Coal to Liquid Fuel Market

Coal to Liquid Fuel Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700107 | Last Updated : July 23, 2025 |

Format : ![]()

![]()

![]()

![]()

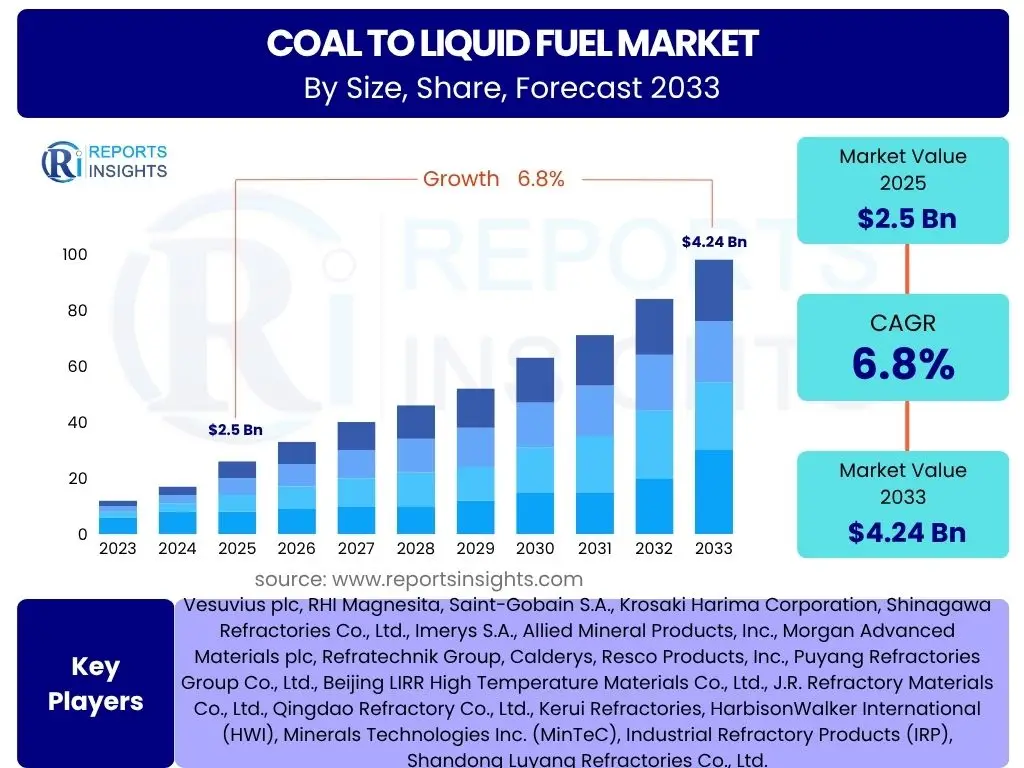

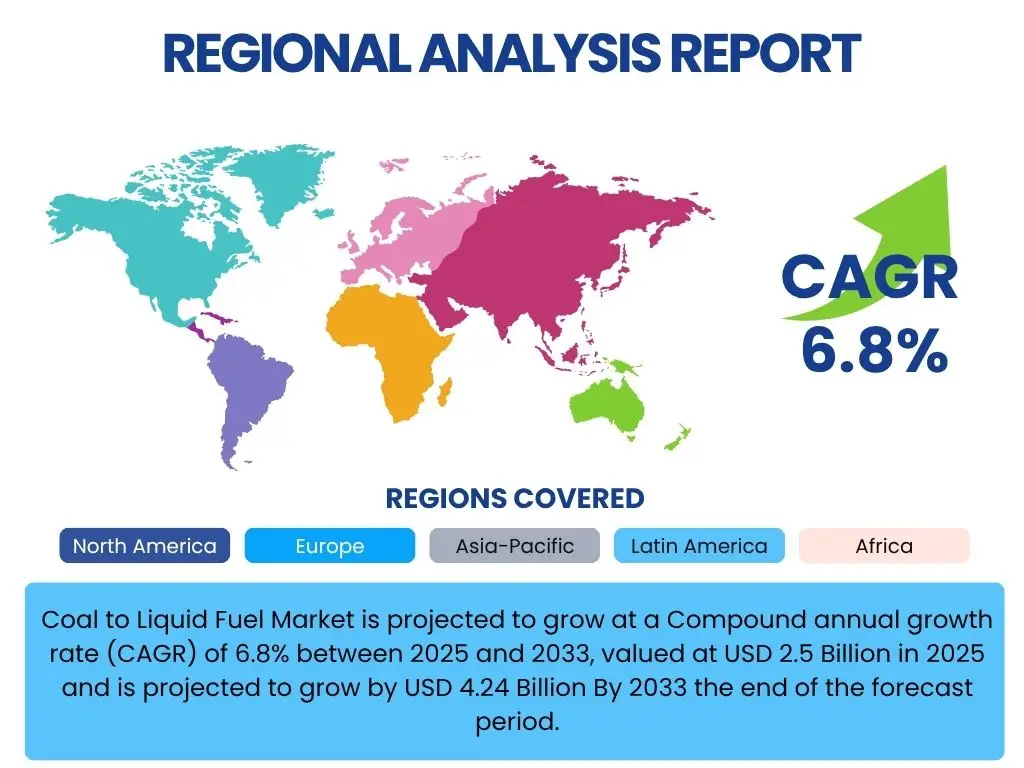

Coal to Liquid Fuel Market is projected to grow at a Compound annual growth rate (CAGR) of 6.8% between 2025 and 2033, current valued at USD 2.5 Billion in 2025 and is projected to grow by USD 4.24 Billion By 2033 the end of the forecast period.

Key Coal to Liquid Fuel Market Trends & Insights

The Coal to Liquid (CTL) fuel market is experiencing transformative shifts driven by global energy security imperatives and technological advancements aimed at enhancing process efficiency and reducing environmental impact. A notable trend is the increasing focus on integrating carbon capture and storage (CCS) technologies to mitigate greenhouse gas emissions, addressing a major environmental concern associated with coal utilization. Additionally, there is a growing emphasis on modular CTL plant designs, which offer greater flexibility, scalability, and reduced capital expenditure, making the technology more accessible for diverse regional energy strategies. The market is also witnessing a push towards co-production facilities that yield not only liquid fuels but also high-value chemicals, thereby improving economic viability and diversifying revenue streams for CTL operations.

- Integration of Carbon Capture and Storage (CCS) technologies to reduce environmental footprint.

- Development of modular and smaller-scale CTL plants for enhanced flexibility.

- Shift towards co-production of fuels and chemicals to improve economic efficiency.

- Focus on advanced catalytic processes to increase yield and selectivity.

- Rising interest in sustainable coal utilization strategies.

AI Impact Analysis on Coal to Liquid Fuel

Artificial intelligence (AI) is poised to revolutionize the Coal to Liquid (CTL) fuel industry by optimizing various stages of the production process, from feedstock management to product distribution. AI-driven predictive maintenance systems can forecast equipment failures, minimizing downtime and significantly improving operational efficiency and safety in complex CTL plants. Furthermore, AI algorithms can enhance process control by real-time monitoring and adjusting parameters such as temperature, pressure, and catalyst activity, leading to higher conversion rates and improved fuel quality. In research and development, AI accelerates the discovery of new catalysts and optimizes reaction pathways, reducing the time and cost associated with developing more efficient and environmentally friendly CTL technologies. This integration of AI not only streamlines operations but also contributes to the sustainability goals of the industry by optimizing resource utilization.

- AI-driven optimization of reaction parameters for enhanced yield and efficiency.

- Predictive maintenance for equipment in CTL plants, reducing operational costs and downtime.

- AI-powered simulation and modeling for process design and catalyst discovery.

- Enhanced supply chain management and logistics for coal feedstock and fuel distribution.

- Real-time monitoring and anomaly detection to improve safety and environmental compliance.

Key Takeaways Coal to Liquid Fuel Market Size & Forecast

- The global Coal to Liquid Fuel market is projected for substantial growth, driven by energy security concerns and technological advancements.

- Market valuation is estimated at USD 2.5 Billion in 2025, indicating a significant current market presence.

- The market is forecast to reach USD 4.24 Billion by 2033, demonstrating a robust compound annual growth rate of 6.8%.

- This growth trajectory highlights increasing investments and strategic importance of CTL technologies in the global energy mix.

- The forecast period emphasizes a steady expansion, offering considerable opportunities for stakeholders in the energy sector.

Coal to Liquid Fuel Market Drivers Analysis

The Coal to Liquid (CTL) fuel market is propelled by a confluence of critical factors, primarily centered on global energy independence and the abundant availability of coal reserves. Countries with significant coal deposits, yet limited domestic oil resources, view CTL as a strategic pathway to enhance their energy security and reduce reliance on volatile global oil markets. This geopolitical driver is compounded by the imperative to diversify energy portfolios and mitigate the economic impact of fluctuating crude oil prices. Furthermore, ongoing advancements in CTL technologies are making these processes more efficient, economically viable, and environmentally compliant, which in turn stimulates investment and adoption across various regions seeking to leverage their indigenous coal resources for liquid fuel production. The increasing demand for liquid transportation fuels, particularly in rapidly industrializing economies, also serves as a fundamental driver for the market's expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Energy Security Concerns | +1.2% | Asia Pacific, Middle East & Africa, North America | Long-term (5+ years) |

| Abundance of Coal Reserves | +1.0% | China, India, South Africa, USA, Australia | Mid-term (3-5 years) |

| Volatility of Crude Oil Prices | +0.9% | Global, particularly import-reliant nations | Short to Mid-term (1-5 years) |

| Technological Advancements in CTL Processes | +0.8% | Developed economies, R&D hubs | Long-term (5+ years) |

| Increasing Demand for Transportation Fuels | +0.7% | Emerging economies, rapidly industrializing regions | Mid-term (3-5 years) |

Coal to Liquid Fuel Market Restraints Analysis

Despite its strategic advantages, the Coal to Liquid (CTL) fuel market faces significant restraints that temper its growth trajectory. Paramount among these is the substantial capital expenditure required for establishing and operating CTL facilities, which often runs into billions of dollars, making project financing a considerable challenge. Environmental concerns also present a formidable hurdle; CTL processes are historically associated with high greenhouse gas emissions and intensive water consumption, drawing scrutiny from environmental advocacy groups and stringent regulatory bodies. This often leads to public opposition and delays in project approvals. Furthermore, the increasing global emphasis on renewable energy sources and the declining costs of alternatives like solar and wind power pose significant competitive pressure, potentially diverting investments away from fossil fuel-based technologies, including CTL. The inherent complexity of CTL processes also contributes to operational risks and challenges.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure (CAPEX) | -1.5% | Global, particularly developing nations | Long-term (5+ years) |

| Environmental Concerns (GHG Emissions, Water Usage) | -1.3% | Europe, North America, rapidly industrializing APAC countries | Mid to Long-term (3-8 years) |

| Competition from Renewable Energy Sources | -1.1% | Global, especially developed economies | Mid-term (3-5 years) |

| Fluctuating Crude Oil Prices (when low) | -0.8% | Global, particularly countries with crude oil imports | Short-term (1-3 years) |

| Regulatory Hurdles and Public Opposition | -0.7% | North America, Europe, parts of Asia Pacific | Mid-term (3-5 years) |

Coal to Liquid Fuel Market Opportunities Analysis

Significant opportunities are emerging within the Coal to Liquid (CTL) fuel market, largely driven by innovative technological integrations and evolving global energy landscapes. A primary opportunity lies in the integration of Carbon Capture and Storage (CCS) technologies, which can significantly reduce the carbon footprint of CTL plants, making them more environmentally acceptable and compliant with stricter climate regulations. This integration not only addresses environmental concerns but also potentially opens avenues for carbon credit markets. Furthermore, the strategic co-production of high-value chemicals alongside liquid fuels presents a compelling economic advantage, diversifying revenue streams and improving the overall profitability of CTL projects. The development of advanced catalytic processes and gasification technologies promises to enhance conversion efficiency and reduce operational costs, making CTL more competitive. Additionally, the increasing focus on regional energy independence, particularly in coal-rich nations seeking to minimize reliance on imported fuels, creates a strong impetus for new CTL projects, supported by government initiatives and strategic investments.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Carbon Capture and Storage (CCS) | +1.0% | North America, Europe, Asia Pacific | Long-term (5+ years) |

| Co-production of High-Value Chemicals | +0.9% | Global, particularly industrial hubs | Mid-term (3-5 years) |

| Advancements in Catalytic Processes and Gasification | +0.8% | Developed economies, research-intensive regions | Long-term (5+ years) |

| Government Support for Strategic Energy Assets | +0.7% | China, India, South Africa, USA | Mid-term (3-5 years) |

| Modular and Smaller-Scale CTL Plant Development | +0.6% | Niche applications, remote areas, specialized industries | Short to Mid-term (1-5 years) |

Coal to Liquid Fuel Market Challenges Impact Analysis

The Coal to Liquid (CTL) fuel market confronts several substantial challenges that could impede its growth and widespread adoption. Foremost among these are the stringent environmental regulations and mounting pressure from climate change mitigation efforts, which often target coal-intensive industries due to their high carbon emissions. This regulatory scrutiny can lead to increased compliance costs, project delays, or even cancellations. Furthermore, securing substantial long-term financing remains a critical hurdle, as the immense capital requirements for CTL projects often face skepticism from investors concerned about environmental risks, volatile energy prices, and the long payback periods. Public perception and social license to operate also pose a significant challenge, with strong opposition from environmental groups and local communities often impacting project feasibility. The inherent complexity and scale of CTL technologies also translate into considerable operational risks and the need for highly specialized technical expertise, further complicating project execution and cost management.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations | -1.0% | Europe, North America, select APAC countries | Mid to Long-term (3-8 years) |

| High Capital Intensity and Financing Difficulties | -0.9% | Global, particularly in capital-constrained regions | Long-term (5+ years) |

| Negative Public Perception and Social License Issues | -0.8% | Global, especially in regions with strong environmental activism | Mid-term (3-5 years) |

| Fluctuations in Coal and Crude Oil Prices | -0.7% | Global, impacting economic viability | Short to Mid-term (1-5 years) |

| Technological Complexities and Operational Risks | -0.6% | Global, particularly new market entrants | Mid-term (3-5 years) |

Coal to Liquid Fuel Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Coal to Liquid Fuel market, offering critical insights into its current dynamics, historical performance, and future growth projections. The scope encompasses detailed market segmentation, competitive landscape assessment, and regional market analysis, tailored to empower stakeholders with actionable intelligence for strategic decision-making. The report highlights key market trends, influential drivers, significant restraints, emerging opportunities, and prevailing challenges that shape the industry landscape, providing a holistic view for navigating the complexities of the global energy sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.5 Billion |

| Market Forecast in 2033 | USD 4.24 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Energy Solutions, Synfuels Corporation, CoalChem Dynamics, LiquiFuels Inc., PetroCoal Holdings, Carbon Conversion Technologies, Energy Transition Fuels, Integrated Fuels Systems, Advanced Coal Processing, Green Synfuels, TerraHydrocarbons, Power Liquids Group, Future Fuel Innovations, CoalGasification Systems, Prime Carbon Solutions, Phoenix Fuels Ltd., Delta Energy Corp., United Coal Synthetics, NextGen Fuels, Evergreen Synfuels |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Coal to Liquid Fuel market is meticulously segmented to provide a granular understanding of its diverse components and their respective contributions to market growth. This comprehensive segmentation allows for a precise analysis of technological adoption patterns, product demand across various applications, and the strategic positioning of market players. Each segment and subsegment is analyzed to highlight specific market dynamics, growth drivers, and potential opportunities within the broader CTL landscape. This detailed breakdown offers stakeholders the ability to identify high-growth areas and tailor their strategies to specific market niches, ensuring a targeted and effective approach to market penetration and expansion.

- By Technology: This segment delves into the various conversion processes employed to transform coal into liquid fuels.

- Fischer-Tropsch (FT) Synthesis: An indirect liquefaction process widely adopted for its flexibility in producing various fuels and chemicals.

- Methanol to Gasoline (MTG): A process that first converts coal to methanol, then to high-octane gasoline.

- Direct Coal Liquefaction (DCL): Converts coal directly into liquid fuels under high pressure and temperature with catalysts.

- Indirect Coal Liquefaction (ICL): A two-step process involving coal gasification followed by synthesis of liquid fuels.

- By Product Type: This segmentation categorizes the market based on the specific types of liquid fuels and valuable co-products generated from CTL processes.

- Diesel: High-quality diesel fuel suitable for transportation and industrial use.

- Gasoline: Refined motor gasoline for light-duty vehicles.

- Jet Fuel: Aviation turbine fuel meeting stringent specifications for aircraft.

- Naphtha: A versatile petrochemical feedstock used in various chemical processes.

- Lubricants: High-performance lubricants derived from synthetic processes.

- Chemical Feedstock: Intermediate chemicals used as raw materials in the chemical industry.

- By Application: This segment examines the end-use industries and sectors where CTL products find their primary utility.

- Transportation Fuel: Primary application for powering vehicles, aircraft, and maritime vessels.

- Chemical Industry Feedstock: Utilization of CTL-derived naphtha and other chemicals for plastics, fertilizers, and other industrial products.

- Power Generation Blending: Blending of CTL fuels with conventional fuels for enhanced energy efficiency or reduced emissions in power plants.

- Industrial Solvents: Use of specific CTL fractions as solvents in various industrial processes.

Regional Highlights

The global Coal to Liquid Fuel market exhibits distinct regional dynamics, influenced by local coal reserves, energy policies, economic development, and environmental regulations. Asia Pacific stands out as a dominant and rapidly growing region due to its vast coal resources and surging energy demand, particularly in countries like China and India, where energy security is a top national priority. These nations are heavily investing in CTL projects to reduce reliance on oil imports and leverage indigenous coal. North America, while possessing significant coal reserves, faces stricter environmental regulations and a mature oil and gas industry, leading to a more cautious and selective approach to CTL development, often focusing on integration with carbon capture technologies. Europe, with its strong environmental mandates, has a more limited CTL presence, generally concentrating on research and development for cleaner conversion technologies or niche applications. The Middle East and Africa, rich in natural resources, are also exploring CTL as part of broader energy diversification strategies, especially in countries with abundant coal and a drive for industrialization. Latin America shows nascent interest, mainly driven by countries aiming to capitalize on their coal deposits for domestic fuel supply.

- Asia Pacific: Emerging as the largest and fastest-growing market due to significant coal reserves in China and India, coupled with high energy demand and strategic focus on energy independence. Governmental support and large-scale projects are key drivers.

- North America: Driven by energy security objectives and technological innovation, with emphasis on integrating advanced environmental controls like Carbon Capture and Storage (CCS). The United States is a key player due to its substantial coal resources.

- Europe: Characterized by stringent environmental regulations, leading to limited large-scale CTL production but active research into cleaner, more efficient conversion processes and co-production of chemicals.

- Middle East and Africa: Growing interest in CTL for energy diversification and industrial development, particularly in South Africa, which has a long history and substantial investment in coal liquefaction technologies.

- Latin America: Nascent market exploring CTL potential in countries with significant coal deposits, aiming to enhance domestic fuel supply and reduce import dependency.

Top Key Players:

The market research report covers the analysis of key stake holders of the Coal to Liquid Fuel Market. Some of the leading players profiled in the report include -- Global Energy Solutions

- Synfuels Corporation

- CoalChem Dynamics

- LiquiFuels Inc.

- PetroCoal Holdings

- Carbon Conversion Technologies

- Energy Transition Fuels

- Integrated Fuels Systems

- Advanced Coal Processing

- Green Synfuels

- TerraHydrocarbons

- Power Liquids Group

- Future Fuel Innovations

- CoalGasification Systems

- Prime Carbon Solutions

- Phoenix Fuels Ltd.

- Delta Energy Corp.

- United Coal Synthetics

- NextGen Fuels

- Evergreen Synfuels

Frequently Asked Questions:

What is Coal to Liquid (CTL) Fuel?

The Coal to Liquid (CTL) fuel process converts solid coal into liquid hydrocarbons, such as gasoline, diesel, and jet fuel. This is typically achieved through either direct liquefaction, where coal is converted directly, or indirect liquefaction (e.g., Fischer-Tropsch synthesis), where coal is first gasified into syngas and then synthesized into liquid fuels. CTL technology aims to diversify energy sources and leverage abundant coal reserves.What are the primary drivers for the Coal to Liquid Fuel market growth?

The primary drivers for the Coal to Liquid Fuel market growth include increasing global energy security concerns, the vast availability of coal reserves worldwide, and the volatility in global crude oil prices. Technological advancements in CTL processes enhancing efficiency and environmental performance also significantly contribute to its market expansion.What are the environmental implications of Coal to Liquid Fuel technology?

Historically, CTL technology has been associated with high greenhouse gas emissions and significant water consumption. However, newer developments focus on integrating Carbon Capture and Storage (CCS) technologies and improving water efficiency to mitigate these environmental impacts. Regulatory pressures are also driving the industry towards more sustainable practices.How does AI influence the Coal to Liquid Fuel industry?

Artificial intelligence (AI) influences the CTL industry by optimizing operational efficiency through predictive maintenance, improving process control for higher yields and fuel quality, and accelerating research and development for new catalysts and advanced conversion technologies. AI also enhances supply chain management and contributes to better safety and environmental monitoring.What are the key technological advancements in Coal to Liquid Fuel production?

Key technological advancements in CTL production include the integration of Carbon Capture and Storage (CCS) systems to reduce emissions, the development of more efficient and selective catalysts, advancements in gasification technologies, and the rise of modular and smaller-scale CTL plants. There's also a growing focus on co-producing high-value chemicals alongside fuels to improve economic viability.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted