High Voltage Inverter Market

High Voltage Inverter Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701613 | Last Updated : July 30, 2025 |

Format : ![]()

![]()

![]()

![]()

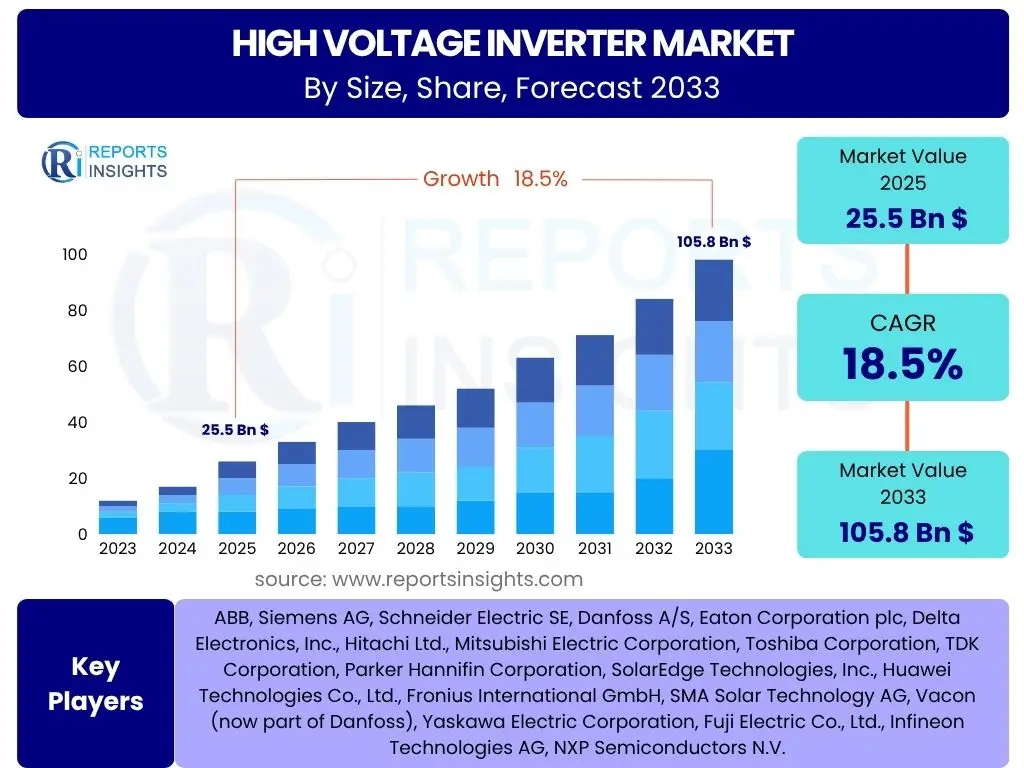

High Voltage Inverter Market Size

According to Reports Insights Consulting Pvt Ltd, The High Voltage Inverter Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at 25.5 Billion USD in 2025 and is projected to reach 105.8 Billion USD by the end of the forecast period in 2033.

Key High Voltage Inverter Market Trends & Insights

The High Voltage Inverter market is undergoing significant transformation, driven by an accelerating global shift towards electrification and sustainable energy solutions. Common user inquiries often revolve around the underlying technological advancements, market adoption rates, and the integration of these inverters across diverse sectors. A primary trend observed is the continuous evolution in power semiconductor materials, such as Silicon Carbide (SiC) and Gallium Nitride (GaN), which are enabling higher efficiencies, power densities, and reduced form factors for inverters. This material innovation is critical for meeting the demanding performance requirements of electric vehicles and large-scale renewable energy installations.

Another prominent trend is the increasing demand for bidirectional inverters, which are essential for Vehicle-to-Grid (V2G) and Grid-to-Vehicle (G2V) applications, as well as for sophisticated energy storage systems. As consumers and industries increasingly embrace distributed energy resources, the capability to seamlessly manage power flow both into and out of the grid becomes paramount. Furthermore, the market is witnessing a surge in modular and scalable inverter designs, offering greater flexibility and easier integration into various system architectures, from residential solar setups to complex industrial motor drives. These modular solutions simplify maintenance and allow for capacity expansion as energy needs evolve.

The convergence of digitalization and inverter technology is also shaping the market landscape. There is a growing emphasis on smart inverters equipped with advanced communication capabilities, enabling real-time monitoring, predictive maintenance, and optimized energy management through cloud-based platforms. These intelligent features not only enhance operational efficiency and reliability but also contribute to the stability and resilience of modern power grids. The interplay of these trends highlights a dynamic market driven by innovation, sustainability imperatives, and the relentless pursuit of energy efficiency across various applications.

- Adoption of Silicon Carbide (SiC) and Gallium Nitride (GaN) for enhanced efficiency and power density.

- Increasing demand for bidirectional inverters for V2G, G2V, and advanced energy storage systems.

- Growth in modular and scalable inverter designs for diverse application flexibility.

- Integration of smart features, connectivity, and cloud-based monitoring for optimized energy management.

- Miniaturization and higher power output leading to compact system designs.

AI Impact Analysis on High Voltage Inverter

User questions frequently probe into how Artificial Intelligence (AI) is revolutionizing the High Voltage Inverter domain, focusing on aspects like predictive maintenance, optimized performance, and grid integration challenges. AI's influence is profoundly enhancing the operational intelligence of high voltage inverters, moving beyond traditional control mechanisms to more adaptive and predictive functionalities. For instance, AI algorithms are being deployed for real-time fault detection and diagnosis, allowing inverters to identify anomalies and potential failures before they lead to system downtime, thereby significantly improving reliability and reducing maintenance costs. This capability is particularly crucial in critical applications such as electric vehicle powertrains and large-scale renewable energy farms.

Furthermore, AI-driven optimization techniques are transforming how high voltage inverters manage power flow and energy conversion. Machine learning models can analyze vast datasets of operational parameters, weather patterns, grid conditions, and load demands to dynamically adjust inverter settings for maximum efficiency and power output. This level of granular control ensures that energy conversion losses are minimized, and power quality is optimized, which is vital for grid stability and energy conservation. The ability of AI to learn from historical data and adapt to changing environmental and operational conditions makes inverters more resilient and performant.

The integration of AI also extends to advanced grid management and demand-response applications. Smart inverters, empowered by AI, can communicate seamlessly with grid operators, participating in frequency regulation, voltage support, and peak shaving services. This intelligent interaction enables better utilization of renewable energy sources, smoother grid integration, and enhanced grid resilience against fluctuations. While the benefits are substantial, concerns often arise regarding data security, the complexity of AI model deployment, and the need for robust computational resources, all of which are being addressed through ongoing research and development to unlock the full potential of AI in high voltage inverter technology.

- Enhanced predictive maintenance and fault detection through AI algorithms.

- Optimized energy conversion efficiency and power quality via machine learning.

- Improved grid integration and stability through AI-driven demand response.

- Development of self-learning and adaptive control systems for varying operating conditions.

- Potential for cybersecurity risks and the need for robust data protection in AI-enabled systems.

Key Takeaways High Voltage Inverter Market Size & Forecast

Analyzing common user questions about the High Voltage Inverter market size and forecast reveals a strong interest in understanding the primary growth catalysts, regional market dominance, and the long-term sustainability of the projected growth. A significant takeaway is the undeniable correlation between the rapid expansion of the electric vehicle (EV) industry and the surging demand for high voltage inverters. EVs, ranging from passenger cars to heavy-duty trucks, are fundamentally reliant on efficient inverters for powertrain management, making automotive electrification a colossal driver for market expansion. This trend is not confined to passenger vehicles but extends to electric buses, trains, and marine vessels, signifying a broad-based demand across the transportation sector.

Another crucial insight is the pivotal role of renewable energy integration, particularly solar and wind power, in shaping the high voltage inverter market's trajectory. As countries worldwide commit to decarbonization targets, the deployment of large-scale solar farms and wind turbines necessitates robust and high-efficiency inverters to convert generated DC power into AC power suitable for grid injection. The increasing capacity of these renewable energy projects directly translates into a higher demand for advanced high voltage inverter solutions, supporting grid modernization and energy transition efforts. This application segment is characterized by a continuous push for higher power ratings and grid-friendly features.

Geographically, Asia Pacific is emerging as a powerhouse, primarily due to aggressive investments in renewable energy infrastructure, burgeoning EV manufacturing hubs, and rapid industrialization in countries like China and India. This region is not only a major consumer but also a significant production base for high voltage inverters, driving innovation and cost efficiencies. The market forecast underscores a robust growth trajectory, propelled by ongoing technological advancements, supportive government policies promoting electrification, and the global imperative to transition towards cleaner energy sources. While initial investment costs and grid integration complexities remain considerations, the overarching demand for efficient power conversion solutions ensures sustained market expansion well into the next decade.

- Electric Vehicle (EV) adoption is the primary growth engine, particularly in passenger and commercial segments.

- Renewable energy integration, specifically solar and wind, significantly contributes to market expansion.

- Asia Pacific region is projected to be the largest and fastest-growing market due to favorable policies and industrial growth.

- Technological advancements in SiC/GaN and smart inverter features are enhancing performance and driving adoption.

- Global energy transition and decarbonization efforts provide a foundational demand for high voltage inverters.

High Voltage Inverter Market Drivers Analysis

The High Voltage Inverter market is propelled by a confluence of powerful drivers, each contributing significantly to its robust growth trajectory. A primary driver is the accelerating global adoption of electric vehicles (EVs), encompassing passenger cars, commercial fleets, and public transport. High voltage inverters are indispensable components in EV powertrains, converting DC battery power to AC for motor operation and managing regenerative braking, thereby directly linking EV sales growth to inverter demand. As battery technology advances and charging infrastructure expands, the impetus for EV adoption strengthens, creating sustained demand for highly efficient and compact high voltage inverter solutions.

Another critical driver is the increasing global investment in renewable energy sources, particularly utility-scale solar and wind power projects. High voltage inverters are fundamental to these installations, converting the variable DC output from solar panels or rectified AC from wind turbines into stable, grid-compatible AC power. Government incentives, falling costs of renewable energy generation, and ambitious decarbonization targets worldwide are fueling massive deployments of these projects, consequently boosting the demand for high-capacity, grid-tied high voltage inverters. This shift towards green energy infrastructure creates a long-term growth opportunity for the market.

Furthermore, the modernization of industrial infrastructure and the growing demand for energy-efficient industrial motors and drives also serve as significant market drivers. High voltage inverters enable precise control and variable speed operation of industrial motors, leading to substantial energy savings and improved operational efficiency in manufacturing, HVAC, and process industries. As industries increasingly adopt automation and seek to reduce energy consumption, the integration of advanced inverter technology becomes a strategic imperative. The combined effect of these drivers creates a resilient and expanding market for high voltage inverters across various sectors.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Electric Vehicle (EV) Adoption | +5.0% | North America, Europe, Asia Pacific (China, Japan, South Korea) | 2025-2033 (Long-term) |

| Growing Investment in Renewable Energy | +4.5% | Asia Pacific (China, India), Europe, North America | 2025-2033 (Long-term) |

| Industrial Automation and Energy Efficiency Mandates | +3.0% | Europe, North America, Asia Pacific | 2025-2030 (Medium-term) |

| Advancements in Power Semiconductor Technology (SiC, GaN) | +2.5% | Global | 2025-2033 (Ongoing) |

| Expansion of Grid Infrastructure and HVDC Projects | +2.0% | China, India, Europe, North America | 2026-2033 (Long-term) |

High Voltage Inverter Market Restraints Analysis

Despite the robust growth drivers, the High Voltage Inverter market faces several significant restraints that could impede its full potential. One major restraint is the relatively high initial cost associated with advanced high voltage inverter systems, particularly those incorporating newer technologies like Silicon Carbide (SiC) and Gallium Nitride (GaN). While these materials offer superior performance and efficiency, their manufacturing processes are complex and currently more expensive than traditional silicon-based components. This higher upfront investment can be a deterrent for cost-sensitive applications or smaller businesses, potentially slowing down the adoption rate, especially in emerging economies where budget constraints are more pronounced.

Another significant challenge stems from the complexity of design, integration, and thermal management in high-power applications. High voltage inverters operate under immense electrical and thermal stresses, requiring sophisticated cooling systems, robust insulation, and precise control algorithms to ensure reliability and longevity. The intricate engineering involved in designing compact yet highly efficient inverters for demanding environments, such as electric vehicle powertrains or utility-scale renewable energy plants, necessitates specialized expertise and rigorous testing. This complexity can lead to longer development cycles and higher R&D costs, limiting the pace of market innovation and product diversification for some manufacturers.

Furthermore, the global supply chain for critical components, including power semiconductors and specialized capacitors, presents a potential restraint. Geopolitical tensions, trade disputes, and unforeseen events such as pandemics can disrupt the supply of these essential materials, leading to production delays and increased costs. The reliance on a concentrated number of suppliers for advanced power electronics components introduces vulnerability, potentially impacting the timely delivery and overall pricing of high voltage inverters. Overcoming these supply chain fragilities requires strategic diversification and localized manufacturing initiatives, which are long-term endeavors.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Cost of Advanced Inverter Systems | -3.5% | Global, particularly Emerging Markets | 2025-2029 (Medium-term) |

| Complex Design and Thermal Management Challenges | -2.0% | Global | 2025-2033 (Long-term) |

| Supply Chain Disruptions for Key Components | -1.5% | Global | 2025-2027 (Short-term) |

| Lack of Standardization and Interoperability Issues | -1.0% | Global, especially emerging markets | 2025-2030 (Medium-term) |

| Grid Integration Complexities and Regulatory Hurdles | -1.0% | Specific Regions with evolving grids | 2026-2033 (Long-term) |

High Voltage Inverter Market Opportunities Analysis

The High Voltage Inverter market is rife with significant opportunities that can accelerate its growth and innovation. A substantial opportunity lies in the burgeoning demand for energy storage systems (ESS), particularly grid-scale battery storage and hybrid power plants. As renewable energy penetration increases, the intermittency of solar and wind power necessitates robust storage solutions, with high voltage inverters playing a critical role in managing the charge and discharge cycles and ensuring seamless grid integration. The global push for grid modernization and resilience opens new avenues for inverters capable of sophisticated energy management and ancillary grid services.

Another promising opportunity is the expansion into new and emerging applications beyond traditional EVs and renewables. This includes the electrification of heavy-duty vehicles (e.g., long-haul trucks, mining equipment), marine vessels, and rail transport, which require specialized high voltage inverter solutions tailored for extreme power demands and harsh operating conditions. Furthermore, the development of Vehicle-to-Grid (V2G) and Vehicle-to-Home (V2H) technologies, which allow EVs to feed power back to the grid or home, represents a transformative opportunity. These bidirectional power flows necessitate advanced high voltage inverters that can efficiently handle two-way energy conversion, thereby enhancing grid stability and providing additional revenue streams for EV owners.

Moreover, technological advancements, particularly in areas like Wide Bandgap (WBG) semiconductors (SiC and GaN), continue to unlock new performance benchmarks, creating opportunities for product differentiation and market expansion. The ongoing miniaturization, increased efficiency, and higher power density offered by WBG-based inverters enable their deployment in more compact and demanding spaces, fostering adoption in previously challenging applications. Coupled with the increasing integration of artificial intelligence and machine learning for predictive maintenance and optimized performance, these technological leaps position the market for continued innovation and the creation of highly intelligent, efficient, and reliable high voltage power conversion solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Energy Storage Systems (ESS) | +4.0% | Global, particularly North America, Europe, Asia Pacific | 2025-2033 (Long-term) |

| Electrification of Heavy-Duty Vehicles, Marine, and Rail | +3.5% | North America, Europe, Asia Pacific | 2026-2033 (Long-term) |

| Development of Vehicle-to-Grid (V2G) and V2H Technologies | +3.0% | Europe, North America, Japan, South Korea | 2027-2033 (Long-term) |

| Smart Grid Initiatives and Distributed Energy Resources | +2.5% | Global | 2025-2033 (Long-term) |

| Expansion in Emerging Markets and Rural Electrification | +2.0% | Asia Pacific (India, Southeast Asia), Africa, Latin America | 2026-2033 (Long-term) |

High Voltage Inverter Market Challenges Impact Analysis

The High Voltage Inverter market, while experiencing robust growth, confronts several inherent challenges that demand innovative solutions and strategic foresight. One significant challenge is managing the thermal dissipation in high-power density inverter designs. As inverters become more compact and powerful, the amount of heat generated increases, posing significant engineering hurdles for effective cooling. Inadequate thermal management can lead to reduced efficiency, decreased lifespan of components, and even system failures, particularly in demanding environments like automotive powertrains or utility-scale installations where space is limited and operating temperatures can be extreme. Developing advanced cooling solutions, such as liquid cooling or integrated heat sinks, is crucial but adds to complexity and cost.

Another key challenge involves ensuring the long-term reliability and robustness of high voltage inverters in diverse and often harsh operating conditions. Inverters are subjected to electrical stresses, vibrations, humidity, and temperature fluctuations, which can degrade components over time. The stringent reliability requirements, especially in automotive and grid applications where failures can have severe consequences, necessitate rigorous testing, robust component selection, and sophisticated fault-tolerant designs. Meeting these high standards while also keeping manufacturing costs competitive remains a continuous balancing act for manufacturers, influencing product development cycles and market entry barriers for new players.

Furthermore, the rapid pace of technological evolution, particularly in power semiconductor materials and control algorithms, presents a double-edged sword. While it drives innovation, it also creates a challenge for manufacturers to keep pace with the latest advancements, requiring continuous investment in research and development. The need for specialized expertise in areas like Wide Bandgap (WBG) materials, complex software integration, and system-level optimization means that talent acquisition and retention are critical. Moreover, the evolving regulatory landscape, especially concerning grid codes and safety standards for high voltage systems, demands constant adaptation and compliance, which can be time-consuming and costly for market participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Thermal Management in High Power Density Designs | -2.5% | Global | 2025-2033 (Long-term) |

| Ensuring Long-Term Reliability and Durability | -2.0% | Global | 2025-2033 (Long-term) |

| Cybersecurity Risks in Smart Inverter Systems | -1.5% | Global | 2026-2033 (Long-term) |

| High Research and Development Investment Requirements | -1.0% | Global | 2025-2030 (Medium-term) |

| Evolving Regulatory Landscape and Grid Code Compliance | -1.0% | Global, particularly developed economies | 2025-2033 (Ongoing) |

High Voltage Inverter Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the High Voltage Inverter market, offering a detailed understanding of its size, growth trends, competitive landscape, and future outlook. It encapsulates insights into market dynamics, including key drivers, restraints, opportunities, and challenges, along with a thorough segmentation and regional analysis, enabling stakeholders to make informed strategic decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | 25.5 Billion USD |

| Market Forecast in 2033 | 105.8 Billion USD |

| Growth Rate | 18.5% |

| Number of Pages | 256 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ABB, Siemens AG, Schneider Electric SE, Danfoss A/S, Eaton Corporation plc, Delta Electronics, Inc., Hitachi Ltd., Mitsubishi Electric Corporation, Toshiba Corporation, TDK Corporation, Parker Hannifin Corporation, SolarEdge Technologies, Inc., Huawei Technologies Co., Ltd., Fronius International GmbH, SMA Solar Technology AG, Vacon (now part of Danfoss), Yaskawa Electric Corporation, Fuji Electric Co., Ltd., Infineon Technologies AG, NXP Semiconductors N.V. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The High Voltage Inverter market is extensively segmented across various parameters including type, power rating, application, and end-use industry, providing a granular view of its diverse landscape. This segmentation allows for a detailed understanding of where growth opportunities are most concentrated and how different technological approaches cater to specific market needs. The differentiation by inverter type, for instance, highlights the prevalence and evolving capabilities of single-phase and three-phase systems in meeting varying power requirements for homes, businesses, and industrial operations.

Further segmentation by power rating (low, medium, high) is crucial for identifying market demand across a spectrum of applications, from residential solar installations to large-scale grid infrastructure projects and heavy-duty electric vehicles. This categorization helps to pinpoint the specific engineering challenges and market requirements unique to each power class. The application-based segmentation, spanning electric vehicles, renewable energy, industrial motors, and grid infrastructure, directly reflects the primary end-use cases driving the market's expansion, with each segment exhibiting distinct growth dynamics influenced by policy, technological maturity, and consumer adoption.

Finally, the end-use industry segmentation provides insight into the vertical markets that are increasingly relying on high voltage inverters for their electrification and energy efficiency initiatives. The automotive sector, for example, is experiencing unprecedented growth in demand, while the energy and utilities sector is driven by the global transition to sustainable energy. This multi-faceted segmentation ensures a comprehensive analysis, allowing stakeholders to identify niche markets, assess competitive positioning, and tailor strategies to capitalize on the most promising avenues within the high voltage inverter ecosystem.

- By Type:

- Single-Phase

- Three-Phase

- By Power Rating:

- Low Power (<10 kW)

- Medium Power (10 kW - 100 kW)

- High Power (>100 kW)

- By Application:

- Electric Vehicles (EVs)

- Passenger EVs

- Commercial EVs

- Electric Buses

- Renewable Energy

- Solar Inverters

- Wind Inverters

- Industrial Motors & Drives

- Grid Infrastructure

- HVDC Converters

- FACTS Devices

- Energy Storage Systems

- Rail & Marine

- Electric Vehicles (EVs)

- By End-Use Industry:

- Automotive

- Energy & Utilities

- Manufacturing & Industrial

- Transportation (Rail & Marine)

- Commercial & Residential

Regional Highlights

The global High Voltage Inverter market exhibits distinct regional dynamics, with specific geographical areas emerging as key growth hubs due to varying levels of industrialization, renewable energy policies, and electric vehicle adoption rates. North America, encompassing the United States and Canada, represents a significant market driven by substantial investments in grid modernization, renewable energy projects, and the accelerating transition towards electric mobility. The region benefits from strong government incentives for EV adoption and solar installations, coupled with a robust industrial sector that increasingly integrates high voltage inverters for efficiency gains. Furthermore, a strong presence of key technology developers and research institutions fosters continuous innovation, particularly in advanced power electronics and smart grid solutions.

Europe stands as a mature yet rapidly evolving market, propelled by stringent environmental regulations, ambitious decarbonization targets, and pioneering efforts in renewable energy integration. Countries like Germany, Norway, and the United Kingdom are leading the charge in electric vehicle penetration and offshore wind energy deployment, creating consistent demand for high-efficiency and reliable high voltage inverters. The region's focus on sustainable development, coupled with significant R&D in power semiconductor technologies and grid-interactive inverters, positions it as a key innovator and early adopter of advanced inverter solutions, particularly for Vehicle-to-Grid (V2G) applications and sophisticated energy storage systems.

Asia Pacific (APAC) is projected to be the largest and fastest-growing market for high voltage inverters, primarily due to the overwhelming growth in China, Japan, South Korea, and India. China's unparalleled expansion in electric vehicle manufacturing and renewable energy capacity, along with its massive industrial base, makes it a dominant force in both demand and supply. India's aggressive renewable energy targets and burgeoning EV market also contribute significantly to regional growth. This region benefits from favorable government policies, rapid urbanization, and extensive infrastructure development, leading to a surge in demand for high voltage inverters across automotive, energy, and industrial sectors. The sheer scale of development in APAC positions it as the epicenter of future market expansion.

Latin America and the Middle East & Africa (MEA) are emerging markets with considerable growth potential, albeit from a lower base. In Latin America, countries like Brazil and Mexico are witnessing increasing investments in renewable energy, particularly solar and wind, and a nascent but growing interest in electric mobility. These developments are gradually driving the demand for high voltage inverters. Similarly, the MEA region, particularly the GCC countries, is diversifying its energy mix away from fossil fuels, with significant solar power projects and smart city initiatives requiring advanced power conversion technologies. While challenges like infrastructure development and policy frameworks exist, the long-term outlook for these regions remains positive as they increasingly embrace electrification and sustainable energy solutions.

- North America: Strong growth driven by EV adoption, grid modernization, and renewable energy investments.

- Europe: High adoption rates due to strict environmental policies, advanced grid integration, and V2G initiatives.

- Asia Pacific (APAC): Dominant and fastest-growing market, fueled by massive EV manufacturing, renewable energy expansion, and industrialization in China and India.

- Latin America: Emerging market with growing investments in renewable energy and developing EV infrastructure.

- Middle East & Africa (MEA): Gradually increasing adoption driven by diversification of energy sources and smart city projects.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the High Voltage Inverter Market.- ABB

- Siemens AG

- Schneider Electric SE

- Danfoss A/S

- Eaton Corporation plc

- Delta Electronics, Inc.

- Hitachi Ltd.

- Mitsubishi Electric Corporation

- Toshiba Corporation

- TDK Corporation

- Parker Hannifin Corporation

- SolarEdge Technologies, Inc.

- Huawei Technologies Co., Ltd.

- Fronius International GmbH

- SMA Solar Technology AG

- Vacon (now part of Danfoss)

- Yaskawa Electric Corporation

- Fuji Electric Co., Ltd.

- Infineon Technologies AG

- NXP Semiconductors N.V.

Frequently Asked Questions

Analyze common user questions about the High Voltage Inverter market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a high voltage inverter?

A high voltage inverter is an electronic device that converts direct current (DC) power from a source, such as a battery or solar panel, into alternating current (AC) power at a high voltage level. These inverters are critical for applications requiring substantial power output, including electric vehicle powertrains, large-scale renewable energy systems, and industrial motor drives, enabling efficient energy conversion and management.

What are the primary applications driving the High Voltage Inverter market?

The High Voltage Inverter market is predominantly driven by the rapid growth of Electric Vehicles (EVs), where they manage power for electric motors and regenerative braking. Other key applications include large-scale renewable energy systems (solar and wind farms), industrial motor control for energy efficiency, and grid infrastructure projects like High Voltage Direct Current (HVDC) transmission.

How is AI impacting the performance and reliability of high voltage inverters?

AI is significantly enhancing high voltage inverters by enabling predictive maintenance, optimizing energy conversion efficiency through real-time data analysis, and improving grid integration. AI algorithms can detect anomalies, adjust operational parameters for peak performance, and facilitate smarter interaction with the power grid, leading to increased reliability and extended lifespan.

Which region holds the largest share in the High Voltage Inverter market?

The Asia Pacific (APAC) region currently holds the largest share and is projected to be the fastest-growing market for High Voltage Inverters. This dominance is attributed to extensive investments in electric vehicle manufacturing, significant expansion of renewable energy capacity, and rapid industrialization, particularly in countries like China and India.

What are the key technological advancements shaping the future of high voltage inverters?

Key technological advancements include the widespread adoption of Wide Bandgap (WBG) semiconductors like Silicon Carbide (SiC) and Gallium Nitride (GaN) for higher efficiency and power density. The increasing integration of smart features, advanced control algorithms, and bidirectional capabilities for Vehicle-to-Grid (V2G) applications are also pivotal in shaping the market's future.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted