Flame Retardant Resin Market

Flame Retardant Resin Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707863 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

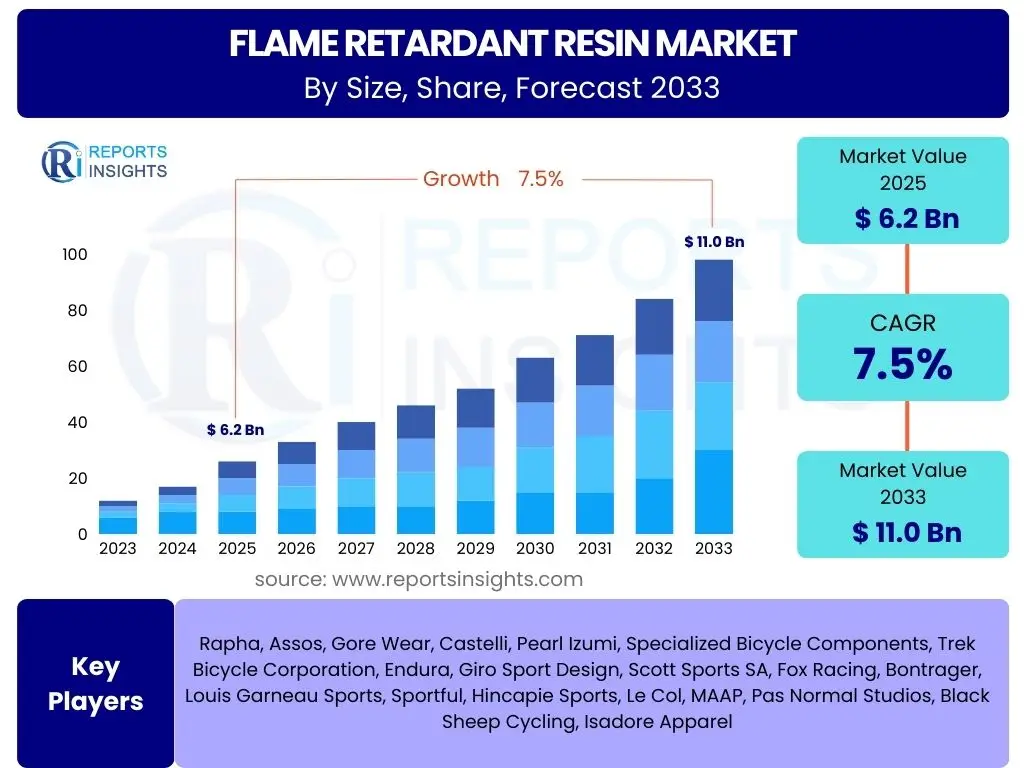

Flame Retardant Resin Market Size

According to Reports Insights Consulting Pvt Ltd, The Flame Retardant Resin Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2025 and 2033. The market is estimated at USD 6.2 Billion in 2025 and is projected to reach USD 11.0 Billion by the end of the forecast period in 2033.

Key Flame Retardant Resin Market Trends & Insights

The Flame Retardant Resin market is witnessing significant transformation driven by evolving regulatory landscapes and a heightened focus on safety and sustainability across various industries. A prominent trend is the accelerating shift towards halogen-free flame retardant solutions, driven by environmental concerns and increasingly stringent global regulations. This paradigm shift is pushing manufacturers to innovate and invest in the development of phosphorus-based, nitrogen-based, and inorganic flame retardant compounds that offer comparable performance without the environmental drawbacks of halogenated alternatives.

Another critical insight is the growing demand from high-growth sectors such as electric vehicles, 5G infrastructure, and advanced electronics, where compact, high-performance materials with superior fire safety properties are indispensable. Miniaturization in electronics and the need for enhanced thermal stability in battery components for EVs are creating specific design challenges and driving the adoption of specialized flame retardant resins. Furthermore, the market is seeing an increased interest in multi-functional resins that not only offer fire resistance but also possess other desirable properties like improved mechanical strength, UV resistance, and chemical inertness, enabling broader applications and greater material efficiency.

- Shift towards halogen-free flame retardants driven by environmental regulations.

- Increasing demand from electric vehicles (EVs), 5G technology, and high-performance electronics.

- Development of bio-based and sustainable flame retardant solutions.

- Growth in intumescent flame retardant systems for enhanced char formation.

- Emphasis on multi-functional resins offering combined properties like fire resistance and mechanical strength.

- Adoption of smart manufacturing and automation in resin production.

AI Impact Analysis on Flame Retardant Resin

Artificial intelligence (AI) is poised to revolutionize the Flame Retardant Resin market by enhancing efficiency, accelerating innovation, and optimizing product development cycles. Users are particularly interested in how AI can streamline research and development (R&D) efforts for new flame retardant formulations. AI and machine learning algorithms can analyze vast datasets of material properties, chemical structures, and performance characteristics to predict the efficacy of novel compounds, significantly reducing the time and cost associated with traditional experimental testing. This capability allows researchers to rapidly identify promising candidates for halogen-free or high-performance applications, addressing market demands for safer and more effective solutions more quickly.

Beyond R&D, AI’s impact extends to optimizing manufacturing processes and supply chain management within the flame retardant resin industry. Predictive analytics, powered by AI, can forecast demand fluctuations, optimize inventory levels, and enhance production scheduling, thereby minimizing waste and improving operational efficiency. Furthermore, AI-driven quality control systems can monitor production lines in real-time, detecting anomalies and ensuring consistent product quality, which is crucial for high-stakes applications requiring precise fire safety standards. The integration of AI tools is expected to lead to more cost-effective production, faster market entry for new products, and a more resilient supply chain, directly benefiting both manufacturers and end-users.

- Accelerated R&D through AI-driven material discovery and property prediction.

- Optimized manufacturing processes via predictive analytics and process control.

- Enhanced quality assurance and consistency in resin production using AI monitoring.

- Improved supply chain efficiency and demand forecasting.

- Development of smart flame retardant materials with self-healing or adaptive properties.

- Personalized material solutions based on specific application requirements through AI modeling.

Key Takeaways Flame Retardant Resin Market Size & Forecast

The Flame Retardant Resin market is on a robust growth trajectory, primarily fueled by the unwavering global commitment to enhanced fire safety across diverse sectors. Users frequently inquire about the primary factors underpinning this growth and the most impactful segments. The forecast indicates sustained expansion, driven by stringent regulatory frameworks mandating fire-resistant materials in construction, electronics, and transportation. This regulatory push, combined with rapid urbanization and industrialization in emerging economies, creates a fertile ground for market expansion, particularly for advanced and environmentally compliant resin formulations.

A crucial takeaway from the market forecast is the accelerating shift towards non-halogenated flame retardant solutions. While halogenated options still hold a significant share, the market's future growth is heavily skewed towards sustainable alternatives, presenting both opportunities and challenges for manufacturers. Furthermore, the electrical & electronics and building & construction sectors are expected to remain the largest consumers, with increasing demand for high-performance resins capable of meeting stringent safety standards in modern infrastructure and consumer goods. The market's resilience is also attributed to continuous innovation, with ongoing research into novel chemistries and synergistic systems that offer improved fire performance with minimal impact on material properties.

- Significant market growth anticipated, driven by global fire safety regulations.

- Strong demand from key end-use industries like electrical & electronics, and building & construction.

- Dominant trend towards non-halogenated and sustainable flame retardant solutions.

- Continuous innovation in resin chemistries and synergistic flame retardant systems.

- Asia Pacific is projected to be the fastest-growing region due to industrial expansion and infrastructure development.

- Market evolution towards multi-functional flame retardant resins with enhanced performance attributes.

Flame Retardant Resin Market Drivers Analysis

The global Flame Retardant Resin market is significantly propelled by the increasing stringency of fire safety regulations across various industries and geographies. Governments and regulatory bodies worldwide are consistently updating and implementing stricter codes for fire performance in materials used in construction, automotive, electrical & electronics, and aerospace sectors. These mandates compel manufacturers to integrate flame retardant resins into their products to ensure compliance and enhance public safety. The liability associated with fire incidents also drives companies to adopt superior flame retardant solutions, thereby stimulating market demand.

Another major driver is the rapid growth and expansion of key end-use industries. The booming construction sector, especially in developing economies, along with the escalating production of electronic devices and the increasing complexity of automotive components (particularly with the rise of electric vehicles and their battery safety requirements), all necessitate high volumes of flame retardant resins. Furthermore, the persistent demand for lightweight materials with enhanced performance characteristics in sectors like aerospace and transportation, without compromising on fire safety, further fuels the innovation and adoption of advanced flame retardant resin technologies. This synergistic demand from multiple sectors ensures a robust and sustained growth trajectory for the market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stricter Fire Safety Regulations | +2.0% | Global, particularly Europe, North America, China | Short to Long-term |

| Growth in Electrical & Electronics Sector | +1.8% | Asia Pacific, North America, Europe | Medium to Long-term |

| Rising Demand from Construction Industry | +1.5% | Asia Pacific, Middle East, Africa | Medium to Long-term |

| Increasing Adoption in Automotive & Transportation (especially EVs) | +1.2% | Global, particularly Europe, China, North America | Medium to Long-term |

| Technological Advancements in Flame Retardant Materials | +1.0% | Global | Long-term |

Flame Retardant Resin Market Restraints Analysis

Despite significant growth drivers, the Flame Retardant Resin market faces notable restraints, primarily concerning environmental and health impacts of certain chemistries. Historically, halogenated flame retardants have been highly effective but are increasingly scrutinized due to concerns about their persistence in the environment, potential bioaccumulation, and the release of toxic fumes during combustion. This scrutiny leads to regulatory restrictions and consumer preference shifts, compelling manufacturers to invest heavily in non-halogenated alternatives, which can sometimes be more expensive or offer different performance profiles, thereby slowing market adoption in some segments.

Another key restraint is the complexity associated with processing flame retardant resins and their potential impact on the overall material properties. Integrating flame retardant additives into polymers can sometimes compromise the mechanical strength, thermal stability, or aesthetic qualities of the final product. Achieving an optimal balance between fire resistance and other desired material properties often requires extensive R&D and specialized processing techniques, which can increase production costs and limit the widespread application of certain flame retardant systems. Furthermore, the fluctuating prices of raw materials, particularly those derived from petrochemicals, can also exert pressure on manufacturers, impacting profit margins and overall market stability.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Environmental and Health Concerns of Halogenated FRs | -1.5% | Global, particularly Europe, North America | Short to Medium-term |

| High Cost of Non-Halogenated Alternatives | -1.0% | Global | Medium to Long-term |

| Processing Difficulties and Impact on Material Properties | -0.8% | Global | Medium-term |

| Volatile Raw Material Prices | -0.5% | Global | Short-term |

| Stringent Regulatory Approval Processes | -0.7% | Global | Medium to Long-term |

Flame Retardant Resin Market Opportunities Analysis

Significant opportunities in the Flame Retardant Resin market stem from the burgeoning demand for sustainable and environmentally friendly solutions. The increasing regulatory pressure and consumer preference for "green" products are creating a fertile ground for the development and adoption of bio-based and recyclable flame retardants. Manufacturers who can successfully innovate in this space, offering solutions with reduced environmental footprints without compromising on fire safety performance, are poised to capture a substantial share of the market. This includes the exploration of natural polymers and naturally derived flame retardant additives, as well as the development of circular economy approaches for flame retardant materials.

Emerging economies, particularly in Asia Pacific and Latin America, present vast untapped market potential. Rapid industrialization, urbanization, and significant infrastructure development in these regions are driving a substantial increase in demand for fire-safe materials in construction, electronics, and automotive industries. As these regions adopt and enforce more stringent fire safety standards, the demand for advanced flame retardant resins will surge. Furthermore, the continuous advancements in material science, including the development of synergistic flame retardant systems and nanotechnology-enabled solutions, offer opportunities to create resins with enhanced fire performance, lighter weight, and improved mechanical properties, catering to specialized and high-value applications across various sectors.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Bio-based and Sustainable FRs | +1.8% | Global | Medium to Long-term |

| Growth in Emerging Economies (e.g., Asia Pacific) | +1.5% | Asia Pacific, Latin America, MEA | Medium to Long-term |

| Increasing Demand for Smart & Advanced Materials | +1.2% | Global | Long-term |

| Synergistic Flame Retardant Systems | +1.0% | Global | Medium to Long-term |

| Application in Electric Vehicle Battery Components | +0.9% | Global | Medium to Long-term |

Flame Retardant Resin Market Challenges Impact Analysis

The Flame Retardant Resin market faces substantial challenges, primarily stemming from the complex and fragmented global regulatory environment. Varying fire safety standards and chemical substance regulations across different regions and countries create a significant hurdle for manufacturers seeking to produce and distribute their products internationally. Compliance with these diverse regulations often requires extensive testing, certification, and potentially the development of region-specific formulations, leading to increased R&D costs, longer time-to-market, and operational complexities. This regulatory labyrinth can slow down innovation and hinder market penetration, particularly for smaller and medium-sized enterprises.

Another critical challenge is the inherent trade-off between fire retardancy and other desirable material properties. Achieving high levels of flame resistance often requires adding significant amounts of flame retardant additives, which can negatively impact a material's mechanical strength, processability, aesthetics, or overall durability. Engineers and material scientists continuously grapple with optimizing these properties to meet specific application requirements without compromising fire safety. Furthermore, the public perception and potential consumer backlash against certain chemical components, even if deemed safe by regulators, can pose an additional challenge, compelling manufacturers to constantly innovate and communicate the safety and efficacy of their products transparently. Managing waste and end-of-life solutions for products containing flame retardant resins also presents an ongoing environmental and economic challenge.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex and Fragmented Regulatory Landscape | -1.3% | Global | Long-term |

| Balancing Fire Retardancy with Other Material Properties | -1.1% | Global | Short to Medium-term |

| Public Perception and Consumer Acceptance | -0.9% | Developed Regions (Europe, North America) | Medium-term |

| High Research and Development Costs | -0.8% | Global | Long-term |

| Waste Management and Recycling of FR-containing Materials | -0.7% | Global | Long-term |

Flame Retardant Resin Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the Flame Retardant Resin market, covering historical data, current market dynamics, and future projections. It delivers critical insights into market size, growth drivers, restraints, opportunities, and key trends influencing the industry's trajectory from 2025 to 2033. The scope includes a detailed segmentation analysis by resin type, flame retardant type, application, and end-use, alongside a thorough regional and competitive landscape assessment to equip stakeholders with actionable intelligence for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.2 Billion |

| Market Forecast in 2033 | USD 11.0 Billion |

| Growth Rate | 7.5% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Albemarle Corporation, BASF SE, Clariant AG, Covestro AG, Dow Inc., DuPont de Nemours, Inc., Huber Engineered Materials, ICL Group Ltd., Lanxess AG, LyondellBasell Industries Holdings B.V., SABIC, Sumitomo Chemical Co., Ltd., Teijin Limited, ADEKA Corporation, Italmatch Chemicals S.p.A., Kingfa Sci. & Tech. Co., Ltd., Chemtura Corporation (now part of Lanxess), Celanese Corporation, Mitsui Chemicals, Inc., Solvay S.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Flame Retardant Resin market is meticulously segmented to provide a granular view of its various components and their respective contributions to the overall market dynamics. This segmentation helps in understanding the specific drivers and trends impacting different product categories and application areas. The primary segments include distinctions by the type of flame retardant employed, such as halogenated versus non-halogenated chemistries, reflecting the ongoing shift in regulatory preferences and environmental concerns. Furthermore, the market is categorized by the base resin type, which encompasses a wide array of polymers like epoxy, polypropylene, and polycarbonate, each tailored for specific performance requirements across diverse industries.

Further breakdown by application highlights the key end-use sectors where these resins are indispensable, including the building & construction industry, electrical & electronics, and automotive & transportation. Each application segment has unique fire safety standards and performance criteria, driving demand for specialized flame retardant resin formulations. The end-use segmentation then refines this by differentiating between residential, commercial, and industrial applications, allowing for a precise assessment of market penetration and growth potential within distinct economic activities. This multi-layered segmentation is crucial for stakeholders to identify niche opportunities and develop targeted strategies for market expansion.

- By Flame Retardant Type: Halogenated, Non-Halogenated

- By Resin Type: Epoxy, Polyester, Polypropylene (PP), Polycarbonate (PC), Polyamide (PA), Polyvinyl Chloride (PVC), Polyethylene (PE), Acrylonitrile Butadiene Styrene (ABS), Others

- By Application: Building & Construction, Electrical & Electronics, Automotive & Transportation, Wire & Cable, Aerospace, Textiles, Adhesives & Sealants, Coatings, Others

- By End-Use: Residential, Commercial, Industrial, Institutional

Regional Highlights

- North America: Mature market with stringent fire safety regulations, driving demand for advanced and non-halogenated flame retardant resins, particularly in the construction and automotive sectors.

- Europe: A leader in environmental regulations, strongly advocating for halogen-free solutions and bio-based flame retardants; significant market for high-performance resins in electronics and railway applications.

- Asia Pacific (APAC): Fastest-growing region due to rapid industrialization, urbanization, and robust growth in electronics manufacturing, automotive production (including EVs), and construction activities, especially in China, India, Japan, and South Korea.

- Latin America: Emerging market with growing infrastructure development and increasing adoption of international fire safety standards, leading to steady demand for flame retardant resins.

- Middle East and Africa (MEA): Significant investment in construction and infrastructure projects, particularly in the GCC countries, creating strong demand for fire-resistant materials in commercial and residential buildings.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Flame Retardant Resin Market.- Albemarle Corporation

- BASF SE

- Clariant AG

- Covestro AG

- Dow Inc.

- DuPont de Nemours, Inc.

- Huber Engineered Materials

- ICL Group Ltd.

- Lanxess AG

- LyondellBasell Industries Holdings B.V.

- SABIC

- Sumitomo Chemical Co., Ltd.

- Teijin Limited

- ADEKA Corporation

- Italmatch Chemicals S.p.A.

- Kingfa Sci. & Tech. Co., Ltd.

- Celanese Corporation

- Mitsui Chemicals, Inc.

- Solvay S.A.

- Evonik Industries AG

Frequently Asked Questions

What are flame retardant resins?

Flame retardant resins are polymer compounds formulated with specific additives that inhibit, suppress, or delay the combustion of materials. They are critical for enhancing fire safety in various products and applications by reducing flammability, limiting smoke generation, and preventing flame spread.

Why are flame retardant resins important?

Flame retardant resins are crucial for public safety and regulatory compliance. They protect lives and property by making materials less prone to ignition and reducing the rate at which fires spread, thereby providing valuable escape time and minimizing damage in applications like electronics, construction, and transportation.

What are the main types of flame retardant resins?

The main types include halogenated (e.g., brominated, chlorinated) and non-halogenated (e.g., phosphorus-based, nitrogen-based, inorganic hydroxides, silicone-based) resins. The market is increasingly shifting towards non-halogenated options due to environmental and health concerns.

Which industries primarily use flame retardant resins?

Key industries utilizing flame retardant resins include Building & Construction (insulation, flooring), Electrical & Electronics (circuit boards, cables), Automotive & Transportation (interior components, battery enclosures), Wire & Cable, and Aerospace, due to stringent fire safety requirements in these sectors.

What are the future trends in the flame retardant resin market?

Future trends include a strong emphasis on sustainable and bio-based flame retardant solutions, continued growth in non-halogenated formulations, increasing demand from the electric vehicle sector, and the development of multi-functional resins with enhanced performance properties beyond just fire resistance.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted