Steel Market

Steel Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710290 | Last Updated : January 02, 2026 |

Format : ![]()

![]()

![]()

![]()

Steel Market Size

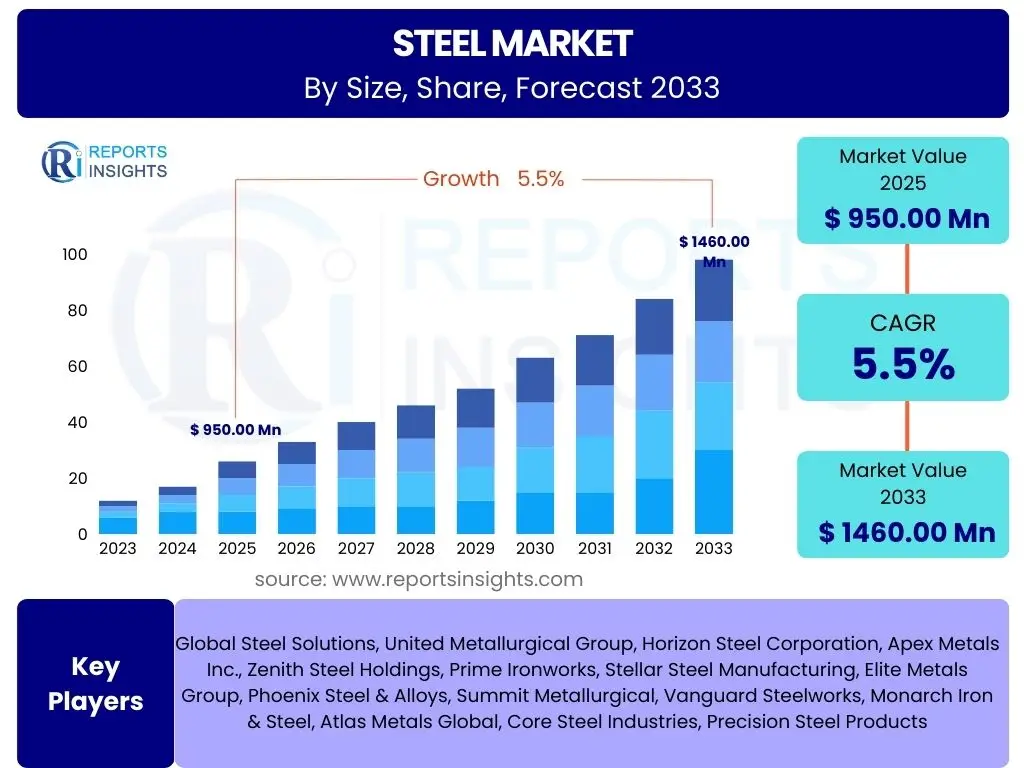

According to Reports Insights Consulting Pvt Ltd, The Steel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.5% between 2025 and 2033. The market is estimated at USD 950.00 Billion in 2025 and is projected to reach USD 1460.00 Billion by the end of the forecast period in 2033.

Key Steel Market Trends & Insights

User inquiries frequently highlight the evolving landscape of the steel industry, with a strong focus on sustainability, technological integration, and demand shifts in key end-use sectors. Stakeholders are particularly interested in how environmental regulations and circular economy principles are influencing production processes and product development. There is also significant curiosity regarding the adoption of advanced manufacturing techniques and smart factory concepts, alongside the impact of global geopolitical dynamics on raw material supply chains and trade flows.

The transition towards green steel production, driven by stringent carbon emission targets, represents a pivotal trend reshaping the market. This involves the increased use of electric arc furnaces (EAFs), hydrogen-based steelmaking, and carbon capture technologies. Furthermore, the demand for high-strength and lightweight steel in the automotive and construction sectors continues to drive innovation, as industries seek materials that contribute to energy efficiency and reduced environmental footprint. The digital transformation within steel manufacturing is also gaining momentum, leveraging data analytics and automation to optimize operations and enhance productivity.

- Escalating adoption of green steel production methods and decarbonization initiatives.

- Growing demand for advanced, high-strength, and lightweight steel from automotive and construction sectors.

- Increased integration of digital technologies, automation, and AI across the steel value chain.

- Shifting global supply chain dynamics influencing raw material procurement and market competitiveness.

- Emphasis on circular economy principles, promoting steel recycling and extended product lifecycles.

AI Impact Analysis on Steel

Common user questions regarding AI's impact on the steel industry center around its applications in optimizing production, enhancing quality control, and improving supply chain efficiency. There is significant interest in how artificial intelligence can reduce operational costs, minimize waste, and predict maintenance needs, thereby extending equipment lifespan. Users also frequently inquire about the challenges associated with AI adoption, such as data security, the need for specialized skills, and the integration with legacy systems.

AI is increasingly being deployed in various stages of steel production, from raw material sourcing and furnace operations to rolling and finishing processes. Predictive analytics powered by AI algorithms can anticipate equipment failures, enabling proactive maintenance and reducing downtime. Machine learning models are also crucial for optimizing energy consumption in energy-intensive processes, leading to substantial cost savings and a reduced carbon footprint. Furthermore, AI-driven quality inspection systems can detect defects with high precision and speed, ensuring consistent product quality and reducing material waste.

The future expectation is that AI will drive a more autonomous and data-driven steel industry, enabling greater agility and responsiveness to market demands. While the initial investment and skill gap present hurdles, the long-term benefits in terms of efficiency, sustainability, and competitive advantage are expected to drive widespread adoption. Collaboration between technology providers and steel manufacturers will be key to developing tailored AI solutions that address specific industry challenges and maximize operational gains.

- Optimization of production processes through predictive analytics and machine learning.

- Enhanced quality control and defect detection using AI-powered vision systems.

- Improved energy efficiency and reduced operational costs via AI-driven process control.

- Predictive maintenance for machinery, minimizing downtime and extending asset life.

- Supply chain optimization, including demand forecasting and logistics management.

Key Takeaways Steel Market Size & Forecast

User queries about the key takeaways from the steel market size and forecast often revolve around understanding the primary growth drivers, the resilience of the market against economic fluctuations, and the long-term sustainability prospects. Stakeholders are keen to identify the most lucrative segments and regions, as well as the underlying factors contributing to the projected market expansion. The emphasis is on actionable insights that can inform strategic planning and investment decisions, considering both opportunities and potential risks.

The forecast for the steel market indicates a steady growth trajectory, primarily fueled by urbanization, infrastructure development in emerging economies, and the continuous demand from key industries such as automotive and construction. Despite cyclical challenges, the market demonstrates resilience due to its fundamental role in global economic activity. The increasing focus on sustainable and green steel production methods is not only a regulatory imperative but also a significant growth area, attracting investments in new technologies and processes.

Overall, the market is poised for sustained expansion, albeit with evolving dynamics. Innovation in material science, coupled with digital transformation, will be crucial for maintaining competitiveness. Companies that prioritize sustainability, invest in advanced manufacturing, and strategically position themselves in high-growth application areas are likely to capture significant market share. The regional disparity in growth rates also highlights the importance of localized strategies to capitalize on specific market opportunities.

- Steady market expansion driven by infrastructure projects and industrialization globally.

- Significant growth in demand for specialized and high-performance steel products.

- Increased investment in green steel technologies and sustainable production methods.

- Emerging economies, particularly in Asia Pacific, will be key growth engines.

- Digital transformation and AI integration are critical for operational efficiency and competitive advantage.

Steel Market Drivers Analysis

The global steel market is primarily driven by robust demand from key end-use sectors, propelled by widespread urbanization, infrastructure development, and industrial growth. The expanding construction industry, particularly in developing nations, necessitates vast quantities of steel for residential, commercial, and public works projects. Similarly, the automotive sector's continuous evolution towards safer, lighter, and more fuel-efficient vehicles fuels the demand for advanced and specialized steel grades.

Furthermore, rapid industrialization, especially in Asia Pacific and parts of Latin America, increases the consumption of steel in manufacturing processes for machinery, equipment, and various consumer goods. Government initiatives aimed at boosting manufacturing capabilities and upgrading existing infrastructure also play a crucial role in stimulating steel demand. The inherent recyclability of steel also supports its sustainable appeal, aligning with global environmental objectives and fostering its continued use across diverse applications.

Technological advancements in steel production, leading to more efficient processes and higher-quality products, further support market expansion by making steel a more competitive and versatile material. The growing energy sector, including renewable energy infrastructure, also represents a significant driver, requiring steel for wind turbines, solar panel frames, and power transmission structures. These multifaceted drivers collectively contribute to the market's positive outlook, ensuring a consistent and diverse demand base.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Urbanization & Infrastructure Development | +1.5% | Asia Pacific, Latin America, Africa | Medium to Long Term (2025-2033) |

| Growth in Automotive & Transportation Sector | +1.2% | North America, Europe, Asia Pacific | Medium Term (2025-2030) |

| Industrialization and Manufacturing Sector Expansion | +1.0% | Asia Pacific, Middle East & Africa | Long Term (2025-2033) |

| Technological Advancements in Steel Production | +0.8% | Global | Medium to Long Term (2025-2033) |

Steel Market Restraints Analysis

Despite robust demand, the steel market faces significant restraints that can impede its growth trajectory. Volatility in raw material prices, particularly iron ore and coking coal, presents a major challenge, directly impacting production costs and profit margins for steel manufacturers. These price fluctuations are often influenced by geopolitical tensions, supply chain disruptions, and global economic shifts, making long-term planning difficult for market participants.

Environmental regulations and escalating pressures for decarbonization represent another substantial restraint. Steel production is energy-intensive and a significant contributor to carbon emissions. Compliance with stricter environmental policies, coupled with the high capital investment required for adopting green technologies like hydrogen-based steelmaking or carbon capture, poses a considerable financial burden on companies, especially smaller players. This can lead to increased operational costs and potentially slow down production expansion.

Furthermore, trade protectionism and tariffs imposed by various countries can disrupt international trade flows, creating market inefficiencies and increasing the cost of steel. Overcapacity in certain regions, particularly in Asia, also contributes to downward pressure on steel prices, affecting profitability across the industry. These combined factors necessitate careful strategic navigation for companies operating in the global steel market.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices (Iron Ore, Coking Coal) | -1.3% | Global | Short to Medium Term (2025-2028) |

| Stringent Environmental Regulations & Decarbonization Costs | -1.0% | Europe, North America, Asia Pacific (China) | Medium to Long Term (2025-2033) |

| Global Trade Tensions & Protectionist Measures | -0.7% | Global | Short to Medium Term (2025-2029) |

| Overcapacity in Key Producing Regions | -0.5% | Asia Pacific (China, India) | Medium Term (2025-2030) |

Steel Market Opportunities Analysis

Significant opportunities exist within the steel market, primarily driven by the burgeoning demand for sustainable and specialized steel products. The global imperative for decarbonization is fostering a substantial shift towards green steel production, opening avenues for companies investing in hydrogen-reduced steel, electric arc furnace (EAF) technologies utilizing scrap, and carbon capture utilization and storage (CCUS) solutions. This transition not only addresses environmental concerns but also positions early adopters for a competitive advantage in a future-proof market.

The increasing focus on developing advanced high-strength steels (AHSS) and ultra-high-strength steels (UHSS) presents another lucrative opportunity. These materials are critical for automotive light-weighting, enhancing fuel efficiency and reducing emissions, as well as for specialized applications in defense, aerospace, and energy sectors. Continuous innovation in metallurgy and manufacturing processes to produce these advanced grades can unlock new market segments and command premium pricing.

Furthermore, the growth of renewable energy infrastructure globally, including wind turbines, solar farms, and hydropower projects, requires substantial amounts of steel. Investment in urban infrastructure modernization, smart cities, and resilient construction also creates sustained demand for durable and sustainable steel solutions. Leveraging digital technologies for smart manufacturing, predictive maintenance, and supply chain optimization offers efficiency gains and new business models, enhancing market responsiveness and profitability.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of Green Steel & Sustainable Production Methods | +1.8% | Europe, North America, Asia Pacific | Long Term (2026-2033) |

| Rising Demand for Advanced & High-Strength Steels | +1.5% | Global | Medium to Long Term (2025-2033) |

| Expansion in Renewable Energy Infrastructure | +1.2% | Global | Medium to Long Term (2025-2033) |

| Digital Transformation & Smart Manufacturing Initiatives | +0.9% | Global | Short to Medium Term (2025-2030) |

Steel Market Challenges Impact Analysis

The steel market faces a complex array of challenges that significantly impact its stability and growth. Intense global competition, particularly from overcapacity in certain regions, often leads to price erosion and reduced profit margins for manufacturers. This competitive pressure is exacerbated by varied production costs and governmental subsidies across different countries, creating an uneven playing field and challenging market equilibrium.

Fluctuating energy costs represent another critical challenge, as steel production is highly energy-intensive. Spikes in electricity or fuel prices can directly increase operational expenses, compelling companies to seek more efficient production methods or absorb higher costs, which ultimately impacts profitability. Geopolitical instability and trade disputes further complicate the global supply chain, leading to uncertainty in raw material procurement and market access.

Additionally, the industry grapples with the imperative to innovate and adapt to rapidly evolving technological landscapes and environmental mandates. The significant capital expenditure required for upgrading to greener technologies, alongside the need to develop new, higher-performance steel grades, poses a considerable financial and technical hurdle. Workforce challenges, including the need for skilled labor in advanced manufacturing and digital technologies, also present a bottleneck for innovation and efficient operation.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Global Competition & Overcapacity | -1.4% | Global, particularly Asia Pacific | Medium to Long Term (2025-2033) |

| Volatile Energy Prices & High Operating Costs | -1.1% | Global | Short to Medium Term (2025-2029) |

| Stringent Regulatory & Environmental Compliance Costs | -0.9% | Europe, North America, Asia Pacific | Medium to Long Term (2025-2033) |

| Geopolitical Instability & Trade Disruptions | -0.8% | Global | Short Term (2025-2027) |

Steel Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global steel market, offering valuable insights into its current size, historical performance, and future growth projections. It meticulously examines key market drivers, restraints, opportunities, and challenges, providing a holistic view of the factors influencing market dynamics. The scope also includes a detailed segmentation analysis, regional highlights, and profiles of leading market players, designed to equip stakeholders with essential information for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 950.00 Billion |

| Market Forecast in 2033 | USD 1460.00 Billion |

| Growth Rate | 5.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Steel Solutions, United Metallurgical Group, Horizon Steel Corporation, Apex Metals Inc., Zenith Steel Holdings, Prime Ironworks, Stellar Steel Manufacturing, Elite Metals Group, Phoenix Steel & Alloys, Summit Metallurgical, Vanguard Steelworks, Monarch Iron & Steel, Atlas Metals Global, Core Steel Industries, Precision Steel Products |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The steel market is comprehensively segmented to provide granular insights into its diverse components and their respective contributions to overall market dynamics. This segmentation facilitates a deeper understanding of varying demand patterns, technological preferences, and regional consumption trends, enabling stakeholders to pinpoint specific areas of growth and opportunity. The analysis covers various product types, applications, end-user industries, and production processes, each influenced by unique market forces and technological advancements.

- By Product Type: This segment includes Flat Steel (e.g., sheets, plates, coils used in automotive, construction, and appliances), Long Steel (e.g., bars, rods, wires, structural sections critical for construction and infrastructure), Stainless Steel (valued for corrosion resistance in various industries), and Specialty Steel (engineered for specific high-performance applications).

- By Application: Key applications span Construction & Infrastructure (buildings, bridges, roads), Automotive & Transportation (car bodies, railway tracks), Mechanical Equipment (machinery, tools), Packaging (food cans, containers), and Energy (pipelines, power generation), among others.

- By End-User Industry: This category further refines the application segments, focusing on major industries like Construction, Automotive, Manufacturing, Consumer Goods, and Energy & Power, providing a demand-side perspective.

- By Process: The primary production processes include Basic Oxygen Furnace (BOF) for virgin iron ore, Electric Arc Furnace (EAF) for scrap recycling, and Induction Furnace (IF), reflecting different raw material inputs and environmental footprints.

Regional Highlights

- Asia Pacific: This region is the largest and fastest-growing market for steel, driven by rapid urbanization, extensive infrastructure development in countries like China and India, and a booming manufacturing sector. Significant government investments in construction and industrial expansion further bolster demand.

- Europe: Characterized by a strong emphasis on sustainable and green steel production, Europe is a leader in adopting advanced manufacturing processes and decarbonization initiatives. The region sees steady demand from automotive, construction, and specialized engineering sectors, coupled with stringent environmental regulations.

- North America: With a mature automotive industry and ongoing infrastructure revitalization projects, North America exhibits consistent demand for steel. The region is also increasingly focused on utilizing recycled steel and implementing modern, efficient production technologies.

- Latin America: This region presents significant growth potential, fueled by emerging economies investing in infrastructure, mining, and automotive manufacturing. Brazil and Mexico are key markets, demonstrating increasing industrial activity and urbanization trends.

- Middle East and Africa (MEA): The MEA region is experiencing growth due to large-scale construction projects, diversification of economies away from oil, and increasing industrialization. Investments in energy infrastructure and urban development are prominent drivers.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Steel Market.- Global Steel Solutions

- United Metallurgical Group

- Horizon Steel Corporation

- Apex Metals Inc.

- Zenith Steel Holdings

- Prime Ironworks

- Stellar Steel Manufacturing

- Elite Metals Group

- Phoenix Steel & Alloys

- Summit Metallurgical

- Vanguard Steelworks

- Monarch Iron & Steel

- Atlas Metals Global

- Core Steel Industries

- Precision Steel Products

- Dynamic Steel International

- Everest Metals Corporation

- Fusion Steelworks

- Quantum Metals Group

- Resilient Steel Industries

Frequently Asked Questions

What is the projected growth rate of the Steel Market?

The Steel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.5% between 2025 and 2033.

What are the primary drivers for the Steel Market's expansion?

Key drivers include global urbanization, extensive infrastructure development, growth in the automotive sector, and expansion of industrial and manufacturing activities, especially in emerging economies.

How is artificial intelligence impacting the steel industry?

AI is significantly impacting the steel industry by optimizing production processes, enhancing quality control, enabling predictive maintenance, improving energy efficiency, and streamlining supply chain management.

Which regions are expected to be key growth markets for steel?

Asia Pacific is the largest and fastest-growing region due to rapid industrialization and infrastructure projects, while Europe and North America show steady demand and a strong focus on sustainable production.

What are the main challenges facing the Steel Market?

Major challenges include volatile raw material and energy prices, intense global competition, stringent environmental regulations, high decarbonization costs, and geopolitical instability affecting trade.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted