EDA in Automotive Market

EDA in Automotive Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700711 | Last Updated : July 27, 2025 |

Format : ![]()

![]()

![]()

![]()

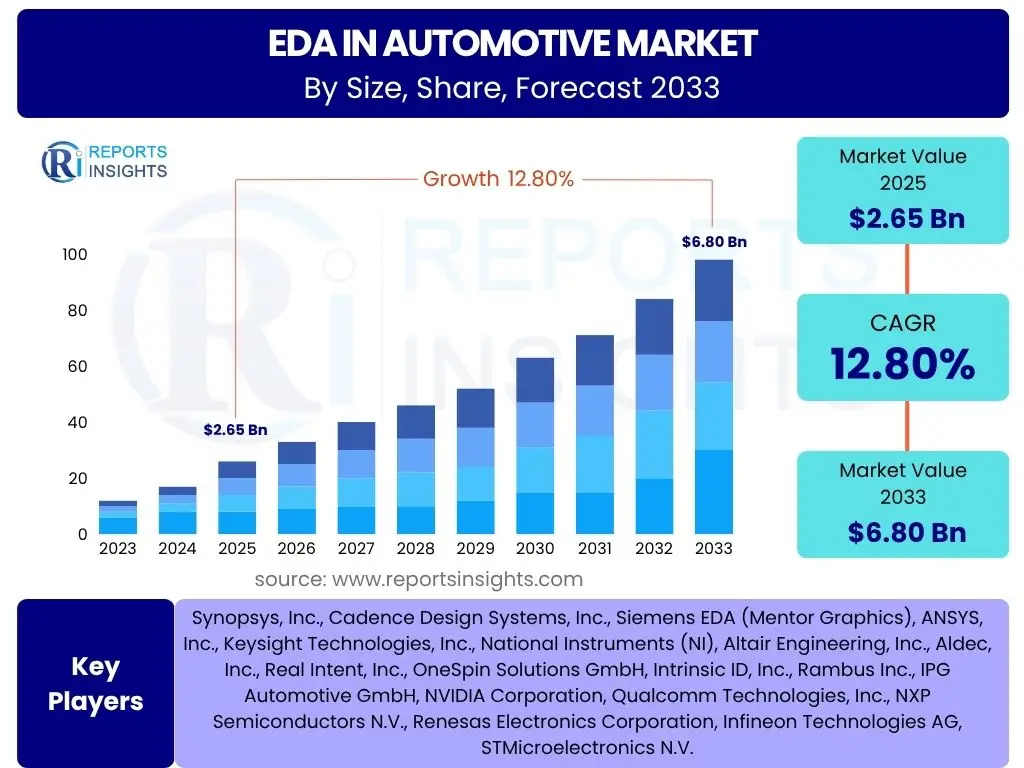

EDA in Automotive Market Size

EDA in Automotive Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2025 and 2033. The market is estimated at USD 2.65 billion in 2025 and is projected to reach USD 6.80 billion by the end of the forecast period in 2033. This substantial growth is primarily driven by the escalating complexity of electronic systems within modern vehicles, including advanced driver-assistance systems (ADAS), infotainment, and electrification components. The shift towards software-defined vehicles and autonomous driving capabilities necessitates more sophisticated and integrated EDA tools to manage the intricate interplay of hardware and software.

The expansion is further fueled by the increasing adoption of electric vehicles (EVs), which require advanced power management ICs, battery management systems, and high-performance computing units for efficient operation. These components demand rigorous design, verification, and validation processes, making EDA tools indispensable for automotive original equipment manufacturers (OEMs) and semiconductor suppliers. Regulatory pressures for enhanced safety, reduced emissions, and improved vehicle performance also contribute to the demand for advanced EDA solutions that can optimize designs for reliability, functional safety, and cybersecurity.

Key EDA in Automotive Market Trends & Insights

The EDA in Automotive market is undergoing a transformative period, largely influenced by the automotive industry's rapid evolution towards autonomous, connected, electric, and shared (ACES) mobility. Users frequently inquire about the impact of these megatrends on EDA tool development and adoption. A primary trend involves the increasing demand for system-level design and verification, moving beyond traditional chip-level focus to encompass entire electronic control units (ECUs) and vehicle architectures. This holistic approach is crucial for managing the immense complexity and ensuring functional safety and cybersecurity across diverse vehicle domains. The integration of artificial intelligence and machine learning within EDA workflows is another significant trend, promising to accelerate design cycles and enhance verification efficiency, addressing the challenges posed by ever-growing data volumes and design iterations.

Furthermore, the automotive industry's push for software-defined vehicles is driving the need for EDA tools that can seamlessly integrate hardware and software development. This includes co-design and co-verification capabilities that allow designers to optimize performance, power consumption, and thermal management across the entire system. The emphasis on robust cybersecurity measures at every stage of the design process, from chip to system, is also a critical trend, demanding specialized EDA tools for vulnerability detection and mitigation. The growing importance of compliance with stringent automotive standards such as ISO 26262 for functional safety and the upcoming ISO/SAE 21434 for automotive cybersecurity is shaping EDA tool requirements, pushing for more integrated and automated compliance features.

- Shift to system-level design and verification.

- Integration of AI and machine learning for design automation and optimization.

- Increased demand for hardware-software co-design and co-verification.

- Enhanced focus on functional safety (ISO 26262) and cybersecurity (ISO/SAE 21434) compliance.

- Adoption of cloud-based EDA for scalability and collaboration.

- Proliferation of advanced packaging technologies requiring specialized EDA.

- Growing importance of digital twins for vehicle lifecycle management.

AI Impact Analysis on EDA in Automotive

Common user questions regarding AI's impact on EDA in automotive frequently revolve around its potential to revolutionize design efficiency, verification speed, and overall system performance. Artificial intelligence, particularly machine learning, is increasingly integrated into EDA workflows to address the growing complexity of automotive electronic systems. AI algorithms can optimize chip layouts, reduce power consumption, and identify potential design flaws much faster than traditional methods. For instance, in design space exploration, AI can rapidly evaluate numerous design parameters to achieve optimal performance metrics, significantly cutting down the iterative design process. This is particularly valuable for complex System-on-Chips (SoCs) and ECUs found in ADAS and autonomous driving systems, where millions of gates need to be precisely optimized.

Moreover, AI is transforming the verification and validation stages of automotive electronic design. By employing machine learning, EDA tools can analyze vast amounts of simulation data to predict potential bugs, accelerate fault detection, and reduce the time spent on exhaustive testing. This is crucial for ensuring the functional safety and reliability of automotive components, which are paramount in safety-critical applications. AI-driven verification can identify corner cases that human engineers might overlook, leading to more robust and dependable designs. The ability of AI to learn from past design failures and successes also contributes to continuous improvement in design methodologies, fostering innovation and reducing time-to-market for new automotive technologies.

The application of AI extends to managing the complexity of software-defined vehicles. AI can assist in the automated generation of test cases for software integration, optimizing the interface between hardware and software components. This helps in bridging the traditional gap between hardware and software development teams, facilitating a more cohesive design process. Furthermore, AI is being explored for predictive maintenance within vehicles, where EDA tools can model potential component failures based on design parameters and operational data, leading to more reliable automotive systems. As data volumes from vehicle sensors and ECUs continue to grow, AI's role in analyzing this data to refine future automotive electronic designs will become even more pronounced.

- Accelerated design space exploration and optimization for automotive ICs.

- Enhanced verification efficiency through intelligent test pattern generation and bug prediction.

- Automated fault detection and diagnosis in complex electronic systems.

- Improved power, performance, and area (PPA) optimization for automotive SoCs.

- Facilitation of hardware-software co-design and integration.

- Prediction of design risks and potential functional safety violations.

- Reduction in design cycle times and faster time-to-market for new automotive features.

Key Takeaways EDA in Automotive Market Size & Forecast

Analysis of common user questions regarding the EDA in Automotive market size and forecast reveals a strong interest in understanding the core growth drivers and the long-term sustainability of this expansion. A key takeaway is the undeniable link between the escalating complexity of automotive electronics and the indispensable role of advanced EDA tools. The forecasted robust CAGR signifies that the automotive industry’s innovation cycle, particularly in areas like autonomous driving, electrification, and connected services, will continue to heavily rely on sophisticated design and verification software. This dependency positions EDA as a critical enabler, rather than just a supporting technology, for the future of mobility.

Another significant insight is that the market's growth is not uniform across all segments but is particularly pronounced in areas supporting high-performance computing, artificial intelligence integration, and functional safety compliance. As vehicles transform into complex computing platforms, the demand for specialized EDA solutions that can handle multi-core processors, high-speed interfaces, and vast amounts of sensor data will intensify. This implies a strategic shift for EDA vendors towards offering integrated platforms that address cross-domain design challenges and adhere to stringent automotive industry standards. The emphasis on software-defined vehicles further reinforces the need for EDA tools that bridge the hardware-software design gap, enabling seamless co-development and validation.

- Market growth driven by increasing electronic content and complexity in vehicles.

- Strong demand for advanced EDA tools due to autonomous driving and EV proliferation.

- Functional safety and cybersecurity compliance are paramount drivers for EDA adoption.

- Integration of AI/ML within EDA workflows is crucial for efficiency gains.

- Shift towards system-level design and verification for holistic vehicle architecture.

- Opportunities for specialized EDA solutions catering to high-performance computing and communication.

- Sustained investment in R&D by EDA vendors to meet evolving automotive requirements.

EDA in Automotive Market Drivers Analysis

The EDA in Automotive market is experiencing significant tailwinds from several key drivers that are reshaping the entire automotive industry. The relentless increase in the electronic content per vehicle, driven by features such as advanced driver-assistance systems (ADAS), in-car infotainment, and sophisticated body electronics, necessitates more advanced and integrated EDA solutions. These complex electronic systems require rigorous design, verification, and validation to ensure performance, reliability, and safety. Furthermore, the rapid global transition towards electric vehicles (EVs) and hybrid electric vehicles (HEVs) is a major catalyst, as these vehicles incorporate highly complex power electronics, battery management systems, and specialized control units that demand precise EDA tools for optimal energy efficiency and thermal management. The regulatory landscape, with evolving safety standards like ISO 26262 and cybersecurity regulations, also compels automotive OEMs and Tier 1 suppliers to adopt sophisticated EDA tools that can ensure compliance and reduce development risks.

Another pivotal driver is the ongoing evolution towards autonomous driving, which requires massive computational power and intricate sensor fusion capabilities. Designing the System-on-Chips (SoCs) and embedded systems for autonomous vehicles involves managing billions of transistors and integrating diverse IP blocks, making state-of-the-art EDA tools indispensable for efficient development and verification. The trend of software-defined vehicles (SDVs), where vehicle functions are increasingly managed by software running on centralized computing platforms, also boosts the demand for EDA solutions that facilitate hardware-software co-design and validation. This shift requires EDA tools to support continuous integration and deployment methodologies, enabling agile development cycles. Finally, the growing global push for vehicle connectivity and the implementation of V2X (vehicle-to-everything) communication technologies necessitate advanced EDA for high-speed communication interfaces and robust networking architectures within vehicles.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Complexity of Automotive Electronics | +1.8% | Global | Long-term (2025-2033) |

| Rising Adoption of Electric and Autonomous Vehicles | +1.5% | North America, Europe, APAC | Mid to Long-term (2025-2033) |

| Strict Regulatory Compliance for Safety and Cybersecurity | +1.2% | Europe, North America, Japan | Short to Mid-term (2025-2029) |

| Growth of Software-Defined Vehicles (SDVs) | +1.0% | Global | Mid to Long-term (2027-2033) |

| Advancements in Automotive Semiconductor Technology | +0.9% | APAC, North America | Short to Mid-term (2025-2030) |

EDA in Automotive Market Restraints Analysis

Despite robust growth, the EDA in Automotive market faces several significant restraints that could temper its expansion. One primary restraint is the exceptionally high cost associated with advanced EDA software licenses and associated hardware infrastructure. Implementing comprehensive EDA suites requires substantial upfront investment, which can be a barrier for smaller companies or startups, limiting their ability to innovate and compete effectively. This financial hurdle often translates into slower adoption rates for the latest EDA technologies, particularly in cost-sensitive markets. Furthermore, the inherent complexity of integrating various EDA tools from different vendors into a cohesive design flow poses a considerable challenge. Achieving seamless interoperability between design, verification, and layout tools from disparate sources can lead to inefficiencies, increased development time, and potential errors, thereby acting as a dampener on rapid market expansion.

Another critical restraint is the acute shortage of highly skilled EDA professionals with expertise in both automotive electronics and complex software tools. The specialized nature of automotive design, combined with the continuous evolution of EDA technologies, necessitates a workforce with a unique blend of domain knowledge and technical proficiency. Recruiting and retaining such talent is a persistent challenge for companies, hindering the optimal utilization of advanced EDA capabilities and slowing down project execution. Moreover, intellectual property (IP) protection concerns pose a restraint, particularly when dealing with third-party IP cores and collaborating across different organizations in the automotive supply chain. Ensuring the security and integrity of proprietary design data throughout the development lifecycle adds layers of complexity and cost, potentially slowing down collaborative innovation in the industry.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of EDA Tools and Infrastructure | -0.8% | Global, particularly Emerging Markets | Long-term (2025-2033) |

| Complexity of Tool Integration and Interoperability | -0.6% | Global | Mid-term (2025-2030) |

| Shortage of Skilled EDA Professionals | -0.5% | North America, Europe, APAC | Long-term (2025-2033) |

| Data Security and IP Protection Concerns | -0.3% | Global | Mid-term (2025-2030) |

EDA in Automotive Market Opportunities Analysis

The EDA in Automotive market is poised to capitalize on several significant opportunities arising from the ongoing transformation of the automotive industry. The increasing adoption of cloud-based EDA solutions presents a major growth avenue, offering enhanced scalability, flexibility, and reduced upfront infrastructure costs for automotive designers. Cloud platforms enable global collaboration, faster access to compute resources for simulation and verification, and facilitate agile development cycles, which are crucial for the rapid innovation pace in automotive electronics. This shift also broadens the accessibility of advanced EDA tools to a wider range of companies, including startups and smaller enterprises, fostering a more dynamic and competitive landscape. The development of specialized EDA tools tailored for specific automotive applications, such as power electronics for EVs or high-performance computing for autonomous driving, offers significant opportunities for vendors to capture niche markets and provide highly optimized solutions.

Furthermore, the emergence of new vehicle architectures, particularly domain-centric or centralized computing architectures, opens new design paradigms that require innovative EDA approaches. These architectures demand integrated design and verification tools that can handle multi-domain interactions and ensure seamless functionality across various vehicle systems. Opportunities also lie in addressing the growing need for enhanced functional safety and cybersecurity measures at every layer of the automotive electronic stack. EDA vendors can differentiate themselves by offering tools with integrated features for safety analysis, fault injection, and vulnerability assessment, aligning with stringent industry standards like ISO 26262 and ISO/SAE 21434. The expansion into emerging automotive markets, particularly in Asia Pacific and Latin America, driven by increasing vehicle production and rising demand for advanced features, also presents substantial growth prospects for EDA solution providers. Strategic partnerships and collaborations between EDA vendors, semiconductor manufacturers, and automotive OEMs can further unlock synergistic opportunities, fostering innovation and accelerating market adoption.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Adoption of Cloud-Based EDA Solutions | +1.3% | Global | Mid to Long-term (2026-2033) |

| Development of Specialized Tools for EV/AV Architectures | +1.1% | North America, Europe, APAC | Short to Mid-term (2025-2030) |

| Integration of AI/ML for Advanced Automation | +1.0% | Global | Mid to Long-term (2027-2033) |

| Demand for Enhanced Functional Safety and Cybersecurity EDA | +0.9% | Global | Short to Mid-term (2025-2029) |

| Expansion into Emerging Markets (APAC, Latin America) | +0.7% | APAC, Latin America | Mid to Long-term (2027-2033) |

EDA in Automotive Market Challenges Impact Analysis

The EDA in Automotive market confronts several critical challenges that demand innovative solutions from industry players. One significant challenge is ensuring functional safety and security across the entire automotive electronic system. As vehicles become more autonomous and connected, the consequences of system failures or cyberattacks become severe, necessitating rigorous safety compliance (e.g., ISO 26262) and cybersecurity measures (e.g., ISO/SAE 21434). EDA tools must evolve to incorporate advanced features for fault injection, safety analysis, and vulnerability assessment throughout the design flow, adding layers of complexity to development. Another formidable challenge is managing the exponentially growing volume of data generated by advanced automotive designs, particularly during verification and simulation phases. The sheer size of design files, test patterns, and simulation results requires massive computational resources and efficient data management strategies, posing significant infrastructure and processing challenges for design teams.

Furthermore, the rapid pace of technological change within the automotive industry presents a continuous challenge for EDA vendors. The swift evolution of semiconductor processes, new communication standards (e.g., 5G, Automotive Ethernet), and the constant introduction of new vehicle architectures demand that EDA tools remain cutting-edge and adaptable. This requires continuous investment in research and development to keep pace with industry advancements, ensuring tool relevance and effectiveness. Additionally, the global supply chain disruptions, while not directly related to EDA software, impact the hardware development cycles in automotive, which in turn can influence the adoption and utilization rates of EDA tools. Interoperability issues between different EDA tools from various vendors and the need for seamless integration into existing design flows also remain a persistent challenge, potentially increasing design complexity and time-to-market. Addressing these challenges requires close collaboration between EDA providers, semiconductor manufacturers, and automotive OEMs to develop harmonized and robust solutions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ensuring Functional Safety and Cybersecurity | -0.7% | Global | Long-term (2025-2033) |

| Managing Growing Data Volumes and Complexity | -0.6% | Global | Mid-term (2025-2030) |

| Rapid Technological Advancements in Automotive | -0.5% | Global | Short to Mid-term (2025-2029) |

| Interoperability and Integration of Diverse Toolchains | -0.4% | Global | Mid-term (2025-2030) |

EDA in Automotive Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the EDA in Automotive Market, encompassing its size, growth trajectory, key trends, and a detailed examination of the drivers, restraints, opportunities, and challenges shaping the industry. It offers a strategic overview of the market's dynamics from 2019 to 2033, with a particular focus on the forecast period from 2025 to 2033. The report meticulously segments the market by various parameters, including tool type, application, vehicle type, and design flow, providing granular insights into each category. It also features a thorough regional analysis and profiles leading companies in the sector, offering stakeholders a complete understanding of the competitive landscape and market potential to facilitate informed decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.65 billion |

| Market Forecast in 2033 | USD 6.80 billion |

| Growth Rate | 12.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Synopsys, Inc., Cadence Design Systems, Inc., Siemens EDA (Mentor Graphics), ANSYS, Inc., Keysight Technologies, Inc., National Instruments (NI), Altair Engineering, Inc., Aldec, Inc., Real Intent, Inc., OneSpin Solutions GmbH, Intrinsic ID, Inc., Rambus Inc., IPG Automotive GmbH, NVIDIA Corporation, Qualcomm Technologies, Inc., NXP Semiconductors N.V., Renesas Electronics Corporation, Infineon Technologies AG, STMicroelectronics N.V. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The EDA in Automotive market is segmented to provide a granular understanding of its diverse facets, reflecting the multifaceted requirements of modern automotive design. These segments offer insights into specific tool functionalities, applications within vehicles, types of vehicles utilizing these tools, and stages of the design process. The segmentation by tool type, including Computer-Aided Engineering (CAE), IC Design, PCB & Multi-chip Module (MCM) Design, System-Level Design, and Intellectual Property (IP), highlights the varied software solutions employed across the electronic design workflow. Within IC design, further sub-segmentation into Simulation & Verification, Physical Design & Verification, Synthesis, and Test tools underscores the intricate steps involved in creating complex automotive chips. This detailed breakdown helps identify areas of concentrated demand and technological advancement.

The application-based segmentation, encompassing ADAS, Infotainment & Telematics, Body Electronics & Chassis, Powertrain & Engine Control, and Safety & Security Systems, illustrates how EDA tools are critical across different functional domains within a vehicle. Each application area presents unique design challenges and compliance requirements, driving demand for specialized EDA capabilities. Furthermore, the market is segmented by vehicle type, differentiating between Passenger Vehicles, Commercial Vehicles, and the rapidly growing Electric Vehicles (EVs), recognizing their distinct electronic architectures and performance needs. The segmentation by design flow, categorizing tools into Front-End Design and Back-End Design, offers a perspective on the sequential stages of the electronic design automation process. Finally, segmentation by technology node (Below 10nm, 10nm-28nm, Above 28nm) reflects the advanced process technologies increasingly being adopted for high-performance automotive semiconductors, influencing the capabilities and complexity of required EDA tools.

- By Tool Type:

- CAE (Computer-Aided Engineering): Tools for mechanical analysis, thermal analysis, and electromagnetic compatibility (EMC) simulation.

- IC Design:

- Simulation & Verification: For functional verification, circuit simulation, and mixed-signal verification.

- Physical Design & Verification: Layout, routing, design rule checking (DRC), and layout versus schematic (LVS).

- Synthesis: Logic synthesis and high-level synthesis (HLS) for converting abstract designs into gate-level netlists.

- Test: Design for testability (DFT), automatic test pattern generation (ATPG), and fault simulation.

- PCB & Multi-chip Module (MCM) Design: For printed circuit board layout, routing, and signal integrity analysis.

- System-Level Design: Tools for architecture exploration, system modeling, and hardware-software co-design.

- IP (Intellectual Property): Reusable design blocks and verification IP for various functionalities (e.g., processors, interfaces, memory controllers).

- By Application:

- ADAS (Advanced Driver-Assistance Systems): For designing radar, lidar, camera, and sensor fusion processing units.

- Infotainment & Telematics: For multimedia, connectivity, and navigation systems.

- Body Electronics & Chassis: For comfort, lighting, security, and chassis control systems.

- Powertrain & Engine Control: For engine management, transmission control, and electric vehicle power electronics.

- Safety & Security Systems: For functional safety (ISO 26262) and cybersecurity (ISO/SAE 21434) compliant designs.

- By Vehicle Type:

- Passenger Vehicles: Mainstream consumer cars.

- Commercial Vehicles: Trucks, buses, and specialized industrial vehicles.

- Electric Vehicles (EVs): Including Battery Electric Vehicles (BEVs) and Hybrid Electric Vehicles (HEVs).

- By Design Flow:

- Front-End Design: Conceptualization, architectural design, RTL coding, and functional verification.

- Back-End Design: Physical implementation, layout, routing, timing closure, and final verification for manufacturing.

- By Technology Node:

- Below 10nm: For cutting-edge, high-performance computing automotive chips.

- 10nm-28nm: Predominant for a wide range of automotive SoCs and microcontrollers.

- Above 28nm: For legacy systems, power management ICs, and simpler control units.

Regional Highlights

- North America: North America represents a significant market for EDA in Automotive, driven by substantial investments in autonomous driving technologies, electric vehicle research and development, and advanced semiconductor manufacturing. The presence of leading automotive OEMs and Tier 1 suppliers, alongside prominent EDA tool providers and research institutions, fosters a robust innovation ecosystem. The region's stringent safety regulations and the strong push for connected vehicle technologies further accelerate the adoption of sophisticated EDA solutions for complex system design, verification, and validation. Silicon Valley continues to be a hub for semiconductor innovation, directly influencing EDA tool advancements.

- Europe: Europe is a mature and highly innovative market, characterized by strong emphasis on functional safety (ISO 26262) and the rapid transition to electric mobility. Countries such as Germany, France, and the UK are at the forefront of automotive engineering, with established automotive manufacturers and a growing ecosystem of specialized semiconductor companies. The region's commitment to reducing carbon emissions and enhancing vehicle safety standards fuels the demand for advanced EDA tools for power electronics, battery management systems, and highly integrated ADAS solutions. Collaborations between research institutes, automotive players, and EDA vendors are common, driving the development of next-generation design methodologies.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing market for EDA in Automotive, primarily due to the region's burgeoning automotive production, particularly in China, Japan, South Korea, and India. China's aggressive push for electric vehicles and autonomous driving, coupled with significant government support for domestic semiconductor industries, is creating immense demand for EDA tools. Japan and South Korea continue to be leaders in automotive electronics and semiconductor manufacturing, investing heavily in advanced design technologies. The growing middle class and increasing disposable incomes are driving the demand for feature-rich vehicles, necessitating advanced EDA solutions to design their complex electronic architectures efficiently and cost-effectively.

- Latin America: The Latin American market for EDA in Automotive is emerging, driven by increasing vehicle production and the gradual adoption of advanced electronic features in new car models. While smaller compared to other regions, there is a growing interest in electric vehicles and connected car technologies, particularly in countries like Brazil and Mexico. The market is influenced by the expansion strategies of global automotive OEMs and their local manufacturing operations, leading to a rising, albeit slower, demand for modern EDA tools to support localized design and integration efforts. The focus often lies on cost-effective and efficient design solutions.

- Middle East and Africa (MEA): The MEA region is at an nascent stage regarding EDA in Automotive, with growth primarily driven by infrastructure development, smart city initiatives, and a gradual shift towards modern vehicle technologies. Countries in the Gulf Cooperation Council (GCC) are investing in diversifying their economies, including developing localized automotive manufacturing and technology hubs. While the adoption of advanced EDA tools is still limited compared to other regions, there is a growing recognition of the importance of electronic design automation as the automotive sector evolves and incorporates more complex systems, particularly for infotainment, connectivity, and foundational safety features.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the EDA in Automotive Market.- Synopsys, Inc.

- Cadence Design Systems, Inc.

- Siemens EDA (Mentor Graphics)

- ANSYS, Inc.

- Keysight Technologies, Inc.

- National Instruments (NI)

- Altair Engineering, Inc.

- Aldec, Inc.

- Real Intent, Inc.

- OneSpin Solutions GmbH

- Intrinsic ID, Inc.

- Rambus Inc.

- IPG Automotive GmbH

- NVIDIA Corporation

- Qualcomm Technologies, Inc.

- NXP Semiconductors N.V.

- Renesas Electronics Corporation

- Infineon Technologies AG

- STMicroelectronics N.V.

- Texas Instruments Inc.

Frequently Asked Questions

What is the projected growth rate for the EDA in Automotive Market?

The EDA in Automotive Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2025 and 2033, driven by increasing electronic complexity in vehicles.

What are the primary drivers of the EDA in Automotive Market?

Key drivers include the increasing complexity of automotive electronics, the rapid adoption of electric and autonomous vehicles, and stringent regulatory requirements for functional safety and cybersecurity.

How is AI impacting EDA in the Automotive sector?

AI integration in EDA for automotive is enhancing design optimization, accelerating verification processes, improving fault detection, and enabling more efficient hardware-software co-design, significantly reducing design cycles.

What are the major challenges in the EDA in Automotive Market?

Major challenges include ensuring robust functional safety and cybersecurity throughout the design process, managing exponentially growing data volumes from complex designs, and keeping pace with rapid technological advancements in the automotive industry.

Which regions are leading the adoption of EDA in Automotive?

North America and Europe are mature markets with high adoption, while Asia Pacific, particularly China, Japan, and South Korea, is expected to be the fastest-growing region due to significant investments in EV and autonomous driving technologies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted