Distribution Voltage Regulator Market

Distribution Voltage Regulator Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700452 | Last Updated : July 24, 2025 |

Format : ![]()

![]()

![]()

![]()

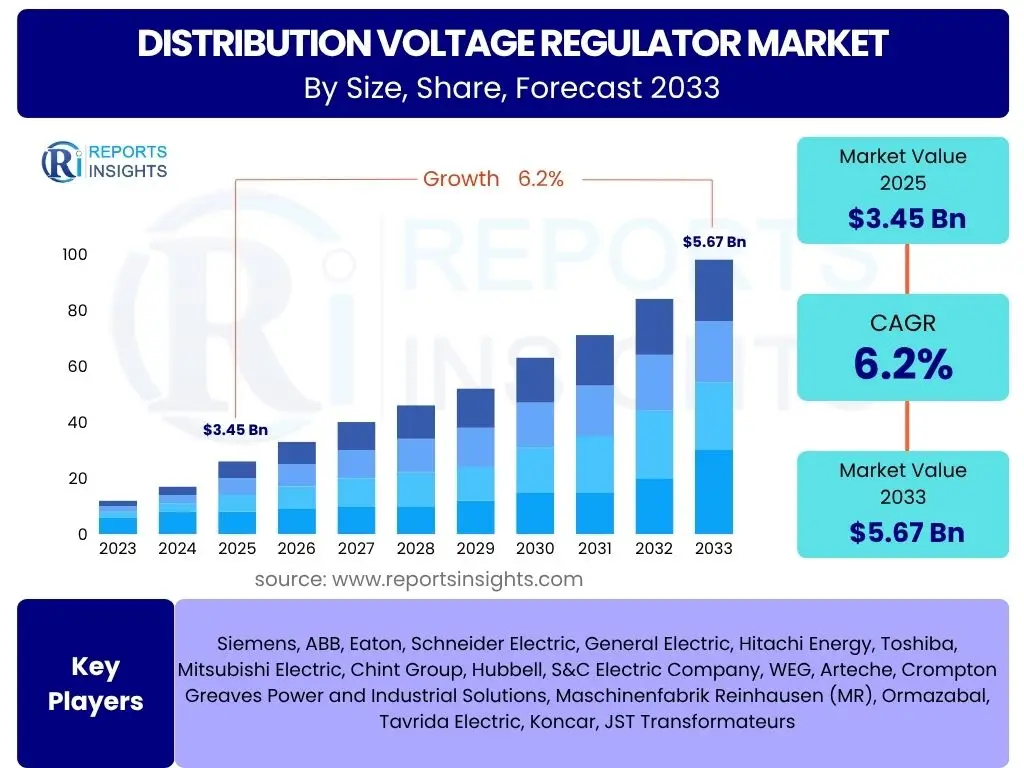

Distribution Voltage Regulator Market Size

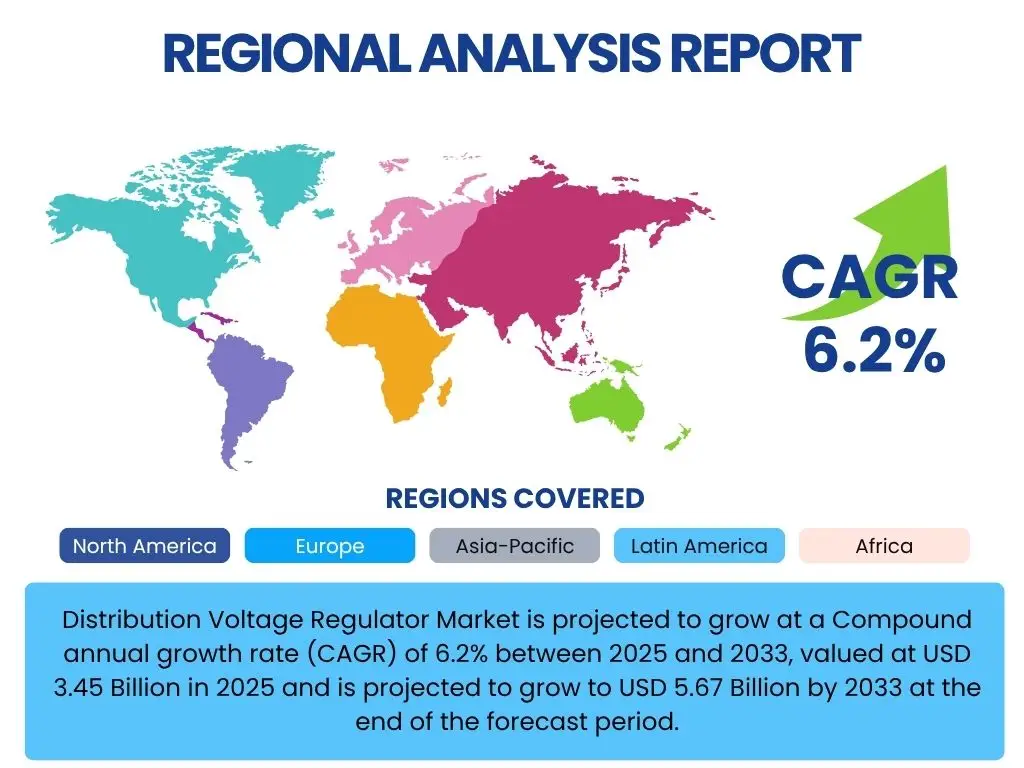

Distribution Voltage Regulator Market is projected to grow at a Compound annual growth rate (CAGR) of 6.2% between 2025 and 2033, valued at USD 3.45 Billion in 2025 and is projected to grow to USD 5.67 Billion by 2033 at the end of the forecast period.

Key Distribution Voltage Regulator Market Trends & Insights

The market is experiencing significant shifts driven by grid modernization initiatives, the accelerating integration of renewable energy sources, and the imperative for enhanced grid stability and efficiency. Key trends influencing the distribution voltage regulator market include:

- Increasing adoption of smart grid technologies to optimize power flow and reduce losses.

- Growing demand for robust voltage regulation solutions to manage fluctuating loads from renewable energy integration.

- Emphasis on grid resiliency and reliability in the face of climate change and extreme weather events.

- Technological advancements in digital controls and communication capabilities for real-time monitoring and management.

- Expansion of electrification programs and infrastructure development in emerging economies.

AI Impact Analysis on Distribution Voltage Regulator

Artificial Intelligence (AI) is set to revolutionize the distribution voltage regulator market by enabling more proactive, predictive, and efficient grid management. Its impact is primarily seen in:

- Enhancing predictive maintenance capabilities for voltage regulators, reducing downtime and operational costs.

- Optimizing voltage control through real-time data analysis, leading to improved power quality and energy efficiency.

- Facilitating seamless integration of distributed energy resources (DERs) by dynamically adjusting voltage levels.

- Improving grid fault detection and isolation, significantly enhancing grid reliability and faster restoration.

- Enabling autonomous grid operation and decision-making for optimal voltage profile management across complex networks.

Key Takeaways Distribution Voltage Regulator Market Size & Forecast

- The Distribution Voltage Regulator Market is poised for substantial growth, driven by global electricity demand and grid infrastructure upgrades.

- Significant investment in smart grid technologies and renewable energy integration acts as a primary growth catalyst.

- Technological advancements in voltage regulator design and control systems are enhancing operational efficiency and reliability.

- The market's expansion is intrinsically linked to efforts in modernizing aging power distribution networks worldwide.

- Asia Pacific and North America are expected to be key growth regions, spurred by urbanization and industrial expansion.

- AI and digitalization are transforming voltage regulation from reactive to predictive, improving grid performance.

Distribution Voltage Regulator Market Drivers Analysis

The distribution voltage regulator market is propelled by a confluence of factors, each contributing significantly to its expansion and technological evolution. Global efforts towards grid modernization and the imperative for efficient energy management stand as foundational drivers. The increasing integration of renewable energy sources, such as solar and wind power, introduces inherent variability into the grid, necessitating advanced voltage regulation solutions to maintain stability and power quality. Furthermore, the burgeoning demand for electricity, fueled by urbanization, industrial growth, and the proliferation of electric vehicles, places continuous pressure on existing grid infrastructure, driving the adoption of voltage regulators to optimize power delivery and minimize losses. These intertwined factors create a robust growth environment for the market.| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Grid Modernization and Smart Grid Initiatives: Investments in upgrading aging electrical infrastructure and deploying smart grid technologies to improve efficiency, reliability, and connectivity of power distribution networks. | +1.5% | North America, Europe, Asia Pacific (China, India) | Short to Medium Term (2025-2029) |

| Integration of Renewable Energy Sources: The intermittent nature of solar and wind power necessitates robust voltage regulation to maintain grid stability and power quality, driving demand for advanced regulators. | +1.2% | Europe, Asia Pacific (China, India, Australia), North America | Medium to Long Term (2027-2033) |

| Increasing Electricity Consumption and Urbanization: Rapid urbanization and industrialization, particularly in emerging economies, lead to rising electricity demand, requiring enhanced voltage management to prevent fluctuations and ensure stable supply. | +0.8% | Asia Pacific (India, Southeast Asia), Latin America, Africa | Short to Long Term (2025-2033) |

| Aging Grid Infrastructure: Deteriorating infrastructure in developed regions necessitates replacement and upgrades, including modern voltage regulators, to improve grid resilience and reduce power losses. | +0.7% | North America, Europe | Medium Term (2026-2030) |

| Government Regulations and Energy Efficiency Mandates: Strict governmental policies promoting energy efficiency, reduced carbon emissions, and grid reliability encourage utilities to adopt advanced voltage regulation technologies. | +0.6% | Europe, North America, parts of Asia Pacific | Short to Medium Term (2025-2029) |

Distribution Voltage Regulator Market Restraints Analysis

Despite its robust growth potential, the distribution voltage regulator market faces several significant restraints that could impede its expansion. High initial capital investment for procurement and installation of advanced voltage regulators, especially for utilities operating on limited budgets, can be a major barrier. The complexity associated with integrating new voltage regulation technologies into existing, often legacy, grid infrastructures presents technical and operational challenges. Furthermore, the long operational life cycles of current grid equipment can delay the adoption of newer, more efficient regulator technologies, as utilities may defer upgrades until existing assets reach the end of their service life. These factors require careful consideration for market stakeholders.| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment: The significant upfront cost associated with purchasing and installing advanced voltage regulators can deter utilities and industrial consumers, particularly those with budget constraints. | -0.9% | Globally, particularly emerging economies | Short to Medium Term (2025-2029) |

| Complex Integration with Legacy Systems: Integrating modern digital voltage regulators into existing, often outdated, grid infrastructure poses technical challenges and requires substantial system redesign. | -0.7% | North America, Europe (regions with established grids) | Medium Term (2026-2030) |

| Long Operational Life Cycle of Existing Equipment: The durability of current voltage regulators means utilities often delay replacement until assets reach end-of-life, slowing the adoption of newer technologies. | -0.5% | Globally, more pronounced in developed markets | Long Term (2028-2033) |

| Stringent Regulatory Approvals: The need for compliance with various national and international standards and lengthy approval processes can delay market entry and product deployment. | -0.4% | Europe, North America | Short Term (2025-2027) |

Distribution Voltage Regulator Market Opportunities Analysis

Significant opportunities exist within the distribution voltage regulator market, driven by evolving energy landscapes and technological advancements. The decentralization of power generation, characterized by a proliferation of distributed energy resources (DERs) like rooftop solar and microgrids, creates a strong demand for local, responsive voltage regulation. The push for smart cities and the digitization of utility operations present avenues for integrating advanced, communication-enabled voltage regulators that can contribute to a more resilient and efficient grid. Furthermore, the expansion of electric vehicle charging infrastructure necessitates stable power supply at charging stations, offering a specialized growth niche for voltage regulator deployment. These emerging trends provide fertile ground for market innovation and expansion.| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of Distributed Energy Resources (DERs): The increasing adoption of DERs (solar, wind, energy storage) creates a demand for localized and dynamic voltage regulation solutions to manage bidirectional power flow. | +1.3% | North America, Europe, Asia Pacific (Australia, Japan) | Medium to Long Term (2027-2033) |

| Expansion of Electric Vehicle (EV) Charging Infrastructure: The proliferation of EV charging stations, often drawing significant power, requires stable and controlled voltage, offering a new application area for regulators. | +1.0% | North America, Europe, Asia Pacific (China) | Short to Medium Term (2025-2029) |

| Development of Smart Cities and Digital Utilities: Initiatives to build smart cities incorporate advanced digital infrastructure, driving the demand for smart, remotely controllable voltage regulators as part of integrated grid solutions. | +0.8% | Asia Pacific (Singapore, South Korea), Europe, Middle East | Medium Term (2026-2030) |

| Microgrid and Off-Grid Electrification Projects: The establishment of microgrids and efforts to bring electricity to remote areas, especially in developing regions, open new markets for stand-alone voltage regulation solutions. | +0.6% | Africa, Southeast Asia, Latin America | Long Term (2028-2033) |

Distribution Voltage Regulator Market Challenges Impact Analysis

The distribution voltage regulator market faces several inherent challenges that require innovative solutions and strategic adaptation from industry players. Cyber security threats to digital voltage regulators and interconnected grid systems present a critical challenge, demanding robust security protocols to prevent operational disruptions. The lack of standardized protocols for communication and integration among diverse grid components can hinder the seamless deployment and interoperability of new voltage regulation technologies. Moreover, the shortage of skilled labor proficient in installing, maintaining, and operating advanced digital voltage regulators poses a significant human capital challenge, particularly in regions undergoing rapid grid modernization. Addressing these challenges is paramount for sustained market growth.| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cyber Security Vulnerabilities: The increasing digitalization of voltage regulators and their integration into smart grids expose them to cyber threats, requiring continuous investment in robust security measures. | -0.8% | Globally, particularly in technologically advanced regions | Short to Long Term (2025-2033) |

| Lack of Standardized Communication Protocols: Inconsistent communication standards across different manufacturers and grid components complicate the integration and interoperability of new voltage regulators. | -0.6% | Globally, varying by regional adoption | Medium Term (2026-2030) |

| Shortage of Skilled Workforce: A deficit of trained professionals capable of installing, maintaining, and troubleshooting advanced digital voltage regulators can impede deployment and efficient operation. | -0.5% | Globally, more acute in developing regions | Short to Medium Term (2025-2029) |

| Environmental and Geopolitical Factors: Extreme weather events, natural disasters, and geopolitical instability can disrupt supply chains, damage infrastructure, and delay project implementations. | -0.4% | Regionally specific (e.g., hurricane-prone areas, politically unstable zones) | Short to Long Term (2025-2033) |

Distribution Voltage Regulator Market - Updated Report Scope

This updated report provides a comprehensive analysis of the Distribution Voltage Regulator Market, offering detailed insights into market dynamics, segmentation, regional trends, and competitive landscape. It covers a forecast period extending to 2033, providing stakeholders with critical data for strategic decision-making and market positioning. The scope includes an in-depth assessment of market size, growth drivers, restraints, opportunities, and challenges, along with the impact of AI on market evolution.| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.45 Billion |

| Market Forecast in 2033 | USD 5.67 Billion |

| Growth Rate | 6.2% from 2025 to 2033 |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Siemens, ABB, Eaton, Schneider Electric, General Electric, Hitachi Energy, Toshiba, Mitsubishi Electric, Chint Group, Hubbell, S&C Electric Company, WEG, Arteche, Crompton Greaves Power and Industrial Solutions, Maschinenfabrik Reinhausen (MR), Ormazabal, Tavrida Electric, Koncar, JST Transformateurs |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Distribution Voltage Regulator Market is comprehensively segmented to provide granular insights into its various dimensions, enabling a detailed understanding of market dynamics and opportunities across different product types, phases, control methods, applications, end-users, and installation types. This meticulous segmentation allows stakeholders to identify specific growth avenues and tailor strategies for diverse market niches.- By Product Type:

- Step-Voltage Regulators: These are the most common type, providing discrete voltage adjustments through tap changes, widely used for maintaining stable voltage in distribution networks.

- Induction Voltage Regulators: Offer continuous voltage regulation and are often employed in applications requiring very precise control.

- Tap-Changing Transformers: While often integrated, these refer to larger power transformers equipped with tap changers for voltage regulation at higher voltage levels, influencing distribution.

- By Phase:

- Single-Phase: Primarily used for residential and light commercial loads, ensuring stable voltage to individual consumers.

- Three-Phase: Employed in industrial, commercial, and utility applications where high power loads and three-phase supply are prevalent.

- By Control Method:

- Automatic: Regulators equipped with intelligent control systems that automatically adjust voltage levels in response to grid conditions, crucial for smart grid operations.

- Manual: Require manual intervention for tap changes, often found in less dynamic or older grid segments.

- By Application:

- Utility (Transmission & Distribution): The largest segment, encompassing voltage regulation within utility substations and along distribution lines to ensure stable power delivery to end-users.

- Industrial: Used in manufacturing plants, heavy industries, and other industrial facilities to protect sensitive machinery from voltage fluctuations.

- Commercial: Employed in commercial buildings, shopping malls, and data centers to maintain power quality for various electrical systems.

- Residential: Less common as dedicated units but integrated into local distribution networks serving residential areas to ensure household voltage stability.

- By End-User:

- Power Generation: Ensuring stable voltage at the point of power generation before transmission.

- Transmission and Distribution: The core segment, focusing on maintaining voltage levels across vast networks.

- Renewable Energy: Critical for integrating intermittent renewable sources into the grid without compromising stability.

- Oil and Gas: Protecting sensitive equipment in drilling, refining, and transportation operations from voltage irregularities.

- Mining: Ensuring reliable power supply for heavy machinery and operations in mining sites.

- Manufacturing: Maintaining stable voltage for continuous production lines and precision equipment.

- By Installation:

- Pole-Mounted: Compact regulators designed for installation on utility poles, common in rural and suburban distribution.

- Pad-Mounted: Enclosed regulators installed on concrete pads, typically in urban or residential areas for aesthetic and safety reasons.

- Substation: Larger, high-capacity regulators installed within substations to manage voltage for wider distribution areas.

Regional Highlights

The global Distribution Voltage Regulator Market exhibits distinct regional dynamics, with certain geographies playing pivotal roles in market growth and technological adoption. Understanding these regional highlights is crucial for market participants to identify lucrative opportunities and adapt their strategies accordingly.- North America: This region is a major market for distribution voltage regulators, primarily driven by extensive grid modernization efforts and the urgent need to replace aging infrastructure. The integration of distributed energy resources and the proliferation of smart grid initiatives also significantly contribute to the demand for advanced voltage regulation solutions. Policies promoting renewable energy and energy efficiency further stimulate market growth, particularly in countries like the United States and Canada, which are investing heavily in grid resilience and automation.

- Europe: Europe stands as a key market, propelled by stringent government regulations aimed at reducing carbon emissions and promoting renewable energy integration. Countries across the European Union are actively modernizing their power grids to accommodate high levels of wind and solar power, necessitating sophisticated voltage regulators. Emphasis on grid stability, energy efficiency, and the development of smart cities also drives investment in advanced, digitally controlled voltage regulation technologies.

- Asia Pacific (APAC): APAC is anticipated to be the fastest-growing market due to rapid industrialization, urbanization, and significant investments in power infrastructure development, especially in emerging economies like China, India, and Southeast Asian countries. The escalating demand for electricity, coupled with ambitious renewable energy targets and the expansion of smart grid projects, creates a vast market for distribution voltage regulators. Government initiatives to ensure reliable power supply for growing populations and industries are primary catalysts.

- Latin America: This region is witnessing steady growth, largely driven by increasing electricity demand, particularly in industrial and commercial sectors, and ongoing efforts to expand electrification in underserved areas. Investments in grid infrastructure upgrades and renewable energy projects in countries like Brazil and Mexico contribute to the adoption of voltage regulators, albeit at a slower pace compared to developed regions.

- Middle East and Africa (MEA): The MEA region presents emerging opportunities, primarily due to significant infrastructure investments, particularly in the Gulf Cooperation Council (GCC) countries, focusing on diversifying economies and meeting rising energy demands. Electrification initiatives in various African nations also create a latent demand for basic and advanced voltage regulation solutions to stabilize nascent grids and facilitate access to power.

Top Key Players:

The market research report covers the analysis of key stake holders of the Distribution Voltage Regulator Market. Some of the leading players profiled in the report include -- Siemens

- ABB

- Eaton

- Schneider Electric

- General Electric

- Hitachi Energy

- Toshiba

- Mitsubishi Electric

- Chint Group

- Hubbell

- S&C Electric Company

- WEG

- Arteche

- Crompton Greaves Power and Industrial Solutions

- Maschinenfabrik Reinhausen (MR)

- Ormazabal

- Tavrida Electric

- Koncar

- Beijing Power Equipment Group

- SEL (Schweitzer Engineering Laboratories)

Frequently Asked Questions:

What is a distribution voltage regulator and why is it important?

A distribution voltage regulator is an electrical device designed to automatically maintain a stable voltage level within a power distribution network. It compensates for voltage fluctuations caused by varying load demands, generation changes, or line impedance. Its importance lies in ensuring power quality, preventing equipment damage, minimizing energy losses, and enhancing the overall reliability and efficiency of the electrical grid for consumers and industries alike.How does the integration of renewable energy impact the demand for voltage regulators?

The integration of intermittent renewable energy sources, such as solar and wind power, introduces variability into the grid's voltage profile. This necessitates more dynamic and responsive voltage regulation. Voltage regulators are crucial for compensating for these fluctuations, maintaining stable voltage levels, and ensuring seamless grid integration of distributed renewable energy, thereby increasing their demand.What role does smart grid technology play in the distribution voltage regulator market?

Smart grid technology significantly enhances the functionality and efficiency of distribution voltage regulators. It enables real-time monitoring, remote control, and automated adjustments of voltage levels based on dynamic grid conditions. This integration supports predictive maintenance, optimizes power flow, reduces technical losses, and improves overall grid resilience, making smart grid compatibility a key driver for advanced voltage regulator adoption.What are the key types of distribution voltage regulators available in the market?

The primary types of distribution voltage regulators include step-voltage regulators, which adjust voltage in discrete steps, and induction voltage regulators, which provide continuous voltage adjustment. Additionally, tap-changing transformers, while not standalone regulators, incorporate mechanisms for voltage regulation within their design, playing a vital role in maintaining stable voltage across the distribution network. Each type serves specific applications based on control precision and grid requirements.What challenges does the distribution voltage regulator market face?

The distribution voltage regulator market faces challenges such as high initial capital investment required for procurement and installation, particularly for advanced digital models. Integrating new technologies into existing legacy grid infrastructures can be complex. Furthermore, cyber security vulnerabilities due to increased digitalization and a shortage of skilled labor for maintenance and operation pose significant hurdles for market growth and efficient deployment.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted