ESD Protection Device Market

ESD Protection Device Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704207 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

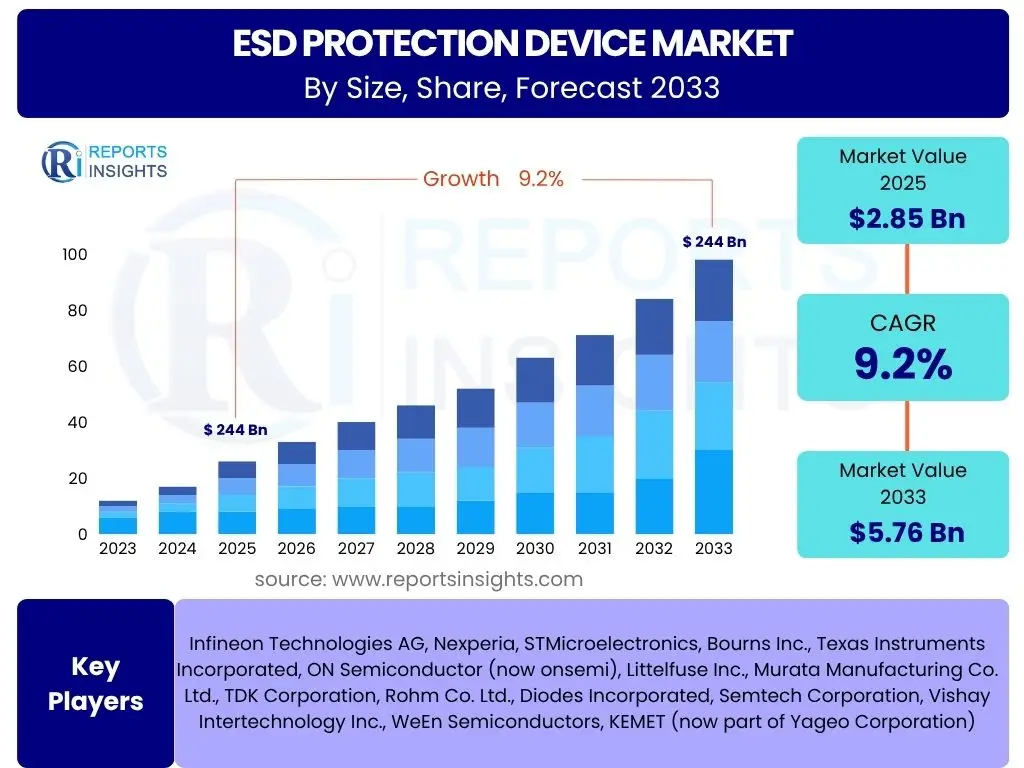

ESD Protection Device Market Size

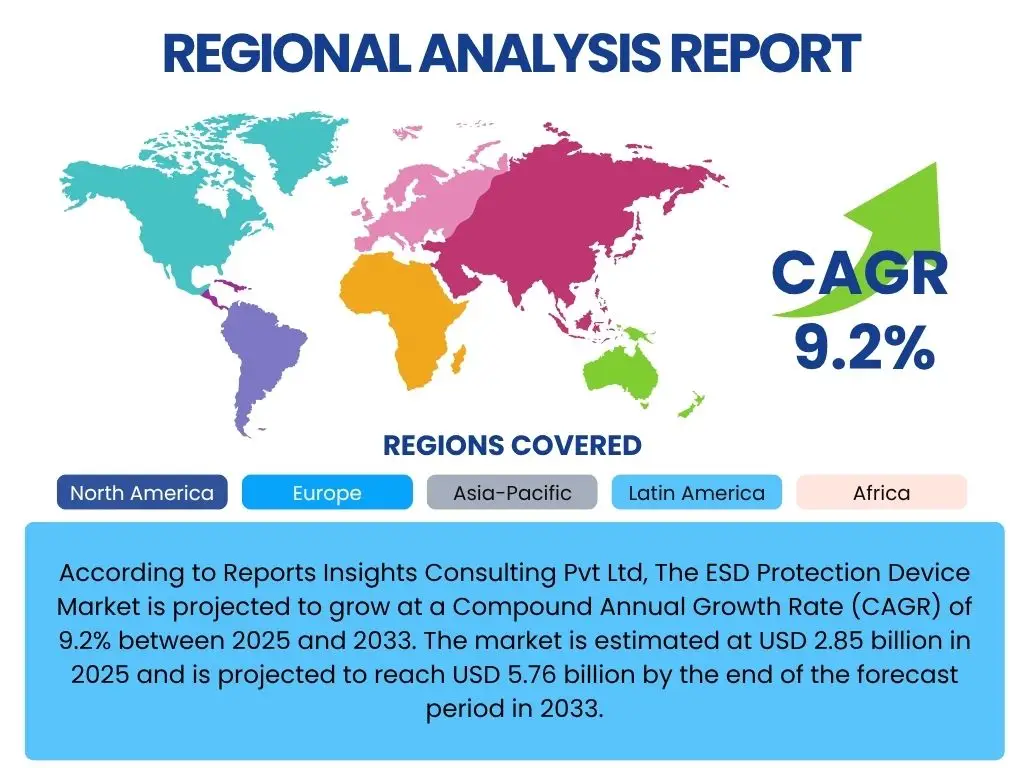

According to Reports Insights Consulting Pvt Ltd, The ESD Protection Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.2% between 2025 and 2033. The market is estimated at USD 2.85 billion in 2025 and is projected to reach USD 5.76 billion by the end of the forecast period in 2033.

Key ESD Protection Device Market Trends & Insights

The ESD Protection Device market is currently experiencing significant transformative trends driven by the rapid evolution of electronics. Key insights indicate a growing emphasis on miniaturization and higher integration of protective solutions, essential for compact and high-performance devices. Furthermore, the increasing adoption of advanced semiconductor technologies, such as FinFET and GAAFET, necessitates more sophisticated ESD solutions that can handle lower voltage tolerances and higher power densities. This shift is particularly evident in segments like 5G infrastructure, artificial intelligence hardware, and advanced automotive systems, where reliability and signal integrity are paramount.

Another prominent trend is the rising demand for robust ESD protection in harsh operating environments, including industrial automation, automotive electronics, and outdoor communication equipment. This leads to innovations in packaging technologies and materials that enhance durability and thermal management. The industry is also witnessing a move towards multi-functional ESD solutions that integrate other circuit protection features, simplifying board design and reducing overall component count. Sustainability and regulatory compliance are also influencing material selection and manufacturing processes, pushing for lead-free and environmentally friendly solutions.

- Miniaturization and integration of ESD components.

- Increasing adoption of advanced semiconductor nodes requiring enhanced protection.

- Growing demand for robust ESD solutions in harsh environments.

- Development of multi-functional and integrated protection devices.

- Emphasis on eco-friendly materials and manufacturing processes.

- Rising importance of ESD in high-frequency and high-speed data transmission applications.

AI Impact Analysis on ESD Protection Device

Artificial intelligence is profoundly influencing the ESD Protection Device market, primarily through two major avenues: the increasing demand for AI-specific hardware and the application of AI in the design and manufacturing of ESD solutions. The proliferation of AI accelerators, edge AI devices, and high-performance computing (HPC) for AI workloads necessitates extremely reliable and highly efficient ESD protection. These AI-driven systems often operate at higher clock speeds, with lower voltage rails, and feature complex chip architectures, making them exceptionally susceptible to electrostatic discharge events. Therefore, there is a burgeoning need for specialized ESD devices that can protect sensitive AI circuitry without compromising performance or introducing signal integrity issues.

Beyond hardware requirements, AI and machine learning (ML) are being leveraged to optimize the design, testing, and fault prediction of ESD protection circuits. AI algorithms can analyze vast datasets from simulations and real-world failure patterns to identify optimal placement, sizing, and design topologies for ESD devices, leading to more effective and compact solutions. Predictive maintenance and anomaly detection, facilitated by AI, can also enhance the reliability of electronic systems, indirectly reducing the impact of ESD failures over the product lifecycle. This dual impact positions AI as both a significant driver for new ESD protection challenges and a powerful tool for developing advanced solutions.

- Increased demand for ESD protection in AI accelerators and edge AI devices.

- Requirement for high-performance ESD solutions for complex AI chip architectures.

- Application of AI/ML in optimizing ESD circuit design and simulation.

- AI-driven fault prediction and reliability enhancement for electronic systems.

- Development of specialized ESD solutions for lower voltage and higher speed AI hardware.

Key Takeaways ESD Protection Device Market Size & Forecast

The ESD Protection Device market is poised for robust growth, driven by the pervasive integration of electronics across all major industries and the continuous advancement of semiconductor technology. The forecast indicates a significant expansion in market size, reflecting the critical role ESD protection plays in ensuring device reliability and longevity. Key insights reveal that while consumer electronics remain a substantial segment, the automotive, industrial, and telecommunications sectors are emerging as primary growth engines due to their stringent reliability requirements and the increasing sophistication of their electronic systems. This growth is underpinned by continuous innovation in materials, design methodologies, and integration techniques, aiming to provide more effective protection in increasingly complex and compact devices.

Furthermore, the market's expansion is not uniform across all regions; Asia Pacific, specifically, is expected to maintain its dominance due to a strong manufacturing base and high consumption of electronic goods. However, North America and Europe are also projected to exhibit healthy growth, fueled by advancements in automotive electronics, industrial IoT, and data center infrastructure. The emphasis on high-speed data transfer and lower power consumption in next-generation devices will continue to drive demand for highly efficient and low-capacitance ESD solutions. The overall trajectory points towards a resilient market that is integral to the advancement and reliability of the global electronics industry.

- Market projected to reach USD 5.76 billion by 2033, growing at 9.2% CAGR.

- Strong growth fueled by miniaturization and complex electronic systems.

- Automotive, industrial, and telecommunications sectors are key growth drivers.

- Asia Pacific retains market leadership due to manufacturing and consumption.

- Innovation in low-capacitance and high-speed ESD solutions is critical.

ESD Protection Device Market Drivers Analysis

The proliferation of electronic devices across various sectors serves as a primary driver for the ESD protection device market. As consumer electronics become more sophisticated and ubiquitous, their increased susceptibility to electrostatic discharge necessitates robust protective measures. Simultaneously, the automotive industry's rapid adoption of advanced electronics for infotainment, ADAS (Advanced Driver-Assistance Systems), and electric vehicle (EV) powertrains introduces new challenges and a heightened demand for resilient ESD solutions capable of operating in harsh environments.

Furthermore, the global expansion of 5G infrastructure and the growing demand for high-speed data transmission in data centers and telecommunication networks are significant contributors. These applications rely on highly sensitive components operating at gigahertz frequencies, where even minor ESD events can cause catastrophic failures or signal integrity degradation. The ongoing trend of miniaturization in semiconductor manufacturing, leading to smaller geometries and lower operating voltages, inherently increases the vulnerability of integrated circuits to ESD, thereby creating an imperative for more effective and integrated protection solutions. Regulatory compliance and industry standards also compel manufacturers to integrate ESD protection, ensuring product reliability and reducing warranty claims.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing adoption of consumer electronics | +2.5% | Global, particularly APAC | Short-term to Long-term |

| Rising electronic content in automotive industry (EVs, ADAS) | +2.0% | North America, Europe, China | Mid-term to Long-term |

| Expansion of 5G infrastructure and data centers | +1.8% | Global, particularly North America, APAC | Mid-term |

| Miniaturization of semiconductor devices | +1.5% | Global | Long-term |

| Stringent regulatory standards and reliability requirements | +1.0% | Global | Ongoing |

ESD Protection Device Market Restraints Analysis

Despite the strong growth drivers, the ESD Protection Device market faces several inherent restraints that can impact its expansion. One significant challenge is the trade-off between ESD protection performance and signal integrity, especially in high-speed data applications. Integrating robust ESD solutions can introduce parasitic capacitance and resistance, which may degrade signal quality, increase insertion loss, and limit bandwidth. Designing devices that offer effective protection without compromising system performance requires sophisticated engineering and often leads to increased design complexity and cost.

Another restraint is the fluctuating cost of raw materials and manufacturing complexities associated with advanced ESD devices. As semiconductor geometries shrink and performance requirements become more stringent, the processes and materials needed to produce effective ESD solutions become more specialized and expensive. This can lead to higher unit costs, which might be a barrier for cost-sensitive applications. Furthermore, the fragmented nature of the market with numerous suppliers and varying product specifications can create challenges for standardization and broad adoption, sometimes leading to over-specification or under-protection in designs due to lack of clarity or consistent industry benchmarks.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Trade-off between ESD performance and signal integrity | -1.2% | Global | Ongoing |

| Increasing design complexity and cost of advanced solutions | -1.0% | Global | Mid-term |

| Fluctuations in raw material prices | -0.8% | Global | Short-term |

| Lack of standardized testing and certification procedures | -0.7% | Global | Long-term |

ESD Protection Device Market Opportunities Analysis

The ESD Protection Device market is ripe with opportunities driven by technological advancements and the emergence of new application areas. The continuous evolution of semiconductor technology, particularly the shift towards advanced process nodes (e.g., 5nm, 3nm), creates a persistent need for innovative and more effective ESD solutions. These smaller geometries are inherently more susceptible to ESD events, opening avenues for high-performance, ultra-low capacitance ESD devices and integrated protection schemes. The development of new materials and packaging technologies, such as through-silicon vias (TSVs) and advanced wafer-level packaging, presents opportunities for more compact and efficient ESD integration within complex chip architectures.

The rapid expansion of electric vehicles (EVs) and autonomous driving systems represents a significant growth avenue. EVs contain a vastly higher number of electronic control units (ECUs) and power electronics compared to conventional vehicles, all requiring robust ESD protection to ensure safety and reliability. Similarly, the proliferation of Internet of Things (IoT) devices, ranging from smart home appliances to industrial sensors, offers a broad and diverse market for miniaturized and cost-effective ESD solutions. Emerging markets in Asia, Latin America, and Africa are also providing untapped potential as their digital infrastructure and consumer electronics adoption rates accelerate. Furthermore, the increasing focus on cyber-physical systems and industrial automation demands resilient ESD solutions for critical infrastructure, creating specialized high-reliability market niches.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Electric Vehicles (EVs) and Autonomous Driving | +1.5% | Global, particularly North America, Europe, APAC | Mid-term to Long-term |

| Proliferation of IoT and Wearable Devices | +1.3% | Global | Short-term to Mid-term |

| Development of advanced semiconductor process nodes (e.g., 5nm, 3nm) | +1.0% | Global | Long-term |

| Expansion in emerging economies for electronic manufacturing | +0.9% | Asia, Latin America, Africa | Mid-term to Long-term |

| Increased demand for industrial automation and smart factory solutions | +0.8% | Europe, North America, China | Mid-term |

ESD Protection Device Market Challenges Impact Analysis

The ESD Protection Device market faces several critical challenges that demand continuous innovation and strategic adaptation. One of the foremost challenges is the ever-decreasing device geometries in semiconductor manufacturing. As transistors shrink to nanometer scales, they become increasingly sensitive to even minor electrostatic discharges, requiring more precise and efficient protection mechanisms. This necessitates a delicate balance between providing robust protection and minimizing the impact on signal integrity and power consumption, which is particularly difficult in high-speed and low-power applications.

Another significant challenge stems from the dynamic nature of ESD events and the complexity of testing and validating ESD protection in integrated circuits. ESD events can vary widely in voltage, current, and duration, making it challenging to design a single, universal protection solution. Furthermore, the integration of multiple functionalities onto a single chip increases the complexity of ESD pathfinding and introduces new failure modes. The global supply chain volatility, including semiconductor shortages and geopolitical tensions, also poses a challenge by potentially disrupting the availability of critical materials and manufacturing capacity for ESD devices, impacting production schedules and costs across the electronics industry. Ensuring compliance with evolving international standards for ESD protection also remains a continuous and demanding task for manufacturers.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ever-decreasing device geometries and heightened sensitivity | -1.5% | Global | Ongoing |

| Balancing robust protection with minimal signal degradation | -1.3% | Global | Ongoing |

| Complexities in testing and validating ESD protection for integrated circuits | -1.0% | Global | Mid-term |

| Supply chain disruptions and geopolitical factors | -0.8% | Global | Short-term to Mid-term |

| Meeting evolving industry standards and regulatory requirements | -0.7% | Global | Ongoing |

ESD Protection Device Market - Updated Report Scope

This market research report provides a detailed and extensive analysis of the global ESD Protection Device market. It encompasses a comprehensive examination of market dynamics, including key drivers, restraints, opportunities, and challenges influencing industry growth. The report segmentations are thoroughly investigated across various dimensions such as product type, application, end-use industry, and regional landscape, offering a granular view of market trends and revenue streams. Special emphasis is placed on the impact of emerging technologies like Artificial Intelligence and the rapid expansion of interconnected devices, providing forward-looking insights crucial for strategic decision-making. The report also includes an updated competitive landscape, profiling key market players and their strategic initiatives.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.85 Billion |

| Market Forecast in 2033 | USD 5.76 Billion |

| Growth Rate | 9.2% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Infineon Technologies AG, Nexperia, STMicroelectronics, Bourns Inc., Texas Instruments Incorporated, ON Semiconductor (now onsemi), Littelfuse Inc., Murata Manufacturing Co. Ltd., TDK Corporation, Rohm Co. Ltd., Diodes Incorporated, Semtech Corporation, Vishay Intertechnology Inc., WeEn Semiconductors, KEMET (now part of Yageo Corporation) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The ESD Protection Device market is extensively segmented to provide a detailed understanding of its diverse components and their respective growth trajectories. These segmentations are critical for identifying specific market niches, understanding user preferences, and targeting strategic investments. The primary segmentation by type includes various technologies such as Transient Voltage Suppressor (TVS) Diodes, Zener Diodes, Multi-Layer Varistors (MLVs), and specialized ESD Suppressors, each offering unique characteristics in terms of clamping voltage, capacitance, and power handling capabilities, making them suitable for different applications.

Further segmentation by application highlights the key industries driving demand, including the pervasive consumer electronics sector, the rapidly expanding automotive industry with its stringent reliability requirements, and the foundational telecommunications and computing sectors that underpin modern digital infrastructure. End-use industry segmentation provides even finer granularity, distinguishing between specific product categories like mobile devices, wearables, data center servers, and medical diagnostic equipment, each with distinct ESD protection needs. These detailed segmentations reveal the complex interplay of technological evolution and market demand across the global landscape.

- By Type: TVS Diodes, Zener Diodes, MLVs, ESD Suppressors, Thyristor Surge Suppressors, Others.

- By Application: Consumer Electronics, Automotive, Industrial, Telecommunications, Computing & Data Centers, Medical Devices, Aerospace & Defense, Others.

- By End-Use Industry: Mobile Devices, Wearables, Laptops & PCs, Servers & Data Storage, Networking Equipment, Industrial Control Systems, Infotainment Systems, ADAS, Medical Imaging, Diagnostic Equipment, etc.

- By Voltage Rating: Low Voltage, Medium Voltage, High Voltage.

- By Packaging Type: Surface Mount Devices (SMD), Through-Hole Devices (THD), Wafer Level Chip Scale Packaging (WLCSP).

Regional Highlights

- Asia Pacific (APAC): Dominates the market due to robust manufacturing capabilities in countries like China, South Korea, Japan, and Taiwan, coupled with high consumer electronics production and consumption. The region is a hub for semiconductor fabrication and assembly, driving significant demand for ESD protection.

- North America: Exhibits strong growth driven by technological innovation, the presence of major automotive and IT companies, and increasing investments in data centers and 5G infrastructure. High adoption of advanced technologies and stringent regulatory standards contribute to market expansion.

- Europe: A significant market influenced by its thriving automotive industry, industrial automation, and strong focus on R&D in semiconductor technologies. Germany, France, and the UK are key contributors to demand for high-reliability ESD solutions.

- Latin America: An emerging market with growing electronic manufacturing activities and increasing adoption of consumer electronics and telecommunication infrastructure. Brazil and Mexico are leading the regional growth.

- Middle East and Africa (MEA): Shows gradual growth, primarily driven by increasing investments in IT and telecommunications infrastructure, smart city initiatives, and the gradual expansion of consumer electronics markets.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the ESD Protection Device Market.- Infineon Technologies AG

- Nexperia

- STMicroelectronics

- Bourns Inc.

- Texas Instruments Incorporated

- ON Semiconductor (onsemi)

- Littelfuse Inc.

- Murata Manufacturing Co. Ltd.

- TDK Corporation

- Rohm Co. Ltd.

- Diodes Incorporated

- Semtech Corporation

- Vishay Intertechnology Inc.

- WeEn Semiconductors

- KEMET (now part of Yageo Corporation)

Frequently Asked Questions

What is the projected growth rate for the ESD Protection Device Market?

The ESD Protection Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.2% between 2025 and 2033, reaching an estimated USD 5.76 billion by 2033.

Which factors are primarily driving the growth of the ESD Protection Device Market?

Key drivers include the increasing adoption of consumer electronics, the rising electronic content in the automotive industry (e.g., EVs, ADAS), the expansion of 5G infrastructure and data centers, and the ongoing miniaturization of semiconductor devices.

How is Artificial Intelligence impacting the ESD Protection Device market?

AI impacts the market by increasing demand for robust ESD protection in AI-specific hardware (accelerators, edge AI) and by enabling AI/ML applications to optimize the design, testing, and fault prediction of ESD protection circuits themselves.

Which regions are key contributors to the ESD Protection Device market revenue?

Asia Pacific is the leading region due to extensive manufacturing and high consumption, while North America and Europe also contribute significantly due to technological advancements and automotive/industrial electronics growth.

What are the main types of ESD Protection Devices available in the market?

The main types include TVS Diodes, Zener Diodes, Multi-Layer Varistors (MLVs), ESD Suppressors, and Thyristor Surge Suppressors, each tailored for different protection requirements.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted