Semiconductor Defect Inspection System Market

Semiconductor Defect Inspection System Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705450 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

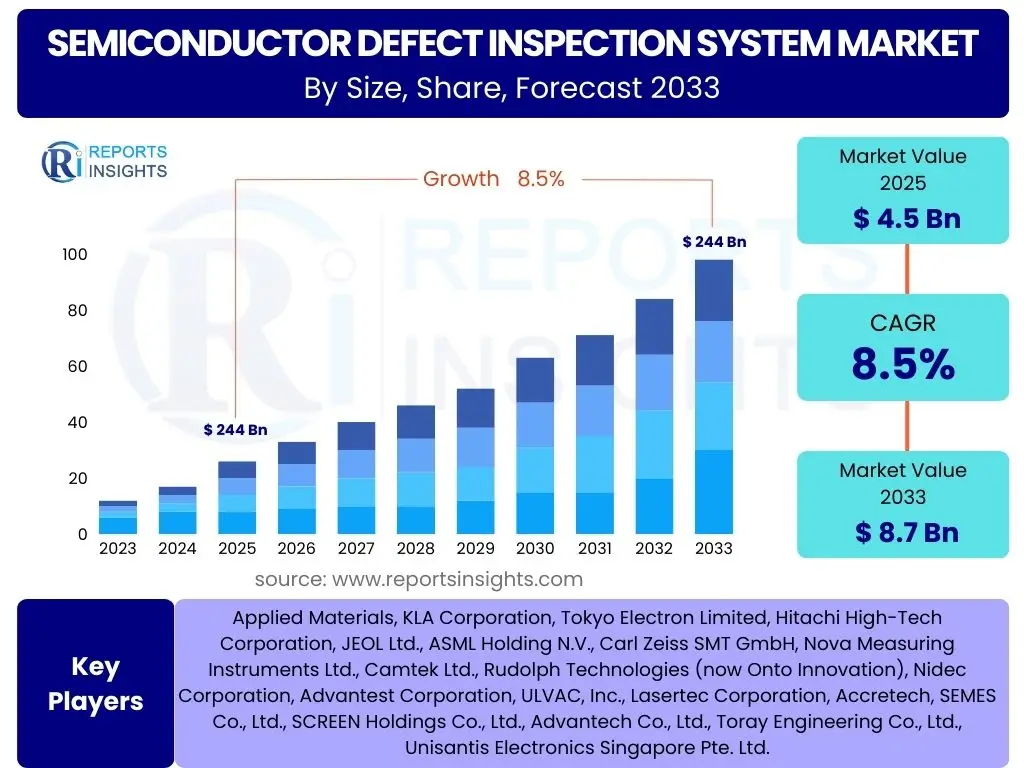

Semiconductor Defect Inspection System Market Size

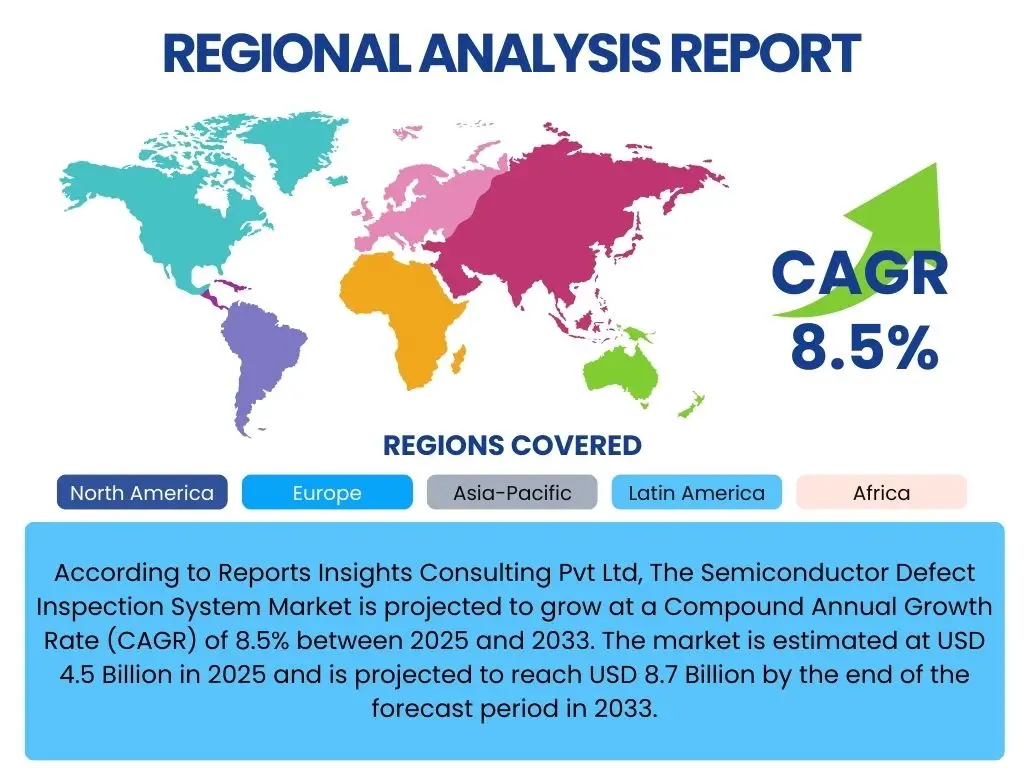

According to Reports Insights Consulting Pvt Ltd, The Semiconductor Defect Inspection System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 4.5 Billion in 2025 and is projected to reach USD 8.7 Billion by the end of the forecast period in 2033.

Key Semiconductor Defect Inspection System Market Trends & Insights

User inquiries frequently focus on the technological evolution and strategic shifts within the semiconductor defect inspection market. There is a keen interest in how advancements in imaging, data processing, and automation are shaping the industry. Market participants and stakeholders are particularly interested in the adoption of next-generation inspection methodologies, the impact of miniaturization in semiconductor components, and the increasing demand for advanced packaging solutions. Furthermore, questions arise concerning the integration of inspection systems into broader semiconductor manufacturing workflows and the increasing importance of inline metrology for yield optimization.

The market is currently witnessing a significant pivot towards enhanced sensitivity and throughput, driven by the escalating complexity of chip designs and the imperative for higher manufacturing yields. This trend is fostering innovation in optical and e-beam inspection techniques, pushing the boundaries of what is detectable at the nanometer scale. Companies are investing heavily in research and development to address the challenges posed by new materials, intricate 3D structures, and heterogeneous integration. The proliferation of specialized chips for AI, automotive, and high-performance computing applications further amplifies the need for robust and precise defect detection at every stage of the manufacturing process.

- Advanced optical inspection systems with enhanced resolution and speed are becoming standard.

- Increased adoption of e-beam inspection for critical dimension measurement and sub-nanometer defect detection.

- Growing emphasis on inline and in-situ inspection capabilities for real-time process control.

- Development of hybrid inspection platforms combining multiple technologies for comprehensive defect coverage.

- Expansion of inspection requirements for advanced packaging technologies, including 3D ICs and fan-out packages.

- Focus on AI and machine learning for improved defect classification, root cause analysis, and false positive reduction.

- Rising demand for fully automated inspection solutions to minimize human intervention and enhance throughput.

AI Impact Analysis on Semiconductor Defect Inspection System

Common user questions regarding AI's influence on semiconductor defect inspection systems highlight expectations for improved accuracy, efficiency, and predictive capabilities. Users are keen to understand how AI can overcome the limitations of traditional inspection methods, particularly in distinguishing between critical defects and nuisance patterns, and in accelerating the analysis of vast amounts of inspection data. There is also significant interest in AI's role in enabling fully autonomous inspection processes and its potential to contribute to proactive yield management strategies.

Artificial intelligence, particularly machine learning and deep learning algorithms, is profoundly transforming the semiconductor defect inspection landscape. AI algorithms are being deployed to enhance the detection of subtle or complex defects that might be overlooked by human operators or traditional rule-based systems. By analyzing large datasets of historical defect images and associated process parameters, AI models can learn to identify patterns indicative of potential yield excursions, thereby enabling more precise and timely corrective actions. This capability is critical for advanced nodes where defect sensitivity is paramount.

The integration of AI extends beyond simple defect detection to sophisticated defect classification and root cause analysis. AI-powered systems can automatically categorize defects, prioritize their criticality, and even suggest potential sources within the manufacturing process. This significantly reduces the time and effort required for engineers to diagnose and resolve issues, leading to faster process ramp-up and improved overall equipment effectiveness. Furthermore, AI contributes to adaptive inspection strategies, allowing systems to dynamically adjust inspection parameters based on real-time process variations, optimizing both throughput and sensitivity.

- Enhanced Defect Detection: AI algorithms improve the identification of subtle and complex defects, reducing false positives and increasing detection accuracy.

- Automated Defect Classification: Machine learning enables rapid and accurate categorization of defects, streamlining analysis and reporting.

- Predictive Maintenance: AI can forecast equipment failures or process excursions based on inspection data, enabling proactive intervention.

- Optimized Inspection Recipes: AI models learn from continuous inspection data to fine-tune inspection parameters for improved efficiency and sensitivity.

- Reduced Human Intervention: AI-driven automation minimizes the need for human review, increasing throughput and consistency.

- Faster Root Cause Analysis: Advanced algorithms accelerate the identification of defect sources, shortening debug cycles.

- Data Overload Management: AI efficiently processes and extracts insights from massive volumes of inspection data, turning raw data into actionable intelligence.

Key Takeaways Semiconductor Defect Inspection System Market Size & Forecast

User queries regarding key takeaways from the Semiconductor Defect Inspection System market size and forecast consistently point to an emphasis on sustained growth, driven by fundamental shifts in semiconductor manufacturing. Stakeholders are keen to understand the primary forces propelling this growth, such as technological advancements in chip design, the expanding applications of semiconductors, and the critical need for higher yields in complex manufacturing processes. They also seek insights into the segments and regions expected to exhibit the most significant growth and investment opportunities.

The market for semiconductor defect inspection systems is poised for robust expansion, underpinned by the relentless pursuit of smaller feature sizes and higher transistor densities in integrated circuits. As chip designs become increasingly intricate, the probability of microscopic defects occurring during manufacturing rises significantly, making advanced inspection indispensable. This drives continuous investment in cutting-edge inspection technologies capable of detecting defects at the atomic or molecular level, ensuring the reliability and performance of advanced semiconductor devices. The market's upward trajectory is a direct reflection of the industry's commitment to quality and efficiency in the face of escalating complexity.

Furthermore, the diversification of semiconductor applications across high-growth sectors like automotive electronics, artificial intelligence, 5G communication, and the Internet of Things (IoT) is a pivotal factor contributing to the market's positive outlook. Each of these sectors demands specialized and highly reliable chips, necessitating stringent quality control throughout the production cycle. The increasing adoption of advanced packaging techniques, such as chiplets and 3D stacking, also introduces new inspection challenges and opportunities, further solidifying the long-term growth prospects for the defect inspection system market.

- Consistent Growth Trajectory: The market is projected for significant expansion driven by technological advancements and increasing demand for semiconductors.

- Critical for Advanced Nodes: Inspection systems are indispensable for manufacturing chips at sub-10nm and sub-5nm nodes due to extreme sensitivity to defects.

- Yield Management Imperative: The primary driver for adoption is the necessity to optimize manufacturing yields and reduce waste in high-cost production.

- Technological Evolution: Continuous innovation in optical, e-beam, and AI-powered inspection techniques is vital for market sustainment and growth.

- Emerging Applications Influence: Growth is significantly influenced by the proliferation of semiconductors in AI, automotive, IoT, and 5G.

- Advanced Packaging Demand: The complexity of advanced packaging solutions (e.g., 3D ICs, fan-out) necessitates specialized inspection, opening new market avenues.

- Regional Dynamics: Asia Pacific, particularly countries with robust foundry ecosystems, will remain a dominant force in market adoption and investment.

Semiconductor Defect Inspection System Market Drivers Analysis

The semiconductor defect inspection system market is primarily propelled by the relentless demand for smaller, more powerful, and increasingly complex semiconductor devices. As the industry pushes towards advanced nodes (e.g., 7nm, 5nm, and beyond) and innovative architectures like 3D NAND and FinFETs, even minuscule defects can severely impact device performance and yield. This necessitates highly sensitive and accurate inspection tools capable of detecting sub-nanometer flaws across various manufacturing stages, from bare wafer to packaged chips. The imperative to achieve high yields in multi-billion dollar fabrication facilities drives significant investment in advanced inspection solutions.

Another crucial driver is the exponential growth of semiconductor applications across diverse end-use industries. The proliferation of artificial intelligence, high-performance computing, 5G communication, autonomous vehicles, and the Internet of Things (IoT) has significantly increased the demand for specialized and high-quality integrated circuits. Each of these applications requires chips with specific performance characteristics and high reliability, making comprehensive defect inspection an indispensable part of the manufacturing process to ensure product integrity and minimize field failures. This widespread adoption translates directly into a higher demand for sophisticated inspection capabilities.

Furthermore, the ongoing shift towards advanced packaging technologies, such as system-in-package (SiP), wafer-level chip-scale packaging (WLCSP), and 3D stacking, presents new challenges and opportunities for defect inspection. These complex assembly methods introduce new potential failure points and require inspection beyond the traditional front-end-of-line (FEOL) and back-end-of-line (BEOL) processes. Consequently, manufacturers are investing in inspection systems capable of characterizing defects in stacked dies, interconnections, and package-level assemblies, thereby expanding the market scope for inspection equipment.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Miniaturization and Increasing Chip Complexity | +2.5% | Global, particularly Asia Pacific (Taiwan, South Korea) | 2025-2033 (Long-term) |

| Growing Demand for High-Performance Computing & AI | +1.8% | North America, Asia Pacific (China, Japan) | 2025-2030 (Mid-term) |

| Proliferation of IoT and 5G Devices | +1.5% | Global, strong in Asia Pacific and Europe | 2025-2030 (Mid-term) |

| Emphasis on Yield Optimization in Fabrication | +1.2% | Global (all major foundry regions) | 2025-2033 (Long-term) |

| Advancements in Automotive Electronics (ADAS, EVs) | +1.0% | Europe, North America, Asia Pacific (Japan, South Korea) | 2026-2033 (Mid to Long-term) |

| Shift Towards Advanced Packaging Technologies | +0.8% | Global, particularly Asia Pacific (Packaging Hubs) | 2027-2033 (Long-term) |

| Increasing R&D Investment in New Materials | +0.7% | North America, Europe, Asia Pacific | 2028-2033 (Long-term) |

Semiconductor Defect Inspection System Market Restraints Analysis

The high initial capital expenditure associated with advanced semiconductor defect inspection systems represents a significant restraint on market growth. These systems are technologically complex, incorporating highly sensitive optics, precision mechanics, and sophisticated software, which translates into substantial upfront costs for semiconductor manufacturers. For smaller foundries or new entrants, the financial burden of acquiring and maintaining such equipment can be prohibitive, potentially limiting their ability to upgrade to the latest inspection capabilities and hindering broader market penetration.

Another notable restraint is the increasing complexity and volume of data generated by advanced inspection tools. While these systems provide an unprecedented level of detail, managing, storing, and analyzing terabytes or even petabytes of inspection data presents considerable challenges. Effective defect analysis requires robust data infrastructure, advanced analytics, and skilled personnel, which can add to operational costs and complexity. The difficulty in extracting actionable insights from this data deluge efficiently can sometimes offset the benefits of high-resolution inspection, posing a bottleneck for manufacturers.

Furthermore, the shortage of highly skilled professionals capable of operating, maintaining, and interpreting the results from complex defect inspection systems acts as a significant constraint. These specialized roles require expertise in optics, electronics, materials science, and data analytics. The limited availability of such talent, coupled with the long training periods required, can impede the efficient deployment and utilization of advanced inspection technologies, particularly in regions where the semiconductor talent pool is less developed, thereby slowing down market adoption and expansion.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure and Ownership Costs | -1.5% | Global, particularly emerging economies | 2025-2033 (Long-term) |

| Technological Complexity and Integration Challenges | -1.0% | Global (all manufacturers) | 2025-2030 (Mid-term) |

| Skilled Labor Shortage and Training Requirements | -0.8% | Global, prominent in developed economies | 2025-2033 (Long-term) |

| Increasing Volume and Complexity of Data Generated | -0.7% | Global (all manufacturers) | 2025-2030 (Mid-term) |

| Economic Downturns Affecting Capital Spending | -0.5% | Global (dependent on macroeconomic cycles) | Short-term (cyclical) |

| Cybersecurity Risks for Connected Systems | -0.3% | Global (all manufacturers) | 2026-2033 (Mid to Long-term) |

Semiconductor Defect Inspection System Market Opportunities Analysis

Significant opportunities in the semiconductor defect inspection system market arise from the continuous evolution of semiconductor manufacturing processes, particularly the shift towards extreme ultraviolet (EUV) lithography and the adoption of novel materials. EUV technology, while enabling smaller feature sizes, introduces new types of defects and requires unprecedented inspection sensitivity. This creates a strong demand for specialized EUV-patterned wafer inspection systems and metrology tools capable of characterizing defects that were previously undetectable, opening lucrative avenues for innovation and market expansion for inspection equipment providers.

The burgeoning markets for emerging technologies such as quantum computing, photonics, and advanced MEMS (Micro-Electro-Mechanical Systems) also present substantial growth opportunities. These next-generation devices often involve unique materials, intricate 3D structures, and highly specialized manufacturing processes, necessitating bespoke defect inspection solutions. Developing inspection systems tailored to the specific requirements of these niche but high-growth areas allows companies to diversify their product portfolios and capture new revenue streams beyond traditional silicon-based manufacturing.

Furthermore, the increasing focus on smart manufacturing and Industry 4.0 initiatives within the semiconductor sector offers opportunities for integrating advanced inspection systems into comprehensive factory automation and data ecosystems. This involves leveraging real-time data analytics, artificial intelligence, and machine learning to create self-optimizing inspection processes. Companies that can provide holistic solutions encompassing hardware, software, and data integration capabilities will be well-positioned to capitalize on the industry's drive towards fully automated, lights-out semiconductor fabrication, enhancing efficiency and yield management.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of EUV-Specific Inspection Solutions | +2.0% | Global, especially leading-edge foundries (Asia Pacific) | 2025-2033 (Long-term) |

| Expansion into Emerging Technology Sectors (Quantum, Photonics) | +1.5% | North America, Europe, Asia Pacific (R&D hubs) | 2027-2033 (Long-term) |

| Integration with Smart Factory and Industry 4.0 Initiatives | +1.3% | Global (all advanced manufacturers) | 2025-2030 (Mid-term) |

| Growth in Specialty Semiconductor Manufacturing (e.g., SiC, GaN) | +1.0% | Global (Automotive, Power Electronics regions) | 2026-2033 (Mid to Long-term) |

| Retrofit and Upgrade Market for Existing Fabs | +0.8% | Global (especially mature fabs) | 2025-2029 (Short to Mid-term) |

| Strategic Partnerships and Collaborations for Innovation | +0.7% | Global | 2025-2033 (Long-term) |

Semiconductor Defect Inspection System Market Challenges Impact Analysis

A primary challenge facing the semiconductor defect inspection system market is the escalating technical difficulty of detecting ever-smaller and more complex defects. As semiconductor feature sizes shrink to single-digit nanometers and device architectures become three-dimensional, distinguishing between genuine defects and benign process variations or noise becomes increasingly difficult. This requires constant innovation in illumination sources, optics, detectors, and algorithms, pushing the limits of physics and engineering. The high research and development costs associated with achieving this advanced sensitivity pose a significant hurdle for manufacturers of inspection equipment.

Another significant challenge is the rapid pace of technological change in the semiconductor industry itself. New process technologies, materials, and device structures emerge frequently, demanding that defect inspection systems maintain compatibility and effectiveness across a wide range of evolving manufacturing environments. This necessitates continuous adaptation and upgrades to existing inspection platforms, often leading to shorter product lifecycles and intense pressure on equipment suppliers to deliver new capabilities quickly. Keeping pace with these rapid shifts requires substantial investment and agility, presenting a formidable competitive and operational challenge.

Furthermore, managing the immense volume of data generated by high-resolution inspection tools poses a considerable challenge. Modern inspection systems produce terabytes of data per wafer, and analyzing this information effectively to identify, classify, and localize defects in real-time requires sophisticated data processing capabilities, including advanced computational infrastructure and intelligent algorithms. The sheer scale of data can overwhelm conventional analysis methods, leading to bottlenecks in defect review and limiting the speed at which process improvements can be implemented, thereby impacting overall manufacturing efficiency.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technical Difficulty of Detecting Smaller, Complex Defects | -1.2% | Global (all manufacturers) | 2025-2033 (Long-term) |

| Rapid Technological Obsolescence and R&D Costs | -1.0% | Global (equipment manufacturers) | 2025-2030 (Mid-term) |

| Data Management, Storage, and Analysis Complexity | -0.9% | Global (all manufacturers) | 2025-2030 (Mid-term) |

| High Cost of Ownership and Maintenance | -0.7% | Global (all manufacturers) | 2025-2033 (Long-term) |

| Integration with Existing Fab Infrastructure | -0.5% | Global (all manufacturers) | 2025-2029 (Short to Mid-term) |

| Supply Chain Disruptions for Critical Components | -0.4% | Global (cyclical) | Short-term (event-driven) |

Semiconductor Defect Inspection System Market - Updated Report Scope

This report provides an in-depth analysis of the Semiconductor Defect Inspection System Market, covering market size estimations, growth forecasts, and a comprehensive examination of market dynamics including drivers, restraints, opportunities, and challenges. It delves into the impact of key technological advancements such as AI, dissects various market segments, and highlights regional market performance, offering critical insights for strategic decision-making within the semiconductor industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 8.7 Billion |

| Growth Rate | 8.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Applied Materials, KLA Corporation, Tokyo Electron Limited, Hitachi High-Tech Corporation, JEOL Ltd., ASML Holding N.V., Carl Zeiss SMT GmbH, Nova Measuring Instruments Ltd., Camtek Ltd., Rudolph Technologies (now Onto Innovation), Nidec Corporation, Advantest Corporation, ULVAC, Inc., Lasertec Corporation, Accretech, SEMES Co., Ltd., SCREEN Holdings Co., Ltd., Advantech Co., Ltd., Toray Engineering Co., Ltd., Unisantis Electronics Singapore Pte. Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The semiconductor defect inspection system market is segmented across various dimensions, reflecting the diverse technological needs and applications within semiconductor manufacturing. These segments enable a detailed understanding of where growth opportunities are most prominent and how different inspection technologies cater to specific stages of the production process. Analyzing these segments provides valuable insights into the market's structure and the specialization required for effective defect management across the value chain, from bare wafer processing to final chip assembly.

Each segmentation criterion offers a unique perspective on market dynamics. For instance, the 'Type' segmentation differentiates between optical and e-beam technologies, highlighting their respective strengths in terms of speed, resolution, and defect types they can detect. The 'Product Type' segment focuses on the specific form of the semiconductor material being inspected, such as bare wafers, patterned wafers, or masks, which dictates the type of inspection system required. Understanding these distinctions is crucial for identifying precise market needs and for tailoring solutions to address the evolving challenges of advanced semiconductor manufacturing.

- By Type:

- Optical Defect Inspection System: Dominant for high-throughput, general-purpose inspection and larger defects. Utilizes various illumination techniques.

- E-beam Defect Inspection System: Crucial for sub-nanometer defect detection, particularly for critical dimension control and voltage contrast. Slower but higher resolution.

- Others (e.g., Acoustic, X-ray): Niche applications for specific defect types or materials not detectable by optical or e-beam methods.

- By Product Type:

- Bare Wafer Inspection System: Inspects blank silicon wafers for surface defects, particles, and contamination before patterning.

- Patterned Wafer Inspection System: Inspects wafers at various stages of front-end and back-end processing for pattern defects, particles, and scratches.

- Mask/Reticle Inspection System: Critical for ensuring the quality of photomasks, which are essential for lithography.

- Chip/Die Inspection System: Inspects individual chips or dies post-dicing for structural defects, wire bonding issues, and packaging flaws.

- By Application:

- Process Control: Inline monitoring and feedback to maintain manufacturing process stability and quality.

- R&D and Design Debug: Used during research and development to identify and resolve design or process flaws.

- Yield Management: Central to maximizing the number of functional chips produced per wafer by identifying and addressing yield detractors.

- Failure Analysis: Detailed investigation of specific failed devices to determine the root cause of malfunction.

- By End User:

- Foundries: Major consumers of inspection systems due to their high-volume, multi-customer manufacturing operations.

- Integrated Device Manufacturers (IDMs): Companies that design, manufacture, and sell their own chips, requiring comprehensive in-house inspection.

- Outsourced Semiconductor Assembly and Test (OSAT) Companies: Utilize inspection systems for post-fabrication assembly and testing processes.

- Research Institutions: Employ inspection tools for materials science research, device physics studies, and advanced technology development.

- By Industry Vertical:

- Consumer Electronics: Driving demand for high-volume, cost-effective inspection for smartphones, laptops, etc.

- Automotive: Requires highly reliable chips for ADAS, infotainment, and electric vehicles, necessitating rigorous inspection.

- Healthcare: Growing demand for specialized chips in medical devices and diagnostics.

- Industrial: Chips used in industrial automation, robotics, and smart factories.

- Telecommunication: Essential for 5G components, data centers, and network infrastructure.

- Aerospace & Defense: Demands ultra-high reliability and robust inspection for mission-critical applications.

- Others: Includes AI hardware, high-performance computing, quantum computing components, etc.

Regional Highlights

- Asia Pacific (APAC): The APAC region dominates the semiconductor defect inspection system market, primarily driven by the presence of major semiconductor manufacturing hubs, including Taiwan, South Korea, China, and Japan. These countries host leading foundries and IDMs that are at the forefront of advanced node development and high-volume production. Significant government support and continuous investments in new fabrication plants and technological upgrades further solidify APAC's leading position, making it the most critical region for market growth and technological adoption. The demand for advanced inspection tools is intrinsically linked to the expansion of existing fabs and the construction of new ones in this region.

- North America: North America represents a significant market for semiconductor defect inspection systems, characterized by strong research and development activities and the presence of leading semiconductor design companies and equipment manufacturers. The region focuses on cutting-edge technologies, including AI chips, advanced memory solutions, and specialized processors for high-performance computing. Investment in new fabrication facilities and the upgrading of existing ones to support domestic chip production initiatives are expected to drive consistent demand for advanced inspection tools, particularly those incorporating AI and advanced analytics for yield enhancement.

- Europe: Europe is a growing market, spurred by its strong focus on automotive electronics, industrial IoT, and a robust research ecosystem. Countries like Germany, France, and the Netherlands are investing in semiconductor manufacturing capabilities and R&D for advanced materials and specialized chips. The emphasis on developing highly reliable and efficient chips for critical applications, coupled with initiatives to strengthen domestic semiconductor supply chains, contributes to the demand for precise defect inspection systems. Collaboration between research institutions and industry players is also fostering innovation in inspection technologies within the region.

- Latin America, Middle East, and Africa (MEA): These regions currently hold a smaller share of the global market but are emerging with increasing investments in semiconductor manufacturing and assembly capabilities. While the focus remains more on mature process nodes and assembly services, growing industrialization, infrastructure development, and digital transformation initiatives are gradually creating demand for semiconductor components. This in turn drives a nascent but growing market for defect inspection systems, particularly for quality assurance in packaging and testing facilities. Strategic long-term investments in these regions could lead to future growth opportunities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Semiconductor Defect Inspection System Market.- Applied Materials

- KLA Corporation

- Tokyo Electron Limited

- Hitachi High-Tech Corporation

- JEOL Ltd.

- ASML Holding N.V.

- Carl Zeiss SMT GmbH

- Nova Measuring Instruments Ltd.

- Camtek Ltd.

- Onto Innovation

- Nidec Corporation

- Advantest Corporation

- ULVAC, Inc.

- Lasertec Corporation

- Accretech

- SEMES Co., Ltd.

- SCREEN Holdings Co., Ltd.

- Advantech Co., Ltd.

- Toray Engineering Co., Ltd.

- Unisantis Electronics Singapore Pte. Ltd.

Frequently Asked Questions

What is the primary function of a semiconductor defect inspection system?

The primary function of a semiconductor defect inspection system is to detect and characterize flaws, anomalies, or imperfections on semiconductor wafers, masks, or chips during various stages of the manufacturing process. These systems are crucial for ensuring the quality, reliability, and yield of integrated circuits by identifying critical defects that could impair device performance or cause failures.

How is AI transforming defect inspection in semiconductors?

AI is transforming defect inspection by enabling more precise and efficient defect detection, classification, and analysis. AI algorithms, especially deep learning, can differentiate between critical defects and benign noise, automate defect categorization, and predict potential process issues. This leads to reduced false positives, faster root cause analysis, and improved overall yield management, moving towards more autonomous and intelligent inspection workflows.

What are the key types of semiconductor defect inspection systems?

The key types of semiconductor defect inspection systems include optical inspection systems, which are high-throughput and versatile for various defect sizes, and e-beam (electron beam) inspection systems, which offer ultra-high resolution for detecting sub-nanometer defects and analyzing electrical characteristics. Hybrid systems combining these technologies are also emerging to provide comprehensive defect coverage.

What factors are driving the growth of the semiconductor defect inspection market?

The market's growth is primarily driven by the continuous miniaturization of semiconductor devices, increasing chip complexity, the burgeoning demand for high-performance computing and AI chips, and the critical need for enhanced manufacturing yields. The proliferation of semiconductors in diverse applications such as automotive, IoT, and 5G further fuels the demand for advanced and reliable inspection solutions.

What challenges does the semiconductor defect inspection market face?

The market faces several challenges, including the escalating technical difficulty of detecting increasingly smaller and more intricate defects, the high capital expenditure and operational costs associated with advanced inspection equipment, and the immense volume and complexity of data generated, requiring sophisticated data management and analysis capabilities. Additionally, the rapid pace of technological change and the shortage of skilled talent pose significant hurdles.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted