Next Generation Storage Device Market

Next Generation Storage Device Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705544 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

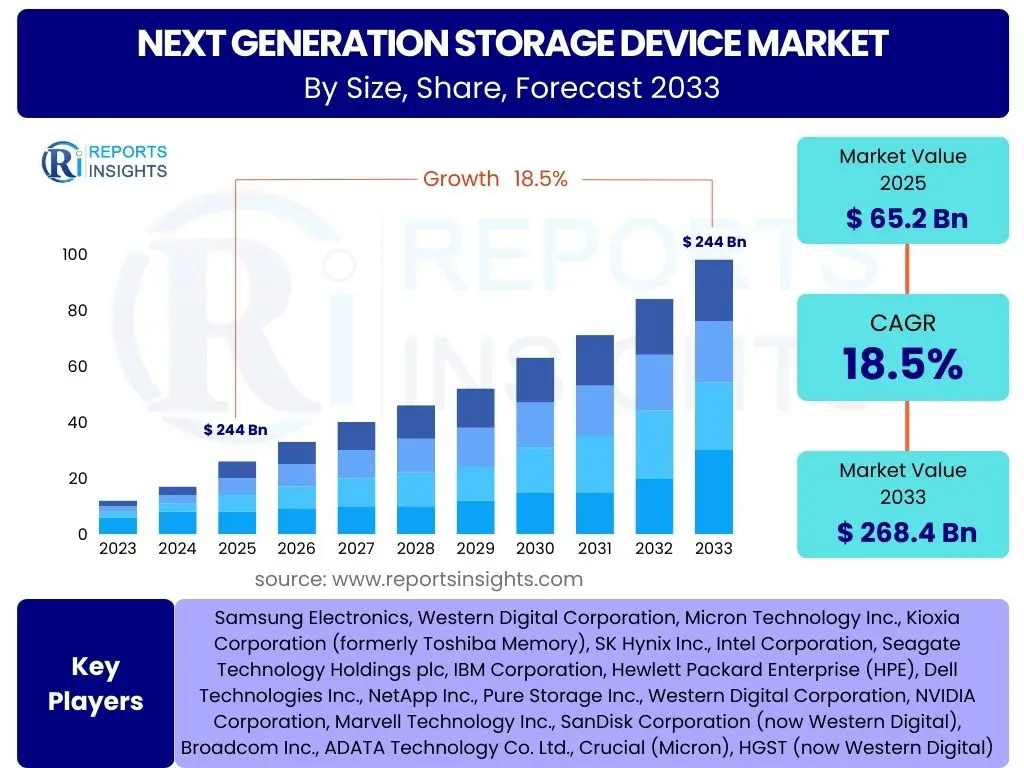

Next Generation Storage Device Market Size

According to Reports Insights Consulting Pvt Ltd, The Next Generation Storage Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 65.2 billion in 2025 and is projected to reach USD 268.4 billion by the end of the forecast period in 2033.

Key Next Generation Storage Device Market Trends & Insights

The Next Generation Storage Device market is significantly influenced by a confluence of evolving technological landscapes and escalating data demands. Users frequently inquire about the underlying shifts driving the adoption of these advanced storage solutions. Key trends indicate a decisive move towards faster, denser, and more energy-efficient storage, driven by applications requiring low latency and high throughput. The integration of advanced materials and architectures, such as 3D NAND and new memory types, alongside sophisticated software-defined storage solutions, is reshaping enterprise and cloud infrastructure.

Furthermore, the proliferation of artificial intelligence, machine learning, and the Internet of Things generates unprecedented volumes of data, necessitating storage solutions capable of handling massive datasets with speed and reliability. This demand fuels innovations in flash-based storage, persistent memory, and intelligent data management systems that can adapt to dynamic workloads. The emphasis is increasingly on solutions that not only store data but also enable quicker processing, analysis, and accessibility across diverse environments, from the core data center to the network edge.

- Exponential data growth necessitating higher capacity and performance.

- Shift from traditional HDDs to Solid State Drives (SSDs) and NVMe-based solutions.

- Emergence of persistent memory technologies (e.g., Optane) for improved data access.

- Increased adoption of software-defined storage (SDS) and hyperconverged infrastructure (HCI).

- Growing demand for storage at the edge to support IoT and real-time analytics.

- Advancements in 3D NAND and QLC (Quad-Level Cell) technologies for cost-effective, high-density storage.

- Development of DNA storage and other long-term archival solutions.

- Emphasis on energy efficiency and sustainability in data center operations.

AI Impact Analysis on Next Generation Storage Device

The profound impact of Artificial Intelligence (AI) on the Next Generation Storage Device market is a central theme of user inquiries. Users are keen to understand how AI's requirements for vast datasets, high-speed data access, and parallel processing capabilities are reshaping storage innovations. AI workloads, including machine learning training and inference, demand incredibly low latency and high IOPS (Input/Output Operations Per Second) to feed data to powerful GPUs and CPUs efficiently. This demand accelerates the adoption of NVMe SSDs, persistent memory, and other high-performance storage solutions, moving beyond traditional storage bottlenecks.

Moreover, AI is not only a consumer of advanced storage but also a catalyst for intelligent storage management. AI algorithms are being integrated into storage systems for predictive analytics, automated tiering, data deduplication, compression, and enhanced security. This leads to more efficient resource utilization, reduced operational overheads, and optimized data placement based on access patterns and performance requirements. The symbiotic relationship between AI and next-generation storage is expected to drive significant advancements, making storage infrastructures more agile, scalable, and responsive to complex computational demands across various industries.

- AI workloads necessitate high-performance, low-latency storage for data training and inference.

- Increased adoption of NVMe SSDs and parallel file systems to support AI/ML data pipelines.

- Growth of specialized storage solutions optimized for AI compute clusters.

- AI-driven data management solutions for intelligent tiering, data lifecycle management, and predictive maintenance.

- Demand for scalable and elastic storage architectures to accommodate growing AI datasets.

- Rise of edge AI drives need for robust, compact, high-performance storage at distributed locations.

Key Takeaways Next Generation Storage Device Market Size & Forecast

Common user questions regarding the Next Generation Storage Device market size and forecast reveal a strong interest in understanding the core growth drivers and the long-term trajectory of this sector. The primary takeaway is the significant expansion anticipated, fueled by the relentless growth of digital data and the increasing demand for faster, more efficient, and scalable data storage solutions. This market's trajectory is deeply intertwined with advancements in cloud computing, AI, IoT, and big data analytics, all of which necessitate robust underlying storage infrastructures. The shift away from traditional mechanical storage towards solid-state and emerging memory technologies is a fundamental aspect of this growth, promising enhanced performance and reliability.

Furthermore, the forecast underscores a critical trend: the convergence of hardware innovation with intelligent software solutions. This integration enables storage systems to not only handle larger volumes of data but also to manage it more effectively, optimizing costs and performance. The market's growth is not merely about capacity but also about speed, security, and the ability to seamlessly integrate with diverse computing environments. The substantial projected CAGR indicates a continuous investment in research and development, aiming to overcome current limitations and unlock new possibilities in data storage and retrieval, making it a pivotal component of the digital economy's infrastructure.

- Market projected for substantial growth, reaching USD 268.4 billion by 2033.

- CAGR of 18.5% signifies rapid adoption and innovation.

- Data explosion and digital transformation are primary market accelerators.

- Shift to high-performance, low-latency solutions like NVMe is a key driver.

- Integration of AI and machine learning into storage management enhances efficiency.

- Focus on energy efficiency and sustainability gaining prominence.

Next Generation Storage Device Market Drivers Analysis

The Next Generation Storage Device market is primarily propelled by the unprecedented global surge in data generation, driven by increasing digitalization across all sectors. The proliferation of IoT devices, the widespread adoption of cloud computing services, and the escalating demand for big data analytics solutions contribute significantly to this data deluge. Enterprises are continuously seeking more efficient, higher-performance storage solutions to manage, process, and extract value from their ever-growing datasets, fueling the demand for technologies beyond traditional storage paradigms.

Moreover, the rise of advanced computational workloads, particularly in Artificial Intelligence (AI) and Machine Learning (ML), necessitates ultra-fast and low-latency storage. These applications require instantaneous access to vast amounts of data for training models and real-time inference, making traditional storage a bottleneck. Consequently, the imperative to support such demanding applications acts as a powerful driver for the adoption of NVMe SSDs, persistent memory, and other next-generation storage architectures that can keep pace with modern processing capabilities.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Exponential Data Growth & Digital Transformation | +4.5% | Global, particularly APAC & North America | 2025-2033 |

| Increasing Adoption of Cloud Computing | +3.8% | North America, Europe, APAC | 2025-2033 |

| Rise of AI, ML, and Big Data Analytics | +4.2% | Global, especially tech-hubs | 2025-2033 |

| Demand for High-Performance Computing (HPC) | +3.0% | North America, Europe, China | 2025-2030 |

| Proliferation of IoT and Edge Computing | +2.5% | Global, particularly industrial sectors | 2027-2033 |

Next Generation Storage Device Market Restraints Analysis

Despite the robust growth prospects, the Next Generation Storage Device market faces several inherent restraints that could temper its expansion. One significant hurdle is the relatively high initial cost associated with advanced storage technologies, such as NVMe SSDs and persistent memory, compared to traditional HDD solutions. This elevated upfront investment can deter small and medium-sized enterprises (SMEs) or organizations with limited IT budgets from immediate adoption, thereby slowing market penetration in certain segments.

Another critical restraint involves the complexity of integrating these new storage solutions into existing legacy IT infrastructures. Many organizations operate with deeply entrenched systems that are not easily compatible with cutting-edge storage technologies, requiring significant investment in system overhauls, skilled personnel, and data migration. Furthermore, concerns regarding data security, privacy, and regulatory compliance, especially with increasing data volumes and distributed storage architectures, pose challenges for widespread adoption as organizations prioritize robust protection measures.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Cost of Advanced Solutions | -2.0% | Global, impacting SMEs | 2025-2030 |

| Complexity of Integration with Legacy Systems | -1.5% | Mature markets with established IT infrastructure | 2025-2033 |

| Data Security and Privacy Concerns | -1.0% | Global, particularly regulated industries | 2025-2033 |

| Supply Chain Volatility for Key Components | -0.8% | Global, affecting manufacturing hubs | 2025-2027 |

Next Generation Storage Device Market Opportunities Analysis

The Next Generation Storage Device market is replete with significant opportunities driven by emerging technologies and evolving digital landscapes. The increasing adoption of 5G networks globally is poised to create immense volumes of data at the edge, fostering a critical demand for high-performance, low-latency storage solutions closer to data sources. This presents a substantial opportunity for specialized edge storage devices that can support real-time analytics, IoT applications, and distributed AI workloads without relying heavily on centralized data centers.

Furthermore, the ongoing research and development in novel memory technologies beyond NAND flash, such as Resistive RAM (RRAM), Phase-change Memory (PCM), and Magnetic RAM (MRAM), offer promising avenues for breakthrough performance and density improvements. These emerging technologies could unlock new possibilities for in-memory computing and ultra-fast non-volatile storage, addressing the bottlenecks of current architectures. The growing need for efficient long-term archival solutions, including the potential for DNA-based storage, also presents a nascent yet potentially transformative opportunity for addressing the escalating challenge of preserving vast digital heritage over extended periods.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of 5G Networks & Edge Computing | +3.5% | Global, especially developing regions | 2026-2033 |

| Development of Novel Memory Technologies (e.g., RRAM, PCM) | +2.8% | North America, APAC (R&D hubs) | 2028-2033 |

| Demand for Archival and Long-Term Storage Solutions | +2.0% | Global, particularly enterprises & research institutions | 2025-2033 |

| Growth of Data Centers and Hyperscale Cloud Providers | +1.5% | North America, Europe, APAC | 2025-2033 |

Next Generation Storage Device Market Challenges Impact Analysis

The Next Generation Storage Device market faces significant challenges, primarily related to the continuous demand for higher performance within shrinking form factors, often leading to thermal management and power consumption issues. As storage density increases and speeds accelerate, dissipating heat effectively becomes a complex engineering challenge, impacting device reliability and operational costs in data centers. Balancing performance gains with energy efficiency is a persistent hurdle for manufacturers and system integrators.

Another major challenge involves the rapidly evolving technological landscape, which can lead to rapid obsolescence of current-generation technologies. This necessitates continuous research and development investments, placing financial strain on market players. Furthermore, maintaining data integrity and ensuring robust data recovery mechanisms for extremely dense and fast storage technologies is complex, requiring sophisticated error correction and redundancy protocols. The increasing sophistication of cyber threats also poses a significant challenge, demanding advanced security features embedded directly into storage hardware and software to protect sensitive information.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Thermal Management & Power Consumption Issues | -1.2% | Global, impacting data centers | 2025-2033 |

| Rapid Technological Obsolescence | -0.9% | Global, impacting manufacturers & consumers | 2025-2030 |

| Ensuring Data Integrity & Recovery for Dense Storage | -0.7% | Global, impacting all sectors | 2025-2033 |

| Cybersecurity Risks & Data Protection Requirements | -0.5% | Global, highly regulated industries | 2025-2033 |

Next Generation Storage Device Market - Updated Report Scope

This report offers a detailed analysis of the Next Generation Storage Device market, encompassing its current landscape, projected growth trajectories, and critical factors influencing market dynamics. It provides an in-depth exploration of technological advancements, market segmentation across various dimensions, regional insights, and the competitive strategies of key industry players. The scope includes an examination of market drivers, restraints, opportunities, and challenges, providing a comprehensive understanding of the forces shaping the market's future from 2025 to 2033.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 65.2 Billion |

| Market Forecast in 2033 | USD 268.4 Billion |

| Growth Rate | 18.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Samsung Electronics, Western Digital Corporation, Micron Technology Inc., Kioxia Corporation (formerly Toshiba Memory), SK Hynix Inc., Intel Corporation, Seagate Technology Holdings plc, IBM Corporation, Hewlett Packard Enterprise (HPE), Dell Technologies Inc., NetApp Inc., Pure Storage Inc., Western Digital Corporation, NVIDIA Corporation, Marvell Technology Inc., SanDisk Corporation (now Western Digital), Broadcom Inc., ADATA Technology Co. Ltd., Crucial (Micron), HGST (now Western Digital) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Next Generation Storage Device market is broadly segmented across several critical dimensions, allowing for a granular understanding of its diverse components and drivers. These segmentations by technology, storage type, end-user, application, and interface highlight the varied demands and innovative solutions emerging within the industry. The rapid evolution of storage technologies, from high-performance NVMe SSDs and persistent memory to advanced magnetic and nascent DNA storage, reflects the industry's response to escalating data volumes and performance requirements across different use cases.

The distinction between storage types like DAS, NAS, SAN, and the expanding domain of cloud storage underscores the architectural choices enterprises and consumers make based on scalability, accessibility, and cost. Furthermore, the segmentation by end-user demonstrates the widespread applicability of next-generation storage across enterprise data centers, cloud providers, and specialized sectors like automotive and healthcare, each presenting unique demands for capacity, speed, and reliability. This comprehensive segmentation provides a robust framework for market analysis, identifying key growth areas and investment opportunities within the intricate ecosystem of modern data storage.

- By Technology: Solid State Drive (SSD), NVMe SSD, Hybrid HDD, Persistent Memory (e.g., Optane, 3D XPoint), Magnetic Storage (e.g., HAMR, MAMR), DNA Storage, Holographic Storage, Quantum Storage

- By Storage Type: Direct Attached Storage (DAS), Network Attached Storage (NAS), Storage Area Network (SAN), Cloud Storage

- By End-User: Enterprise (Data Centers, Cloud Providers, Financial Services, Healthcare, Government), Consumer (Gaming, Personal Computing, Mobile Devices), Telecommunications, Automotive, Industrial, Research & Education

- By Application: Archiving & Backup, Data Processing, High-Performance Computing, AI/ML Workloads, Virtualization, IoT & Edge Analytics

- By Interface: SATA, SAS, PCIe, Fibre Channel, Ethernet

Regional Highlights

- North America: Dominates the market due to early adoption of advanced technologies, presence of major tech companies, significant investments in data centers and cloud infrastructure, and strong demand from AI/ML and HPC sectors. The region benefits from robust R&D and a highly skilled workforce.

- Europe: Exhibits significant growth, driven by increasing digital transformation initiatives, stringent data privacy regulations (e.g., GDPR) necessitating localized storage, and growing adoption of cloud services. Countries like Germany, the UK, and France are key contributors with strong manufacturing and enterprise sectors.

- Asia Pacific (APAC): Poised for the highest growth rate, fueled by rapid digitalization, expanding IT infrastructure, increasing smartphone penetration, and massive data generation from emerging economies like China and India. Government initiatives promoting digital economies and smart cities also contribute to market expansion.

- Latin America: Shows emerging potential with growing internet penetration and increasing adoption of cloud services by businesses. Economic development and foreign investments in IT infrastructure are key factors, albeit with slower adoption rates compared to developed regions.

- Middle East and Africa (MEA): Expected to witness steady growth, driven by diversification efforts from oil-dependent economies into technology, significant government investments in smart city projects, and the rise of digital services. However, challenges related to infrastructure and skilled labor persist.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Next Generation Storage Device Market.- Samsung Electronics

- Western Digital Corporation

- Micron Technology Inc.

- Kioxia Corporation (formerly Toshiba Memory)

- SK Hynix Inc.

- Intel Corporation

- Seagate Technology Holdings plc

- IBM Corporation

- Hewlett Packard Enterprise (HPE)

- Dell Technologies Inc.

- NetApp Inc.

- Pure Storage Inc.

- NVIDIA Corporation

- Marvell Technology Inc.

- SanDisk Corporation (now Western Digital)

- Broadcom Inc.

- ADATA Technology Co. Ltd.

- Crucial (Micron)

- HGST (now Western Digital)

Frequently Asked Questions

Analyze common user questions about the Next Generation Storage Device market and generate a concise list of summarized FAQs reflecting key topics and concerns.What defines a "Next Generation Storage Device" and how does it differ from traditional storage?

Next Generation Storage Devices are advanced solutions offering significantly higher performance, capacity, and efficiency than traditional HDDs. They utilize technologies like NVMe, 3D NAND, and persistent memory, providing ultra-low latency, high throughput, and often integrating with AI for intelligent data management, unlike older mechanical or slower flash storage.

What are the primary drivers of growth for the Next Generation Storage Device market?

The market's growth is primarily driven by exponential data generation, the pervasive adoption of cloud computing, the increasing demand from AI/ML and High-Performance Computing (HPC) workloads, and the expansion of IoT and edge computing requiring faster, more distributed storage solutions.

How is AI impacting the development and adoption of these new storage technologies?

AI impacts storage by demanding high-performance, low-latency devices for data-intensive workloads like training and inference. Conversely, AI is also being integrated into storage systems for intelligent data management, optimizing performance, automating tiering, and enhancing efficiency across the storage infrastructure.

What are the main challenges facing the Next Generation Storage Device market?

Key challenges include the high initial cost of advanced solutions, complex integration with legacy IT systems, significant thermal management and power consumption concerns, rapid technological obsolescence requiring continuous R&D, and ensuring robust data integrity and cybersecurity for increasingly dense storage.

Which regions are leading the adoption of Next Generation Storage Devices?

North America currently leads in adoption due to robust tech infrastructure and early innovation. Asia Pacific (APAC) is projected for the highest growth, driven by rapid digitalization and expanding economies, while Europe also shows strong adoption spurred by digital transformation initiatives and data privacy regulations.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted