Semiconductor Manufacturing Equipment Market

Semiconductor Manufacturing Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705634 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

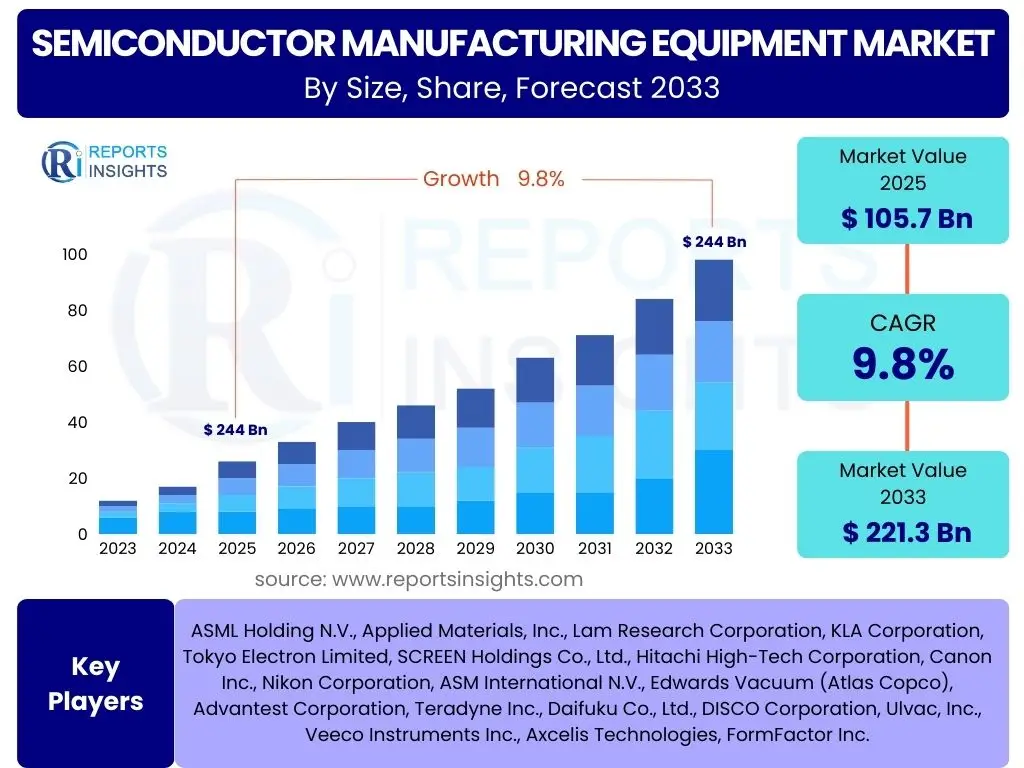

Semiconductor Manufacturing Equipment Market Size

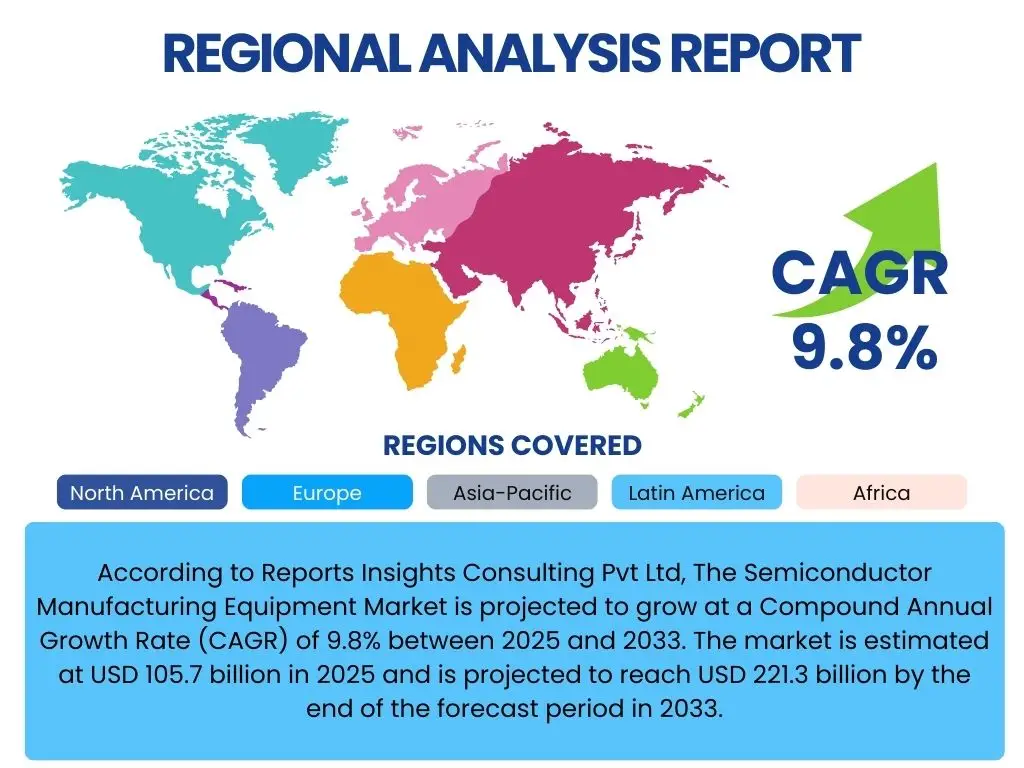

According to Reports Insights Consulting Pvt Ltd, The Semiconductor Manufacturing Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. The market is estimated at USD 105.7 billion in 2025 and is projected to reach USD 221.3 billion by the end of the forecast period in 2033.

Key Semiconductor Manufacturing Equipment Market Trends & Insights

User inquiries frequently highlight the accelerating pace of technological innovation and the increasing complexity of semiconductor manufacturing. Key areas of interest include the shift towards advanced packaging solutions, the integration of artificial intelligence and machine learning in fabrication processes, and the growing emphasis on sustainable manufacturing practices. The industry is also witnessing a significant geographical diversification of manufacturing capabilities, driven by geopolitical considerations and the desire for supply chain resilience.

Another prominent trend involves the miniaturization of components, pushing the boundaries of lithography and deposition technologies. This drive for higher transistor density and improved performance necessitates continuous advancements in equipment capabilities, including extreme ultraviolet (EUV) lithography and atomic layer deposition (ALD). Furthermore, the increasing demand for specialized chips for emerging applications like AI, 5G, and automotive electronics is fueling investment in diverse equipment categories.

- Advanced packaging technologies adoption for performance and power efficiency.

- Integration of AI, ML, and automation for smart manufacturing.

- Increased focus on sustainable and energy-efficient equipment solutions.

- Diversification of global manufacturing hubs and supply chains.

- Ramp-up of advanced lithography, including EUV, and deposition techniques.

- Surging demand for specialized equipment for SiC and GaN power devices.

AI Impact Analysis on Semiconductor Manufacturing Equipment

Common user questions regarding AI's influence on semiconductor manufacturing equipment revolve around its potential to enhance operational efficiency, improve yield rates, and reduce manufacturing costs. Users are particularly interested in how AI can optimize complex processes like lithography and etching, enable predictive maintenance for critical equipment, and streamline quality control. There is a strong expectation that AI will be a transformative force, leading to more autonomous and intelligent fabs.

Beyond process optimization, AI is also anticipated to play a crucial role in equipment design and development, accelerating innovation cycles. The ability of AI to analyze vast datasets generated during manufacturing allows for immediate identification of anomalies and opportunities for process refinement, significantly improving equipment performance and lifespan. This integration is expected to reduce human error, enhance throughput, and provide a competitive edge in an increasingly complex manufacturing landscape.

- Optimized equipment parameters for enhanced yield and throughput.

- Predictive maintenance leading to reduced downtime and increased equipment longevity.

- Automated defect detection and classification for improved quality control.

- Accelerated R&D cycles for new equipment design and material innovation.

- Intelligent fab management and scheduling for improved operational efficiency.

Key Takeaways Semiconductor Manufacturing Equipment Market Size & Forecast

Analysis of user inquiries about the market forecast reveals a strong interest in the sustained growth trajectory of the semiconductor manufacturing equipment market, primarily driven by persistent demand for advanced electronics. Stakeholders are keen to understand the specific segments poised for significant expansion, such as advanced packaging and AI-driven process equipment. The forecast indicates that despite potential cyclical fluctuations inherent to the semiconductor industry, the long-term outlook remains robust, underpinned by foundational technological shifts.

A key takeaway from the market forecast is the critical role of capital expenditure by chip manufacturers in fueling equipment demand. Geopolitical strategies, including government incentives for domestic semiconductor production, are also significantly influencing investment patterns and shaping regional market dynamics. The increasing complexity of chip designs and the imperative for higher performance are consistently pushing the boundaries of current manufacturing capabilities, ensuring continued demand for sophisticated and innovative equipment solutions throughout the forecast period.

- Sustained market growth driven by global digital transformation and advanced technology adoption.

- Significant capital expenditure by chipmakers worldwide to expand and upgrade fabs.

- Critical role of advanced packaging and AI-enabled equipment in future growth.

- Geopolitical initiatives and supply chain resilience shaping regional investment.

- Continuous innovation in process technology essential for market leadership.

Semiconductor Manufacturing Equipment Market Drivers Analysis

The global demand for advanced electronic devices is a primary catalyst for the semiconductor manufacturing equipment market. The proliferation of 5G and future 6G networks, coupled with the rapid expansion of artificial intelligence (AI) and machine learning (ML) applications across various industries, necessitates a continuous increase in semiconductor production capacity and technological sophistication. This drives significant investment in new and upgraded manufacturing equipment capable of handling increasingly complex chip designs and higher volumes.

Furthermore, the automotive industry's accelerating transition towards electric vehicles (EVs) and autonomous driving systems is a major demand driver. Modern vehicles require a growing number of sophisticated semiconductors for power management, sensors, infotainment, and advanced driver-assistance systems (ADAS). Government initiatives and subsidies aimed at boosting domestic semiconductor manufacturing capabilities in key regions also play a crucial role, mitigating supply chain vulnerabilities and fostering regional market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Surging Demand for Advanced Electronics (5G, AI, IoT) | +2.5% | Global, especially APAC, North America | Long-term (2025-2033) |

| Growth in Automotive Electronics & EVs | +1.8% | Europe, North America, China, Japan | Mid to Long-term (2025-2033) |

| Government Initiatives & Subsidies for Domestic Production | +1.5% | USA, EU, China, Japan, South Korea, India | Mid-term (2025-2029) |

| Expansion of Data Centers and Cloud Computing Infrastructure | +1.2% | North America, Europe, China | Long-term (2025-2033) |

| Advancements in Advanced Packaging Technologies | +1.0% | Global, particularly South Korea, Taiwan, Japan | Long-term (2025-2033) |

Semiconductor Manufacturing Equipment Market Restraints Analysis

The semiconductor manufacturing equipment market faces significant restraints, notably the inherently high capital expenditure required for establishing and upgrading fabrication facilities. The immense costs associated with cutting-edge equipment, R&D, and maintaining cleanroom environments can limit investments, particularly for smaller players or during periods of economic uncertainty. This high barrier to entry contributes to market consolidation and makes it challenging for new entrants.

Geopolitical tensions and trade disputes also pose a substantial restraint, leading to uncertainties in global supply chains and potentially restricting the flow of critical equipment and components. Export controls and tariffs can disrupt manufacturing processes and delay equipment deployment. Furthermore, the cyclical nature of the semiconductor industry, characterized by boom-and-bust cycles, can lead to periods of oversupply or undersupply, impacting equipment demand and creating volatility for manufacturers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure & R&D Costs | -1.5% | Global | Long-term (2025-2033) |

| Geopolitical Tensions & Trade Disputes | -1.2% | Global, particularly USA-China, Europe | Mid-term (2025-2029) |

| Cyclical Nature of the Semiconductor Industry | -1.0% | Global | Short to Mid-term (2025-2027) |

| Skilled Labor Shortages | -0.8% | North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Environmental Regulations & Compliance Costs | -0.5% | Europe, North America, Japan | Long-term (2025-2033) |

Semiconductor Manufacturing Equipment Market Opportunities Analysis

The expansion into emerging technologies presents significant opportunities for the semiconductor manufacturing equipment market. The increasing adoption of silicon carbide (SiC) and gallium nitride (GaN) for power electronics and radio frequency (RF) applications, particularly in EVs, industrial power systems, and 5G infrastructure, requires specialized equipment that differs from traditional silicon processing. This creates a new niche for equipment manufacturers to innovate and supply dedicated solutions for these wide bandgap (WBG) materials.

Furthermore, the ongoing global trend of reshoring semiconductor manufacturing and establishing new fabrication plants (fabs) in various regions, driven by supply chain security concerns and government incentives, offers substantial growth opportunities. These new fab constructions necessitate large-scale equipment procurement. Additionally, the increasing complexity of chip designs and the demand for higher integration density open doors for advancements in metrology, inspection, and process control equipment, ensuring yield and quality in advanced nodes.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emerging Technologies (SiC, GaN, Quantum Computing) | +2.0% | Global, particularly North America, Europe, Japan | Long-term (2025-2033) |

| New Fab Construction & Expansion Projects Globally | +1.8% | USA, Europe, Japan, India, Southeast Asia | Mid to Long-term (2025-2033) |

| Growth in Advanced Metrology, Inspection & Process Control | +1.5% | Global | Long-term (2025-2033) |

| Development of Chiplets and Heterogeneous Integration | +1.0% | Global | Mid to Long-term (2025-2033) |

| Increased Investment in Sustainable & Green Manufacturing | +0.7% | Europe, North America, Japan | Long-term (2025-2033) |

Semiconductor Manufacturing Equipment Market Challenges Impact Analysis

The semiconductor manufacturing equipment market faces significant challenges, particularly related to the rapid pace of technological obsolescence. As chip designs become more intricate and smaller, equipment manufacturers must constantly invest heavily in research and development to keep pace with evolving process nodes. This creates pressure to innovate quickly, and equipment can become outdated rapidly, impacting investment returns and increasing R&D intensity.

Maintaining a highly skilled workforce is another pressing challenge. The specialized nature of semiconductor equipment manufacturing demands engineers, technicians, and researchers with advanced expertise in diverse fields such as physics, materials science, and software engineering. The global shortage of such talent can hinder innovation, production capacity, and equipment servicing. Additionally, the industry's susceptibility to geopolitical shifts and trade policies can disrupt supply chains and market access, complicating long-term planning and investment strategies for equipment manufacturers.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence & High R&D Intensity | -1.3% | Global | Long-term (2025-2033) |

| Shortage of Highly Skilled Workforce | -1.0% | Global, particularly developed economies | Long-term (2025-2033) |

| Complex Global Supply Chain Dependencies | -0.8% | Global | Mid-term (2025-2029) |

| Intensifying Geopolitical Risks & Protectionism | -0.7% | Global, particularly USA, China, EU | Mid-term (2025-2029) |

| Fluctuations in Raw Material Prices | -0.4% | Global | Short-term (2025-2026) |

Semiconductor Manufacturing Equipment Market - Updated Report Scope

This report offers a detailed analysis of the Semiconductor Manufacturing Equipment market, providing a comprehensive overview of its size, growth trajectory, and key dynamics. It delves into the various segments, identifying major drivers, restraints, opportunities, and challenges influencing market expansion. The scope encompasses a thorough examination of technological advancements, regional trends, and the competitive landscape, delivering actionable insights for stakeholders seeking to navigate this complex and rapidly evolving industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 105.7 Billion |

| Market Forecast in 2033 | USD 221.3 Billion |

| Growth Rate | 9.8% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ASML Holding N.V., Applied Materials, Inc., Lam Research Corporation, KLA Corporation, Tokyo Electron Limited, SCREEN Holdings Co., Ltd., Hitachi High-Tech Corporation, Canon Inc., Nikon Corporation, ASM International N.V., Edwards Vacuum (Atlas Copco), Advantest Corporation, Teradyne Inc., Daifuku Co., Ltd., DISCO Corporation, Ulvac, Inc., Veeco Instruments Inc., Axcelis Technologies, FormFactor Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The semiconductor manufacturing equipment market is comprehensively segmented to provide granular insights into its diverse components and applications. Key segmentations include equipment type, which differentiates between the intricate processes involved in front-end (wafer fabrication) and back-end (assembly, packaging, and testing) manufacturing. Each of these broad categories further branches into specialized equipment, reflecting the complexity and precision required at every stage of semiconductor production.

Further segmentation by application highlights the varied end-users of semiconductor manufacturing equipment, such as foundries that produce chips for multiple clients, memory manufacturers focusing on DRAM and NAND, and integrated device manufacturers (IDMs) that design, manufacture, and sell their own chips. The market is also analyzed based on end-use industries, including consumer electronics, automotive, and industrial sectors, illustrating how demand from these diverse industries drives the equipment market. This multi-faceted segmentation allows for a detailed understanding of market dynamics across different technological processes and end-user demands.

- By Equipment Type:

- Front-End Equipment (Lithography, Deposition, Etching, Cleaning, Ion Implantation, Metrology & Inspection, Diffusion & Oxidation)

- Back-End Equipment (Assembly & Packaging, Test Equipment)

- By Application:

- Foundry

- Memory (DRAM, NAND)

- Integrated Device Manufacturers (IDMs)

- OSAT (Outsourced Semiconductor Assembly and Test)

- By End-Use Industry:

- Consumer Electronics

- Automotive

- Industrial

- IT & Telecommunication

- Healthcare

- Aerospace & Defense

Regional Highlights

- Asia Pacific (APAC): Dominates the market due to the presence of major semiconductor manufacturing hubs in Taiwan, South Korea, China, and Japan. Significant investments in new fabs and advanced technology adoption drive unparalleled growth. China is rapidly expanding its domestic capabilities, while Taiwan and South Korea remain at the forefront of advanced node production.

- North America: A key region for R&D and equipment innovation, driven by strong government support and initiatives like the CHIPS Act. The region is witnessing reshoring efforts and substantial investments in new fabs, particularly in the U.S., focusing on advanced logic and specialty semiconductors.

- Europe: Growing emphasis on strengthening regional semiconductor supply chains with initiatives like the European Chips Act. Germany, France, and Ireland are key centers for research, development, and manufacturing, particularly in automotive and industrial semiconductors.

- Latin America & Middle East and Africa (MEA): Emerging regions with nascent but growing semiconductor industries. While smaller in market share, increasing digitalization and government interest in local manufacturing could spur future investments in equipment.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Semiconductor Manufacturing Equipment Market.- ASML Holding N.V.

- Applied Materials, Inc.

- Lam Research Corporation

- KLA Corporation

- Tokyo Electron Limited

- SCREEN Holdings Co., Ltd.

- Hitachi High-Tech Corporation

- Canon Inc.

- Nikon Corporation

- ASM International N.V.

- Edwards Vacuum (Atlas Copco)

- Advantest Corporation

- Teradyne Inc.

- Daifuku Co., Ltd.

- DISCO Corporation

- Ulvac, Inc.

- Veeco Instruments Inc.

- Axcelis Technologies

- FormFactor Inc.

Frequently Asked Questions

What is the projected growth rate for the Semiconductor Manufacturing Equipment market?

The Semiconductor Manufacturing Equipment market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033.

What are the primary drivers of growth in this market?

Key growth drivers include the surging global demand for advanced electronics (5G, AI, IoT), the rapid expansion of automotive electronics and electric vehicles (EVs), and significant government initiatives and subsidies aimed at boosting domestic semiconductor manufacturing capabilities.

How is AI impacting the Semiconductor Manufacturing Equipment sector?

AI is significantly impacting the sector by enabling optimized equipment parameters for enhanced yield, predictive maintenance to reduce downtime, automated defect detection, accelerated R&D cycles for new equipment design, and intelligent fab management for improved operational efficiency.

Which regions are expected to dominate the Semiconductor Manufacturing Equipment market?

The Asia Pacific (APAC) region is expected to dominate due to major manufacturing hubs in Taiwan, South Korea, China, and Japan. North America and Europe are also significant, driven by strong R&D, innovation, and government-led reshoring initiatives.

What are the main challenges faced by the market?

Major challenges include rapid technological obsolescence and high R&D intensity, a shortage of highly skilled workers, complex global supply chain dependencies, and increasing geopolitical risks and protectionist trade policies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted