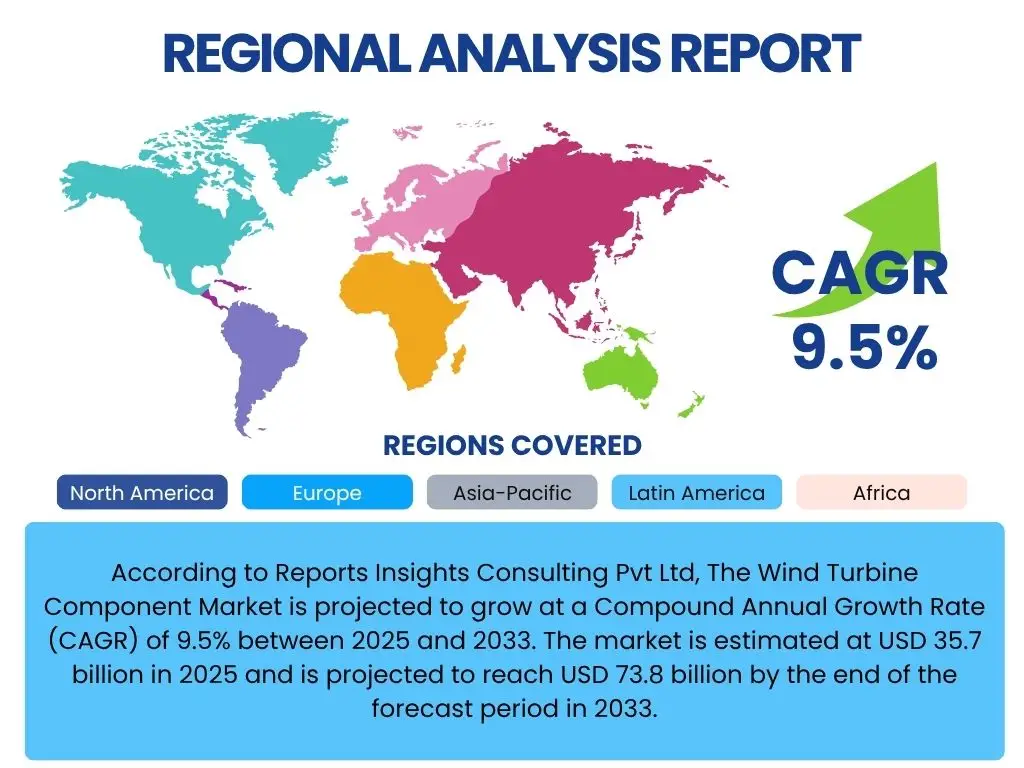

According to Reports Insights Consulting Pvt Ltd, The Wind Turbine Component Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 35.7 billion in 2025 and is projected to reach USD 73.8 billion by the end of the forecast period in 2033.

Key Wind Turbine Component Market Trends & Insights

User inquiries frequently focus on the evolving landscape of wind energy technology and market dynamics. Analysis indicates a strong emphasis on larger, more efficient turbine designs, the expansion of offshore wind projects, and the integration of advanced digital technologies for enhanced performance and maintenance. Stakeholders are particularly interested in how these trends influence component demand, manufacturing processes, and the overall supply chain resilience. The shift towards circular economy principles and sustainable materials also represents a significant area of interest, reflecting a broader industry commitment to environmental responsibility alongside energy generation targets. Furthermore, the global push for decarbonization and energy independence is accelerating the adoption of wind power, driving continuous innovation in component design and material science to meet increasing energy demands.

The market is witnessing a profound transformation driven by technological advancements aimed at improving efficiency, reducing operational costs, and extending the lifespan of wind turbines. This includes the development of lighter, stronger blades made from advanced composites, more robust drivetrains capable of handling higher capacities, and sophisticated control systems that optimize energy capture. The trend towards modular design is also gaining traction, facilitating easier transportation, installation, and maintenance of large-scale components. These innovations are critical for achieving the lower Levelized Cost of Energy (LCOE) required to make wind power increasingly competitive with traditional energy sources, thereby stimulating further investment and expansion.

- Turbine Upscaling: Development and deployment of larger capacity turbines (10MW+) for enhanced power output.

- Offshore Wind Expansion: Significant investment and project pipeline growth in offshore wind farms globally, including floating offshore wind technology.

- Advanced Materials: Increased adoption of composite materials, recyclables, and sustainable solutions for blades and other components.

- Digitalization and IoT: Integration of sensors, data analytics, and Artificial Intelligence for predictive maintenance and operational optimization.

- Supply Chain Localization: Efforts to localize component manufacturing and reduce reliance on single-source suppliers to enhance resilience.

- Hybrid Power Solutions: Growing interest in combining wind energy with energy storage systems and other renewable sources for grid stability.

AI Impact Analysis on Wind Turbine Component

User questions regarding Artificial Intelligence's impact on the wind turbine component market frequently revolve around its potential to revolutionize operational efficiency, predictive maintenance, and design optimization. There is significant interest in how AI algorithms can analyze vast datasets from turbine sensors to anticipate failures, optimize performance in real-time based on weather conditions, and extend asset lifespan. Stakeholders also inquire about AI's role in the design and manufacturing phases, including material selection, aerodynamic profiling, and quality control. The general expectation is that AI will drive down operational expenditures (OpEx), improve energy yield, and contribute to more sustainable and reliable wind energy systems, addressing key challenges in the industry.

AI’s influence extends across the entire lifecycle of wind turbine components, from initial concept and design through manufacturing, operation, and end-of-life management. In the design phase, AI-driven simulations can rapidly iterate on component geometries and material compositions, leading to more efficient and durable designs. During manufacturing, AI-powered vision systems and robotics enhance precision and quality control, reducing defects and waste. For operational phases, AI is pivotal in predictive analytics, enabling condition-based monitoring that detects anomalies and predicts component failures before they occur, thus minimizing downtime and maintenance costs. This proactive approach significantly improves the reliability and availability of wind assets, which is critical for maximizing energy production and investment returns.

- Predictive Maintenance: AI algorithms analyze sensor data to forecast component failures, enabling proactive repairs and reducing downtime.

- Optimized Performance: AI fine-tunes turbine pitch and yaw in real-time based on wind conditions, maximizing energy capture and reducing stress on components.

- Design Optimization: AI-driven simulations accelerate the design of more aerodynamically efficient blades and robust mechanical components.

- Quality Control: AI-powered vision systems enhance precision and detect manufacturing defects in components, improving overall product quality.

- Site Selection & Resource Assessment: AI analyzes vast meteorological and topographical data for optimal wind farm component deployment.

- Supply Chain Management: AI improves forecasting for component demand, optimizing inventory and logistics for manufacturers and operators.

Key Takeaways Wind Turbine Component Market Size & Forecast

Common user inquiries often seek a concise summary of the most critical insights derived from the wind turbine component market size and forecast. The primary takeaway is the robust and sustained growth projected for the market, driven by an accelerating global commitment to renewable energy and supportive governmental policies. This expansion is underpinned by continuous technological advancements leading to larger, more efficient turbines and a strong emphasis on offshore wind development. The market is not only growing in terms of volume but also evolving in complexity, demanding innovation in material science, manufacturing processes, and digital integration. These factors collectively position the wind turbine component sector as a dynamic and strategically important segment within the broader renewable energy landscape.

Furthermore, the forecast highlights the increasing financial viability and competitiveness of wind energy, primarily due to the decreasing Levelized Cost of Energy (LCOE) over time. This makes wind power an attractive investment and a key solution for meeting escalating electricity demand and climate targets. The demand for specialized and high-performance components, such as longer blades, advanced drivetrains, and sophisticated control systems, is expected to surge, creating significant opportunities for manufacturers and suppliers. The market's resilience will increasingly depend on diversified supply chains, sustainable manufacturing practices, and the ability to adapt to rapid technological shifts, ensuring long-term growth and stability.

- Significant Market Expansion: Projected robust growth from USD 35.7 billion in 2025 to USD 73.8 billion by 2033, indicating a healthy investment landscape.

- Strong CAGR: A Compound Annual Growth Rate of 9.5% highlights sustained momentum and increasing adoption of wind energy globally.

- Technological Advancements: Growth is significantly propelled by innovations in turbine size, material science, and digital integration.

- Offshore Wind Dominance: Offshore projects, especially floating solutions, are expected to be a key growth driver for specialized components.

- Policy-Driven Growth: Government incentives, renewable energy targets, and decarbonization efforts worldwide are crucial enablers of market expansion.

- Supply Chain Focus: Resilience and localization of component manufacturing are becoming critical factors for market stability and future growth.

Wind Turbine Component Market Drivers Analysis

The wind turbine component market's expansion is fundamentally propelled by the global imperative to transition towards sustainable energy sources and mitigate climate change. This overarching drive is manifested through various governmental policies and international agreements that set ambitious renewable energy targets and provide financial incentives for wind power development. Decreasing Levelized Cost of Energy (LCOE) for wind energy, primarily due to technological advancements and economies of scale, has made it increasingly competitive with traditional fossil fuels. This cost reduction makes wind projects more attractive to investors and utility companies, directly stimulating demand for high-performance and cost-effective components.

Furthermore, growing concerns over energy security and geopolitical stability are prompting nations to diversify their energy mix and reduce reliance on imported fossil fuels. Wind energy, as a domestic and inexhaustible resource, offers a compelling solution, driving increased investment in large-scale wind farm developments. The continuous innovation in turbine technology, including the development of larger turbines with higher power output and enhanced efficiency, directly translates into increased demand for specialized, robust, and advanced components. These drivers collectively create a fertile ground for sustained growth in the wind turbine component manufacturing sector.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Decarbonization Goals & Policies | +2.5% | Global, particularly Europe, North America, China | 2025-2033 |

| Decreasing LCOE of Wind Energy | +1.8% | Global, especially emerging economies | 2025-2033 |

| Technological Advancements & Turbine Upscaling | +1.5% | Global, leading R&D nations (Germany, Denmark, China) | 2025-2033 |

| Energy Security & Independence Initiatives | +1.2% | Europe, North America, India | 2025-2033 |

| Supportive Regulatory Frameworks & Incentives | +1.0% | North America (PTC/ITC), Europe (Auctions), Asia Pacific (FIT) | 2025-2033 |

Wind Turbine Component Market Restraints Analysis

Despite the robust growth trajectory, the wind turbine component market faces several significant restraints that could impede its full potential. One of the primary concerns is grid integration challenges, where existing electrical grids may not be sufficiently robust or intelligent to handle the intermittent nature of wind power at large scales. This can lead to curtailment of wind generation, impacting project viability and the demand for new components. Another restraint is the 'Not In My Backyard' (NIMBY) phenomenon, where local opposition to wind farm development due to visual impact, noise concerns, or potential environmental effects can delay or halt projects, limiting the deployment of turbines and their components.

Furthermore, supply chain bottlenecks and geopolitical tensions present substantial risks. The global wind industry relies on a complex supply chain for raw materials and specialized components, and disruptions from events like pandemics, trade disputes, or natural disasters can lead to increased costs and delayed deliveries. High upfront capital expenditures for manufacturing facilities and large-scale wind projects also serve as a barrier, particularly for new entrants or regions with limited access to financing. These restraints necessitate strategic planning, technological solutions, and collaborative efforts across the industry and with governments to mitigate their impact on market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Grid Integration & Infrastructure Limitations | -1.5% | Global, especially developing regions | 2025-2030 |

| Permitting & Siting Challenges (NIMBY) | -1.0% | Europe, North America, densely populated areas | 2025-2033 |

| Supply Chain Volatility & Geopolitical Risks | -0.8% | Global, particularly regions reliant on specific imports | 2025-2028 |

| High Upfront Capital Expenditure | -0.7% | Emerging markets, new project developers | 2025-2033 |

| Raw Material Price Fluctuations | -0.5% | Global, particularly for steel, rare earth elements, composites | 2025-2027 |

Wind Turbine Component Market Opportunities Analysis

The wind turbine component market is characterized by several promising opportunities that can significantly accelerate its growth. The substantial global potential for offshore wind energy, especially the development of floating offshore wind technology, represents a vast untapped resource. As conventional onshore sites become saturated and turbine sizes increase, offshore locations offer stronger and more consistent wind resources, driving demand for specialized, robust, and corrosion-resistant components designed for marine environments. This segment is poised for exponential growth, opening new revenue streams for component manufacturers and service providers.

Another key opportunity lies in the growing trend of repowering older wind farms. As turbines age and technology advances, replacing older, less efficient models with modern, higher-capacity turbines can significantly boost energy output and extend the operational life of existing sites. This creates a recurring demand for new components, from blades and drivetrains to control systems, even in mature wind energy markets. Furthermore, the integration of wind power with green hydrogen production offers a novel pathway for energy storage and decarbonization of hard-to-abate sectors, potentially driving demand for components used in electrolyzers and associated infrastructure powered by dedicated wind farms. The expansion into emerging markets, particularly in Asia, Africa, and Latin America, also presents significant growth avenues as these regions increasingly invest in renewable energy infrastructure to meet their growing energy demands and climate commitments.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Offshore Wind Farm Development (Fixed & Floating) | +2.0% | Europe, North America, East Asia (China, Japan, South Korea) | 2025-2033 |

| Repowering of Existing Wind Farms | +1.5% | Europe, North America, mature markets | 2025-2033 |

| Integration with Green Hydrogen Production | +1.2% | Europe, Australia, North America, regions with H2 strategies | 2028-2033 |

| Expansion into Emerging Markets | +1.0% | India, Southeast Asia, Latin America, parts of Africa | 2025-2033 |

| Advancements in Composite Materials & Manufacturing | +0.8% | Global, R&D focused countries | 2025-2033 |

Wind Turbine Component Market Challenges Impact Analysis

The wind turbine component market faces several inherent challenges that require innovative solutions and strategic foresight. One significant challenge is the volatility of raw material prices, particularly for steel, copper, and rare earth elements critical for generators and magnets, as well as composite resins for blades. Unpredictable price fluctuations can severely impact manufacturing costs, profit margins, and the overall competitiveness of wind projects. This necessitates robust supply chain management and diversification strategies to mitigate financial risks. Another critical challenge is the inherent intermittency of wind power, which poses complexities for grid stability and requires sophisticated energy storage solutions or grid upgrades, adding to project costs and potentially slowing down deployment.

The increasing size and complexity of modern wind turbine components, while beneficial for energy generation, also present logistical and manufacturing hurdles. Transporting colossal blades and nacelles to remote onshore sites or integrating them into complex offshore installations requires specialized infrastructure and highly skilled labor. Furthermore, the environmental impact concerns related to turbine component manufacturing, particularly the disposal of composite blades at the end of their operational life, are growing. This prompts a need for more sustainable materials and circular economy solutions. Addressing these challenges requires collaborative efforts across the industry, significant investment in research and development, and supportive regulatory frameworks to ensure the continued sustainable growth of the wind energy sector.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Price Volatility & Supply Disruptions | -1.2% | Global, particularly for specialized metals and composites | 2025-2028 |

| Logistical & Transportation Complexities for Large Components | -0.9% | Global, especially for remote or offshore sites | 2025-2033 |

| Skilled Labor Shortages & Workforce Development | -0.7% | Global, particularly in manufacturing and O&M | 2025-2033 |

| End-of-Life Management & Recycling of Blades | -0.6% | Europe, North America, countries with strict environmental regulations | 2028-2033 |

| Cybersecurity Threats to Digitalized Components & Systems | -0.4% | Global, particularly critical infrastructure | 2025-2033 |

Wind Turbine Component Market - Updated Report Scope

This report provides a comprehensive analysis of the global Wind Turbine Component Market, offering detailed insights into market size, growth drivers, restraints, opportunities, and challenges. It segments the market by component type, application, and end-use, providing granular data for strategic decision-making. The scope also includes a thorough examination of regional dynamics, competitive landscape, and the impact of emerging technologies such as Artificial Intelligence. The forecast period extends to 2033, providing long-term projections and identifying key trends shaping the industry's future. The report is designed to assist stakeholders, investors, and industry participants in understanding market potential, identifying growth avenues, and formulating effective business strategies.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 35.7 billion |

| Market Forecast in 2033 | USD 73.8 billion |

| Growth Rate | 9.5% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Vestas Wind Systems A/S, Siemens Gamesa Renewable Energy S.A., General Electric, Goldwind, Nordex SE, Enercon GmbH, Suzlon Energy Limited, Ming Yang Smart Energy Group Limited, Shanghai Electric Wind Power Group Co., Ltd., Xinjiang Goldwind Science & Technology Co., Ltd., Siemens Energy AG, TPI Composites, Inc., LM Wind Power (a GE Renewable Energy business), ZF Friedrichshafen AG, Winergy AG, NGC Renewables (Nanjing High Accurate Drive Equipment Manufacturing Group Co., Ltd.), Siemens Gamesa Renewable Energy S.A., TPI Composites, Inc., Broadwind Energy, Inc., CS Wind Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Wind Turbine Component Market is meticulously segmented to provide a granular understanding of its diverse landscape and address specific market dynamics. This segmentation allows for targeted analysis of supply and demand across various product types, operational environments, and end-use applications, offering valuable insights for market participants. Understanding these distinct segments is crucial for identifying niche opportunities, tailoring product development, and optimizing market entry strategies. The market can be broadly categorized by the specific components that constitute a wind turbine, differentiating between key structural, mechanical, and electrical elements.

Further segmentation by application highlights the growing distinction between onshore and offshore wind farms, each requiring unique component specifications and installation expertise due to varying environmental conditions and logistical challenges. The onshore segment, traditionally dominant, continues to expand with larger and more efficient turbines, while offshore wind is experiencing rapid growth due to superior wind resources and scalable project sizes. Lastly, segmentation by end-use provides insights into the primary sectors driving demand, ranging from utility-scale power generation to industrial and commercial applications, reflecting the diverse consumption patterns and regulatory frameworks across different economic segments.

- By Component

- Blades

- Nacelles

- Towers

- Drivetrains (Gearboxes, Generators, Main Shafts)

- Generators

- Gearboxes

- Control Systems

- Others (Bearings, Brakes, Yaw and Pitch Systems, Cooling Systems)

- By Application

- Onshore

- Offshore

- By End-Use

- Utility

- Industrial

- Commercial

Regional Highlights

- Asia Pacific (APAC): Dominates the market, driven by massive wind energy expansion in China and India, coupled with growing investments in offshore wind by countries like Japan, South Korea, and Australia. Supportive government policies and ambitious renewable energy targets fuel component demand.

- Europe: A mature and pioneering market for wind energy, characterized by significant offshore wind development, particularly in the North Sea. Strong regulatory support, high decarbonization targets, and an emphasis on technological innovation drive demand for advanced components. Germany, UK, Denmark, and Spain are key contributors.

- North America: Exhibiting robust growth, primarily led by the United States with its Production Tax Credit (PTC) and Investment Tax Credit (ITC) driving onshore wind installations. Canada also contributes, with increasing focus on renewable energy targets. Future growth is anticipated from offshore wind projects along the East Coast.

- Latin America: Emerging as a significant market with countries like Brazil, Mexico, and Chile investing heavily in wind energy to diversify their power grids and meet growing electricity demand. Abundant wind resources and supportive policies attract foreign investments in wind farm development, stimulating component demand.

- Middle East and Africa (MEA): A nascent but rapidly growing market, driven by ambitious renewable energy plans in countries such as Saudi Arabia, UAE, and Egypt in the Middle East, and South Africa and Morocco in Africa. Investment in utility-scale wind projects is increasing, leading to a gradual rise in demand for wind turbine components as infrastructure develops.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Wind Turbine Component Market.- Vestas Wind Systems A/S

- Siemens Gamesa Renewable Energy S.A.

- General Electric

- Goldwind

- Nordex SE

- Enercon GmbH

- Suzlon Energy Limited

- Ming Yang Smart Energy Group Limited

- Shanghai Electric Wind Power Group Co., Ltd.

- Xinjiang Goldwind Science & Technology Co., Ltd.

- Siemens Energy AG

- TPI Composites, Inc.

- LM Wind Power (a GE Renewable Energy business)

- ZF Friedrichshafen AG

- Winergy AG

- NGC Renewables (Nanjing High Accurate Drive Equipment Manufacturing Group Co., Ltd.)

- Broadwind Energy, Inc.

- CS Wind Corporation

- Mita-Teknik A/S

- Bachmann electronic GmbH

Frequently Asked Questions

What is the projected growth rate of the Wind Turbine Component Market?

The Wind Turbine Component Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033, indicating robust expansion driven by global renewable energy initiatives.

What are the primary drivers of growth in the Wind Turbine Component Market?

Key drivers include global decarbonization goals, decreasing Levelized Cost of Energy (LCOE) for wind, technological advancements in turbine design, and supportive government policies and incentives worldwide.

How is Artificial Intelligence impacting the Wind Turbine Component Market?

AI is significantly impacting the market by enabling predictive maintenance, optimizing turbine performance, accelerating component design, and enhancing quality control in manufacturing processes.

What are the main challenges facing the Wind Turbine Component Market?

Major challenges include raw material price volatility, complex logistics for large components, skilled labor shortages, and environmental concerns related to end-of-life component management and recycling.

Which regions are leading the growth in the Wind Turbine Component Market?

Asia Pacific, particularly China and India, currently leads the market due to extensive wind energy deployment. Europe and North America also exhibit strong growth, driven by mature offshore wind sectors and favorable policies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted