Speed Reducer Market

Speed Reducer Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708488 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

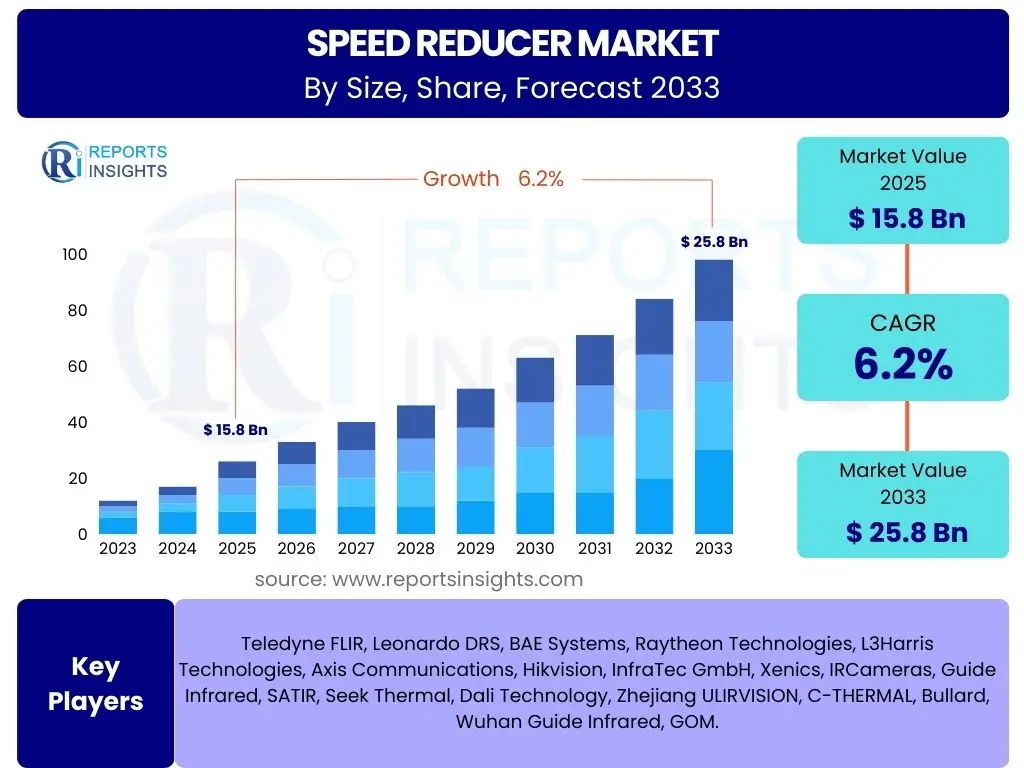

Speed Reducer Market Size

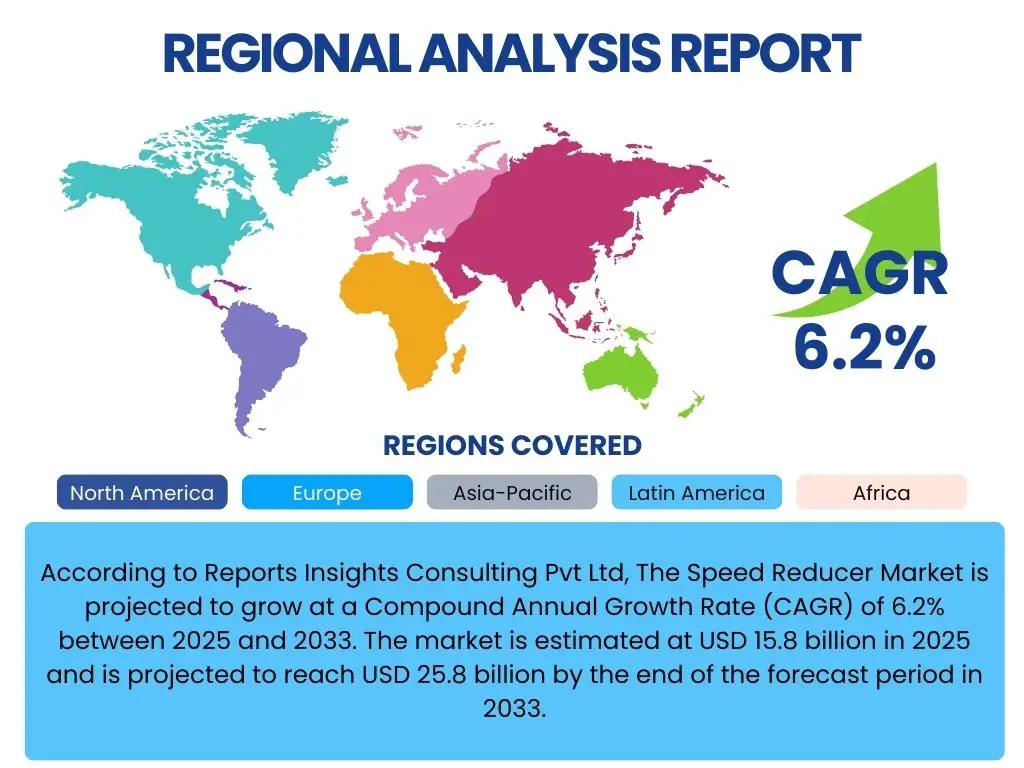

According to Reports Insights Consulting Pvt Ltd, The Speed Reducer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% between 2025 and 2033. The market is estimated at USD 15.8 billion in 2025 and is projected to reach USD 25.8 billion by the end of the forecast period in 2033.

Key Speed Reducer Market Trends & Insights

Current market analyses indicate a strong user interest in how speed reducer technology is evolving to meet modern industrial demands. Common inquiries highlight the integration of smart features, the drive for enhanced energy efficiency, and the adoption of more compact and modular designs. Users are also keenly observing the impact of advanced manufacturing techniques and the push for sustainable solutions within the speed reducer sector, emphasizing factors like material innovation and extended product lifecycles.

There is a discernible shift towards solutions that offer higher power density and reduced maintenance requirements, reflecting industries' need for greater operational efficiency and lower total cost of ownership. The burgeoning demand for customized solutions, particularly in specialized applications like robotics and renewable energy, underscores the market's move away from one-size-fits-all products. Furthermore, the increasing complexity of automation systems necessitates speed reducers that can integrate seamlessly with sophisticated control mechanisms, driving innovation in sensor integration and communication capabilities.

- Growing adoption of intelligent and connected speed reducers for predictive maintenance.

- Emphasis on energy-efficient designs to reduce operational costs and environmental impact.

- Increasing demand for compact, lightweight, and modular speed reducer solutions.

- Integration with Industry 4.0 and IoT for enhanced monitoring and control.

- Development of advanced materials for improved durability and performance.

- Rising customization requirements for specific industrial applications.

- Expansion of applications in robotics, automation, and renewable energy sectors.

AI Impact Analysis on Speed Reducer

User questions related to the impact of AI on the Speed Reducer market frequently revolve around its potential to revolutionize design, manufacturing, and operational processes. The primary themes emerging from these queries include the application of AI for predictive analytics in maintenance, optimizing performance parameters, and enhancing quality control throughout the production lifecycle. There is significant interest in how AI can contribute to more efficient energy consumption and the extension of equipment lifespan through intelligent monitoring.

Furthermore, stakeholders are exploring AI's role in accelerating the design phase, enabling rapid prototyping, and simulating diverse operating conditions to develop more robust and application-specific speed reducer solutions. The potential for AI to drive smarter automation in manufacturing facilities, from assembly to testing, is also a key area of discussion. While the benefits are clear, concerns regarding data security, the need for specialized skills, and the initial investment in AI infrastructure are also part of the broader conversation among market participants.

The integration of AI algorithms with sensor data from speed reducers promises to transform maintenance strategies from reactive to proactive, minimizing downtime and maximizing asset utilization. This not only enhances operational efficiency but also offers significant cost savings over the equipment's lifespan. AI-driven optimization can also fine-tune operational parameters in real-time, adapting to varying loads and environmental conditions, thereby ensuring peak performance and extended durability.

- Predictive maintenance through AI algorithms analyzing operational data.

- Optimization of speed reducer design and manufacturing processes using machine learning.

- Enhanced quality control and fault detection through AI-powered vision systems.

- Real-time performance monitoring and adaptive control for energy efficiency.

- Automated diagnostics and troubleshooting to reduce downtime.

- Facilitating the development of smart, self-optimizing speed reducer systems.

- Improved supply chain management and inventory optimization.

Key Takeaways Speed Reducer Market Size & Forecast

Analysis of user questions regarding the Speed Reducer market size and forecast reveals a consistent focus on understanding the primary growth catalysts and potential investment avenues. Users are particularly interested in identifying the sectors that will drive the most significant demand and the geographical regions expected to exhibit robust growth. The insights gathered suggest a strong emphasis on the long-term viability of the market, exploring how current technological advancements and industrial shifts will influence future market trajectory and revenue generation.

Moreover, inquiries often touch upon the impact of macroeconomic factors, regulatory landscapes, and the competitive environment on market expansion. Stakeholders seek clarity on market segmentation, pinpointing which types of speed reducers or end-use applications will offer the most lucrative opportunities over the forecast period. The overall sentiment indicates a strategic lookout for sustainable growth paths and effective risk mitigation strategies within this dynamic industrial component sector.

The consistent growth projected for the speed reducer market underscores its indispensable role in industrial automation and manufacturing across diverse sectors. Key takeaways highlight the critical importance of embracing technological advancements, particularly in smart and energy-efficient designs, to capitalize on emerging opportunities. Furthermore, understanding regional industrialization trends and adapting to evolving end-user demands will be paramount for market players seeking sustained success and competitive advantage throughout the forecast period.

- Robust growth anticipated, driven by increasing industrial automation and manufacturing expansion.

- Significant market potential in emerging economies and developing industrial sectors.

- Technological innovation, especially in smart and energy-efficient designs, will be crucial for competitive advantage.

- Diversification into high-growth applications like robotics and renewable energy offers lucrative opportunities.

- Strategic partnerships and mergers & acquisitions are key for market expansion and technology acquisition.

Speed Reducer Market Drivers Analysis

The speed reducer market is significantly propelled by the global surge in industrial automation across various manufacturing sectors. Industries are increasingly adopting automated systems to enhance productivity, precision, and operational efficiency, which directly fuels the demand for high-performance speed reducers essential for precise motion control. Furthermore, the expansion of the manufacturing sector, particularly in emerging economies, contributes substantially to market growth, as new production facilities and machinery require robust and reliable power transmission components.

A growing emphasis on energy efficiency and sustainable manufacturing practices also acts as a key driver. Modern speed reducers are designed to minimize energy loss, aligning with stringent environmental regulations and corporate sustainability goals, thereby appealing to a broader industrial customer base. The continuous innovation in product design, offering compact, lightweight, and higher power density solutions, further expands their application scope across diverse industries including robotics, material handling, and automotive.

The increasing demand from the renewable energy sector, especially in wind turbines and solar tracking systems, presents another substantial driver for specialized speed reducers capable of handling heavy loads and extreme environmental conditions. Additionally, ongoing infrastructure development projects globally, particularly in construction and mining, necessitate heavy-duty speed reducers for various machinery, ensuring consistent market demand. These combined factors create a fertile ground for sustained market expansion over the forecast period.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Industrial Automation | +1.8% | Global, particularly APAC (China, India), North America, Europe | Short to Long Term (2025-2033) |

| Expansion of Manufacturing Sector | +1.5% | APAC, Latin America, Middle East & Africa | Medium to Long Term (2026-2033) |

| Demand for Energy-Efficient Solutions | +1.2% | Europe, North America, Japan | Short to Medium Term (2025-2030) |

| Rising Adoption in Robotics and Renewable Energy | +1.0% | North America, Europe, China | Medium to Long Term (2027-2033) |

| Infrastructure Development Projects | +0.7% | Emerging Economies, Africa, Southeast Asia | Medium to Long Term (2027-2033) |

Speed Reducer Market Restraints Analysis

Despite robust growth, the speed reducer market faces several significant restraints that could impede its expansion. One primary challenge is the high initial investment cost associated with advanced and specialized speed reducer units, particularly those designed for high-precision or heavy-duty applications. This cost factor can be a barrier for small and medium-sized enterprises (SMEs) or industries with limited capital expenditure, leading them to opt for less sophisticated or older technologies.

Another restraint stems from intense market competition, characterized by the presence of numerous global and regional players. This competitive landscape often leads to pricing pressures and reduced profit margins, making it difficult for manufacturers to invest heavily in research and development for innovative solutions. Furthermore, the market is vulnerable to fluctuating raw material prices, such as steel, aluminum, and specialized alloys, which directly impact production costs and, consequently, the final product pricing.

Technological obsolescence also poses a restraint, as rapid advancements in motor and drive technologies can sometimes reduce the need for certain types of traditional speed reducers, or necessitate significant redesigns and investments to remain competitive. Global economic slowdowns or uncertainties can also dampen industrial investment, affecting demand for new machinery and, by extension, speed reducers. These factors collectively require manufacturers to adopt agile strategies to navigate market challenges.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment Costs | -1.3% | Global, particularly SMEs in developing regions | Short to Medium Term (2025-2030) |

| Intense Market Competition and Pricing Pressure | -1.0% | Global, all major manufacturing hubs | Short to Long Term (2025-2033) |

| Fluctuations in Raw Material Prices | -0.8% | Global supply chains, all manufacturing regions | Short Term (2025-2027) |

| Technological Obsolescence and Product Development Cycles | -0.6% | Developed Markets (Europe, North America, Japan) | Medium Term (2027-2031) |

Speed Reducer Market Opportunities Analysis

The speed reducer market is rich with emerging opportunities driven by several transformative trends and evolving industrial needs. One significant area of opportunity lies in the development of highly customized and application-specific speed reducers, particularly for specialized industries such as robotics, aerospace, and medical equipment. As these sectors demand increasingly precise and compact solutions, manufacturers capable of delivering tailored designs stand to gain a substantial competitive edge.

Furthermore, the rapid expansion of Industry 4.0 and the Internet of Things (IoT) presents a robust opportunity for integrating smart features into speed reducers. This includes incorporating sensors for real-time monitoring, predictive maintenance capabilities, and seamless connectivity with broader industrial control systems. Such intelligent speed reducers offer enhanced operational efficiency and reduced downtime, appealing to forward-thinking industries seeking to optimize their production processes.

The burgeoning markets in developing regions, fueled by rapid industrialization and infrastructure development, offer immense potential for market penetration and growth. Countries in Asia Pacific, Latin America, and Africa are increasingly investing in manufacturing and automation, creating a strong demand for cost-effective yet reliable speed reducer solutions. Additionally, the growing focus on renewable energy, particularly in wind power generation, requires specialized, high-torque, and durable gearboxes, presenting a niche but highly lucrative segment for innovation and market expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Customization for Niche Applications (Robotics, Aerospace) | +1.5% | Global, particularly developed economies | Medium to Long Term (2027-2033) |

| Integration with IoT and Industry 4.0 Technologies | +1.3% | North America, Europe, East Asia | Short to Long Term (2025-2033) |

| Untapped Markets in Developing Economies | +1.0% | APAC (India, Southeast Asia), Latin America, Africa | Medium to Long Term (2026-2033) |

| Growth in Renewable Energy Sector (Wind Turbines) | +0.9% | Europe, North America, China, India | Medium to Long Term (2027-2033) |

Speed Reducer Market Challenges Impact Analysis

The speed reducer market faces several critical challenges that demand strategic responses from manufacturers. One significant challenge is the ongoing need to differentiate products in a highly competitive market, where many players offer similar solutions. Achieving effective product differentiation often requires substantial investment in research and development to introduce innovative features, superior performance, or specialized designs that justify premium pricing and attract specific customer segments, which can be a difficult undertaking.

Maintaining competitive pricing while simultaneously upholding high-quality standards and integrating advanced technologies presents another formidable challenge. Manufacturers must strike a delicate balance between cost-effectiveness and innovation, especially when facing pressure from low-cost alternatives, without compromising on reliability and durability. This is exacerbated by the complexity of global supply chains, which are prone to disruptions from geopolitical events, natural disasters, and pandemics, leading to material shortages and increased logistics costs.

Furthermore, the industry is grappling with a shortage of skilled labor, particularly technicians and engineers proficient in designing, manufacturing, and maintaining advanced speed reducer systems. This talent gap can hinder production efficiency, slow down innovation, and increase operational expenses. Adhering to diverse and evolving international regulatory standards for safety, environmental impact, and energy efficiency across various markets also adds a layer of complexity and cost for manufacturers, requiring continuous adaptation and compliance efforts.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Product Differentiation in a Highly Competitive Market | -1.1% | Global, particularly mature markets | Short to Long Term (2025-2033) |

| Maintaining Competitive Pricing and Profit Margins | -1.0% | Global, all regions with manufacturing presence | Short to Long Term (2025-2033) |

| Supply Chain Disruptions and Raw Material Volatility | -0.9% | Global, interconnected economies | Short to Medium Term (2025-2029) |

| Shortage of Skilled Labor and Technical Expertise | -0.7% | North America, Europe, Japan, and other industrialized nations | Medium to Long Term (2027-2033) |

| Adherence to Evolving Regulatory and Environmental Standards | -0.5% | Europe, North America, specific Asian countries | Long Term (2028-2033) |

Speed Reducer Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Speed Reducer market, covering historical data, current market trends, and future growth projections from 2025 to 2033. The scope includes detailed segmentation by type, application, and end-use industry, alongside a thorough regional analysis. It assesses key market drivers, restraints, opportunities, and challenges, offering strategic insights for stakeholders. The report also features a competitive landscape analysis, profiling leading companies and their strategic initiatives, alongside an impact analysis of artificial intelligence on the market dynamics.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.8 Billion |

| Market Forecast in 2033 | USD 25.8 Billion |

| Growth Rate | 6.2% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Siemens AG, SEW-EURODRIVE GmbH & Co KG, Bonfiglioli Riduttori S.p.A., ABB Ltd., Dana Incorporated, Eaton Corporation, Sumitomo Heavy Industries, Ltd., Cone Drive Operations Inc., Renold plc, NORD DRIVESYSTEMS, WEG S.A., Kumera Corporation, Varvel S.p.A., Flender GmbH, Brevini Power Transmission S.p.A., Zambello Riduttori Srl, Rossi S.p.A., Elecon Engineering Company Limited, China High-Speed Gear Industry Company Limited (CHF), Hangzhou Advance Gearbox Group Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The speed reducer market is extensively segmented to reflect the diverse range of product types, their applications across various industrial processes, and the broad spectrum of end-use industries. This detailed segmentation allows for a granular understanding of market dynamics, identifying specific growth pockets and technological preferences. The variety of speed reducer types addresses distinct power transmission requirements, while their applications span from heavy-duty material handling to precision robotics, showcasing the versatility and critical nature of these components in modern industrial setups. The end-use industry segmentation further clarifies demand patterns, illustrating how sector-specific needs drive innovation and adoption rates.

- By Type:

- Worm Gear Reducer

- Helical Gear Reducer

- Bevel Helical Gear Reducer

- Planetary Gear Reducer

- Cycloidal Gear Reducer

- Shaft Mounted Gear Reducer (SMSR)

- Others (Spur Gear Reducer, Hypoid Gear Reducer)

- By Application:

- Material Handling Equipment

- Industrial Machinery

- Robotics and Automation

- Wind Turbines

- Automotive Industry

- Mining and Construction

- Food and Beverage Processing

- Chemical and Petrochemical

- Others (Textile, Agriculture)

- By End-Use Industry:

- Manufacturing

- Power Generation

- Automotive

- Construction

- Mining

- Food & Beverage

- Chemicals

- Metals & Heavy Industry

- Logistics & Warehousing

- Agriculture

- Marine

- Healthcare & Pharmaceuticals

Regional Highlights

- North America: This region is a mature market characterized by advanced manufacturing capabilities and a strong emphasis on automation and robotics. The demand is driven by upgrades in existing infrastructure and the adoption of smart factory initiatives. Key sectors include automotive, aerospace, and general manufacturing, focusing on high-efficiency and high-precision speed reducers. The presence of major industry players and robust R&D activities also contributes significantly to market growth and innovation.

- Europe: Europe represents a significant market, known for its stringent quality standards, technological innovation, and strong focus on energy efficiency and sustainability. Countries like Germany, Italy, and France are hubs for advanced industrial machinery and automotive production. The region's commitment to Industry 4.0 and renewable energy projects (especially wind power) creates substantial demand for high-performance and specialized speed reducers.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, fueled by rapid industrialization, expanding manufacturing bases (especially in China, India, and Southeast Asia), and increasing investments in infrastructure development. The region's growth is driven by a surge in demand for affordable automation solutions, coupled with an increasing focus on adopting advanced technologies in automotive, electronics, and heavy industries.

- Latin America: This region shows steady growth, primarily influenced by industrialization in countries like Brazil and Mexico, coupled with expanding mining and agricultural sectors. Investments in infrastructure and an increasing focus on local manufacturing capabilities are driving the demand for speed reducers, particularly in material handling and processing applications.

- Middle East and Africa (MEA): The MEA region is witnessing growth driven by diversification efforts from oil-dependent economies into manufacturing and infrastructure, alongside significant investments in mining and construction projects. Emerging industrial hubs and increasing automation in various sectors are creating new opportunities for speed reducer manufacturers, though market penetration rates vary across the region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Speed Reducer Market.- Siemens AG

- SEW-EURODRIVE GmbH & Co KG

- Bonfiglioli Riduttori S.p.A.

- ABB Ltd.

- Dana Incorporated

- Eaton Corporation

- Sumitomo Heavy Industries, Ltd.

- Cone Drive Operations Inc.

- Renold plc

- NORD DRIVESYSTEMS

- WEG S.A.

- Kumera Corporation

- Varvel S.p.A.

- Flender GmbH

- Brevini Power Transmission S.p.A.

- Zambello Riduttori Srl

- Rossi S.p.A.

- Elecon Engineering Company Limited

- China High-Speed Gear Industry Company Limited (CHF)

- Hangzhou Advance Gearbox Group Co., Ltd.

Frequently Asked Questions

Analyze common user questions about the Speed Reducer market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Speed Reducer Market?

The Speed Reducer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% between 2025 and 2033, reaching an estimated value of USD 25.8 billion by 2033.

Which factors are primarily driving the growth of the Speed Reducer Market?

The market is primarily driven by the increasing adoption of industrial automation, expansion of the global manufacturing sector, rising demand for energy-efficient solutions, and growing applications in robotics and renewable energy.

How is AI impacting the Speed Reducer industry?

AI is significantly impacting the speed reducer industry through predictive maintenance, optimized design and manufacturing processes, enhanced quality control, real-time performance monitoring, and the development of smart, self-optimizing systems.

Which regions are expected to show significant growth in the Speed Reducer Market?

The Asia Pacific (APAC) region is expected to exhibit the fastest growth due to rapid industrialization, expanding manufacturing bases, and significant infrastructure development, alongside steady growth in North America and Europe.

What are the key types of speed reducers available in the market?

Key types include Worm Gear Reducers, Helical Gear Reducers, Bevel Helical Gear Reducers, Planetary Gear Reducers, Cycloidal Gear Reducers, and Shaft Mounted Gear Reducers (SMSR), each catering to specific industrial power transmission requirements.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted