Semiconductor IP Market

Semiconductor IP Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703188 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

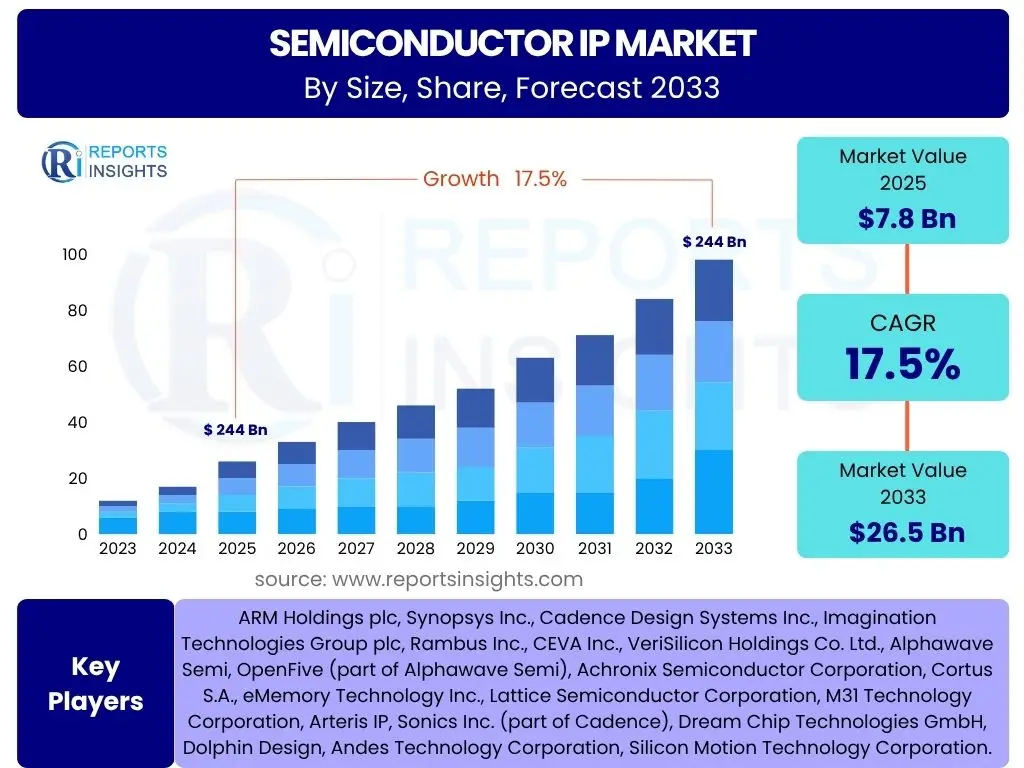

Semiconductor IP Market Size

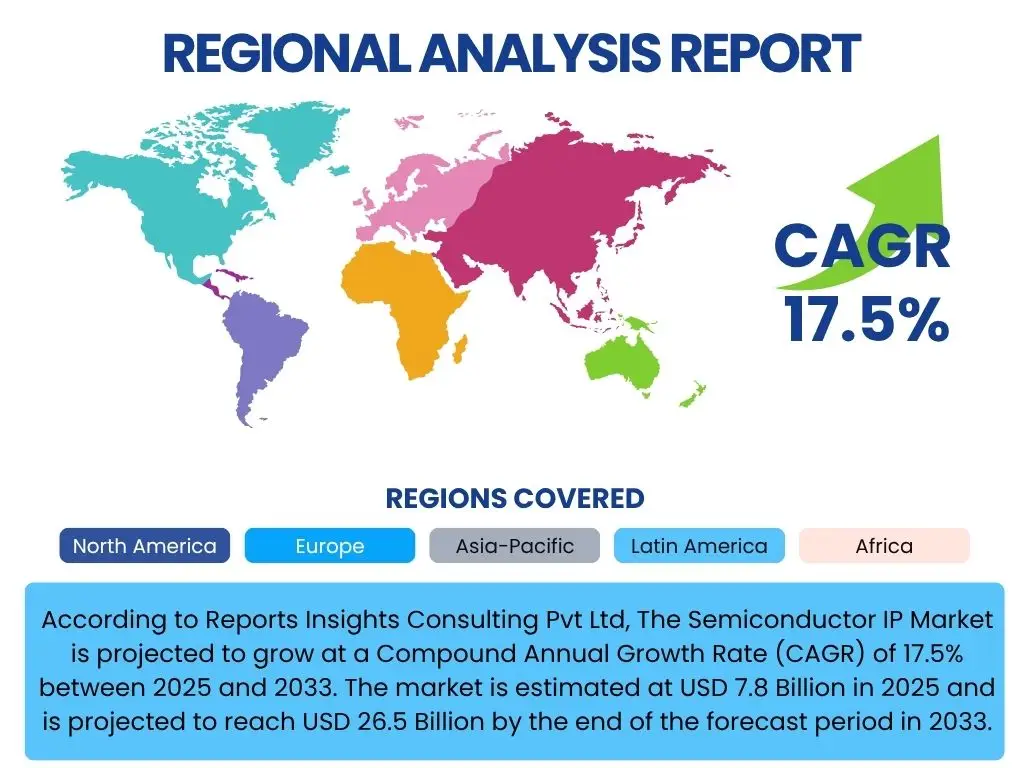

According to Reports Insights Consulting Pvt Ltd, The Semiconductor IP Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 17.5% between 2025 and 2033. The market is estimated at USD 7.8 Billion in 2025 and is projected to reach USD 26.5 Billion by the end of the forecast period in 2033.

Key Semiconductor IP Market Trends & Insights

The Semiconductor IP (Intellectual Property) market is currently experiencing significant transformative trends driven by the escalating demand for highly specialized and energy-efficient processing capabilities across various electronic devices and systems. User queries frequently revolve around the key technological shifts influencing chip design, such as the increasing integration of artificial intelligence and machine learning, the proliferation of the Internet of Things (IoT), and the strategic shift towards modular chip design approaches. These trends underscore a broader industry movement towards optimizing performance, reducing time-to-market, and managing the spiraling costs associated with advanced semiconductor manufacturing.

The market is increasingly influenced by the rise of open-source architectures like RISC-V, which offers a compelling alternative to proprietary instruction set architectures (ISAs), fostering innovation and customization. Additionally, the growing complexity of System-on-Chip (SoC) designs mandates the reuse of verified IP blocks, pushing semiconductor companies to license more diverse and sophisticated IP. This trend is further amplified by the ongoing miniaturization of electronic components and the need for enhanced security features embedded directly into hardware, making security IP a critically important and rapidly evolving segment of the market.

- Escalating demand for high-performance computing (HPC) and specialized accelerators for AI/ML workloads.

- Rapid adoption of chiplet architectures and heterogeneous integration to overcome Moore's Law limitations.

- Increasing proliferation of IoT devices driving demand for low-power, cost-effective, and secure IP.

- Emergence and growing influence of open-source processor architectures, particularly RISC-V.

- Heightened focus on hardware-level security IP to address growing cyber threats and ensure data integrity.

- Expansion of automotive electronics, necessitating robust, safety-certified, and high-reliability IP.

- Advanced packaging technologies are influencing how IP blocks are designed and integrated.

AI Impact Analysis on Semiconductor IP

Common user questions regarding AI's impact on Semiconductor IP frequently address how artificial intelligence itself is both a consumer of specialized IP and a catalyst for new IP development. Users are keen to understand the types of IP critical for AI workloads, such as Neural Processing Units (NPUs) and Graphics Processing Units (GPUs), and how AI algorithms are being leveraged to automate and optimize the IP design and verification processes. There is also significant interest in the long-term implications for IP licensing models and the emergence of entirely new categories of AI-centric IP.

AI's influence extends beyond merely driving demand for specific compute IP; it is fundamentally transforming the entire semiconductor design flow. AI is increasingly used in Electronic Design Automation (EDA) tools for tasks like design space exploration, power optimization, and complex verification, significantly reducing design cycles and costs. This paradigm shift necessitates IP that is not only optimized for AI applications but also compatible with AI-driven design methodologies. Furthermore, the push towards edge AI requires highly efficient, low-power AI IP solutions that can be integrated into a myriad of connected devices, expanding the market for specialized IP.

- Significant increase in demand for AI-specific processor IP, including NPUs, DSPs, and specialized accelerators.

- AI algorithms are revolutionizing EDA tools, improving IP design, verification, and optimization processes.

- New memory IP architectures are emerging to support AI workloads, such as in-memory computing and high-bandwidth memory (HBM).

- Growth of edge AI applications driving demand for low-power, efficient AI IP solutions.

- Increased complexity of AI models necessitates more sophisticated interconnect and interface IP.

- AI-driven IP validation and testing methodologies enhance reliability and performance.

- Development of neuromorphic and quantum computing IP for next-generation AI systems.

Key Takeaways Semiconductor IP Market Size & Forecast

Analysis of common user questions regarding key takeaways from the Semiconductor IP market size and forecast consistently points to the market's robust growth trajectory, driven by an insatiable demand for advanced computing capabilities across diverse end-use sectors. Users are primarily concerned with understanding the core drivers behind this expansion, the segments poised for the most significant growth, and the overall resilience of the market against potential economic headwinds. The insights reveal that the market's future is intrinsically linked to technological innovation and the pervasive digitalization transforming industries globally.

The forecast highlights that while traditional processor IP remains foundational, the most dynamic growth is anticipated in specialized IP blocks designed for emerging technologies such as Artificial Intelligence, 5G connectivity, autonomous systems, and the vast expanse of the Internet of Things. This indicates a strategic shift in investment and development towards IP that enables high-performance, low-power, and secure computing at both the edge and in the cloud. The sustained growth underscores the critical role of IP in facilitating faster time-to-market for complex SoCs and enabling companies to focus on differentiation rather than foundational design elements, cementing its indispensable nature in the modern semiconductor ecosystem.

- The Semiconductor IP market is projected for substantial growth, driven by digital transformation and emerging technologies.

- Specialized IP for AI, IoT, and 5G communications will be key growth accelerators.

- Increasing design complexity and cost pressure drive greater reliance on licensed IP.

- The market's expansion is global, with significant opportunities in Asia Pacific, North America, and Europe.

- Strategic partnerships and mergers & acquisitions among IP vendors are anticipated to consolidate market leadership.

- Hardware-level security and functional safety IP are becoming non-negotiable requirements across industries.

Semiconductor IP Market Drivers Analysis

The Semiconductor IP market is propelled by a confluence of technological advancements and increasing demands from various end-use industries. The proliferation of smart devices, the expansion of high-performance computing, and the critical need for energy efficiency are primary factors fueling the adoption of IP. As semiconductor designs become exponentially more complex and expensive, companies are increasingly turning to licensed IP blocks to accelerate development cycles, reduce design risks, and contain costs, thereby driving market expansion.

Furthermore, the relentless pursuit of miniaturization and integration in electronics necessitates the reuse of pre-verified, optimized IP cores. This trend is particularly evident in emerging sectors such as artificial intelligence, 5G wireless technology, and autonomous vehicles, all of which require highly specialized processing and connectivity solutions that are often best delivered through robust IP portfolios. The drive for innovation, coupled with the competitive pressure to quickly bring advanced products to market, firmly establishes these factors as significant drivers for the Semiconductor IP market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Proliferation of IoT and Connected Devices | +2.8% | Global | Short to Mid-term (2025-2029) |

| Increasing Adoption of AI/ML in Edge and Cloud | +3.5% | North America, APAC | Mid-term (2026-2033) |

| Rising Complexity of System-on-Chip (SoC) Designs | +2.2% | Global | Long-term (2025-2033) |

| Growth in Automotive Electronics and ADAS | +1.9% | Europe, APAC, North America | Mid-term (2026-2033) |

| Emergence of 5G Technology and Infrastructure | +1.7% | Global | Short to Mid-term (2025-2029) |

Semiconductor IP Market Restraints Analysis

Despite its significant growth potential, the Semiconductor IP market faces several restraints that could impede its expansion. One prominent challenge is the substantial upfront licensing costs associated with high-value IP blocks, which can be prohibitive for smaller companies or startups, limiting market access and innovation. Furthermore, the inherent complexities of integrating diverse IP blocks from multiple vendors into a single, cohesive SoC design often lead to extended verification cycles and potential compatibility issues, adding to development time and cost.

Another significant restraint involves intellectual property protection and the risk of piracy or unauthorized use, which remains a constant concern for IP vendors. The highly technical nature of IP and the specialized expertise required for its successful integration also contribute to a scarcity of skilled engineers, posing a bottleneck for market growth. Additionally, the cyclical nature of the semiconductor industry, with its inherent boom and bust periods, can introduce volatility into IP licensing revenues, impacting long-term investment and development strategies.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Licensing Costs and Royalties | -1.2% | Global, especially SMEs | Short-term (2025-2027) |

| Complexity of IP Integration and Verification | -1.3% | Global | Mid-term (2026-2030) |

| Concerns over IP Piracy and Security | -0.8% | Global | Ongoing |

| Dependency on Semiconductor Manufacturing Cycles | -0.7% | Global | Cyclic |

| Lack of Standardization Across IP Architectures | -0.6% | Global | Mid to Long-term (2027-2033) |

Semiconductor IP Market Opportunities Analysis

The Semiconductor IP market is ripe with opportunities, particularly stemming from the accelerating adoption of emerging technologies and the increasing sophistication of system designs. The open-source movement, exemplified by RISC-V, presents a significant avenue for growth by democratizing access to processor architecture, fostering innovation, and enabling greater customization for specialized applications. This trend not only expands the potential user base for IP but also encourages diverse IP core development and community collaboration.

Another compelling opportunity lies in the burgeoning market for chiplet-based designs and heterogeneous integration. As traditional monolithic chip scaling becomes more challenging and costly, breaking down complex SoCs into smaller, interconnected chiplets offers enhanced flexibility, improved yield, and optimized cost-performance ratios. This paradigm shift creates new demand for interface IP, inter-chip communication IP, and specialized management IP for heterogeneous systems, opening up substantial revenue streams for IP vendors focused on advanced packaging and modular design solutions. Furthermore, the expanding need for domain-specific accelerators across various industries presents a continuous opportunity for highly specialized and optimized IP cores.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of RISC-V Architecture Adoption | +2.5% | Global | Mid to Long-term (2026-2033) |

| Development of Chiplet and Heterogeneous Integration | +2.0% | North America, APAC | Mid-term (2027-2033) |

| Increasing Demand for Specialized IP (Neuromorphic, Quantum) | +1.8% | Research & Development Hubs | Long-term (2028-2033) |

| Expanding Use of IP in Data Centers and Cloud Infrastructure | +1.6% | North America, Europe | Mid-term (2025-2030) |

| Strategic Partnerships and Collaborations for IP Development | +1.0% | Global | Ongoing |

Semiconductor IP Market Challenges Impact Analysis

The Semiconductor IP market, while dynamic, faces several significant challenges that could affect its growth trajectory and stability. One of the primary obstacles is the persistent shortage of highly skilled IP design engineers and verification experts. The intricate nature of advanced IP development and integration demands specialized knowledge that is not readily available, leading to talent gaps and increased recruitment costs for companies in the sector. This shortage can slow down innovation and delay time-to-market for new IP solutions.

Another crucial challenge is the rapid pace of technological obsolescence. As semiconductor technology evolves at an unprecedented rate, IP cores designed for previous process nodes or architectural paradigms can quickly become outdated, requiring continuous investment in research and development to maintain relevance. This necessitates significant financial outlays and strategic foresight from IP vendors to ensure their portfolios remain cutting-edge. Furthermore, the complexity of intellectual property litigation and the need for robust legal frameworks to protect IP rights across diverse global jurisdictions remain a persistent concern, adding layers of risk and cost to market participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Shortage of Skilled IP Design and Verification Engineers | -1.4% | Global | Ongoing |

| Rapid Technological Obsolescence and Need for Constant R&D | -0.9% | Global | Short to Mid-term (2025-2029) |

| Intellectual Property Protection and Litigation Risks | -0.7% | Global | Ongoing |

| Need for Standardized Interfaces and Protocols | -0.6% | Global | Mid-term (2026-2031) |

| High Costs Associated with Advanced Process Node Migration | -0.8% | Global | Long-term (2027-2033) |

Semiconductor IP Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Semiconductor IP market, encompassing historical data, current market dynamics, and future projections. The scope includes a detailed examination of market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. The report is designed to offer actionable insights for stakeholders, enabling informed strategic decision-making within the evolving semiconductor ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 7.8 Billion |

| Market Forecast in 2033 | USD 26.5 Billion |

| Growth Rate | 17.5% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ARM Holdings plc, Synopsys Inc., Cadence Design Systems Inc., Imagination Technologies Group plc, Rambus Inc., CEVA Inc., VeriSilicon Holdings Co. Ltd., Alphawave Semi, OpenFive (part of Alphawave Semi), Achronix Semiconductor Corporation, Cortus S.A., eMemory Technology Inc., Lattice Semiconductor Corporation, M31 Technology Corporation, Arteris IP, Sonics Inc. (part of Cadence), Dream Chip Technologies GmbH, Dolphin Design, Andes Technology Corporation, Silicon Motion Technology Corporation. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Semiconductor IP market is meticulously segmented to provide a granular understanding of its diverse components and their respective contributions to overall market dynamics. This segmentation facilitates a deeper analysis of market trends, consumer preferences, and technological shifts within specific product types, design methodologies, and end-use applications. Understanding these segments is crucial for identifying high-growth areas and tailoring strategic initiatives to capitalize on emerging opportunities.

The segmentation by type, for instance, highlights the increasing specialization of IP, from foundational processor and memory blocks to complex interface and security solutions. The distinction between hard and soft IP reflects varying levels of design flexibility and reusability, impacting their adoption across different stages of chip development. Furthermore, application-based segmentation reveals the primary industries driving demand, illustrating how the pervasive integration of electronics across consumer, automotive, and industrial sectors directly fuels the need for diverse Semiconductor IP portfolios. This structured approach ensures a comprehensive view of the market's intricate structure and evolution.

- By Type:

- Processor IP (CPU, GPU, DSP, NPU)

- Memory IP (SRAM, DRAM, Flash)

- Interface IP (USB, PCIe, Ethernet, MIPI)

- Other IP (Analog, Mixed-Signal, Security IP, Physical IP)

- By Design:

- Hard IP

- Soft IP

- By Application:

- Consumer Electronics

- Automotive

- Networking & Communications

- Industrial

- Healthcare

- Data Center & Cloud

- Others

- By Vertical:

- Internet of Things (IoT)

- Artificial Intelligence (AI)

- 5G

- Autonomous Driving

- Cloud Computing

- Edge Computing

Regional Highlights

- North America: This region holds a significant share in the Semiconductor IP market, primarily due to the presence of a large number of established semiconductor companies, robust research and development activities, and early adoption of advanced technologies like AI, IoT, and high-performance computing. Strong investments in data centers and cloud infrastructure, coupled with the thriving automotive sector, contribute substantially to regional market growth.

- Europe: Europe is a key market, driven by its strong automotive industry and increasing focus on industrial automation and advanced manufacturing. The region is also investing heavily in IoT, secure connectivity, and edge computing, creating demand for specialized and high-reliability IP cores. Government initiatives and academic research collaborations further foster innovation in the semiconductor ecosystem.

- Asia Pacific (APAC): APAC is expected to exhibit the highest growth rate during the forecast period. This surge is attributed to the presence of major semiconductor manufacturing hubs, rapidly expanding consumer electronics markets, and significant government investments in digital infrastructure and indigenous chip development (e.g., in China, South Korea, Taiwan, and Japan). The burgeoning adoption of 5G, AI, and IoT in diverse applications across the region fuels demand for a wide range of IP.

- Latin America: This emerging market is witnessing gradual growth driven by increasing digitalization, expanding mobile connectivity, and rising demand for smart devices. While smaller in market share compared to other regions, investment in smart city projects and local manufacturing initiatives are slowly contributing to the adoption of semiconductor IP.

- Middle East and Africa (MEA): The MEA region is a nascent but growing market for Semiconductor IP, propelled by digital transformation initiatives, smart infrastructure development, and growing investments in ICT. Though smaller in volume, increasing internet penetration and adoption of cloud services are expected to drive demand for relevant IP in the long term.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Semiconductor IP Market.- ARM Holdings plc

- Synopsys Inc.

- Cadence Design Systems Inc.

- Imagination Technologies Group plc

- Rambus Inc.

- CEVA Inc.

- VeriSilicon Holdings Co. Ltd.

- Alphawave Semi

- OpenFive (part of Alphawave Semi)

- Achronix Semiconductor Corporation

- Cortus S.A.

- eMemory Technology Inc.

- Lattice Semiconductor Corporation

- M31 Technology Corporation

- Arteris IP

- Sonics Inc. (part of Cadence)

- Dream Chip Technologies GmbH

- Dolphin Design

- Andes Technology Corporation

- Silicon Motion Technology Corporation

Frequently Asked Questions

What is Semiconductor IP and why is it crucial?

Semiconductor IP, or Intellectual Property, refers to reusable blocks of logic, layout, or design that are licensed for integration into larger semiconductor designs, typically System-on-Chips (SoCs). It is crucial because it significantly reduces design complexity, accelerates time-to-market, lowers development costs, and enables specialized functionalities, allowing companies to focus on core innovation rather than rebuilding foundational components.

How is AI transforming the Semiconductor IP market?

AI is transforming the Semiconductor IP market by driving demand for specialized processing units (e.g., NPUs, GPUs, DSPs) and memory IP optimized for AI workloads. Simultaneously, AI is increasingly employed in Electronic Design Automation (EDA) tools to automate and optimize IP design, verification, and integration processes, leading to faster, more efficient, and error-free chip development.

What are the primary growth drivers for Semiconductor IP?

Key growth drivers for Semiconductor IP include the exponential rise of IoT and connected devices, increasing adoption of AI/ML across industries, growing complexity of SoC designs, expansion of automotive electronics (e.g., ADAS), and the rollout of 5G technology. These factors collectively create a strong demand for diverse, high-performance, and energy-efficient IP solutions.

Which regions are leading the Semiconductor IP market, and why?

North America and Asia Pacific are currently leading the Semiconductor IP market. North America benefits from a strong presence of major semiconductor companies, extensive R&D investments, and early adoption of advanced technologies. Asia Pacific's leadership is driven by its vast manufacturing capabilities, rapidly expanding consumer electronics market, and significant government support for semiconductor industry growth and innovation.

What challenges does the Semiconductor IP market face?

The Semiconductor IP market faces challenges such as high initial licensing costs, complexities in IP integration and verification, persistent concerns over IP piracy and security, and the rapid pace of technological obsolescence. Additionally, the shortage of skilled IP design engineers and the cyclical nature of the semiconductor industry also pose significant hurdles to sustained market growth.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted