ESD Suppression Component Market

ESD Suppression Component Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703857 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

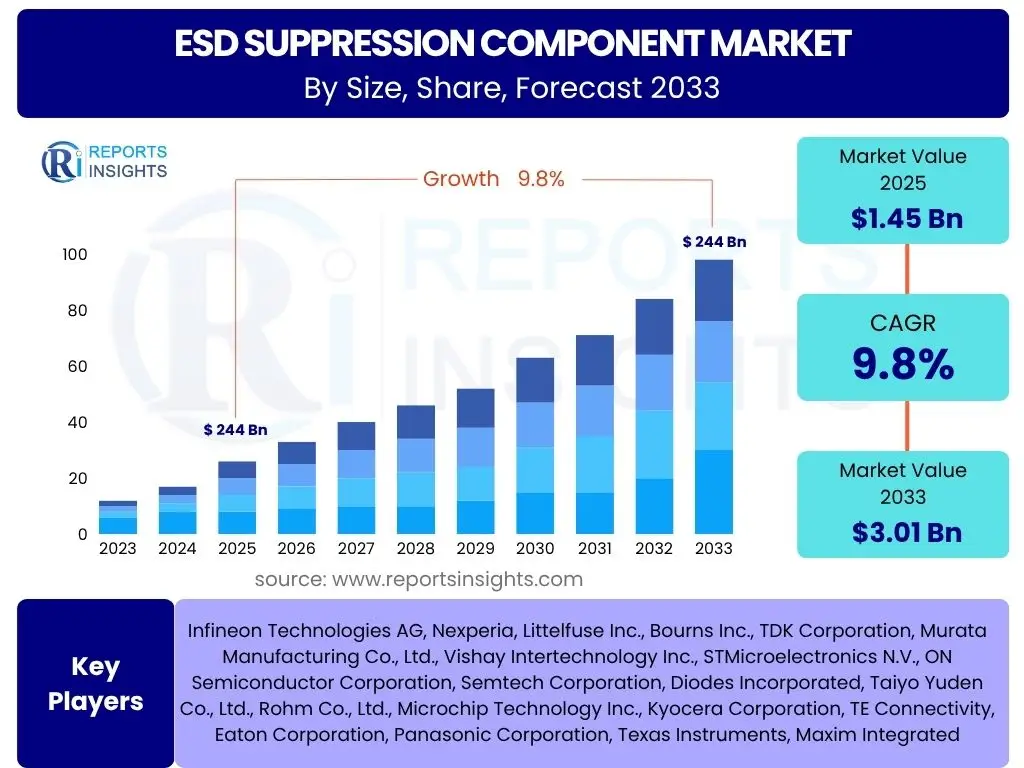

ESD Suppression Component Market Size

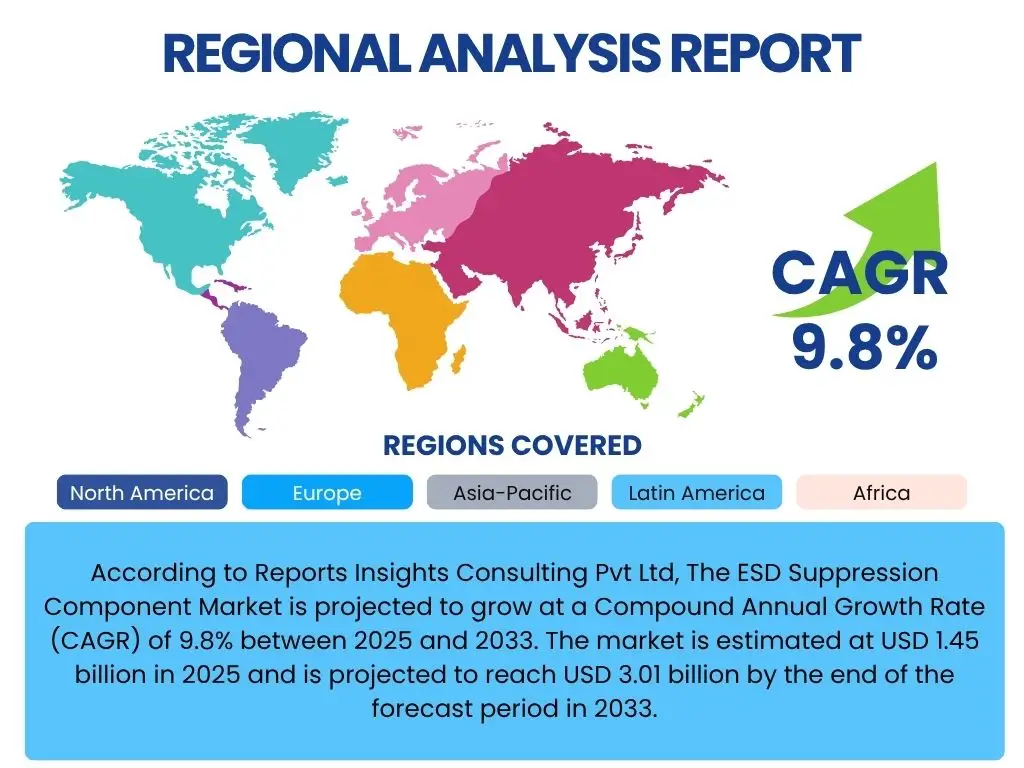

According to Reports Insights Consulting Pvt Ltd, The ESD Suppression Component Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. The market is estimated at USD 1.45 billion in 2025 and is projected to reach USD 3.01 billion by the end of the forecast period in 2033.

Key ESD Suppression Component Market Trends & Insights

Common inquiries from industry stakeholders often revolve around the evolving technological landscape, the impact of new application areas, and the overarching demand for enhanced device protection. The market for ESD suppression components is currently witnessing significant shifts driven by advancements in semiconductor technology, the pervasive integration of electronic systems into everyday objects, and the increasing stringency of regulatory standards. These trends necessitate smaller, more efficient, and robust ESD solutions, pushing manufacturers towards innovation in material science and component design.

Furthermore, the miniaturization of electronic devices, particularly in consumer electronics and wearable technology, presents a dual challenge and opportunity for ESD component manufacturers. While smaller devices require increasingly compact protection solutions, they also amplify the risk of ESD events due to higher component density and reduced physical spacing. This trend, coupled with the global push for sustainability, is also influencing the demand for lead-free and environmentally compliant ESD solutions, compelling market players to align with green manufacturing practices.

- Miniaturization and high-density integration in electronic devices.

- Increasing adoption of Wide Band Gap (WBG) semiconductors (SiC, GaN) requiring specialized ESD protection.

- Growing demand from electric vehicles (EVs) and autonomous driving systems.

- Proliferation of IoT devices and interconnected smart systems.

- Development of multi-functional and ultra-low capacitance ESD components.

- Stricter electromagnetic compatibility (EMC) and ESD standards globally.

AI Impact Analysis on ESD Suppression Component

User discussions frequently explore how artificial intelligence (AI) will influence the design, testing, and application of ESD suppression components, as well as the new demands placed on these components by AI-driven hardware. AI's immediate impact is observed in accelerating research and development cycles, enabling predictive analytics for component failure, and optimizing manufacturing processes for greater efficiency and yield. AI algorithms can simulate complex ESD events, predict component performance under various stress conditions, and assist in designing more resilient and compact protection solutions.

Beyond manufacturing and design, the proliferation of AI-powered devices, from advanced driver-assistance systems (ADAS) in vehicles to complex data centers and edge computing devices, inherently increases the need for robust ESD protection. These sophisticated systems process vast amounts of data at high speeds, making them highly susceptible to electrostatic discharge. AI hardware often incorporates sensitive processors, memory, and high-speed interfaces, all of which require meticulous ESD suppression to ensure reliability and longevity, driving demand for specialized, high-performance components.

- AI-driven optimization of ESD component design and material selection.

- Enhanced predictive maintenance and failure analysis for ESD components using AI.

- Increased demand for robust ESD protection in AI accelerators, edge computing devices, and data center infrastructure.

- AI-assisted quality control and testing methodologies in ESD component manufacturing.

- Development of intelligent ESD solutions capable of adaptive protection.

Key Takeaways ESD Suppression Component Market Size & Forecast

Analysis of user questions regarding the market size and forecast for ESD suppression components consistently points to a strong growth trajectory, driven by the expanding electronics sector and increasing regulatory scrutiny. The primary insights derived from these discussions highlight the indispensability of ESD protection in modern electronic systems, reinforcing the market's resilience against economic fluctuations. Stakeholders are particularly interested in understanding which application areas will contribute most significantly to growth and how component technologies will evolve to meet future demands.

The forecast indicates sustained expansion, primarily fueled by the continued proliferation of smart devices, advancements in automotive electronics, and the build-out of 5G infrastructure. Furthermore, the rising awareness among consumers and manufacturers regarding device reliability and longevity plays a crucial role in driving the adoption of high-quality ESD solutions. The market's growth is also underpinned by ongoing innovation in materials science, leading to more effective and compact suppression components that can protect increasingly sensitive circuits.

- Significant growth anticipated, driven by consumer electronics and automotive sectors.

- Increasing stringency of global ESD/EMC regulations fuels demand.

- Technological advancements leading to smaller, more efficient components.

- Emerging markets present substantial opportunities for expansion.

- Demand for specialized components for high-speed data transmission and high-power applications is rising.

ESD Suppression Component Market Drivers Analysis

The ESD suppression component market is propelled by a confluence of technological advancements, regulatory mandates, and the pervasive expansion of electronic devices across various sectors. The miniaturization trend in electronics necessitates more compact and effective protection, while the increasing complexity and sensitivity of integrated circuits heighten the risk of ESD-induced damage. Global regulatory bodies are also implementing stricter standards for electromagnetic compatibility and electrostatic discharge, compelling manufacturers to integrate robust ESD suppression early in the design phase.

Furthermore, the rapid deployment of 5G networks and the proliferation of Internet of Things (IoT) devices across consumer, industrial, and smart city applications are creating vast new avenues for ESD component demand. These technologies involve numerous interconnected devices and high-speed data transmission, making them particularly vulnerable to transient voltage events. The automotive industry's pivot towards electrification and autonomous driving systems also requires highly reliable ESD protection for sensitive control units, battery management systems, and infotainment units, acting as a significant market driver.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Consumer Electronics and Wearables | +2.5% | Asia Pacific, North America, Europe | 2025-2033 |

| Proliferation of IoT Devices and 5G Infrastructure | +2.0% | Global, particularly APAC and North America | 2025-2033 |

| Increasing Production of Electric Vehicles (EVs) and ADAS | +1.8% | Europe, Asia Pacific (China, Japan, South Korea), North America | 2025-2033 |

| Stringent Regulatory Standards for ESD and EMC | +1.5% | Global | 2025-2033 |

ESD Suppression Component Market Restraints Analysis

Despite robust growth prospects, the ESD suppression component market faces several significant restraints that could temper its expansion. Price sensitivity, particularly in high-volume consumer electronics segments, puts continuous pressure on manufacturers to reduce costs while maintaining performance. This can lead to trade-offs in component quality or material innovation. The inherent complexity of integrating ESD solutions into increasingly miniaturized and high-frequency circuits also poses a challenge, requiring advanced design expertise and extensive testing, which can increase development time and costs.

Furthermore, supply chain vulnerabilities, exacerbated by geopolitical tensions and global events, can lead to disruptions in the availability of raw materials or manufacturing capacity, impacting production and market stability. The rapid pace of technological change within the electronics industry means that ESD suppression solutions must continuously evolve, which can lead to rapid obsolescence of older technologies and a need for constant investment in research and development. Additionally, the availability of alternative protection methods or integrated circuit designs with built-in ESD protection may impact the demand for discrete ESD components in certain applications.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Price Sensitivity and Cost Pressures | -1.2% | Global, particularly emerging markets | 2025-2033 |

| Supply Chain Disruptions and Raw Material Volatility | -0.8% | Global | 2025-2028 |

| Complexity of Integration in High-Density Circuits | -0.5% | Global | 2025-2033 |

ESD Suppression Component Market Opportunities Analysis

The ESD suppression component market is replete with opportunities stemming from evolving technological landscapes and new application frontiers. The growing adoption of Wide Band Gap (WBG) semiconductors like Silicon Carbide (SiC) and Gallium Nitride (GaN) in power electronics for electric vehicles, renewable energy, and industrial power supplies creates a specific demand for ESD components capable of protecting these high-power, high-frequency devices. These semiconductors operate at higher voltages and temperatures, necessitating tailored ESD solutions that can withstand extreme conditions.

Moreover, the expansion into specialized markets such as medical devices, aerospace and defense, and industrial automation presents lucrative opportunities. These sectors demand extremely high reliability and long product lifecycles, driving demand for premium, high-performance ESD solutions. Customization and application-specific integrated ESD protection modules are also emerging as a significant opportunity, allowing manufacturers to offer targeted solutions that are optimally integrated into complex systems, enhancing overall system reliability and performance. Strategic partnerships with semiconductor manufacturers can further open doors for early design-in and collaborative innovation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Wide Band Gap (WBG) Semiconductor Applications | +1.5% | North America, Europe, Asia Pacific | 2025-2033 |

| Emerging Applications in Medical, Aerospace & Defense | +1.0% | North America, Europe | 2025-2033 |

| Development of Integrated and Custom ESD Solutions | +0.8% | Global | 2025-2033 |

ESD Suppression Component Market Challenges Impact Analysis

The ESD suppression component market faces inherent technical challenges driven by the relentless pace of innovation in electronics. Achieving ultra-low capacitance, crucial for high-speed data lines, while simultaneously providing robust protection against high-voltage ESD events, remains a significant engineering hurdle. As data rates in applications like 5G and data centers continue to soar, traditional ESD components can degrade signal integrity, necessitating new designs that are transparent to high-frequency signals. Balancing protection capabilities with minimal signal distortion is a continuous challenge for component manufacturers.

Furthermore, the increasing integration of multiple functionalities into single chips and modules demands highly miniaturized ESD solutions that can fit into extremely constrained spaces without compromising performance or thermal management. Ensuring compatibility across a diverse range of semiconductor technologies and operating environments also adds complexity to design and validation. The threat of counterfeiting, particularly for highly sought-after components, presents a challenge to market integrity and the reputation of legitimate manufacturers, requiring robust intellectual property protection and supply chain vigilance.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving Ultra-Low Capacitance for High-Speed Applications | -0.7% | Global | 2025-2033 |

| Demands for Higher Breakdown Voltage and Current Handling | -0.6% | Global | 2025-2033 |

| Integration Challenges in Miniaturized and Complex Systems | -0.5% | Global | 2025-2033 |

ESD Suppression Component Market - Updated Report Scope

This report provides a comprehensive analysis of the ESD Suppression Component market, offering detailed insights into market dynamics, segmentation, regional trends, and competitive landscape. It covers the historical period from 2019 to 2023, establishes 2024 as the base year, and projects market developments through 2033. The scope includes an in-depth examination of market drivers, restraints, opportunities, and challenges, along with an impact analysis of artificial intelligence on the industry. The report also highlights key market trends and provides granular segmentation to offer a holistic view of the market's structure and potential.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.45 Billion |

| Market Forecast in 2033 | USD 3.01 Billion |

| Growth Rate | 9.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Infineon Technologies AG, Nexperia, Littelfuse Inc., Bourns Inc., TDK Corporation, Murata Manufacturing Co., Ltd., Vishay Intertechnology Inc., STMicroelectronics N.V., ON Semiconductor Corporation, Semtech Corporation, Diodes Incorporated, Taiyo Yuden Co., Ltd., Rohm Co., Ltd., Microchip Technology Inc., Kyocera Corporation, TE Connectivity, Eaton Corporation, Panasonic Corporation, Texas Instruments, Maxim Integrated |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The ESD suppression component market is rigorously segmented to provide a granular understanding of its diverse facets, enabling precise market analysis and strategic planning. This segmentation considers various attributes including the fundamental component type, the wide array of applications where these components are vital, the specific clamping voltage requirements for different circuits, and the physical packaging types preferred by manufacturers. This multi-dimensional approach allows for a detailed examination of market dynamics within each segment, revealing growth pockets and areas of specific demand.

Each segment is influenced by distinct technological needs and market forces. For instance, the demand for TVS diodes often correlates with high-speed data lines and power protection, while varistors find extensive use in industrial and automotive surge protection. Understanding these distinct segment characteristics is critical for identifying specific market opportunities and challenges. The growth in each segment is also influenced by regional manufacturing hubs, regulatory environments, and the dominant end-use industries present in those areas, highlighting the interconnected nature of the market structure.

- By Component Type:

- TVS Diodes (Transient Voltage Suppressor Diodes)

- MLCCs (Multi-Layer Ceramic Capacitors)

- Varistors

- Polymer ESD Suppressors

- Zener Diodes

- Others (e.g., Thyristor Surge Protectors)

- By Application:

- Consumer Electronics (Smartphones, Laptops, Wearables, TVs)

- Automotive (Infotainment, ADAS, Powertrain, Body Electronics)

- Industrial (Automation, Robotics, Power Supplies, LED Lighting)

- Telecommunications (5G Infrastructure, Base Stations, Networking Equipment)

- Computing (Servers, Desktops, Data Centers)

- Medical Devices (Diagnostic Equipment, Implantable Devices)

- Others (Aerospace & Defense, IoT Devices, Smart Home)

- By Clamping Voltage:

- Low Clamping Voltage

- Medium Clamping Voltage

- High Clamping Voltage

- By Package Type:

- Surface Mount Devices (SMD)

- Through-Hole Devices (THD)

Regional Highlights

- Asia Pacific (APAC): Dominates the ESD suppression component market due to its robust electronics manufacturing base, particularly in China, South Korea, Japan, and Taiwan. The region is a global hub for consumer electronics, automotive production, and telecommunications infrastructure development, leading to high demand for ESD components. Rapid industrialization and increasing disposable incomes also fuel the adoption of electronic devices.

- North America: A significant market characterized by high innovation in computing, telecommunications, and automotive sectors. The presence of major technology companies and a strong focus on R&D drives the demand for advanced and specialized ESD suppression components, particularly for high-speed data applications and cutting-edge medical devices.

- Europe: Exhibits strong growth driven by its advanced automotive industry, industrial automation, and stringent regulatory frameworks for electronic product safety and electromagnetic compatibility. Germany, France, and the UK are key contributors, with a focus on high-reliability components for industrial and automotive applications.

- Latin America: An emerging market with growing electronics manufacturing capabilities and increasing adoption of consumer electronics and automotive technologies. Brazil and Mexico are leading countries, attracting investments in manufacturing and assembly, which in turn boosts the demand for ESD components.

- Middle East and Africa (MEA): Shows gradual growth driven by infrastructure development projects, increasing internet penetration, and the expansion of smart city initiatives. Investments in telecommunications and renewable energy are creating new opportunities for ESD component adoption in the region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the ESD Suppression Component Market.- Infineon Technologies AG

- Nexperia

- Littelfuse Inc.

- Bourns Inc.

- TDK Corporation

- Murata Manufacturing Co., Ltd.

- Vishay Intertechnology Inc.

- STMicroelectronics N.V.

- ON Semiconductor Corporation

- Semtech Corporation

- Diodes Incorporated

- Taiyo Yuden Co., Ltd.

- Rohm Co., Ltd.

- Microchip Technology Inc.

- Kyocera Corporation

- TE Connectivity

- Eaton Corporation

- Panasonic Corporation

- Texas Instruments

- Maxim Integrated

Frequently Asked Questions

What is the projected growth rate of the ESD Suppression Component Market?

The ESD Suppression Component Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033, reaching USD 3.01 billion by 2033.

Which factors are primarily driving the ESD Suppression Component Market?

Key drivers include the expanding consumer electronics market, rapid adoption of IoT and 5G technologies, increasing electric vehicle production, and stringent global regulatory standards for ESD and EMC.

How is AI impacting the ESD Suppression Component Market?

AI influences the market by optimizing component design and manufacturing processes, enhancing predictive failure analysis, and creating increased demand for robust ESD protection in AI-powered hardware such as edge computing and data center equipment.

What are the main types of ESD suppression components?

The primary types of ESD suppression components include TVS Diodes, MLCCs, Varistors, Polymer ESD Suppressors, and Zener Diodes, each designed for specific protection needs across various applications.

Which region holds the largest market share for ESD Suppression Components?

Asia Pacific (APAC) currently holds the largest market share due to its dominant position in electronics manufacturing, high volume of consumer electronics production, and significant growth in automotive and telecommunications sectors.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted