Semiconductor Chip Market

Semiconductor Chip Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705911 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

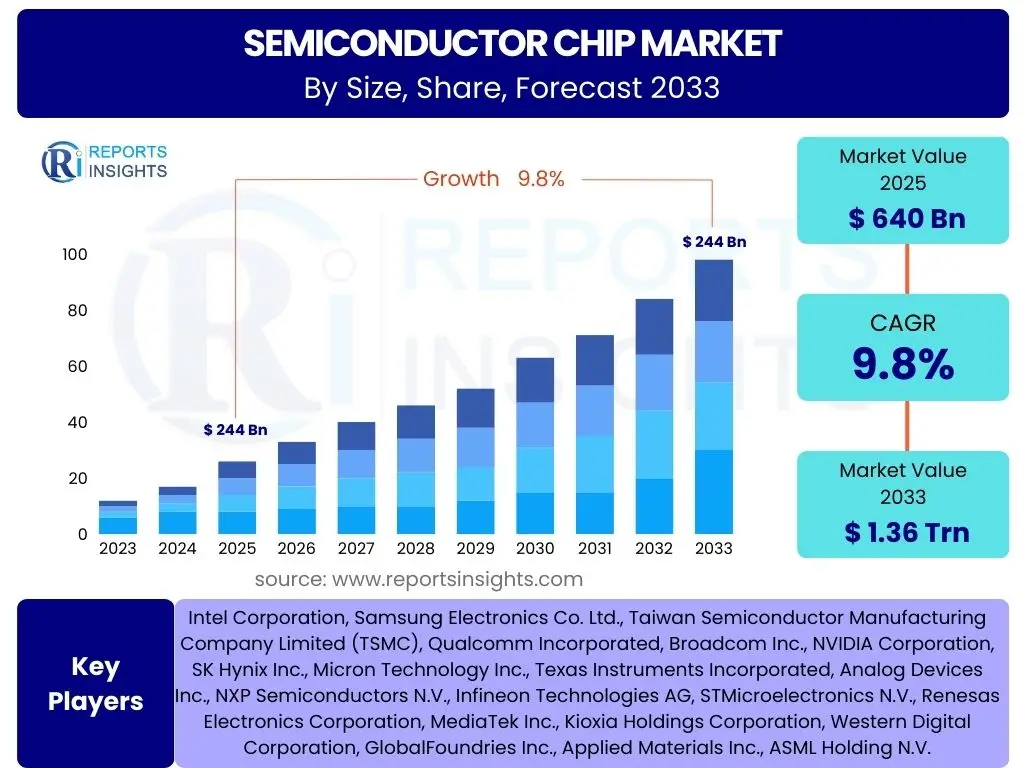

Semiconductor Chip Market Size

According to Reports Insights Consulting Pvt Ltd, The Semiconductor Chip Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. The market is estimated at USD 640 Billion in 2025 and is projected to reach USD 1.36 Trillion by the end of the forecast period in 2033.

Key Semiconductor Chip Market Trends & Insights

The semiconductor chip market is experiencing transformative trends driven by advancements in artificial intelligence, pervasive connectivity, and the increasing demand for high-performance computing. Users frequently inquire about the impact of miniaturization, advanced packaging, and the rise of specialized chips for emerging applications. Furthermore, the market is profoundly shaped by global geopolitical dynamics, requiring enhanced supply chain resilience and localized manufacturing strategies. These trends collectively underscore a rapid evolution in chip design, production, and application.

- Exponential growth in demand for specialized AI and High-Performance Computing (HPC) chips.

- Proliferation of 5G/6G technologies driving demand for advanced RF and baseband processors.

- Significant expansion of automotive electronics due to electric vehicles and autonomous driving.

- Increasing adoption of advanced packaging technologies like chiplets and 3D stacking.

- Emphasis on supply chain diversification and regional manufacturing resilience.

- Rising focus on energy-efficient chips and sustainable manufacturing practices.

- Integration of advanced sensing and IoT capabilities across diverse industries.

AI Impact Analysis on Semiconductor Chip

Common user questions regarding AI's impact on the semiconductor chip market often revolve around how AI drives demand, the types of chips specifically required for AI workloads, and the influence of AI on chip design and manufacturing processes. AI stands as a pivotal catalyst, fundamentally reshaping the semiconductor landscape by necessitating increasingly powerful, specialized, and energy-efficient processing units. This surge in demand spans from data centers and cloud computing to edge devices, directly influencing research and development priorities, manufacturing capacities, and market growth trajectories. The integration of AI also extends to optimizing the very processes of chip design and fabrication, promising greater efficiency and innovation.

- Massive increase in demand for Graphics Processing Units (GPUs), Neural Processing Units (NPUs), and Application-Specific Integrated Circuits (ASICs) tailored for AI workloads.

- Acceleration of AI inference at the edge, leading to a rise in demand for power-efficient AI chips in IoT devices, smartphones, and smart sensors.

- Adoption of AI and machine learning techniques in Electronic Design Automation (EDA) tools, optimizing chip design, verification, and manufacturing processes.

- Growing investment in advanced memory solutions (e.g., HBM) to support the data-intensive nature of AI applications.

- Development of specialized AI hardware architectures (e.g., neuromorphic chips) aiming for greater efficiency and new computing paradigms.

Key Takeaways Semiconductor Chip Market Size & Forecast

Key takeaways from the semiconductor chip market size and forecast consistently highlight robust growth, primarily propelled by expanding digital transformation initiatives and the relentless demand for computational power across diverse sectors. Users often inquire about the primary drivers sustaining this growth and the resilience of the market against economic fluctuations. The forecast indicates that while the market faces cyclical tendencies and geopolitical pressures, fundamental technological advancements in AI, IoT, and high-performance computing provide a strong underlying impetus. Strategic investments in R&D and manufacturing capacity are paramount to capitalizing on this sustained growth trajectory and mitigating potential disruptions.

- The market is poised for significant expansion, driven by widespread digitalization and emerging technologies.

- Growth is largely attributable to the escalating demand from automotive, AI/ML, 5G, and IoT sectors.

- Geopolitical factors and trade policies increasingly influence supply chain strategies and regional manufacturing investments.

- Continuous innovation in chip design and advanced manufacturing processes remains critical for market leadership.

- The industry is highly capital-intensive, with long lead times for new fabrication facilities, impacting supply responsiveness.

Semiconductor Chip Market Drivers Analysis

The semiconductor chip market is profoundly influenced by several key drivers that collectively propel its growth and innovation. Foremost among these is the escalating global demand for advanced electronic devices across consumer, industrial, and automotive sectors. The pervasive integration of digital technologies into everyday life, from smart home appliances to complex industrial automation systems, necessitates ever more sophisticated and powerful chips. Furthermore, the rapid expansion of data centers and cloud computing infrastructure requires high-performance processors and memory solutions to handle vast amounts of data processing and storage, thereby creating sustained demand for semiconductor components.

Technological advancements, such as the rollout of 5G networks, the proliferation of Artificial Intelligence (AI) and Machine Learning (ML), and the development of the Internet of Things (IoT), are also significant drivers. These innovations not only create new application areas for semiconductors but also demand higher levels of integration, miniaturization, and energy efficiency. Additionally, government initiatives and strategic investments in national semiconductor capabilities, particularly in regions aiming for technological sovereignty, provide significant impetus to market growth by fostering domestic research, development, and manufacturing capacity. These multifaceted drivers ensure a resilient and expanding market for semiconductor chips.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Digitalization and Connectivity Expansion | +1.5% | Global | Long-term (2025-2033) |

| Proliferation of AI and Machine Learning Technologies | +1.8% | Global, North America, APAC (China, Korea) | Long-term (2025-2033) |

| Growth in Automotive Electronics and Electric Vehicles | +1.2% | Europe, North America, APAC (Japan, China) | Medium-term (2025-2030) |

| Expansion of Data Centers and Cloud Computing | +1.0% | North America, Europe, APAC | Long-term (2025-2033) |

| IoT Device Proliferation Across Industries | +0.9% | Global | Long-term (2025-2033) |

| Government Support and Strategic Investments | +0.8% | North America, Europe, APAC | Medium-term (2025-2030) |

Semiconductor Chip Market Restraints Analysis

Despite robust growth prospects, the semiconductor chip market faces several significant restraints that can impede its expansion. One primary concern is the exceptionally high capital expenditure required for establishing and upgrading fabrication plants (fabs). The cost of building a state-of-the-art foundry can run into tens of billions of dollars, creating substantial barriers to entry and limiting the number of major players capable of leading-edge production. This high investment risk is compounded by the rapid pace of technological obsolescence, where advanced equipment can become outdated within a few years, necessitating continuous and costly upgrades.

Furthermore, geopolitical tensions and trade disputes pose a considerable restraint, particularly given the globalized nature of the semiconductor supply chain. Restrictions on technology transfer, export controls, and tariffs can disrupt international collaboration, limit market access, and force costly reconfigurations of supply networks. The cyclical nature of the semiconductor industry, characterized by periods of oversupply and undersupply, also introduces volatility and makes long-term planning challenging. Lastly, the increasing complexity of chip design and manufacturing, coupled with a growing global talent shortage in highly specialized engineering fields, can hinder innovation and delay product development, collectively serving as notable brakes on market momentum.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure for Fabrication Plants | -1.5% | Global | Long-term (Ongoing) |

| Geopolitical Tensions and Trade Barriers | -1.2% | Global, particularly US, China, Europe | Medium-term (2025-2030) |

| Cyclical Nature of the Semiconductor Industry | -0.9% | Global | Short to Medium-term (Recurring) |

| Supply Chain Vulnerabilities and Disruptions | -0.8% | Global | Short-term (Ongoing) |

| Shortage of Skilled Workforce and Talent Drain | -0.7% | North America, Europe, APAC | Long-term (Ongoing) |

Semiconductor Chip Market Opportunities Analysis

Significant opportunities abound within the semiconductor chip market, driven by evolving technological paradigms and expanding application domains. The development of advanced packaging technologies, such as chiplets and 3D stacking, represents a major avenue for innovation, enabling greater integration, improved performance, and reduced power consumption without solely relying on traditional transistor scaling. These advancements facilitate the creation of highly customized and efficient solutions for specialized workloads, particularly in AI and high-performance computing, where traditional monolithic chip designs face increasing limitations.

Emerging technologies like quantum computing and neuromorphic computing present long-term opportunities for fundamentally new chip architectures and materials, although their commercialization is still nascent. Furthermore, the increasing focus on sustainability and green manufacturing practices within the industry creates opportunities for developing energy-efficient designs and environmentally friendly production processes, attracting investments and appealing to a growing segment of environmentally conscious consumers and businesses. The expansion into untapped and emerging markets, particularly in developing economies with growing digital infrastructure, also represents a substantial growth opportunity, promising new demand centers for semiconductor products.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advanced Packaging and Chiplet Architectures | +1.8% | Global, particularly North America, APAC (Taiwan, Korea) | Long-term (2025-2033) |

| Development of Next-Gen Materials (e.g., GaN, SiC) | +1.4% | Global, Europe, APAC (Japan) | Medium to Long-term (2025-2033) |

| Growth in Green Semiconductor Manufacturing | +1.0% | Global, particularly Europe, North America | Long-term (2025-2033) |

| Expansion into Emerging Markets and Digitalization | +0.9% | Latin America, Africa, Southeast Asia | Long-term (2025-2033) |

| Rise of Neuromorphic and Quantum Computing Research | +0.7% | North America, Europe, APAC (China, Japan) | Long-term (Post-2030) |

Semiconductor Chip Market Challenges Impact Analysis

The semiconductor chip market navigates several complex challenges that demand strategic responses from industry players. One significant challenge is the escalating cost and complexity of designing and manufacturing chips at advanced process nodes. As transistor sizes shrink and designs become more intricate, the expenses associated with research, development, and sophisticated lithography equipment rise dramatically, making it harder for smaller companies to compete and pushing the boundaries of economic viability for even large players. Maintaining technological leadership requires continuous, massive investments that only a few entities can sustain.

Furthermore, managing the highly intricate and geographically dispersed global supply chain presents persistent challenges. Any disruption, whether from natural disasters, geopolitical events, or logistics bottlenecks, can have cascading effects, leading to shortages and production delays across multiple industries. Cybersecurity threats and intellectual property theft are also growing concerns, as chip designs contain invaluable proprietary information that, if compromised, could result in significant financial losses and erode competitive advantages. Lastly, the rapid pace of technological change often leads to the quick obsolescence of older technologies, requiring constant adaptation and investment in new processes and product lines to remain relevant, posing a continuous challenge for inventory management and product lifecycles.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Escalating Cost and Complexity of Advanced Node Manufacturing | -1.0% | Global | Long-term (Ongoing) |

| Managing Highly Interdependent Global Supply Chains | -0.8% | Global | Medium-term (Ongoing) |

| Cybersecurity Threats and Intellectual Property Protection | -0.6% | Global | Long-term (Ongoing) |

| Rapid Technological Obsolescence and R&D Cycle Times | -0.5% | Global | Short to Medium-term (Recurring) |

| Environmental Regulations and Sustainability Demands | -0.4% | Europe, North America, APAC | Long-term (Ongoing) |

Semiconductor Chip Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the semiconductor chip market, offering detailed insights into its current landscape, historical performance from 2019 to 2023, and a robust forecast spanning 2025 to 2033. The report meticulously dissects market size, growth drivers, restraints, opportunities, and challenges, providing a holistic view for strategic decision-making. It includes extensive segmentation analysis across various parameters and highlights regional dynamics, offering a granular understanding of market trends and competitive positioning. The scope is designed to equip stakeholders with actionable intelligence to navigate the complexities and capitalize on the opportunities within the evolving semiconductor industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 640 Billion |

| Market Forecast in 2033 | USD 1.36 Trillion |

| Growth Rate | 9.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Intel Corporation, Samsung Electronics Co. Ltd., Taiwan Semiconductor Manufacturing Company Limited (TSMC), Qualcomm Incorporated, Broadcom Inc., NVIDIA Corporation, SK Hynix Inc., Micron Technology Inc., Texas Instruments Incorporated, Analog Devices Inc., NXP Semiconductors N.V., Infineon Technologies AG, STMicroelectronics N.V., Renesas Electronics Corporation, MediaTek Inc., Kioxia Holdings Corporation, Western Digital Corporation, GlobalFoundries Inc., Applied Materials Inc., ASML Holding N.V. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The semiconductor chip market is comprehensively segmented to provide granular insights into its diverse components, applications, end-use industries, and underlying technologies. This segmentation allows for a detailed understanding of where growth is concentrated and how different market facets contribute to the overall landscape. By breaking down the market into these specific categories, stakeholders can identify niche opportunities, understand competitive dynamics within distinct areas, and tailor strategies to specific market demands. The multi-dimensional analysis ensures that the report captures the full complexity and interconnectivity of the global semiconductor ecosystem.

- By Component:

- Integrated Circuits (Microprocessors, Memory Chips, Logic ICs)

- Discrete Semiconductors

- Optoelectronics

- Sensors

- By Application:

- Consumer Electronics

- Automotive

- Industrial

- Healthcare

- Data Processing

- Telecommunications

- Aerospace & Defense

- By End-Use Industry:

- Automotive

- Consumer Electronics

- Industrial Automation

- IT & Telecommunication

- Healthcare

- Others

- By Technology:

- FinFET

- Planar Technology

- FD-SOI

Regional Highlights

- North America: A leader in semiconductor design, research, and development, particularly for high-performance computing, AI, and cloud infrastructure. The region also benefits from significant government investments aimed at boosting domestic manufacturing capabilities.

- Europe: Strong focus on automotive semiconductors, industrial automation, and power management ICs. European initiatives aim to enhance wafer manufacturing and R&D for advanced technologies and sustainable practices.

- Asia Pacific (APAC): Dominates global semiconductor manufacturing, assembly, and testing. It is the largest market in terms of consumption, driven by robust consumer electronics, telecommunications, and automotive industries in countries like China, South Korea, Taiwan, and Japan. Significant government support and a vast ecosystem characterize this region.

- Latin America: An emerging market with growing digitalization and increasing adoption of smart devices and automotive electronics. While manufacturing is nascent, demand for imported chips is steadily rising.

- Middle East and Africa (MEA): A developing market with increasing investments in digital infrastructure, IoT, and smart city initiatives, creating new opportunities for semiconductor applications, albeit from a smaller base.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Semiconductor Chip Market.- Intel Corporation

- Samsung Electronics Co. Ltd.

- Taiwan Semiconductor Manufacturing Company Limited (TSMC)

- Qualcomm Incorporated

- Broadcom Inc.

- NVIDIA Corporation

- SK Hynix Inc.

- Micron Technology Inc.

- Texas Instruments Incorporated

- Analog Devices Inc.

- NXP Semiconductors N.V.

- Infineon Technologies AG

- STMicroelectronics N.V.

- Renesas Electronics Corporation

- MediaTek Inc.

- Kioxia Holdings Corporation

- Western Digital Corporation

- GlobalFoundries Inc.

- Applied Materials Inc.

- ASML Holding N.V.

Frequently Asked Questions

Analyze common user questions about the Semiconductor Chip market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Semiconductor Chip Market?

The Semiconductor Chip Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033, driven by increasing digitalization and demand for advanced electronics.

How is AI impacting the Semiconductor Chip Market?

AI is significantly impacting the market by driving demand for specialized chips like GPUs and NPUs, influencing chip design through AI-powered EDA tools, and fostering innovation in edge computing for various applications.

What are the primary drivers for the Semiconductor Chip Market's expansion?

Key drivers include the global expansion of digitalization and connectivity, rapid adoption of AI and machine learning, growth in automotive electronics, and the continuous demand from data centers and cloud computing.

What are the main challenges facing the Semiconductor Chip Industry?

Major challenges include the high capital expenditure for fabrication plants, geopolitical tensions impacting supply chains, the cyclical nature of the industry, and the increasing complexity of advanced manufacturing processes.

Which regions are key players in the Semiconductor Chip Market?

Asia Pacific (APAC) is dominant in manufacturing and consumption, while North America leads in design and R&D. Europe shows strength in automotive and industrial semiconductors, with growing contributions from Latin America and MEA.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted