Extra High Voltage Cable Market

Extra High Voltage Cable Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702542 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Extra High Voltage Cable Market Size

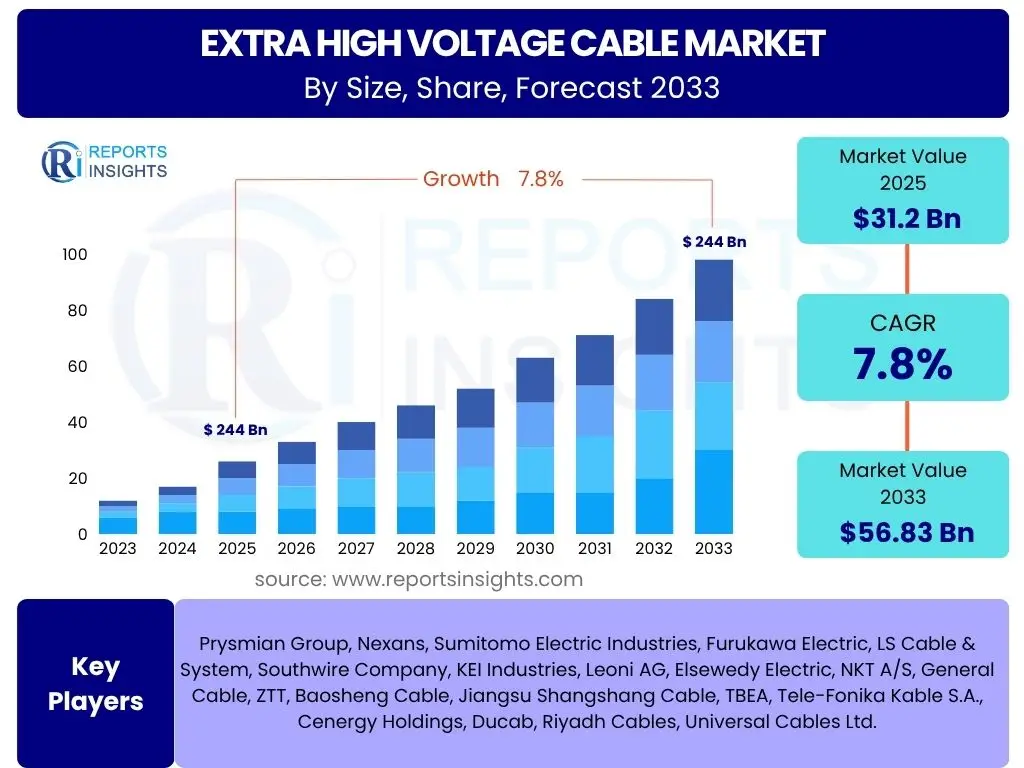

According to Reports Insights Consulting Pvt Ltd, The Extra High Voltage Cable Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 31.2 Billion in 2025 and is projected to reach USD 56.83 Billion by the end of the forecast period in 2033.

Key Extra High Voltage Cable Market Trends & Insights

The Extra High Voltage (EHV) Cable market is witnessing significant transformation driven by global energy transitions and grid modernization imperatives. A predominant trend is the accelerating integration of renewable energy sources, such as large-scale wind and solar farms, which necessitates robust EHV transmission infrastructure to connect remote generation sites to consumption centers. This includes the development of extensive offshore wind projects, particularly in Europe and Asia, requiring specialized submarine EHV cables capable of withstanding harsh marine environments and transmitting power over long distances with minimal losses. The demand for EHV cables is also being propelled by the strategic imperative to enhance grid reliability and resilience, leading to substantial investments in upgrading aging transmission networks and developing smart grid functionalities.

Another crucial trend is the increasing adoption of High Voltage Direct Current (HVDC) transmission technology. HVDC systems offer distinct advantages for long-distance power transmission and interregional grid connections, including lower transmission losses, reduced right-of-way requirements, and enhanced grid stability, especially when integrating intermittent renewable energy. This has led to a surge in demand for HVDC cables, both terrestrial and submarine, capable of operating at higher voltages and capacities. Furthermore, urbanization and industrial growth in emerging economies are fueling demand for reliable and efficient power supply, often leading to undergrounding projects for aesthetic and safety reasons, thereby boosting the market for underground EHV cables. The continuous innovation in cable materials, insulation technologies, and installation techniques is also a key insight, contributing to more efficient, durable, and environmentally friendly EHV cable solutions.

- Accelerated integration of large-scale renewable energy projects (wind, solar).

- Rising global investments in grid modernization and infrastructure upgrades.

- Increasing adoption of High Voltage Direct Current (HVDC) transmission technology.

- Growing trend towards undergrounding of transmission lines in urban and sensitive areas.

- Technological advancements in cable materials and insulation (e.g., XLPE, MI).

- Expansion of cross-border and inter-regional grid interconnections.

- Focus on enhancing grid reliability, resilience, and smart grid integration.

AI Impact Analysis on Extra High Voltage Cable

Artificial Intelligence (AI) is poised to significantly transform various facets of the Extra High Voltage Cable market, primarily by enhancing operational efficiency, predictive maintenance, and overall grid management. Users are increasingly curious about how AI can optimize the lifespan and performance of these critical assets. AI algorithms can analyze vast datasets from sensors embedded in EHV cables, including temperature, vibration, and partial discharge measurements, to detect anomalies and predict potential failures before they occur. This shifts the maintenance paradigm from reactive to proactive, minimizing downtime, reducing operational costs, and extending the operational life of the cables. Such predictive capabilities are particularly valuable for complex and expensive EHV infrastructure, where failures can lead to widespread power outages and significant financial repercussions.

Beyond predictive maintenance, AI also plays a crucial role in optimizing EHV cable network design, capacity planning, and real-time load balancing. AI-powered analytics can simulate various scenarios, identify optimal routing for new cable installations, and manage power flow more efficiently across existing networks, especially with the fluctuating output from renewable energy sources. This contributes to better utilization of grid assets and improved energy transmission efficiency. Concerns often revolve around data security, integration complexity with legacy systems, and the need for specialized AI expertise, yet the potential benefits in terms of reliability, safety, and economic performance are driving increased research and pilot projects. AI's ability to process and interpret complex data patterns offers an unprecedented level of insight into EHV cable health and performance, paving the way for more intelligent and resilient power grids.

- Predictive maintenance and fault detection through real-time data analysis.

- Optimization of cable performance and lifespan through AI-driven insights.

- Enhanced grid stability and efficiency via AI-powered load balancing.

- Automated monitoring and anomaly detection for critical EHV infrastructure.

- Improved resource allocation for maintenance and repair operations.

- Intelligent asset management and lifecycle optimization for EHV cables.

Key Takeaways Extra High Voltage Cable Market Size & Forecast

The Extra High Voltage Cable market is positioned for robust growth throughout the forecast period, primarily driven by the global imperative to decarbonize energy systems and modernize power grids. A significant takeaway is that the transition to renewable energy sources, particularly large-scale offshore wind and solar projects, directly fuels the demand for EHV cables to transmit clean power from generation hubs to consumption centers. This necessitates substantial investments in new transmission lines and the upgrading of existing infrastructure to handle higher capacities and integrate intermittent power flows effectively. The market expansion is also significantly influenced by the increasing focus on enhancing grid reliability and reducing transmission losses, prompting utilities and grid operators to invest in advanced EHV cable solutions.

Another crucial insight is the escalating adoption of High Voltage Direct Current (HVDC) technology, which represents a key enabler for long-distance, high-capacity power transmission and intercontinental grid interconnections. This trend is expected to contribute significantly to the market's value growth, especially in regions with extensive landmasses or deep-sea energy projects. Furthermore, strategic government initiatives and regulatory frameworks supporting renewable energy targets and grid infrastructure development are pivotal in shaping the market landscape. The market's growth trajectory underscores the critical role EHV cables play as foundational components of a resilient, efficient, and sustainable global energy infrastructure, making them indispensable for achieving future energy security and environmental goals.

- Market growth is fundamentally linked to global renewable energy expansion.

- HVDC technology adoption is a primary catalyst for long-distance transmission projects.

- Grid modernization and infrastructure resilience are key investment drivers.

- Asia Pacific and Europe are expected to be major growth hubs due to energy transitions.

- Underground and submarine installations are gaining traction for reliability and aesthetics.

- Continuous technological advancements are crucial for market innovation and efficiency.

Extra High Voltage Cable Market Drivers Analysis

The Extra High Voltage Cable market is propelled by a confluence of interconnected drivers, primarily stemming from the global shift towards sustainable energy and the urgent need for robust power infrastructure. The escalating demand for electricity, fueled by urbanization, industrial growth, and digitalization, necessitates expanding and upgrading existing transmission networks. This expansion often involves EHV cables due to their efficiency in transmitting large blocks of power over long distances with minimal losses, making them indispensable for meeting burgeoning energy requirements worldwide. Furthermore, the imperative to connect increasingly remote renewable energy generation sites, such as large offshore wind farms and expansive solar parks, to major load centers significantly boosts the demand for high-capacity EHV cables, particularly specialized submarine and land HVDC cables. These cables are critical for transferring clean energy efficiently across vast distances, often bridging geographical barriers.

Government initiatives and significant investments in grid modernization and inter-regional grid interconnections also act as potent market drivers. Countries are investing heavily in upgrading aging transmission infrastructure, enhancing grid reliability, and reducing transmission losses. This includes projects aimed at creating interconnected smart grids that can intelligently manage power flow and integrate diverse energy sources. Cross-border energy trading and regional power pooling arrangements further necessitate the installation of new EHV cable lines to facilitate efficient power exchange between nations, improving energy security and market efficiency. These drivers collectively underscore the essential role of EHV cables in facilitating the global energy transition and ensuring reliable power delivery.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Renewable Energy Integration | +2.5% | Europe, Asia Pacific, North America | Long-term (2025-2033) |

| Grid Modernization & Infrastructure Development | +2.0% | North America, Europe, China, India | Medium-term (2025-2030) |

| Growing Demand for Electricity | +1.5% | Asia Pacific (Emerging Economies), Latin America | Long-term (2025-2033) |

| Urbanization & Industrialization | +1.0% | Asia Pacific, Middle East & Africa | Medium-term (2025-2030) |

| Cross-border Interconnections | +0.8% | Europe, Southeast Asia, North Africa | Medium-term (2025-2030) |

Extra High Voltage Cable Market Restraints Analysis

Despite significant growth drivers, the Extra High Voltage Cable market faces several notable restraints that can impede its expansion. One of the primary inhibitors is the extremely high capital investment required for EHV cable projects. These projects involve substantial costs not only for the cables themselves, which are complex to manufacture and require specialized materials, but also for intricate installation processes, sophisticated civil engineering works, and extensive testing. The financial burden can be prohibitive for some developing economies or utilities with limited budgets, leading to delays or cancellation of essential infrastructure upgrades. Additionally, obtaining the necessary regulatory approvals and permits for EHV cable routes, particularly for underground or submarine installations that cross diverse terrains or international waters, can be a protracted and challenging process. Environmental impact assessments and public opposition to new power lines often contribute to significant project delays and increased costs.

Technical challenges associated with installation and maintenance also pose a restraint. Laying EHV cables, especially underground or subsea, requires highly specialized equipment, expertise, and precision, and any errors can lead to costly repairs and operational disruptions. Furthermore, the long lead times for EHV cable manufacturing and project execution can be a bottleneck, affecting the pace of grid development. Environmental concerns, such as the impact on ecosystems during cable laying, particularly for submarine cables, and the management of heat dissipation for underground cables, also present regulatory and technical hurdles. These factors collectively necessitate meticulous planning, substantial financial resources, and coordinated efforts across multiple stakeholders, thereby posing a notable challenge to the rapid proliferation of EHV cable projects.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Investment | -1.2% | Global, Developing Economies | Long-term (Ongoing) |

| Regulatory Hurdles & Permitting | -1.0% | North America, Europe, Asia Pacific | Long-term (Ongoing) |

| Technical Challenges in Installation & Maintenance | -0.8% | Global | Long-term (Ongoing) |

| Environmental Concerns & Land Acquisition Issues | -0.7% | Europe, North America, Highly Populated Areas | Medium-term (2025-2030) |

Extra High Voltage Cable Market Opportunities Analysis

The Extra High Voltage Cable market presents significant opportunities for growth and innovation, primarily driven by the evolution of power transmission technologies and the increasing demand for sustainable and resilient energy infrastructure. A prominent opportunity lies in the accelerating global adoption of High Voltage Direct Current (HVDC) technology. HVDC offers superior efficiency for long-distance power transmission, interconnection of asynchronous grids, and integration of large-scale renewable energy sources, especially offshore wind farms. As more countries commit to ambitious renewable energy targets and grid modernization, the demand for advanced HVDC cables, both land and submarine, will continue to surge. This presents opportunities for manufacturers to invest in R&D for higher voltage capacity cables, enhanced insulation materials, and more efficient installation techniques, catering to the unique requirements of HVDC projects.

Another compelling opportunity is the expansion of offshore wind farm development, particularly in Europe, Asia Pacific, and North America. These massive renewable energy projects require extensive networks of submarine EHV cables to transmit power generated far out at sea back to the onshore grid. The increasing size and complexity of these farms necessitate cables with higher voltage ratings, enhanced durability, and specialized installation capabilities, creating a niche market for manufacturers with expertise in this segment. Furthermore, the global push towards building smart cities and resilient grid infrastructures, often involving undergrounding power lines for aesthetic and safety reasons, offers additional avenues for market expansion. The continuous development of innovative materials, such as superconducting cables or advanced composite conductors, also presents long-term opportunities for improved efficiency and reduced environmental footprint, allowing companies to differentiate their offerings and capture new market segments.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| HVDC Technology Adoption & Expansion | +1.8% | Europe, Asia Pacific, North America | Long-term (2025-2033) |

| Offshore Wind Farm Connectivity | +1.5% | Europe, East Asia, North America | Long-term (2025-2033) |

| Smart Grid & Digitalization Integration | +1.0% | North America, Europe, Developed Asia Pacific | Medium-term (2025-2030) |

| Development of Smart Cities & Undergrounding Projects | +0.9% | Developed Urban Centers Globally | Medium-term (2025-2030) |

Extra High Voltage Cable Market Challenges Impact Analysis

The Extra High Voltage Cable market faces several significant challenges that can impede its growth and operational efficiency. One major hurdle is the inherent complexity and high cost associated with the manufacturing, transportation, and installation of EHV cables. These cables are highly specialized products requiring sophisticated manufacturing processes, robust quality control, and large-scale, heavy equipment for deployment, particularly for submarine or deeply buried underground installations. The substantial upfront capital outlay and the long project lead times can deter potential investments, especially in regions with limited financial resources or unstable economic conditions. Furthermore, the volatility of raw material prices, such as copper, aluminum, and various polymers used in insulation, presents a significant challenge. Sudden fluctuations can impact manufacturing costs, project profitability, and the overall competitiveness of market players, requiring manufacturers to develop robust supply chain management strategies.

Another pressing challenge is the shortage of highly skilled labor and specialized expertise required for the design, installation, and maintenance of EHV cable systems. The intricate nature of these projects demands a workforce with advanced technical skills in electrical engineering, civil works, and marine operations (for submarine cables). The aging workforce in many developed countries and the limited availability of specialized training programs contribute to this talent gap, potentially leading to project delays, increased labor costs, and compromised quality. Additionally, cybersecurity risks are emerging as a critical concern for grid infrastructure, including EHV cable monitoring and control systems. The increasing digitalization of power grids makes them vulnerable to cyberattacks, which could disrupt power transmission, compromise data integrity, or even cause physical damage. Geopolitical instability and trade disputes can also disrupt global supply chains and cross-border project collaborations, adding another layer of complexity to market operations. Addressing these challenges requires strategic investments in training, robust risk management, and international cooperation.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Project Complexity & Cost | -1.5% | Global | Long-term (Ongoing) |

| Raw Material Price Volatility | -1.0% | Global | Short to Medium-term (2025-2028) |

| Skilled Labor Shortage | -0.9% | North America, Europe, Developed Asia | Long-term (Ongoing) |

| Cybersecurity Risks to Grid Infrastructure | -0.7% | Global | Long-term (Ongoing) |

Extra High Voltage Cable Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Extra High Voltage Cable market, covering key market dynamics, segmentation, regional insights, and competitive landscape. The report offers a detailed forecast of market size and growth trajectory, driven by factors such as renewable energy integration, grid modernization initiatives, and increasing power demand worldwide. It also includes a thorough examination of market drivers, restraints, opportunities, and challenges, providing a holistic view of the industry's potential and limitations. Furthermore, the report incorporates an AI impact analysis, detailing how artificial intelligence is transforming the operational efficiency and management of EHV cable infrastructure.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 31.2 Billion |

| Market Forecast in 2033 | USD 56.83 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Prysmian Group, Nexans, Sumitomo Electric Industries, Furukawa Electric, LS Cable & System, Southwire Company, KEI Industries, Leoni AG, Elsewedy Electric, NKT A/S, General Cable, ZTT, Baosheng Cable, Jiangsu Shangshang Cable, TBEA, Tele-Fonika Kable S.A., Cenergy Holdings, Ducab, Riyadh Cables, Universal Cables Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Extra High Voltage Cable market is extensively segmented based on several key parameters to provide a granular view of its diverse landscape and growth opportunities. These segmentations allow for a detailed analysis of market dynamics across different cable types, installation methods, voltage ratings, and end-use applications. Understanding these segments is crucial for identifying specific growth pockets and tailoring strategies to meet distinct market needs, reflecting the complex demands of modern power transmission infrastructure globally. The market's diverse applications, ranging from connecting large-scale renewable energy projects to reinforcing urban grids, necessitate a broad spectrum of EHV cable solutions, each with specific technical requirements and market drivers.

The segmentation by type primarily distinguishes between High Voltage Alternating Current (HVAC) and High Voltage Direct Current (HVDC) cables, reflecting the evolving technological landscape for power transmission. Installation methods categorize cables as overhead, underground, or submarine, each presenting unique engineering challenges and environmental considerations. Voltage ratings provide further granularity, essential for classifying cables based on their transmission capacity. Finally, the application and end-use segments highlight the diverse sectors that rely on EHV cables, from utilities managing national grids to industrial facilities and large-scale commercial developments requiring robust power supply. This comprehensive segmentation underscores the market's adaptability and critical role across various facets of energy infrastructure development.

- By Type:

- HVAC (High Voltage Alternating Current)

- HVDC (High Voltage Direct Current)

- By Installation:

- Overhead

- Underground

- Submarine

- By Voltage:

- 220kV to 400kV

- 401kV to 600kV

- Above 600kV

- By Application:

- Grid Interconnection

- Renewable Energy Integration (Onshore/Offshore Wind, Solar)

- Industrial (Oil & Gas, Mining, Manufacturing)

- Urban Infrastructure

- Others

- By End-Use:

- Utilities

- Industrial

- Commercial

Regional Highlights

- Asia Pacific (APAC): The largest and fastest-growing market for EHV cables, driven by rapid industrialization, urbanization, and substantial government investments in grid expansion and renewable energy projects (e.g., China, India, Japan). High demand for long-distance transmission lines and offshore wind farm connections.

- Europe: A mature market with significant growth fueled by ambitious renewable energy targets, extensive offshore wind development, and the modernization of aging grid infrastructure. Strong emphasis on cross-border interconnections and HVDC projects (e.g., Germany, UK, Nordic countries).

- North America: Experiencing robust demand due to grid modernization initiatives, replacement of aging infrastructure, and integration of renewable energy sources, particularly large-scale solar and wind farms. Focus on enhancing grid resilience and expanding smart grid capabilities (e.g., US, Canada).

- Latin America: Emerging market with increasing investments in power generation, particularly hydropower and solar, necessitating EHV transmission lines to connect new plants to urban centers. Grid expansion and regional interconnections are key drivers (e.g., Brazil, Chile).

- Middle East and Africa (MEA): Growing market due to substantial investments in infrastructure development, diversification of economies, and increasing power demand from industrial and commercial sectors. Development of mega-projects and inter-regional grid links (e.g., UAE, Saudi Arabia, South Africa).

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Extra High Voltage Cable Market.- Prysmian Group

- Nexans

- Sumitomo Electric Industries

- Furukawa Electric

- LS Cable & System

- Southwire Company

- KEI Industries

- Leoni AG

- Elsewedy Electric

- NKT A/S

- General Cable

- ZTT

- Baosheng Cable

- Jiangsu Shangshang Cable

- TBEA

- Tele-Fonika Kable S.A.

- Cenergy Holdings

- Ducab

- Riyadh Cables

- Universal Cables Ltd.

Frequently Asked Questions

What are Extra High Voltage (EHV) Cables?

Extra High Voltage (EHV) cables are specialized electrical cables designed to transmit electricity at very high voltages, typically above 220 kilovolts (kV). These cables are crucial for long-distance power transmission and for connecting large-scale power generation units to the main grid, minimizing energy losses and ensuring stable power supply. They are essential components of modern electricity grids, facilitating the efficient and reliable delivery of power across vast distances, including challenging terrains and underwater environments.

Why is the demand for EHV cables increasing globally?

The demand for EHV cables is increasing globally due to several key factors: the rapid integration of renewable energy sources (such as wind and solar farms) which often require long-distance transmission from remote generation sites; extensive investments in grid modernization and infrastructure upgrades to enhance reliability and efficiency; growing electricity demand driven by urbanization and industrialization; and the development of cross-border grid interconnections to facilitate energy trade and security. These drivers collectively necessitate robust EHV infrastructure for efficient power transmission.

What is the role of HVDC technology in the EHV cable market?

High Voltage Direct Current (HVDC) technology plays a pivotal role in the EHV cable market by offering superior efficiency for long-distance power transmission, particularly for submarine and underground applications. HVDC cables experience lower transmission losses compared to HVAC cables over long distances, making them ideal for connecting offshore wind farms, integrating asynchronous grids, and establishing intercontinental power links. The increasing adoption of HVDC technology is a significant growth driver, expanding the scope and capabilities of the EHV cable market.

What are the primary challenges faced by the EHV cable market?

The EHV cable market faces several significant challenges, including the substantial capital investment required for manufacturing and installation, which can be prohibitive for some projects. Other challenges include complex regulatory and permitting processes that can lead to project delays, volatility in raw material prices (like copper and aluminum), a shortage of highly skilled labor for specialized installations, and the growing concerns related to cybersecurity risks for digitalized grid infrastructure. Addressing these challenges is critical for the sustained growth of the market.

How does AI impact the Extra High Voltage Cable sector?

Artificial Intelligence (AI) impacts the Extra High Voltage Cable sector by enhancing operational efficiency, predictive maintenance, and grid optimization. AI algorithms analyze data from sensors to detect potential faults, predict equipment failures, and optimize cable performance, thereby minimizing downtime and extending asset life. Furthermore, AI assists in optimizing network design, capacity planning, and real-time load balancing, leading to more efficient power flow and improved grid stability. This intelligent approach transforms how EHV cable assets are managed, making grids more reliable and resilient.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted