Eyesight Test Device Market

Eyesight Test Device Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704283 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

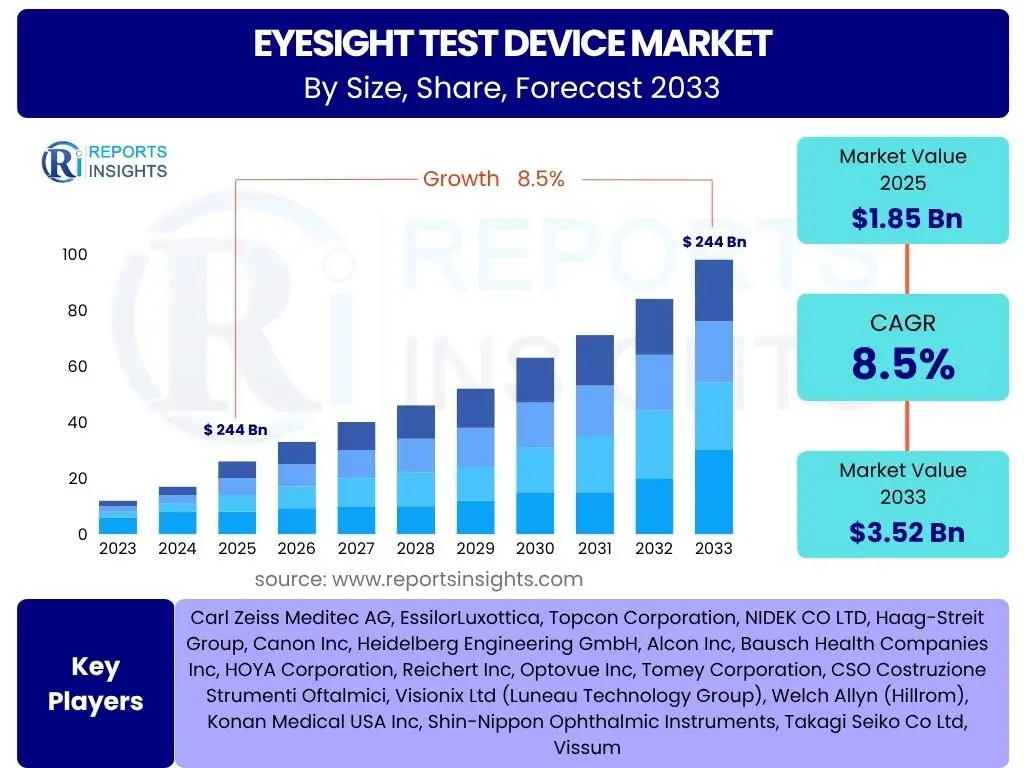

Eyesight Test Device Market Size

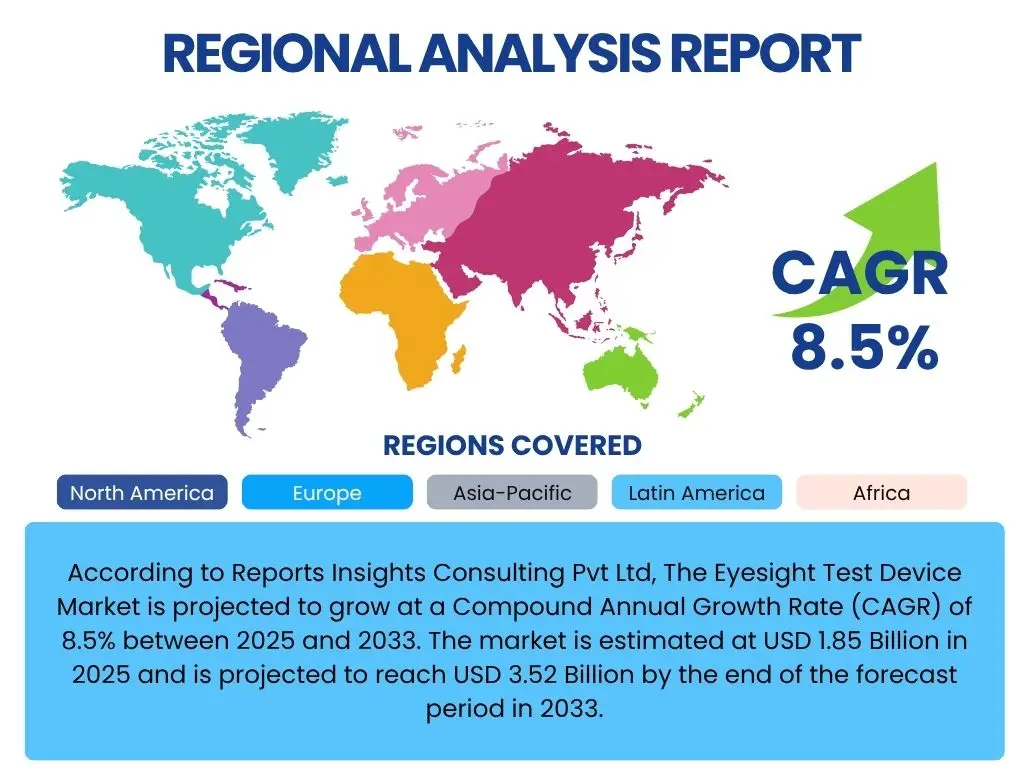

According to Reports Insights Consulting Pvt Ltd, The Eyesight Test Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 3.52 Billion by the end of the forecast period in 2033.

Key Eyesight Test Device Market Trends & Insights

The eyesight test device market is experiencing significant shifts driven by an increasing global burden of ocular diseases, advancements in diagnostic technologies, and a growing emphasis on preventive eye care. User inquiries frequently highlight the shift towards more portable, automated, and AI-integrated devices, alongside a rising demand for home-based or remote diagnostic solutions. There is also a notable trend towards early detection and personalized treatment strategies, fueled by greater awareness regarding the long-term impacts of unaddressed vision impairments. The integration of telemedicine and digital health platforms is further reshaping how eye care services are delivered and accessed, emphasizing efficiency and convenience.

Another prominent trend involves the miniaturization and enhanced user-friendliness of diagnostic tools, making them accessible beyond traditional clinical settings. Users are keen to understand how these innovations can improve diagnostic accuracy, reduce testing time, and lower overall healthcare costs. The market is also seeing an increased focus on non-invasive diagnostic methods and devices that cater to a broader age demographic, from pediatric patients requiring specialized screening to an aging population prone to age-related macular degeneration and glaucoma. Furthermore, sustainability and cost-effectiveness are emerging as important considerations, driving demand for durable and efficient equipment that offers long-term value.

- Growing adoption of portable and handheld diagnostic devices.

- Increasing integration of tele-ophthalmology and remote diagnostic platforms.

- Rising demand for automated and AI-powered diagnostic solutions.

- Emphasis on early detection and preventive eye care programs.

- Development of non-invasive and patient-friendly testing methods.

- Personalization of eye care diagnostics based on individual patient needs.

- Expansion of optical retail chains offering comprehensive eye screening services.

AI Impact Analysis on Eyesight Test Device

User queries regarding the impact of Artificial Intelligence (AI) on eyesight test devices frequently center on its potential to enhance diagnostic accuracy, streamline workflows, and enable earlier disease detection. AI algorithms are increasingly being employed to analyze complex retinal images, optical coherence tomography (OCT) scans, and visual field data, assisting ophthalmologists in identifying subtle patterns indicative of diseases such as diabetic retinopathy, glaucoma, and age-related macular degeneration. This capability not only reduces the burden on human practitioners but also standardizes diagnostic interpretations, leading to more consistent and reliable outcomes. Concerns often revolve around data privacy, regulatory approvals for AI-driven diagnostics, and the potential for AI to displace human expertise, though the consensus leans towards AI as a supportive tool rather than a replacement.

The integration of AI also facilitates predictive analytics, allowing healthcare providers to forecast disease progression and personalize treatment plans more effectively. Users are particularly interested in how AI can optimize screening programs, especially in underserved areas, by enabling automated pre-screening and triaging of patients who require immediate attention. Furthermore, AI is crucial in developing smart diagnostic devices that can adapt to patient responses, provide real-time feedback, and even automate parts of the examination process. This intelligent automation contributes to higher throughput in clinics and offers the potential for widespread, accessible eye health monitoring, transforming the landscape of preventive and proactive eye care management.

- Enhanced diagnostic accuracy and early disease detection through image analysis.

- Automation of routine screening procedures and data interpretation.

- Predictive analytics for disease progression and personalized treatment.

- Integration into tele-ophthalmology for remote diagnosis and monitoring.

- Development of smart, adaptive eyesight testing equipment.

- Reduction in diagnostic time and improved clinical workflow efficiency.

- Potential for wider access to specialized eye care in remote regions.

Key Takeaways Eyesight Test Device Market Size & Forecast

The eyesight test device market is poised for robust growth, primarily driven by the escalating global prevalence of chronic eye conditions and an aging population requiring frequent vision assessments. User questions frequently underscore the significance of technological innovation, particularly in areas like portability, automation, and AI integration, as key accelerators for market expansion. The forecast indicates a substantial increase in market valuation, reflecting a sustained demand for advanced diagnostic solutions that can cater to both clinical and non-clinical settings. This growth trajectory is also influenced by increasing healthcare expenditure and a global shift towards preventive healthcare paradigms, where early diagnosis plays a critical role in managing ocular health.

Furthermore, the market's future is heavily reliant on research and development efforts aimed at creating more affordable, accurate, and user-friendly devices, making eye care accessible to a broader demographic. Key takeaways also highlight the importance of emerging markets, where improving healthcare infrastructure and rising disposable incomes are creating new opportunities for market penetration. The competitive landscape is expected to intensify, with established players focusing on product diversification and strategic collaborations, while new entrants aim to disrupt with innovative technologies. Overall, the market is characterized by dynamic growth, propelled by medical necessity, technological advancements, and evolving patient care models.

- Significant market growth projected, reaching USD 3.52 Billion by 2033.

- Technological advancements, including AI and portability, are primary growth catalysts.

- Increasing prevalence of ocular diseases drives continuous demand.

- Emphasis on preventive care and early diagnosis boosts market expansion.

- Emerging markets offer substantial untapped growth potential.

Eyesight Test Device Market Drivers Analysis

The eyesight test device market is significantly propelled by several synergistic factors. A primary driver is the rising global prevalence of chronic eye diseases such as myopia, glaucoma, cataracts, and diabetic retinopathy, exacerbated by an aging population that is more susceptible to these conditions. This demographic shift necessitates more frequent and accurate diagnostic testing. Additionally, increasing awareness about the importance of early detection and regular eye check-ups, fueled by public health campaigns and improved access to information, is driving consumer demand for sophisticated diagnostic tools. Technological advancements, including the development of portable, automated, and artificial intelligence-integrated devices, are further expanding the market by offering enhanced accuracy, efficiency, and accessibility in diverse healthcare settings.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Prevalence of Ocular Diseases | +2.5% | Global (Asia Pacific, North America) | Short to Long Term |

| Aging Global Population | +1.8% | Europe, North America, Japan | Long Term |

| Technological Advancements in Diagnostics | +2.2% | North America, Europe, China | Short to Mid Term |

| Growing Awareness and Preventive Care Initiatives | +1.0% | Global (Developing Economies) | Mid to Long Term |

Eyesight Test Device Market Restraints Analysis

Despite robust growth drivers, the eyesight test device market faces certain restraints that could impede its full potential. The high cost associated with advanced diagnostic equipment, such as Optical Coherence Tomography (OCT) systems and automated refractors, presents a significant barrier to adoption, particularly in developing economies or smaller healthcare facilities with limited budgets. Additionally, stringent regulatory approval processes for new devices, especially those incorporating novel technologies like AI, can delay market entry and increase R&D costs. Furthermore, the lack of skilled ophthalmologists and trained technicians in many regions, especially rural and underserved areas, limits the effective utilization and widespread deployment of these sophisticated devices, impacting market penetration and growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Advanced Diagnostic Devices | -1.5% | Global (Developing Economies, Small Clinics) | Short to Mid Term |

| Stringent Regulatory Approval Processes | -0.8% | North America, Europe | Short Term |

| Lack of Skilled Professionals | -1.0% | Asia Pacific, Africa, Latin America | Mid to Long Term |

| Limited Reimbursement Policies | -0.5% | Varying by Country | Short to Mid Term |

Eyesight Test Device Market Opportunities Analysis

The eyesight test device market is rich with opportunities, particularly in expanding into emerging economies where healthcare infrastructure is improving and there is a large, untapped patient pool. The increasing adoption of tele-ophthalmology and mobile health platforms presents a significant avenue for growth, enabling remote diagnostics and broader access to eye care, especially in rural areas. Furthermore, the continuous advancements in AI and machine learning offer substantial opportunities for developing more accurate, efficient, and automated diagnostic solutions, reducing human error and improving patient outcomes. The growing demand for personalized medicine and patient-centric care also creates niches for devices that can provide tailored diagnostic insights.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion in Emerging Markets | +1.8% | Asia Pacific, Latin America, Africa | Mid to Long Term |

| Integration of Tele-ophthalmology | +1.5% | Global | Short to Mid Term |

| Advancements in AI and Machine Learning | +2.0% | Global (Developed Economies) | Short to Mid Term |

| Focus on Preventive and Home-based Care | +1.2% | North America, Europe | Mid to Long Term |

Eyesight Test Device Market Challenges Impact Analysis

The eyesight test device market faces several challenges that require strategic navigation. Data security and privacy concerns, particularly with the increasing reliance on digital platforms and AI for patient data processing, pose a significant hurdle, demanding robust cybersecurity measures and compliance with stringent regulations like GDPR and HIPAA. The lack of standardization in diagnostic protocols and device interoperability across different manufacturers and regions can hinder seamless data exchange and integrated care, creating inefficiencies. Moreover, intense competition from low-cost alternatives, especially from local manufacturers in cost-sensitive markets, pressures established players to innovate while maintaining competitive pricing. Lastly, rapid technological obsolescence necessitates continuous investment in R&D, which can be challenging for smaller companies, impacting their market sustainability and competitive edge.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Data Security and Privacy Concerns | -0.9% | Global (Europe, North America) | Short to Mid Term |

| Lack of Standardization and Interoperability | -0.7% | Global | Mid Term |

| Intense Competition from Low-Cost Alternatives | -1.2% | Asia Pacific, Latin America | Short to Mid Term |

| Rapid Technological Obsolescence | -0.6% | Global | Short Term |

Eyesight Test Device Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Eyesight Test Device Market, covering historical performance from 2019 to 2023, with detailed market estimations for 2025 and projections up to 2033. The report meticulously examines market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. It includes a thorough competitive landscape analysis, profiling leading companies, and highlights emerging trends such as the integration of AI, tele-ophthalmology, and the increasing demand for portable diagnostic solutions. The objective is to offer strategic insights for stakeholders to navigate market complexities and capitalize on future growth avenues, ensuring informed decision-making in a rapidly evolving healthcare sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 3.52 Billion |

| Growth Rate | 8.5% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Carl Zeiss Meditec AG, EssilorLuxottica, Topcon Corporation, NIDEK CO LTD, Haag-Streit Group, Canon Inc, Heidelberg Engineering GmbH, Alcon Inc, Bausch Health Companies Inc, HOYA Corporation, Reichert Inc, Optovue Inc, Tomey Corporation, CSO Costruzione Strumenti Oftalmici, Visionix Ltd (Luneau Technology Group), Welch Allyn (Hillrom), Konan Medical USA Inc, Shin-Nippon Ophthalmic Instruments, Takagi Seiko Co Ltd, Vissum |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Eyesight Test Device Market is segmented comprehensively to provide a granular understanding of its diverse components and their contributions to overall market dynamics. This segmentation facilitates detailed analysis by product type, application, and end-user, enabling stakeholders to identify specific growth areas and market opportunities. Each segment addresses distinct needs within the ophthalmology sector, reflecting the varied requirements of patients and healthcare providers globally. The breakdown by product type focuses on the technological innovations driving device development, while application segments highlight the increasing demand for specialized diagnostic capabilities for various eye conditions. End-user segmentation illustrates the different channels through which these devices are adopted, from large hospital networks to local optical stores, indicating diverse market penetration strategies.

The product type segment includes traditional diagnostic tools like refractors and tonometers, alongside advanced imaging systems such as OCT and fundus cameras, which are crucial for detecting complex ocular pathologies. The application segment covers a broad spectrum of diagnostic needs, from routine eye examinations to specialized screenings for prevalent diseases like glaucoma and diabetic retinopathy, underscoring the market's role in addressing major public health challenges. The end-user segment reveals the primary consumers of these devices, including hospitals and specialized ophthalmic clinics, which represent major revenue streams due to their high patient volume and advanced infrastructure. Understanding these segmentations is critical for market players to tailor their product offerings, marketing strategies, and distribution networks effectively.

- By Product Type:

- Refractors (Auto Refractors, Phoropters, Manual Refractors)

- Tonometers (Applanation Tonometers, Non-Contact Tonometers, Rebound Tonometers)

- Fundus Cameras (Non-Mydriatic, Mydriatic, Hybrid)

- Optical Coherence Tomography (OCT)

- Perimeters/Visual Field Analyzers

- Slit Lamps

- Ophthalmoscopes (Direct Ophthalmoscopes, Indirect Ophthalmoscopes)

- Retinoscopes

- Lensmeters

- Pachymeters

- Other Diagnostic Devices

- By Application:

- General Eye Examination

- Glaucoma Diagnosis

- Diabetic Retinopathy Detection

- Macular Degeneration Detection

- Cataract Detection

- Pediatric Eye Screening

- Other Ocular Disease Diagnosis

- By End-User:

- Hospitals

- Ophthalmic Clinics

- Optical Stores and Retail Clinics

- Research Institutes

- Academic Institutions

- Ambulatory Surgical Centers

- Others

Regional Highlights

- North America: Dominates the market due to advanced healthcare infrastructure, high adoption of technologically sophisticated devices, strong presence of key market players, and high prevalence of age-related eye conditions. Investments in R&D and favorable reimbursement policies also contribute to its leading position.

- Europe: Exhibits significant market share, driven by an aging population, increasing awareness about eye health, and robust healthcare expenditure. Countries like Germany, the UK, and France are key contributors due to their strong research base and well-established medical device industry.

- Asia Pacific (APAC): Expected to witness the highest growth rate during the forecast period. This growth is attributed to the large population base, increasing prevalence of eye diseases (especially myopia in East Asia), improving healthcare infrastructure, rising disposable incomes, and growing medical tourism. Government initiatives to promote eye care also play a crucial role.

- Latin America: Demonstrates steady growth, supported by expanding healthcare access, increasing government investments in healthcare, and a rising middle class. Brazil and Mexico are emerging as significant markets within this region.

- Middle East and Africa (MEA): Shows promising growth potential due to improving healthcare facilities, increasing awareness about eye health, and government initiatives aimed at modernizing healthcare systems. However, market growth in some parts of this region may be constrained by limited healthcare spending and infrastructure.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Eyesight Test Device Market.- Carl Zeiss Meditec AG

- EssilorLuxottica

- Topcon Corporation

- NIDEK CO LTD

- Haag-Streit Group

- Canon Inc

- Heidelberg Engineering GmbH

- Alcon Inc

- Bausch Health Companies Inc

- HOYA Corporation

- Reichert Inc

- Optovue Inc

- Tomey Corporation

- CSO Costruzione Strumenti Oftalmici

- Visionix Ltd (Luneau Technology Group)

- Welch Allyn (Hillrom)

- Konan Medical USA Inc

- Shin-Nippon Ophthalmic Instruments

- Takagi Seiko Co Ltd

- Vissum

Frequently Asked Questions

What is the projected growth rate for the Eyesight Test Device Market?

The Eyesight Test Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033, indicating a robust expansion driven by increasing global eye care needs.

How large is the Eyesight Test Device Market expected to be by 2033?

The Eyesight Test Device Market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 3.52 Billion by the end of the forecast period in 2033, demonstrating significant market value appreciation.

What are the key trends influencing the Eyesight Test Device Market?

Key trends include the growing adoption of portable and handheld diagnostic devices, increasing integration of tele-ophthalmology, rising demand for automated and AI-powered solutions, and a strong emphasis on early detection and preventive eye care.

What is the impact of AI on eyesight test devices?

AI significantly enhances diagnostic accuracy, automates routine screening, enables predictive analytics for disease progression, and facilitates remote diagnosis through integration with tele-ophthalmology platforms, ultimately improving efficiency and accessibility of eye care.

Which regions are key contributors to the Eyesight Test Device Market?

North America currently leads the market due to advanced healthcare infrastructure, while Asia Pacific is expected to exhibit the highest growth rate driven by a large population base and improving healthcare access. Europe also holds a significant share due to an aging population and robust healthcare spending.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted