Lumber Market

Lumber Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709442 | Last Updated : December 09, 2025 |

Format : ![]()

![]()

![]()

![]()

Lumber Market Size

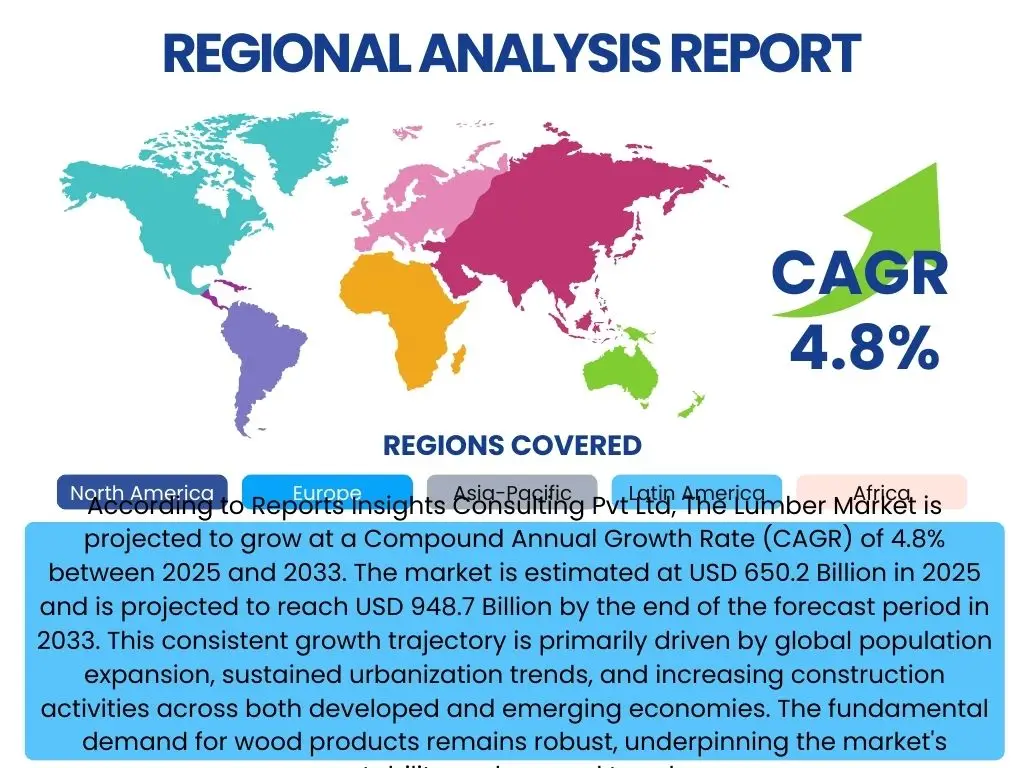

According to Reports Insights Consulting Pvt Ltd, The Lumber Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. The market is estimated at USD 650.2 Billion in 2025 and is projected to reach USD 948.7 Billion by the end of the forecast period in 2033. This consistent growth trajectory is primarily driven by global population expansion, sustained urbanization trends, and increasing construction activities across both developed and emerging economies. The fundamental demand for wood products remains robust, underpinning the market's stability and upward trend.

The valuation reflects a mature yet dynamic industry, continuously adapting to evolving global demands and sustainability imperatives. Factors such as technological advancements in forestry and milling, coupled with the growing preference for natural and renewable building materials, contribute significantly to this optimistic outlook. The inherent versatility of lumber and its broad applications, from structural components in residential and commercial buildings to furniture manufacturing and packaging solutions, ensure its continued relevance and market expansion.

Key Lumber Market Trends & Insights

User inquiries frequently highlight the evolving landscape of the lumber market, focusing on how sustainability, technological innovation, and shifting consumer preferences are shaping its future. There is a strong interest in understanding the impact of environmental regulations, the adoption of advanced manufacturing processes, and the increasing demand for certified and responsibly sourced wood products. Furthermore, users are keen to discern how global supply chain disruptions and geopolitical factors are influencing lumber prices and availability, signaling a need for comprehensive insights into market resilience and adaptability.

A significant trend observed is the accelerating shift towards sustainable forestry and the certification of lumber products. Consumers and industries alike are increasingly prioritizing environmentally friendly sourcing, driving demand for Forest Stewardship Council (FSC) or Programme for the Endorsement of Forest Certification (PEFC) certified timber. This focus is not only a response to regulatory pressures but also a proactive measure by market players to enhance brand reputation and meet corporate social responsibility objectives. The integration of advanced analytics and automation in lumber processing is another critical insight, leading to improved efficiency, reduced waste, and enhanced product quality.

The market is also witnessing a surge in the popularity of engineered wood products (EWPs) such as cross-laminated timber (CLT) and glulam. These products offer superior strength, stability, and environmental benefits compared to traditional lumber, making them highly attractive for large-scale construction projects and prefabricated building solutions. This trend reflects an industry adapting to modern construction demands, offering innovative solutions that are both structurally sound and ecologically responsible, further cementing lumber's role in the future of sustainable building.

- Accelerated adoption of sustainable forestry practices and certification standards (e.g., FSC, PEFC).

- Growing demand for engineered wood products (EWPs) like CLT and glulam in construction.

- Increased integration of digitalization and automation in lumber production and supply chain management.

- Rising preference for renewable and natural building materials over conventional alternatives.

- Volatile global lumber prices influenced by supply chain disruptions, trade policies, and natural events.

- Emphasis on circular economy principles, promoting lumber recycling and repurposing.

- Development of advanced wood modification technologies for enhanced durability and performance.

AI Impact Analysis on Lumber

Common user questions regarding AI's impact on the lumber market revolve around its potential to optimize forest management, enhance operational efficiency in sawmills, and streamline supply chains. Users frequently inquire about how artificial intelligence can contribute to sustainable harvesting practices, improve wood quality assessment, and provide predictive insights for market dynamics. There is a keen interest in understanding the practical applications of AI, from drone-based forest monitoring to automated sorting and grading systems, and the overall economic and environmental benefits it can deliver to a traditionally labor-intensive industry.

AI's influence is particularly transformative in forest management, where it enables more precise and sustainable harvesting. Algorithms can analyze satellite imagery, drone data, and environmental factors to predict forest growth, detect diseases, and optimize felling schedules, minimizing waste and ensuring long-term forest health. This data-driven approach allows for better resource allocation and compliance with environmental regulations, shifting forestry towards a more intelligent and ecologically responsible model. Furthermore, AI-powered predictive analytics can forecast timber yields and market demand, providing invaluable insights for strategic planning and inventory management.

Within lumber processing, AI is revolutionizing sawmill operations through automation and quality control. Machine vision systems, powered by AI, can accurately grade lumber, identify defects, and optimize cutting patterns to maximize yield from each log, reducing material waste and increasing profitability. Robotics integrated with AI can handle heavy machinery and repetitive tasks, improving worker safety and overall operational efficiency. This level of automation not only boosts productivity but also ensures consistent product quality, which is crucial for meeting stringent industry standards and customer expectations in a competitive global market.

- Predictive analytics for optimized forest growth and sustainable harvesting schedules.

- AI-powered machine vision for automated lumber grading, defect detection, and quality control in sawmills.

- Drone and satellite imagery analysis for comprehensive forest inventory, health monitoring, and illegal logging prevention.

- Optimization of lumber supply chain logistics, including route planning and inventory management, through AI algorithms.

- Enhanced demand forecasting and market trend analysis for better production planning and pricing strategies.

- Robotics and automation in sawmills for increased efficiency, reduced labor costs, and improved worker safety.

- Development of smart wood products with integrated sensors for real-time performance monitoring.

Key Takeaways Lumber Market Size & Forecast

User queries regarding key takeaways from the lumber market size and forecast consistently seek concise insights into the industry's future trajectory, particularly concerning sustained growth, pivotal drivers, and inherent challenges. There is a strong demand for understanding the long-term viability of lumber as a primary construction and manufacturing material, alongside the critical factors that will shape its evolution over the coming decade. Users are also interested in identifying the primary investment opportunities and strategic considerations for stakeholders navigating this dynamic global market.

The overarching takeaway is the consistent, albeit moderate, growth projected for the lumber market, driven by an unyielding global demand for construction and housing. Despite fluctuations stemming from economic cycles and geopolitical events, lumber's essential role in infrastructure development and residential expansion ensures its market resilience. The forecast underscores the industry's capacity for adaptation, particularly in embracing sustainable practices and technological innovations to maintain its competitive edge and address environmental concerns. This adaptability is key to unlocking future growth potential and overcoming market hurdles.

Another crucial insight is the increasing influence of sustainability and responsible sourcing on market dynamics. The shift towards green building initiatives and consumer preference for eco-friendly materials is not merely a trend but a fundamental driver shaping procurement, production, and distribution strategies. Companies that invest in certified forests, advanced processing techniques, and efficient supply chains are better positioned to capture market share and achieve long-term success. The integration of advanced analytics and automation will further empower the industry to optimize operations, mitigate risks, and respond effectively to evolving market demands, solidifying lumber's foundational role in a sustainable global economy.

- The global lumber market is poised for steady growth, driven by consistent demand in construction and manufacturing sectors.

- Sustainability and responsible sourcing are no longer niche concerns but core drivers shaping market strategies and consumer preferences.

- Technological advancements, including AI and automation, are crucial for optimizing production efficiency and supply chain management.

- Engineered wood products represent a significant growth segment, offering innovative solutions for modern construction.

- Market resilience is strong, though susceptible to external factors like raw material price volatility and trade policies.

- Asia Pacific will remain a primary growth engine due to rapid urbanization and infrastructure development.

- Strategic investments in sustainable forestry and processing technologies are essential for long-term competitive advantage.

Lumber Market Drivers Analysis

The lumber market is significantly propelled by several key drivers that reflect global economic growth, demographic shifts, and evolving industrial practices. Primarily, the robust expansion in residential and commercial construction worldwide forms the bedrock of demand for various lumber products. Urbanization trends, particularly in emerging economies, necessitate vast housing and infrastructure projects, directly fueling the consumption of timber. This continuous need for new buildings, renovations, and expansions creates a stable and growing demand base for the industry.

Furthermore, the increasing global emphasis on sustainable and green building practices is a powerful driver. Lumber, as a renewable resource, is increasingly preferred over less sustainable materials, aligning with environmental goals and regulatory mandates. This shift is supported by various certifications and standards that promote responsible forestry, enhancing lumber's appeal as an eco-friendly choice. The growing awareness among consumers and developers about the carbon sequestration benefits of wood products further amplifies this demand, positioning lumber as a crucial component in environmentally conscious construction.

Technological advancements in wood processing and the development of innovative engineered wood products also serve as significant drivers. These innovations enhance lumber's structural integrity, durability, and versatility, expanding its application scope beyond traditional uses. Such progress not only opens new markets but also allows lumber to compete more effectively with alternative building materials, showcasing its adaptability and superior performance characteristics in modern construction and design. The ongoing need for DIY and renovation activities also consistently contributes to market demand, particularly in developed regions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Residential & Commercial Construction Boom | +1.5% | Global (Asia Pacific, North America) | 2025-2033 |

| Growing Adoption of Green Building Practices | +0.8% | Europe, North America, Developing Economies | 2025-2033 |

| Urbanization and Infrastructure Development | +1.2% | Asia Pacific, Latin America, Africa | 2025-2033 |

| Increased Demand for Engineered Wood Products | +0.7% | North America, Europe, Japan | 2025-2033 |

| DIY and Renovation Activities | +0.6% | North America, Europe | 2025-2030 |

| Population Growth & Housing Demand | +1.0% | Global | 2025-2033 |

Lumber Market Restraints Analysis

Despite its inherent advantages and market growth, the lumber industry faces several significant restraints that can impede its expansion and influence profitability. One of the primary challenges is the volatile pricing of raw materials, largely influenced by unpredictable factors such as weather patterns, natural disasters like forest fires, and pest infestations. These events can severely disrupt timber supply, leading to sudden price spikes that impact manufacturing costs and, consequently, end-product prices, making financial planning difficult for market participants and potentially reducing consumer demand.

Another critical restraint involves stringent environmental regulations and conservation efforts. While these are essential for sustainable forestry, they can sometimes limit logging access to certain forest areas, increase operational costs due to compliance requirements, and extend the lead times for obtaining permits. These regulations, varying significantly across regions, can create complex operational hurdles for lumber producers, especially those operating internationally, by restricting resource availability and driving up the cost of sustainable harvesting and processing.

Furthermore, the lumber market faces intense competition from alternative building materials such as steel, concrete, and plastic composites. These substitutes often offer competitive pricing, ease of installation, or specific performance characteristics that may be preferred in certain applications. This competition forces lumber producers to continually innovate, differentiate their products, and emphasize the unique benefits of wood to maintain market share. Supply chain disruptions, exacerbated by geopolitical tensions and global logistics challenges, also pose a recurring restraint, affecting the timely delivery of raw timber and processed lumber to markets worldwide.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Price Volatility | -1.0% | Global | 2025-2033 |

| Stringent Environmental Regulations | -0.7% | Europe, North America | 2025-2033 |

| Competition from Substitute Materials | -0.5% | Global | 2025-2033 |

| Supply Chain Disruptions | -0.8% | Global | 2025-2030 |

| Illegal Logging & Trade Barriers | -0.4% | Asia Pacific, Latin America, Africa | 2025-2033 |

Lumber Market Opportunities Analysis

The lumber market is ripe with opportunities that can drive significant growth and innovation, particularly through strategic investments in sustainability and technological advancement. A major opportunity lies in the expanding adoption of engineered wood products (EWPs). These advanced materials, offering superior structural performance, design flexibility, and environmental benefits compared to traditional lumber, are gaining traction in large-scale construction projects, including multi-story residential and commercial buildings. The increasing recognition of their advantages is opening new market segments and challenging conventional building material choices.

Another substantial opportunity resides in the growing global emphasis on sustainable forest management and the circular bioeconomy. As environmental consciousness rises and regulatory frameworks strengthen, there is a clear market advantage for companies demonstrating commitment to responsible sourcing, reforestation, and resource efficiency. Investing in certified sustainable forestry practices not only meets regulatory compliance but also enhances brand reputation and taps into the increasing consumer and corporate demand for eco-friendly products. This paradigm shift encourages innovation in wood utilization and waste reduction, creating value from what was previously considered waste.

Furthermore, market expansion into rapidly developing economies, particularly in Asia Pacific, Latin America, and Africa, presents considerable growth opportunities. These regions are experiencing rapid urbanization, population growth, and significant infrastructure development, leading to a surge in demand for building materials. Companies that can effectively navigate the local market dynamics, establish robust supply chains, and tailor their product offerings to meet regional specificities stand to capture substantial market share. Digital transformation, encompassing everything from smart forest monitoring to e-commerce platforms for lumber, also offers avenues for operational efficiency and market reach.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of Engineered Wood Products (EWPs) | +1.0% | North America, Europe, Asia Pacific | 2025-2033 |

| Expansion in Emerging Economies | +1.3% | Asia Pacific, Latin America, Africa | 2025-2033 |

| Increased Focus on Sustainable & Certified Lumber | +0.9% | Global | 2025-2033 |

| Technological Advancements in Processing & Management | +0.6% | Global | 2025-2033 |

| Development of Prefabricated and Modular Construction | +0.7% | Europe, North America | 2025-2030 |

Lumber Market Challenges Impact Analysis

The lumber market, while dynamic, faces several formidable challenges that require strategic responses from industry stakeholders. Climate change represents a significant and escalating challenge, manifesting through increased frequency and intensity of forest fires, prolonged droughts, and enhanced pest outbreaks. These environmental phenomena directly threaten timber resources by destroying forests, reducing timber yield, and increasing operational costs associated with forest protection and restoration, leading to unpredictable supply shortages and price volatility across the globe.

Another critical challenge is the persistent issue of illegal logging and deforestation, particularly prevalent in regions with weak governance and enforcement. Illegal logging not only leads to unsustainable resource depletion but also creates an unfair competitive landscape by introducing cheap, illicit timber into the market, which undercuts prices for legally and sustainably harvested lumber. This practice tarnishes the industry's reputation, hinders efforts towards sustainability, and complicates the sourcing of certified wood products for legitimate businesses, demanding robust international cooperation and stronger regulatory oversight.

Furthermore, geopolitical instability and trade protectionism pose substantial challenges to the global lumber trade. Tariffs, import restrictions, and political disputes can disrupt established supply chains, increase transportation costs, and create market access barriers, making it difficult for producers to reach international customers. Such uncertainties necessitate greater supply chain resilience and diversification, pushing companies to adapt quickly to shifting trade policies and seek alternative sourcing or market destinations. Labor shortages, particularly skilled labor in forestry and milling, also present an ongoing challenge, impacting production capacity and operational efficiency.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Climate Change Impact (Fires, Pests) | -1.2% | Global | 2025-2033 |

| Illegal Logging & Deforestation | -0.9% | Asia Pacific, Latin America, Africa | 2025-2033 |

| Geopolitical Instability & Trade Barriers | -0.8% | Global | 2025-2030 |

| Labor Shortages & Rising Labor Costs | -0.6% | North America, Europe | 2025-2033 |

| High Transportation & Logistics Costs | -0.5% | Global | 2025-2033 |

Lumber Market - Updated Report Scope

This comprehensive market research report delves into the intricate dynamics of the global lumber market, providing an in-depth analysis of its current size, historical performance, and future growth projections. The scope encompasses a detailed examination of key trends, drivers, restraints, opportunities, and challenges that are shaping the industry landscape. Special attention is given to the impact of evolving sustainability mandates, technological advancements, and shifting consumer preferences on market evolution. The report offers a granular view of market segmentation by type, application, and end-use, complemented by a thorough regional analysis to highlight geographical nuances and growth pockets.

The analysis aims to equip stakeholders with actionable insights, enabling informed strategic decision-making. It covers the competitive landscape by profiling leading market participants, detailing their strategic initiatives, product portfolios, and market positioning. Furthermore, the report incorporates an AI impact analysis, assessing how artificial intelligence and related technologies are revolutionizing forest management, processing efficiency, and supply chain optimization within the lumber sector. This holistic approach ensures a robust understanding of both macro and micro-environmental factors influencing the market's trajectory.

In addition to quantitative market data and forecasts, the report provides qualitative insights derived from extensive primary and secondary research. It addresses common user inquiries regarding market dynamics, offering AEO-optimized answers to frequently asked questions. By presenting a forward-looking perspective, the report identifies emerging opportunities and potential risks, empowering businesses to anticipate market shifts and formulate resilient growth strategies in an increasingly complex global economy. The structured format and detailed breakdowns ensure accessibility and practical utility for a diverse audience, from investors to industry executives.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 650.2 Billion |

| Market Forecast in 2033 | USD 948.7 Billion |

| Growth Rate | 4.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Timber Corp, Forest Innovations Ltd, Nordic Wood Group, Pacific Lumber Solutions, Evergreen Wood Products, Sierra Forest Industries, Redwood Global, Timberland Holdings Inc., Woodlink International, Green Forest Products, Artisan Timber Co., United Wood Group, Prime Lumber Supply, EcoWood Solutions, Frontier Timberworks, Millbrook Lumber, Canopy Wood Products, Summit Timber, Horizon Forestry, Apex Wood Industries |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The lumber market is highly segmented, allowing for a granular understanding of its diverse components and drivers. Segmentation by type primarily distinguishes between softwood and hardwood, each possessing distinct properties, applications, and market values. Softwoods, such as pine and spruce, are characterized by their rapid growth and relatively lower density, making them ideal for structural framing, pulp, and paper production. Hardwoods, including oak and maple, are denser and more durable, finding extensive use in furniture, flooring, and decorative applications due to their aesthetic appeal and longevity. The demand for each type is influenced by regional forest resources and specific end-use requirements, impacting their respective market dynamics and growth trajectories.

Further segmentation by application and end-use provides critical insights into consumption patterns. Residential and commercial construction represent the largest application segments, with lumber being a fundamental material for framing, roofing, and interior finishes. The growth in these sectors directly correlates with urbanization, population growth, and infrastructure development globally. Beyond construction, lumber is vital for furniture manufacturing, packaging (crates, pallets), and industrial applications, each category responding to unique economic and consumer trends. The increasing adoption of prefabricated and modular construction methods is also creating new demand patterns within these application segments, driving innovation in lumber product development.

The detailed segmentation also facilitates an understanding of regional market nuances, as resource availability, regulatory environments, technological adoption rates, and cultural preferences significantly vary across geographical areas. For instance, while North America and Europe show a mature market with a strong emphasis on sustainable forestry and engineered wood products, Asia Pacific is characterized by high growth in basic construction lumber driven by rapid urbanization and industrialization. Analyzing these segments individually and collectively enables market participants to identify lucrative opportunities, tailor their product offerings, and optimize their supply chains to effectively serve diverse customer needs and regional demands.

- By Type:

- Softwood (e.g., Pine, Spruce, Fir)

- Hardwood (e.g., Oak, Maple, Cherry)

- By Application:

- Residential Construction (Single-family homes, Multi-family dwellings)

- Commercial Construction (Office buildings, Retail spaces, Institutional structures)

- Industrial Use (Industrial buildings, Warehouses)

- By End-Use:

- Construction (Framing, Sheathing, Roofing, Siding)

- Furniture Manufacturing (Solid wood furniture, Veneers)

- Packaging (Pallets, Crates, Boxes)

- Pallets and Skids

- Flooring (Hardwood flooring, Engineered wood flooring)

- Pulp & Paper

- Others (Decking, Fencing, Landscaping, DIY projects)

- By Region:

- North America (U.S., Canada, Mexico)

- Europe (Germany, U.K., France, Italy, Spain, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- Latin America (Brazil, Argentina, Rest of Latin America)

- Middle East & Africa (UAE, Saudi Arabia, South Africa, Rest of MEA)

Regional Highlights

Regional dynamics play a pivotal role in shaping the global lumber market, with each geographical area exhibiting unique supply-demand characteristics, regulatory frameworks, and growth trajectories. North America, encompassing the United States and Canada, represents a mature and technologically advanced market. It is characterized by robust domestic demand driven by residential construction and a strong emphasis on sustainable forestry and engineered wood products. The region is a significant producer and exporter of softwood lumber, with a well-established supply chain and increasing adoption of automation in milling. Innovation in wood architecture and modular construction methods further solidify its position as a key market leader.

Europe stands out for its stringent environmental regulations, high value-added wood products, and a strong commitment to the circular bioeconomy. Countries like Germany, Sweden, and Finland are leaders in sustainable forest management and advanced wood processing technologies, focusing on high-quality sawn timber, joinery, and innovative wood-based materials. The region also exhibits a growing preference for certified timber and a strong market for prefabrication and off-site construction, where engineered wood products are extensively utilized. Demand here is stable, driven by renovation activities and green building initiatives.

Asia Pacific is undeniably the growth engine of the global lumber market, primarily fueled by rapid urbanization, massive infrastructure projects, and a burgeoning middle class in countries like China, India, and Southeast Asian nations. While the region is a significant consumer, relying heavily on imports for much of its timber, there is also increasing domestic production and investment in forestry. The demand is diverse, ranging from basic construction lumber to high-quality timber for furniture and interior design. Latin America, particularly Brazil, is a major timber resource, though challenges like illegal logging and infrastructure limitations exist. The Middle East and Africa regions are emerging markets with developing construction sectors, often relying on lumber imports to meet their growing needs for building materials.

- North America: A mature market with high demand from residential construction, a strong focus on sustainable forestry, and a leader in engineered wood products. Key producers like the U.S. and Canada drive exports.

- Europe: Characterized by stringent environmental regulations, advanced wood processing technologies, and a growing market for certified and high value-added lumber products for green building and renovation.

- Asia Pacific (APAC): The fastest-growing region, driven by rapid urbanization, infrastructure development, and increasing housing demand in countries like China, India, and Southeast Asia. Significant importer of lumber.

- Latin America: A resource-rich region, particularly Brazil, with substantial timber reserves. Market growth is influenced by internal development projects but also faces challenges related to sustainable practices and market access.

- Middle East & Africa (MEA): Emerging markets with developing construction sectors and increasing demand for lumber, largely met through imports. Growth is tied to economic diversification and infrastructure investment.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Lumber Market.- Global Timber Corp

- Forest Innovations Ltd

- Nordic Wood Group

- Pacific Lumber Solutions

- Evergreen Wood Products

- Sierra Forest Industries

- Redwood Global

- Timberland Holdings Inc.

- Woodlink International

- Green Forest Products

- Artisan Timber Co.

- United Wood Group

- Prime Lumber Supply

- EcoWood Solutions

- Frontier Timberworks

- Millbrook Lumber

- Canopy Wood Products

- Summit Timber

- Horizon Forestry

- Apex Wood Industries

Frequently Asked Questions

Analyze common user questions about the Lumber market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth of the Lumber Market?

The Lumber Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% from USD 650.2 Billion in 2025 to USD 948.7 Billion by 2033, driven by global construction and sustainable material demand.

What are the primary drivers for the Lumber Market?

Key drivers include robust residential and commercial construction, increasing adoption of green building practices, rapid urbanization, and growing demand for innovative engineered wood products.

How do sustainability concerns impact the Lumber Market?

Sustainability is a major driver, leading to increased demand for certified lumber, adoption of eco-friendly forestry practices, and a shift towards renewable building materials, influencing consumer preferences and industry standards.

What role does technology play in the modern lumber industry?

Technology, particularly AI and automation, is enhancing forest management through predictive analytics, optimizing sawmill operations for efficiency and quality control, and streamlining supply chain logistics.

Which regions are expected to show significant growth in the Lumber Market?

Asia Pacific is anticipated to be the fastest-growing region due to extensive urbanization and infrastructure development, while North America and Europe will maintain stable growth with a focus on value-added products.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted