Petroleum Pitch Market

Petroleum Pitch Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710263 | Last Updated : January 02, 2026 |

Format : ![]()

![]()

![]()

![]()

Petroleum Pitch Market Size

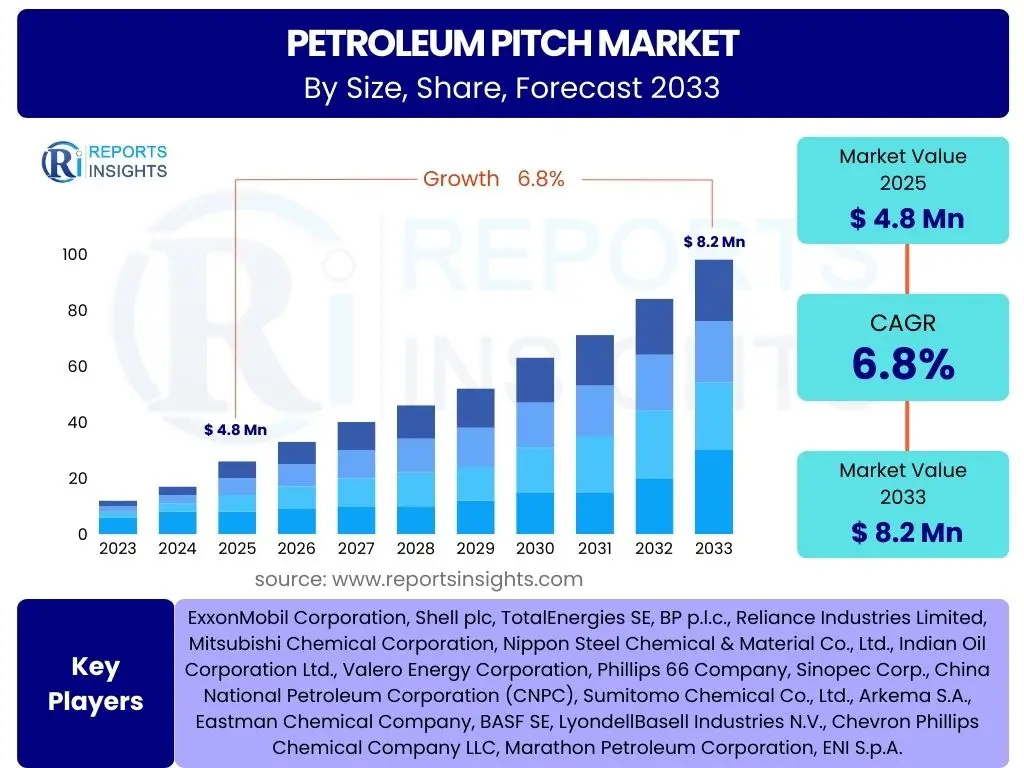

According to Reports Insights Consulting Pvt Ltd, The Petroleum Pitch Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 4.8 Billion in 2025 and is projected to reach USD 8.2 Billion by the end of the forecast period in 2033.

Key Petroleum Pitch Market Trends & Insights

The petroleum pitch market is experiencing a significant transformation driven by evolving industrial demands and technological advancements. A prominent trend is the increasing shift towards high-performance materials, where petroleum pitch serves as a crucial precursor for carbon fibers, essential in aerospace, automotive, and sporting goods industries. Furthermore, its role in the burgeoning energy storage sector, particularly as an anode material in electric vehicle (EV) batteries, is propelling substantial growth.

Industrialization in emerging economies, notably across Asia Pacific and Latin America, continues to fuel demand for traditional applications such as aluminum smelting and graphite electrode production for steel manufacturing. Concurrently, there is a growing emphasis on refining pitch properties through advanced processing techniques to meet stringent application-specific requirements, indicating a market moving towards specialization and higher value-added products.

- Growing demand for petroleum pitch as a precursor for carbon fiber manufacturing.

- Significant expansion in its application for anode materials in electric vehicle batteries.

- Increased adoption in the production of advanced refractory and ceramic materials.

- Focus on developing high-performance pitch grades for specialized industrial applications.

- Rising infrastructure and construction activities, particularly in developing regions.

- Integration of sustainable practices and byproduct valorization within the industry.

AI Impact Analysis on Petroleum Pitch

The integration of Artificial Intelligence (AI) is poised to revolutionize various facets of the petroleum pitch value chain, from initial feedstock management to end-product optimization. AI algorithms can enhance the efficiency of refinery processes by predicting optimal operating conditions for pitch production, thereby minimizing waste and improving yield. This leads to more consistent product quality and reduced operational costs, directly influencing market competitiveness and supply stability.

Furthermore, AI-driven analytics can provide sophisticated demand forecasting models for petroleum pitch, allowing manufacturers to align production capacities with market needs more precisely, reducing inventory risks and optimizing logistics. In research and development, AI is accelerating the discovery and formulation of new pitch grades with enhanced properties for novel applications, such as advanced composites or energy storage, by simulating molecular interactions and predicting material performance. This intelligent approach fosters innovation and opens new market segments for petroleum pitch.

- Enhanced efficiency and yield optimization in petroleum pitch production processes through predictive analytics.

- AI-powered demand forecasting leading to improved supply chain management and inventory control.

- Acceleration of research and development for novel pitch grades and applications via AI-driven material science.

- Improved quality control and consistency of petroleum pitch properties using machine learning algorithms.

- Optimization of energy consumption and reduction of environmental footprint in manufacturing facilities.

Key Takeaways Petroleum Pitch Market Size & Forecast

The petroleum pitch market is set for robust expansion over the forecast period, primarily propelled by the accelerating growth of next-generation industries like electric vehicle batteries and advanced composite materials. Its versatility as a carbon precursor and binder makes it indispensable for applications demanding high thermal stability, electrical conductivity, and mechanical strength. The market’s trajectory is intrinsically linked to global industrial output and technological advancements that unlock new functionalities for this crucial material.

Regional dynamics, particularly the rapid industrialization in Asia Pacific, will significantly influence market growth, with countries like China and India leading in demand for both traditional and advanced applications. Furthermore, ongoing research into sustainable production methods and the development of tailored pitch grades will be critical for manufacturers to capitalize on emerging opportunities and navigate evolving regulatory landscapes. Strategic investments in R&D and capacity expansion are anticipated to be key drivers for market participants aiming to secure a competitive advantage.

- The market's substantial growth is primarily driven by surging demand from the electric vehicle (EV) battery and carbon fiber sectors.

- Petroleum pitch maintains critical importance in traditional industries, including aluminum smelting and graphite electrode manufacturing.

- Continuous technological innovation, particularly in customizing pitch properties, is crucial for market expansion into new high-value applications.

- The Asia Pacific region is expected to remain the dominant market due to extensive industrialization and infrastructure development.

- A growing focus on sustainability and circular economy principles is influencing production methods and supply chain decisions across the industry.

Petroleum Pitch Market Drivers Analysis

The expansion of the petroleum pitch market is significantly influenced by several key drivers, each contributing to its sustained growth across diverse industrial sectors. A primary driver is the burgeoning demand for lightweight and high-strength materials, particularly carbon fibers, which heavily rely on petroleum pitch as a critical precursor. These advanced materials are increasingly adopted in industries such as aerospace, automotive, and wind energy, owing to their superior performance characteristics and contribution to fuel efficiency and structural integrity.

Another powerful catalyst is the rapid growth of the electric vehicle (EV) market. Petroleum pitch is a vital component in the manufacturing of anodes for lithium-ion batteries, which power EVs. As global commitments to decarbonization intensify and consumer adoption of EVs accelerates, the demand for petroleum pitch in battery production is projected to surge considerably. Furthermore, continued expansion in traditional sectors like aluminum smelting and steel manufacturing, where pitch is essential for graphite electrode and anode production, provides a stable foundation for market growth, particularly in industrializing economies.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Carbon Fiber Production | +1.2% | North America, Europe, Asia Pacific | Mid-to-Long Term |

| Rising Demand for EV Battery Anodes | +1.5% | Asia Pacific (China, South Korea), Europe, North America | Short-to-Long Term |

| Expansion of Aluminum and Steel Industries | +0.8% | Asia Pacific (China, India), Latin America | Mid-to-Long Term |

| Increased Infrastructure Development | +0.7% | Asia Pacific, Latin America, Middle East & Africa | Mid-to-Long Term |

| Technological Advancements in Pitch Modification | +0.6% | Global | Mid-to-Long Term |

Petroleum Pitch Market Restraints Analysis

Despite its significant applications, the petroleum pitch market faces several restraints that could temper its growth trajectory. One primary concern is the inherent volatility of crude oil prices, which directly impacts the cost of feedstock for petroleum pitch production. Fluctuations in crude oil markets can lead to unpredictable production costs, affecting manufacturers' profitability and pricing strategies, thereby introducing market instability and hindering long-term investment planning.

Environmental regulations and a growing global emphasis on sustainability also pose considerable challenges. The production and use of petroleum pitch, derived from fossil fuels, can be associated with greenhouse gas emissions and other environmental concerns. Stricter regulations regarding emissions, waste management, and resource utilization may necessitate costly process upgrades and could favor alternative, greener materials in some applications, thereby restraining market expansion. Furthermore, health and safety concerns associated with handling and processing certain grades of pitch, particularly those with higher polycyclic aromatic hydrocarbon (PAH) content, can lead to increased operational costs and regulatory scrutiny.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility of Crude Oil Prices | -0.9% | Global | Short-to-Mid Term |

| Stringent Environmental Regulations | -0.7% | Europe, North America, Asia Pacific (China) | Mid-to-Long Term |

| Competition from Alternative Materials | -0.5% | Global | Mid-to-Long Term |

| Health and Safety Concerns (PAH content) | -0.4% | Europe, North America | Short-to-Mid Term |

Petroleum Pitch Market Opportunities Analysis

The petroleum pitch market presents numerous opportunities for growth and diversification, driven by ongoing research and evolving industrial needs. A significant opportunity lies in the development of advanced pitch grades tailored for emerging applications, such as high-performance battery components beyond traditional anodes, including solid-state electrolytes or new electrode architectures. Innovations in material science are enabling the creation of pitch-derived materials with superior electrical, thermal, and mechanical properties, opening doors to highly specialized, high-value markets.

Furthermore, the increasing focus on the circular economy and sustainable industrial practices offers avenues for innovation in bio-pitch development or the valorization of pitch byproducts. Exploring methods to produce pitch from renewable sources or to enhance the environmental profile of existing production processes could significantly expand market reach and appeal, particularly in regions with stringent environmental policies. The growing demand for advanced composite materials in lightweighting initiatives across automotive and aerospace sectors also represents a substantial opportunity, pushing for higher quality and more specialized petroleum pitch precursors for carbon fiber manufacturing.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of New High-Performance Pitch Grades | +1.1% | Global | Mid-to-Long Term |

| Expansion in Energy Storage Applications (beyond anodes) | +1.0% | Asia Pacific, North America, Europe | Mid-to-Long Term |

| R&D in Sustainable/Bio-Based Pitch Alternatives | +0.8% | Europe, North America | Long Term |

| Untapped Markets in Developing Economies | +0.7% | Latin America, Middle East & Africa | Mid-to-Long Term |

Petroleum Pitch Market Challenges Impact Analysis

The petroleum pitch market faces several notable challenges that could impede its growth and operational efficiency. One significant challenge is the technical complexity associated with consistently producing pitch grades with precise specifications required for high-end applications like carbon fibers and advanced battery materials. Achieving uniform molecular structure and purity, while managing variations in crude feedstock composition, demands sophisticated refining technologies and rigorous quality control, which can be capital-intensive and technically demanding for manufacturers.

Another considerable hurdle is navigating the ever-evolving landscape of environmental regulations and public scrutiny regarding petrochemical products. Industries are under increasing pressure to reduce carbon footprints and adhere to stricter emissions standards, which can necessitate substantial investments in new technologies and compliance measures for pitch producers. Furthermore, competition from alternative materials, such as coal tar pitch or synthetic graphite for specific applications, can present a market challenge, compelling petroleum pitch manufacturers to continuously innovate and differentiate their products based on performance and cost-effectiveness. Ensuring a stable and cost-effective supply chain for feedstock, especially in periods of geopolitical instability or supply disruptions, also remains a persistent operational challenge.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technical Complexity in Achieving Specific Pitch Properties | -0.8% | Global | Mid-to-Long Term |

| Increasing Environmental Compliance Costs | -0.7% | Europe, North America | Short-to-Mid Term |

| Feedstock Supply Chain Volatility & Geopolitical Risks | -0.6% | Global | Short-to-Mid Term |

| Intense Competition from Substitute Materials | -0.5% | Global | Mid-to-Long Term |

Petroleum Pitch Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global petroleum pitch market, encompassing its size, growth trends, segmentation, and competitive landscape. The scope includes a detailed examination of market drivers, restraints, opportunities, and challenges influencing industry dynamics, along with a forward-looking forecast from 2025 to 2033. Special attention is given to the impact of artificial intelligence and regional market variations, offering stakeholders actionable insights for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.8 Billion |

| Market Forecast in 2033 | USD 8.2 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ExxonMobil Corporation, Shell plc, TotalEnergies SE, BP p.l.c., Reliance Industries Limited, Mitsubishi Chemical Corporation, Nippon Steel Chemical & Material Co., Ltd., Indian Oil Corporation Ltd., Valero Energy Corporation, Phillips 66 Company, Sinopec Corp., China National Petroleum Corporation (CNPC), Sumitomo Chemical Co., Ltd., Arkema S.A., Eastman Chemical Company, BASF SE, LyondellBasell Industries N.V., Chevron Phillips Chemical Company LLC, Marathon Petroleum Corporation, ENI S.p.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The petroleum pitch market is extensively segmented by type, application, and region to provide a granular view of its diverse dynamics and growth opportunities. This detailed segmentation allows for a comprehensive understanding of how different product grades and end-use industries contribute to the overall market landscape, enabling stakeholders to identify specific areas of high growth potential and tailor their strategies accordingly. Each segment is influenced by distinct demand patterns, technological requirements, and regional economic conditions.

- By Type:

- Softening Point Below 60°C: Primarily used in applications where lower viscosity is required, such as some binders, protective coatings, and as a component in certain construction materials. Its lower softening point makes it more amenable to processes requiring fluidity at ambient or slightly elevated temperatures.

- Softening Point 60°C-90°C: This medium-grade pitch is versatile and finds extensive use in roofing, paving, and general-purpose binders. It offers a balance between fluidity and structural integrity, making it suitable for a wide range of industrial and construction applications. This segment benefits from infrastructure development projects globally.

- Softening Point Above 90°C: Known as hard pitch, this type is critical for high-performance applications requiring superior carbon yield, thermal stability, and mechanical strength. It is predominantly used as a precursor for carbon fibers, graphite electrodes, and in advanced refractory materials. Demand for this segment is strongly tied to the growth of aerospace, automotive, and specialized metallurgical industries.

- By Application:

- Aluminum Smelting: Petroleum pitch serves as a crucial binder for carbon anodes in the aluminum smelting process, contributing to the structural integrity and electrical conductivity required for efficient electrolysis. This is a traditional and significant application segment.

- Graphite Electrodes: Essential for electric arc furnaces (EAFs) in steel production, petroleum pitch acts as a binder in the manufacture of graphite electrodes, providing high carbon content and thermal stability. The growth of EAF steelmaking drives demand in this area.

- Carbon Fibers: Petroleum pitch is a primary precursor for pitch-based carbon fibers, which are valued for their high modulus, thermal conductivity, and economic viability. These fibers are increasingly used in aerospace, automotive, and sporting goods.

- Refractories: In the refractory industry, pitch is used as a binder and impregnant for carbon-containing refractories, enhancing their resistance to high temperatures and chemical attack in various industrial furnaces.

- Construction (Roofing, Paving): Medium and soft grades of petroleum pitch are utilized in roofing felts, damp-proofing, and road paving applications, contributing to water resistance and durability in civil engineering projects.

- Binders and Adhesives: Beyond specific applications, pitch finds general use as a binding agent in various industrial contexts, including abrasives, foundry cores, and briquetting, owing to its adhesive properties.

- Specialty Chemicals: Petroleum pitch can be processed further to extract or synthesize specialty chemicals, including some aromatics and carbon black precursors, catering to niche industrial requirements.

- Others: This segment includes miscellaneous applications such as sealants, insulating compounds, and as a raw material for certain carbon products not covered in the primary categories.

Regional Highlights

The global petroleum pitch market exhibits significant regional variations, influenced by industrial development, technological adoption, and regulatory landscapes. Each major geographical segment contributes uniquely to the market's overall dynamics, presenting distinct opportunities and challenges for market participants.

- North America: The North American market for petroleum pitch is characterized by mature industrial sectors and a strong focus on high-performance materials. Demand is driven by aerospace, automotive (including the growing EV sector), and advanced manufacturing. Strict environmental regulations encourage innovation in cleaner production methods and the development of specialized pitch grades. The region also sees significant R&D activities aimed at exploring new applications for carbon-based materials.

- Europe: Europe represents a key market with robust demand from its advanced manufacturing base, particularly in the automotive, aerospace, and renewable energy sectors. The region is a leader in carbon fiber production and advanced battery technology research. However, stringent environmental policies and a strong emphasis on sustainability are pushing manufacturers towards more eco-friendly processes and potentially bio-based alternatives, influencing market trends and investment priorities.

- Asia Pacific (APAC): APAC stands as the largest and fastest-growing market for petroleum pitch, primarily due to rapid industrialization, burgeoning infrastructure development, and substantial investments in manufacturing capabilities across countries like China, India, Japan, and South Korea. The region is a major hub for aluminum smelting, steel production, and the manufacturing of electric vehicles and related components, leading to immense demand for pitch in graphite electrodes, anodes, and carbon fiber precursors. Economic growth and urbanization continue to fuel consumption in construction and paving applications.

- Latin America: The Latin American market is experiencing steady growth, driven by increasing industrial output, particularly in metals and construction sectors. Countries like Brazil and Argentina are witnessing infrastructure development and expansion in their industrial bases, contributing to the demand for petroleum pitch in traditional applications. The region also holds potential for future growth in advanced materials as industrial capabilities mature.

- Middle East & Africa (MEA): The MEA region, particularly the GCC countries, is a significant producer of petroleum feedstocks and is increasingly focusing on diversifying its economy through downstream industries. Investments in petrochemical complexes and manufacturing capabilities are expected to drive demand for petroleum pitch in various applications, including aluminum production and construction. Africa's ongoing industrialization and infrastructure projects also contribute to the region's market potential.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Petroleum Pitch Market.- ExxonMobil Corporation

- Shell plc

- TotalEnergies SE

- BP p.l.c.

- Reliance Industries Limited

- Mitsubishi Chemical Corporation

- Nippon Steel Chemical & Material Co., Ltd.

- Indian Oil Corporation Ltd.

- Valero Energy Corporation

- Phillips 66 Company

- Sinopec Corp.

- China National Petroleum Corporation (CNPC)

- Sumitomo Chemical Co., Ltd.

- Arkema S.A.

- Eastman Chemical Company

- BASF SE

- LyondellBasell Industries N.V.

- Chevron Phillips Chemical Company LLC

- Marathon Petroleum Corporation

- ENI S.p.A.

Frequently Asked Questions

What is petroleum pitch used for?

Petroleum pitch is a versatile carbon-rich material primarily used as a binder for aluminum smelting anodes and graphite electrodes. It is also a critical precursor for carbon fibers, utilized in aerospace and automotive industries, and finds applications in refractories, roofing, paving, and specialty chemicals.

How is petroleum pitch produced?

Petroleum pitch is typically a residual byproduct obtained from the high-temperature distillation or thermal cracking of petroleum fractions, particularly heavy oils or residues from crude oil refining. The specific properties of the pitch depend on the feedstock and the processing conditions.

What are the primary drivers of the petroleum pitch market growth?

Key drivers include the surging demand for carbon fibers in lightweight applications, the rapid expansion of the electric vehicle (EV) battery market for anode materials, and continued growth in the aluminum and steel industries for electrode production. Infrastructure development also plays a significant role.

What are the key challenges facing the petroleum pitch market?

Challenges encompass the volatility of crude oil prices, which impacts feedstock costs, stringent environmental regulations requiring significant compliance investments, technical complexities in achieving precise pitch specifications for high-end uses, and competition from alternative materials.

How does AI impact the petroleum pitch industry?

AI enhances efficiency in refinery operations, optimizes pitch production yields, and improves quality control through predictive analytics. It also aids in sophisticated demand forecasting, supply chain optimization, and accelerates research and development for new pitch grades and applications.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted