Wide Bandgap Power Semiconductor Device Market

Wide Bandgap Power Semiconductor Device Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705451 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

Wide Bandgap Power Semiconductor Device Market Size

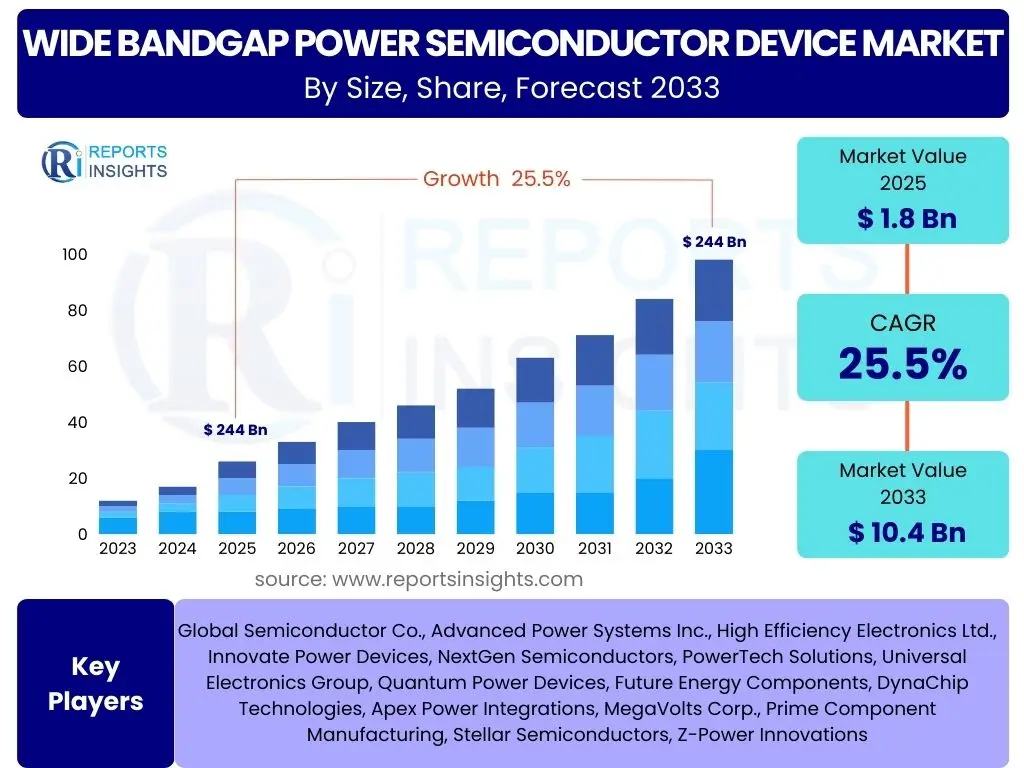

According to Reports Insights Consulting Pvt Ltd, The Wide Bandgap Power Semiconductor Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 25.5% between 2025 and 2033. The market is estimated at USD 1.8 Billion in 2025 and is projected to reach USD 10.4 Billion by the end of the forecast period in 2033.

Key Wide Bandgap Power Semiconductor Device Market Trends & Insights

The Wide Bandgap (WBG) power semiconductor device market is experiencing significant transformation, driven by an increasing demand for energy-efficient power solutions across various industries. A prominent trend involves the accelerated adoption of Silicon Carbide (SiC) and Gallium Nitride (GaN) technologies, which offer superior performance characteristics compared to traditional silicon-based devices. These WBG materials enable higher switching frequencies, reduced power losses, and operation at elevated temperatures, directly contributing to smaller, lighter, and more efficient power electronic systems.

Another critical insight is the expanding application landscape for WBG devices. While initially gaining traction in niche high-power and high-frequency applications, their benefits are now being recognized and integrated into mainstream sectors. The automotive industry, particularly electric vehicles (EVs) and hybrid electric vehicles (HEVs), stands out as a major growth catalyst, where WBG devices are crucial for enhancing the efficiency of onboard chargers, inverters, and DC-DC converters. Similarly, the renewable energy sector, including solar inverters and wind power converters, is increasingly relying on WBG semiconductors to optimize energy harvesting and conversion processes.

Furthermore, technological advancements in manufacturing processes and packaging solutions are enabling cost reduction and improved reliability for WBG devices. This continuous innovation is crucial for broader market penetration and addresses previous concerns regarding their higher initial cost compared to silicon counterparts. The market is also witnessing a trend towards integrated power modules combining multiple WBG components, simplifying system design and improving overall performance for end-users. These collective trends underscore a fundamental shift in power electronics towards more sustainable and efficient solutions.

- Accelerated adoption of SiC and GaN technologies for higher efficiency and power density.

- Significant growth driven by the electric vehicle and hybrid electric vehicle sectors.

- Increasing integration of WBG devices in renewable energy systems, such as solar inverters.

- Advancements in manufacturing techniques leading to cost reduction and improved reliability.

- Development of integrated power modules incorporating multiple WBG components.

- Expansion into industrial applications, data centers, and telecommunications infrastructure.

- Focus on enhanced thermal management solutions for high-power WBG applications.

AI Impact Analysis on Wide Bandgap Power Semiconductor Device

The intersection of Artificial Intelligence (AI) and Wide Bandgap (WBG) power semiconductor devices is emerging as a significant area of innovation, particularly in optimizing system performance and enhancing design efficiencies. AI algorithms are being increasingly employed in the design and simulation phases of WBG devices, enabling engineers to rapidly iterate on complex layouts, predict performance under varied conditions, and identify optimal material compositions. This data-driven approach shortens development cycles and improves the efficacy of new WBG product introductions, addressing the stringent requirements of high-performance applications.

Beyond design, AI is also transforming the operational aspects of systems utilizing WBG semiconductors. Predictive maintenance powered by AI can monitor the health and performance of power electronics, anticipating potential failures and enabling proactive intervention, thereby maximizing uptime and extending the lifespan of critical infrastructure. In complex power management systems, AI can dynamically optimize power conversion and distribution, leveraging the high switching frequencies and lower losses of WBG devices to achieve unprecedented levels of energy efficiency and responsiveness.

The ongoing development of AI at the edge, where processing occurs closer to the data source, further amplifies the demand for efficient power solutions that WBG devices provide. AI-enabled edge devices, from autonomous vehicles to smart sensors, require highly compact, reliable, and energy-efficient power conversion. WBG semiconductors are uniquely positioned to meet these demands, providing the foundational power electronics for next-generation AI-driven applications. This symbiotic relationship between AI and WBG technology is poised to drive innovation across numerous industries, making power systems more intelligent, robust, and sustainable.

- AI-driven optimization in WBG device design and simulation, accelerating development cycles.

- Enhanced predictive maintenance and fault detection in WBG-enabled power systems through AI.

- Dynamic power management and energy efficiency optimization in AI-controlled systems.

- Increased demand for WBG devices in AI at the edge applications, such as autonomous systems.

- AI integration in manufacturing processes for improved yield and quality control of WBG wafers.

Key Takeaways Wide Bandgap Power Semiconductor Device Market Size & Forecast

The Wide Bandgap (WBG) power semiconductor device market is poised for robust expansion, driven primarily by the escalating global emphasis on energy efficiency and the rapid electrification across various sectors. The projected Compound Annual Growth Rate (CAGR) of 25.5% signifies a profound shift in power electronics, moving away from conventional silicon towards SiC and GaN materials. This growth trajectory is strongly supported by widespread adoption in high-growth applications such as electric vehicles, renewable energy infrastructure, and advanced industrial power supplies, where the superior performance attributes of WBG devices are indispensable for achieving higher power density and lower energy losses.

A crucial insight from the market forecast is the substantial increase in market valuation, from an estimated USD 1.8 Billion in 2025 to USD 10.4 Billion by 2033. This exponential growth underscores the increasing maturity and commercial viability of WBG technologies, as manufacturing processes improve and costs become more competitive. The market's expansion is not merely volume-driven but also reflects the increasing complexity and value of WBG integrated solutions, including power modules and advanced packaging techniques that enhance device performance and reliability in demanding environments.

Furthermore, the long-term outlook for the WBG market indicates sustained innovation and diversification across new application areas. As industries continue to miniaturize electronics and demand higher efficiency, the inherent advantages of WBG semiconductors will become even more pronounced, driving continued investment in research and development. The market's resilience and strong growth forecast highlight its pivotal role in enabling the next generation of power electronics, essential for global decarbonization efforts and the advancement of smart technologies.

- The market is set for exponential growth, reflecting a significant industry shift towards WBG materials.

- Electric vehicles and renewable energy remain the primary catalysts for market expansion.

- Technological advancements and economies of scale are improving the cost-effectiveness of WBG devices.

- Increasing integration of WBG devices into power modules and advanced systems for higher value.

- WBG semiconductors are fundamental to achieving higher energy efficiency and sustainability goals.

- The market is anticipated to diversify into new high-power and high-frequency applications.

- Continuous innovation in materials and packaging is critical for sustained market leadership.

Wide Bandgap Power Semiconductor Device Market Drivers Analysis

The wide bandgap power semiconductor device market is primarily driven by the escalating global demand for energy-efficient solutions across diverse industries. With increasing electricity consumption and rising concerns over carbon emissions, there is a strong impetus to reduce power losses in electronic systems. Wide Bandgap (WBG) materials like Silicon Carbide (SiC) and Gallium Nitride (GaN) offer significantly lower switching losses, higher breakdown voltages, and superior thermal conductivity compared to traditional silicon, making them ideal for high-efficiency power conversion.

Another significant driver is the rapid electrification of the automotive sector, particularly the surge in production and adoption of Electric Vehicles (EVs) and Hybrid Electric Vehicles (HEVs). WBG devices are crucial components in EV powertrains, including onboard chargers, inverters, and DC-DC converters, where they enable higher power density, extended range, faster charging, and improved overall system efficiency. The push towards sustainable transportation solutions globally directly translates into a soaring demand for WBG power semiconductors.

Furthermore, the expansion of renewable energy infrastructure, such as solar power generation and wind turbines, provides a substantial impetus for the WBG market. These energy systems require highly efficient power conversion to maximize energy capture and grid integration. WBG semiconductors enhance the performance and reliability of solar inverters, wind turbine converters, and energy storage systems, contributing to a more robust and efficient renewable energy ecosystem. The global commitment to renewable energy targets ensures sustained growth in this application segment.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Energy Efficiency | +5.0% | Global, particularly Europe and Asia Pacific | 2025-2033 |

| Rapid Electrification of Automotive (EV/HEV) | +6.5% | North America, Europe, Asia Pacific (China, Japan, South Korea) | 2025-2033 |

| Growth in Renewable Energy Sector | +4.0% | Europe, Asia Pacific (China, India), North America | 2025-2033 |

| Advancements in Data Center & Telecom Infrastructure | +3.5% | North America, Asia Pacific, Europe | 2025-2033 |

| Miniaturization and High Power Density Requirements | +3.0% | Global | 2025-2033 |

Wide Bandgap Power Semiconductor Device Market Restraints Analysis

Despite the strong growth potential, the Wide Bandgap (WBG) power semiconductor device market faces certain restraints that could impact its expansion. One significant challenge is the relatively high manufacturing cost of WBG materials like SiC and GaN wafers compared to conventional silicon. The complex processes involved in crystal growth and defect management for WBG substrates contribute to higher production expenses, which can translate to a higher price point for the end product. This cost barrier can limit widespread adoption, especially in cost-sensitive applications or regions.

Another restraint is the inherent complexity in designing and integrating WBG devices into existing power electronic systems. While WBG devices offer superior performance, they require specialized design techniques, advanced gate drivers, and effective thermal management solutions due to their higher switching speeds and power densities. Lack of expertise or readily available design tools among engineers accustomed to silicon-based designs can pose an adoption hurdle, necessitating significant investment in training and new design methodologies.

Furthermore, the supply chain for WBG materials and devices is still maturing compared to the highly established silicon ecosystem. While efforts are underway to scale up production capacity for SiC and GaN substrates and devices, supply chain bottlenecks or fluctuations in raw material availability could lead to production delays and impact market stability. Ensuring a robust and resilient supply chain is critical for the sustained growth and broader commercialization of WBG power semiconductors.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs | -2.0% | Global, particularly emerging economies | 2025-2029 |

| Complexity in System Design and Integration | -1.5% | Global, particularly smaller enterprises | 2025-2028 |

| Supply Chain Maturity and Availability | -1.0% | Global | 2025-2027 |

| Lack of Standardization | -0.8% | Global | 2025-2029 |

Wide Bandgap Power Semiconductor Device Market Opportunities Analysis

The Wide Bandgap (WBG) power semiconductor device market presents numerous opportunities for growth and innovation, primarily driven by untapped application areas and evolving technological requirements. The burgeoning market for consumer electronics, particularly fast chargers for smartphones, laptops, and other portable devices, offers a significant opportunity for Gallium Nitride (GaN) devices. GaN's ability to enable smaller, lighter, and more efficient power adapters is highly attractive to consumers and manufacturers alike, fostering a new wave of adoption beyond traditional industrial uses.

Another substantial opportunity lies in the expansion of high-voltage and high-power industrial applications, including motor drives, industrial power supplies, and uninterruptible power supplies (UPS). As industries seek to improve operational efficiency and reduce energy consumption, the superior performance of Silicon Carbide (SiC) devices in these demanding environments becomes increasingly compelling. The trend towards industrial automation and smart factories further amplifies the need for reliable and efficient power management solutions, creating a fertile ground for WBG technology adoption.

Moreover, the continuous development of advanced packaging technologies and module integration for WBG devices opens up new avenues for market penetration. By combining multiple WBG chips into compact, high-performance modules, manufacturers can simplify system design, improve thermal management, and enhance overall reliability. This modular approach makes WBG solutions more accessible and appealing for a broader range of applications, including aerospace, defense, and specialized medical equipment, where reliability and performance are paramount. These opportunities underscore the diverse potential for WBG semiconductors to revolutionize various sectors.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Consumer Electronics Fast Chargers | +3.5% | Asia Pacific, North America, Europe | 2025-2033 |

| Growth in High-Voltage Industrial Applications | +3.0% | Global, particularly developed industrial economies | 2025-2033 |

| Development of Advanced Packaging and Module Integration | +2.5% | Global | 2025-2033 |

| Emergence of Grid-Scale Energy Storage Systems | +2.0% | North America, Europe, Asia Pacific | 2026-2033 |

Wide Bandgap Power Semiconductor Device Market Challenges Impact Analysis

The Wide Bandgap (WBG) power semiconductor device market faces several challenges that require strategic solutions for sustained growth. One significant challenge is the technical complexity associated with manufacturing high-quality WBG wafers, particularly Silicon Carbide (SiC). The stringent purity requirements, high temperatures involved in crystal growth, and the difficulty in minimizing defects can lead to lower yields compared to silicon, which directly impacts production scalability and cost-effectiveness. Overcoming these manufacturing hurdles is crucial for meeting the escalating demand.

Another challenge pertains to the scarcity of skilled workforce and specialized expertise required for WBG device design, fabrication, and system integration. Engineers and technicians with in-depth knowledge of WBG materials properties, high-frequency design principles, and advanced thermal management techniques are in high demand but short supply. This talent gap can slow down the adoption rate and innovation within the industry, as companies struggle to find the right talent to leverage the full potential of WBG technology.

Furthermore, managing the high initial investment required for WBG production facilities and research and development (R&D) poses a notable challenge. Establishing and upgrading foundries for WBG wafer fabrication and device manufacturing involves substantial capital expenditure due to specialized equipment and process requirements. This significant upfront cost can be a barrier for new entrants and may concentrate production among a few large players, potentially limiting market competition and rapid innovation in certain areas. Addressing these challenges through strategic investments, education, and collaborative efforts is essential for the long-term success of the WBG market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technical Complexity in Wafer Manufacturing and Yield | -1.5% | Global | 2025-2028 |

| Shortage of Skilled Workforce and Expertise | -1.2% | Global | 2025-2030 |

| High Capital Investment for Production Facilities | -1.0% | Global | 2025-2029 |

| Thermal Management in High-Power Applications | -0.7% | Global | 2025-2027 |

Wide Bandgap Power Semiconductor Device Market - Updated Report Scope

This report provides a comprehensive analysis of the Wide Bandgap Power Semiconductor Device Market, offering detailed insights into market dynamics, segmentation, regional trends, and competitive landscape. It covers a forecast period from 2025 to 2033, with historical data from 2019 to 2023, providing a complete overview of the market's evolution and projected growth. The study delves into key market drivers, restraints, opportunities, and challenges, along with a thorough segmentation by material, device type, application, and end-use industry, providing a granular view of market trends and potential growth avenues. The report's scope includes detailed profiles of leading market players, offering strategic intelligence for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.8 Billion |

| Market Forecast in 2033 | USD 10.4 Billion |

| Growth Rate | 25.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Semiconductor Co., Advanced Power Systems Inc., High Efficiency Electronics Ltd., Innovate Power Devices, NextGen Semiconductors, PowerTech Solutions, Universal Electronics Group, Quantum Power Devices, Future Energy Components, DynaChip Technologies, Apex Power Integrations, MegaVolts Corp., Prime Component Manufacturing, Stellar Semiconductors, Z-Power Innovations |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Wide Bandgap Power Semiconductor Device Market is comprehensively segmented to provide a detailed understanding of its diverse components and application areas. This segmentation allows for granular analysis of market dynamics, growth drivers, and opportunities across various technology types and end-use sectors. The market is primarily categorized by the type of Wide Bandgap material used, the specific device types produced, the applications they serve, and the broader end-use industries leveraging these advanced semiconductors. Each segment contributes uniquely to the overall market landscape, reflecting distinct technological advantages and market demands.

- By Material:

- Silicon Carbide (SiC): Known for high power, high voltage, and high temperature applications.

- Gallium Nitride (GaN): Ideal for high frequency, high efficiency, and compact power solutions.

- Others: Includes emerging materials like Gallium Oxide (Ga2O3) with potential for ultra-high power applications.

- By Device Type:

- Diodes: Rectifiers and other power diodes.

- Transistors: MOSFETs (Metal-Oxide-Semiconductor Field-Effect Transistors), IGBTs (Insulated Gate Bipolar Transistors), HEMTs (High-Electron-Mobility Transistors).

- Power Modules: Integrated solutions combining multiple WBG devices for specific applications.

- By Application:

- Power Supply & Inverter: For various consumer and industrial power conversion.

- EV/HEV: Critical components for electric and hybrid vehicle powertrains.

- Consumer Electronics: Fast chargers, adapters, and power management in devices.

- Industrial Motor Drives: For energy-efficient operation of industrial machinery.

- Renewable Energy Systems: Solar inverters, wind power converters, energy storage.

- Data Centers: Power conversion and management for server farms.

- Aerospace & Defense: High-reliability, lightweight power systems.

- Telecommunications Infrastructure: Powering base stations and network equipment.

- By End-Use Industry:

- Automotive: All types of electric and hybrid vehicles.

- Energy & Power: Grid infrastructure, renewable energy, power generation and distribution.

- Information & Communication Technology (ICT): Data centers, telecom, consumer electronics.

- Consumer Electronics: Smartphones, laptops, home appliances, gaming consoles.

- Industrial: Manufacturing, heavy machinery, robotics, automation.

- Aerospace & Defense: Avionics, radar systems, power supply for defense equipment.

Regional Highlights

- North America: This region is characterized by significant investments in electric vehicle infrastructure and renewable energy projects, driving the adoption of WBG devices. Strong research and development capabilities, coupled with the presence of key industry players and demand from data centers and aerospace, contribute to its steady market growth.

- Europe: Europe is a leading market due to stringent energy efficiency regulations and robust governmental support for electric mobility and green energy initiatives. Countries like Germany and the Nordic nations are at the forefront of WBG technology adoption in automotive and industrial applications, pushing for higher efficiency and reduced carbon footprint.

- Asia Pacific (APAC): APAC represents the largest and fastest-growing market for Wide Bandgap power semiconductors, primarily driven by the massive electronics manufacturing base, rapid industrialization, and exponential growth in the EV market, especially in China. Government initiatives promoting domestic production and the widespread adoption of consumer electronics further fuel market expansion across countries like China, Japan, South Korea, and India.

- Latin America: While smaller, the Latin American market is exhibiting emerging growth, largely influenced by increasing investments in renewable energy projects and gradual adoption of electric vehicles. Brazil and Mexico are key countries contributing to this region's market development.

- Middle East and Africa (MEA): The MEA region is expected to witness moderate growth, driven by diversification efforts away from oil and gas towards sustainable energy solutions and industrial development. Investments in smart city projects and grid modernization initiatives are slowly creating demand for WBG devices.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Wide Bandgap Power Semiconductor Device Market.- Global Semiconductor Co.

- Advanced Power Systems Inc.

- High Efficiency Electronics Ltd.

- Innovate Power Devices

- NextGen Semiconductors

- PowerTech Solutions

- Universal Electronics Group

- Quantum Power Devices

- Future Energy Components

- DynaChip Technologies

- Apex Power Integrations

- MegaVolts Corp.

- Prime Component Manufacturing

- Stellar Semiconductors

- Z-Power Innovations

- Electro-Gen Corp.

- PowerGrid Solutions

- Infinite Power Tech

- Smart Silicon Innovations

- Green Energy Devices

Frequently Asked Questions

What are Wide Bandgap (WBG) power semiconductors?

Wide Bandgap (WBG) power semiconductors are electronic devices made from materials like Silicon Carbide (SiC) and Gallium Nitride (GaN), which have a larger bandgap than traditional silicon. This characteristic allows them to operate at higher temperatures, voltages, and switching frequencies, leading to significantly improved energy efficiency, smaller component size, and greater power density in electronic systems.

What are the primary applications of Wide Bandgap devices?

Wide Bandgap devices are primarily used in applications requiring high efficiency and power density, such as electric vehicles (EVs) and hybrid electric vehicles (HEVs) for inverters and chargers, renewable energy systems like solar inverters, industrial motor drives, data centers, fast chargers for consumer electronics, and aerospace and defense power systems.

How do SiC and GaN differ in their applications?

Silicon Carbide (SiC) devices are typically favored for high-power, high-voltage applications (e.g., above 600V) in EVs, industrial power supplies, and grid infrastructure due to their robust thermal performance and breakdown voltage. Gallium Nitride (GaN) devices, conversely, excel in high-frequency, lower-to-medium power applications (typically below 600V) like consumer electronics fast chargers, data center power supplies, and telecom equipment, offering superior switching speed and miniaturization.

What are the key drivers for the Wide Bandgap power semiconductor market?

Key drivers include the global demand for energy efficiency, the rapid electrification of the automotive sector, the expansion of renewable energy infrastructure, the increasing need for high power density and miniaturization in electronic devices, and advancements in data center and telecommunications infrastructure requiring optimized power solutions.

What challenges does the Wide Bandgap market face?

Challenges include the relatively higher manufacturing costs of SiC and GaN wafers compared to silicon, the technical complexity in fabricating high-quality WBG devices leading to yield issues, the scarcity of skilled engineers with WBG expertise, and the significant initial capital investment required for establishing and scaling production facilities.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted