Bioplastic Utensil Market

Bioplastic Utensil Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701287 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

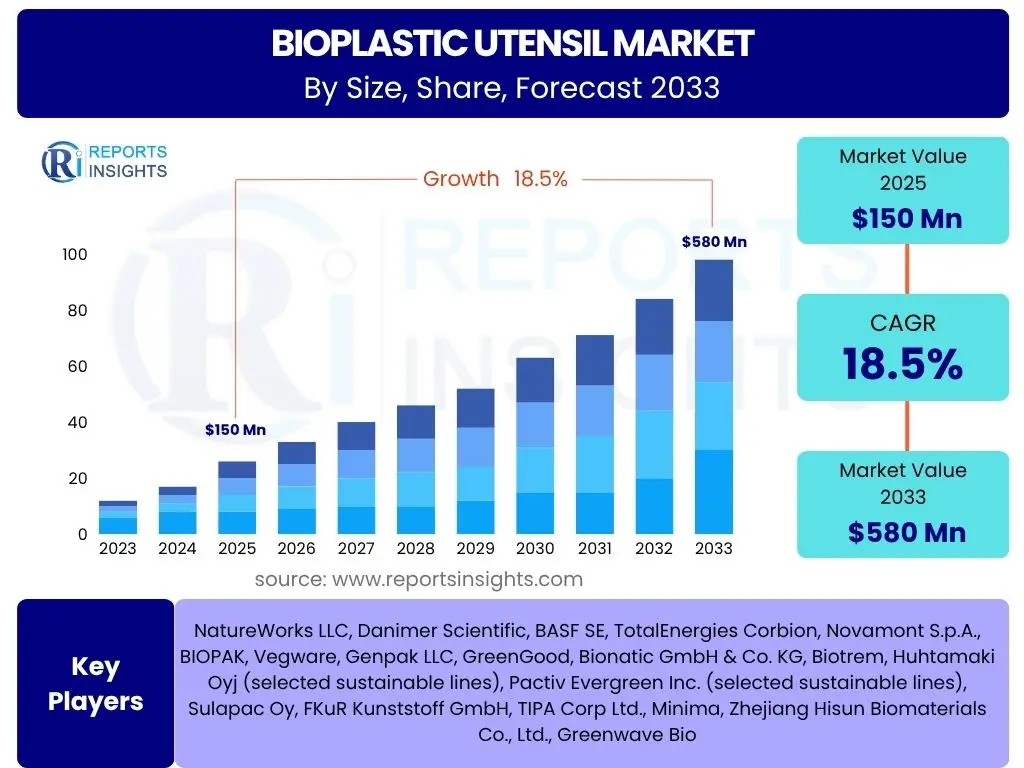

Bioplastic Utensil Market Size

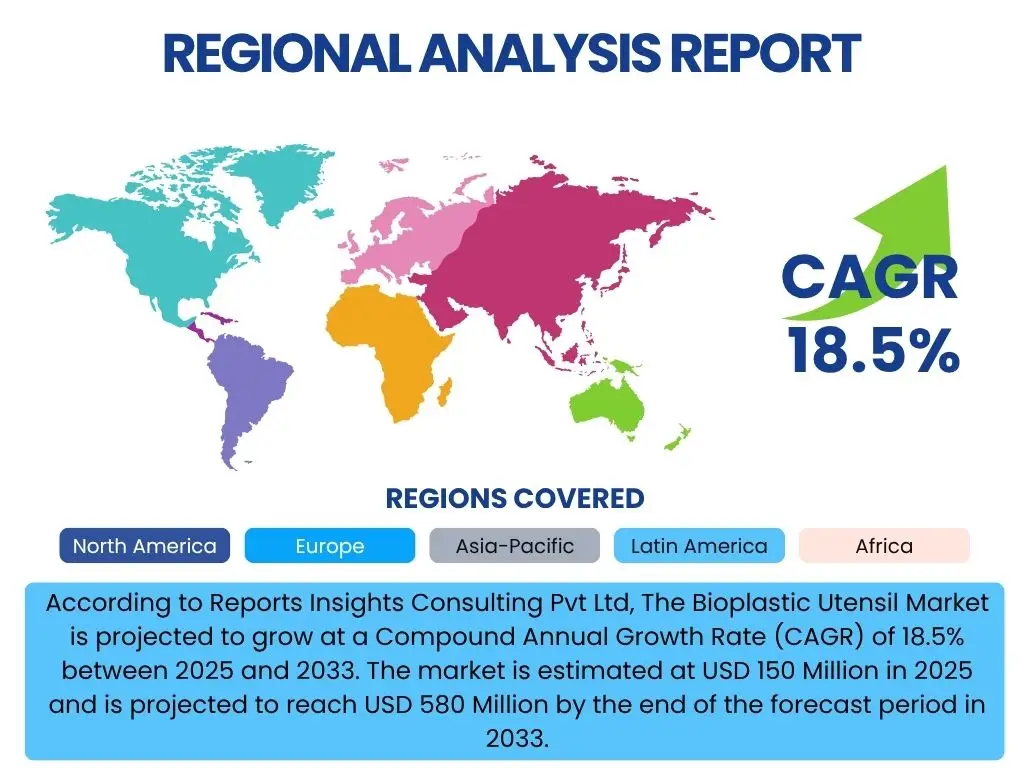

According to Reports Insights Consulting Pvt Ltd, The Bioplastic Utensil Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 150 Million in 2025 and is projected to reach USD 580 Million by the end of the forecast period in 2033.

Key Bioplastic Utensil Market Trends & Insights

The bioplastic utensil market is currently undergoing a transformative phase, driven by an accelerating global push towards sustainability and significant shifts in consumer preferences. Key trends indicate a robust expansion, moving beyond niche markets to mainstream adoption in various sectors. The focus on reducing plastic waste, coupled with advancements in material science, is reshaping the competitive landscape and fostering innovation. This paradigm shift is not merely reactive to regulatory pressures but also proactive, with companies and consumers increasingly prioritizing environmentally responsible products.

Major insights reveal that while initial market penetration was slow due to cost and performance concerns, continuous research and development are addressing these challenges, leading to improved product viability. Furthermore, the increasing awareness regarding the detrimental effects of conventional plastic pollution has created a fertile ground for bioplastic alternatives. The market is witnessing a diversification in material types, moving beyond traditional PLA to include advanced compostable and bio-based polymers, catering to a wider range of applications and disposal methods. This evolution signifies a maturing market poised for significant growth.

- Increasing global regulatory bans on single-use conventional plastics.

- Growing consumer awareness and demand for eco-friendly and compostable products.

- Significant advancements in bioplastic material properties, improving durability and heat resistance.

- Expansion of composting infrastructure in developed regions facilitating end-of-life solutions.

- Rising adoption of bioplastic utensils in the food service, hospitality, and catering sectors.

- Emergence of circular economy principles driving innovation in bio-based feedstock sourcing and end-of-life recycling.

- Collaborations between bioplastic manufacturers and large-scale food service providers to scale adoption.

AI Impact Analysis on Bioplastic Utensil

Artificial Intelligence (AI) is set to play a pivotal role in the evolution of the bioplastic utensil market, offering transformative capabilities across its entire value chain. Users frequently inquire about how AI can optimize production, enhance sustainability, and drive innovation in bioplastic materials. AI's analytical prowess allows for sophisticated data processing, leading to more efficient raw material sourcing, predictive maintenance in manufacturing, and optimized supply chain logistics. This technological integration is expected to reduce operational costs and improve product quality, thereby accelerating the market's growth and competitiveness.

Furthermore, AI's influence extends to research and development, where it can rapidly analyze molecular structures to discover novel biopolymer formulations with enhanced properties, such as improved heat resistance or faster biodegradability. In the context of waste management, AI-powered sorting systems can significantly improve the efficiency of bioplastic recycling and composting processes, ensuring that these materials truly fulfill their environmental promise. This comprehensive impact positions AI as a crucial enabler for the bioplastic utensil market to overcome existing challenges and achieve its full potential for sustainable growth.

- AI-driven optimization of bioplastic production processes, reducing waste and energy consumption.

- Predictive analytics for raw material sourcing, ensuring supply chain stability and efficiency.

- Accelerated discovery and development of new biopolymer formulations through AI-powered material science.

- Enhanced quality control and defect detection in manufacturing using AI-vision systems.

- Optimization of supply chain logistics and inventory management for bioplastic products.

- Improved efficiency of waste sorting and recycling facilities for bioplastics through AI-enabled recognition.

- Personalized product development and market forecasting based on AI analysis of consumer preferences.

Key Takeaways Bioplastic Utensil Market Size & Forecast

The bioplastic utensil market is poised for significant expansion, demonstrating a robust growth trajectory driven by a confluence of environmental imperatives, evolving consumer behaviors, and proactive regulatory frameworks. Key takeaways from the market size and forecast analysis underscore the increasing mainstream acceptance of bioplastic utensils as a viable and preferred alternative to conventional plastics. This growth is not merely incremental but represents a fundamental shift in the sustainable consumption landscape, indicating a strong commitment from both industry players and end-users towards eco-friendly solutions.

Insights reveal that the market's upward trend is further bolstered by continuous innovation in material science, leading to bioplastic utensils with improved performance characteristics and reduced cost disparities compared to their petroleum-based counterparts. The forecast clearly indicates that investments in R&D, coupled with the expansion of waste management infrastructure, will be critical in sustaining this momentum. Stakeholders are recognizing the long-term value in transitioning to bio-based solutions, positioning the bioplastic utensil market as a dynamic and increasingly indispensable component of the global sustainability agenda.

- The market is set for high double-digit CAGR, indicating strong growth potential.

- Regulatory bans on single-use plastics are a primary catalyst for market acceleration.

- Increasing consumer environmental awareness drives demand for sustainable alternatives.

- Technological advancements in bioplastic materials are enhancing product performance and reducing costs.

- The food service and hospitality sectors are key adopters, contributing significantly to market volume.

- Investments in composting and recycling infrastructure are crucial for market expansion and public acceptance.

Bioplastic Utensil Market Drivers Analysis

The imperative to address global plastic pollution stands as a paramount driver for the bioplastic utensil market. Escalating concerns over the environmental impact of conventional single-use plastics, particularly their persistence in landfills and oceans, have spurred a worldwide movement towards sustainable alternatives. Governments and international bodies are enacting stringent regulations and outright bans on various plastic products, including cutlery, compelling industries to transition towards bio-based and biodegradable options. This regulatory push creates a direct and significant demand for bioplastic utensils, positioning them as a compliant and responsible choice for businesses and consumers alike.

Complementing regulatory pressures, a profound shift in consumer preferences is accelerating market growth. Consumers are increasingly environmentally conscious, actively seeking out and willing to pay a premium for products that align with their sustainability values. This demand is particularly strong in the food service sector, where consumers expect eco-friendly options. Furthermore, corporate sustainability initiatives play a crucial role; many large corporations are setting ambitious environmental, social, and governance (ESG) goals, including targets for reducing their plastic footprint. Adopting bioplastic utensils is a tangible way for these companies to demonstrate their commitment to sustainability, enhance brand reputation, and meet shareholder expectations, thereby driving widespread adoption.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Plastic Pollution Crisis and Bans | +5.0-7.0% | Europe, North America, India, China, ASEAN, Latin America | Short- to Long-term (2025-2033) |

| Increasing Consumer Environmental Awareness | +4.0-5.5% | North America, Europe, Developed APAC (Japan, Australia) | Medium- to Long-term (2027-2033) |

| Corporate Sustainability Initiatives and ESG Goals | +3.5-4.5% | Global, particularly multinational corporations | Medium-term (2026-2030) |

| Advancements in Biopolymer Technology | +2.5-3.5% | Global, R&D Hubs (USA, Germany, Japan, China) | Long-term (2028-2033) |

Bioplastic Utensil Market Restraints Analysis

Despite the strong growth drivers, the bioplastic utensil market faces significant restraints that could impede its full potential. One of the primary barriers is the higher production cost associated with bioplastics compared to conventional petroleum-based plastics. The sourcing of bio-based feedstocks, complex manufacturing processes, and smaller economies of scale contribute to a higher unit cost, making bioplastic utensils less competitive on price for many businesses, especially those operating on tight margins. This cost disparity remains a critical challenge, particularly in price-sensitive markets where immediate economic viability often takes precedence over long-term environmental benefits.

Another substantial restraint is the limited and inconsistent infrastructure for composting and industrial biodegradation. While many bioplastic utensils are marketed as compostable or biodegradable, their proper disposal often requires specific industrial composting facilities that are not widely available globally. This lack of adequate end-of-life infrastructure leads to bioplastic utensils frequently ending up in landfills, where they behave much like conventional plastics due to the absence of the necessary conditions for degradation. This issue not only undermines the environmental promise of bioplastics but also contributes to consumer confusion and skepticism, hindering broader adoption and market confidence. Additionally, some bioplastic types may exhibit performance limitations, such as lower heat resistance or durability compared to their plastic counterparts, which can restrict their application in certain scenarios and negatively impact user experience.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher Production Costs than Conventional Plastics | -3.0-4.5% | Global, particularly price-sensitive emerging markets | Short- to Medium-term (2025-2029) |

| Limited Composting Infrastructure | -2.5-3.5% | Global, especially developing regions | Medium- to Long-term (2026-2033) |

| Performance Limitations (e.g., Heat Resistance) | -1.5-2.0% | Global, specific high-temperature applications | Short-term (2025-2027) |

| Consumer Confusion and "Greenwashing" Concerns | -1.0-1.5% | Global | Short- to Medium-term (2025-2029) |

Bioplastic Utensil Market Opportunities Analysis

The bioplastic utensil market presents significant opportunities for growth, particularly in untapped emerging markets where environmental awareness is rapidly increasing and regulatory frameworks are beginning to solidify. Regions in Asia Pacific, Latin America, and Africa are experiencing substantial economic development and a growing middle class, leading to increased consumption in the food service sector. As these regions grapple with escalating plastic waste challenges, they are increasingly open to adopting sustainable alternatives. Early movers in these markets can establish strong footholds, benefiting from less saturated competitive landscapes and a burgeoning demand for eco-friendly solutions.

Technological breakthroughs in biopolymer science offer another compelling opportunity. Continuous research and development are leading to the creation of novel bioplastic formulations with enhanced properties, such as improved durability, heat resistance, and faster, more reliable biodegradability. These innovations address previous performance limitations, making bioplastic utensils suitable for a wider range of applications and environments, including demanding industrial or commercial settings. Furthermore, strategic partnerships between bioplastic manufacturers, large food service chains, and waste management companies can create integrated solutions, from production to proper disposal, thereby streamlining the adoption process and enhancing market scalability. The development of certified home-compostable solutions could also unlock a significant portion of the household market, broadening consumer access and reducing reliance on industrial infrastructure.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Markets | +4.0-5.5% | Asia Pacific, Latin America, Middle East & Africa | Medium- to Long-term (2027-2033) |

| Technological Breakthroughs in Biopolymer Properties | +3.5-4.5% | Global R&D centers (USA, Europe, Japan, China) | Long-term (2028-2033) |

| Strategic Partnerships with Food Service Giants | +3.0-4.0% | Global, major food service chains and retailers | Medium-term (2026-2030) |

| Development of Home-Compostable Solutions | +2.0-3.0% | North America, Europe, Australia | Medium- to Long-term (2027-2033) |

Bioplastic Utensil Market Challenges Impact Analysis

The bioplastic utensil market faces several critical challenges that require strategic intervention to sustain its growth trajectory. One significant challenge is ensuring the sustainable sourcing of bio-based feedstocks. As demand for bioplastics escalates, concerns about land use, competition with food crops, and the environmental impact of agricultural practices (e.g., deforestation, excessive water use, pesticide application) become more pronounced. Ensuring that bioplastic production does not merely shift environmental burdens from one area to another is paramount for maintaining the industry's green credibility and long-term viability.

Another major hurdle is the inconsistent regulatory frameworks and varying definitions of "biodegradable" and "compostable" across different regions and countries. This lack of standardization creates confusion for both manufacturers and consumers, complicates international trade, and can undermine public trust in bioplastic claims. Furthermore, the market faces intense competition from other sustainable alternatives, such as reusable cutlery and non-plastic biodegradable materials like bamboo or wood. Educating consumers on proper disposal methods for different types of bioplastics, particularly distinguishing between industrial compostable and home compostable products, remains a persistent challenge that, if unaddressed, can lead to improper disposal and a failure to realize the environmental benefits of these products. Finally, scaling production efficiently while maintaining competitive pricing against entrenched conventional plastic manufacturers poses an ongoing operational and economic challenge.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Sustainable Sourcing of Feedstocks | -2.0-3.0% | Global | Long-term (2028-2033) |

| Inconsistent Regulatory Frameworks | -1.5-2.5% | Global, particularly cross-border trade | Medium- to Long-term (2027-2033) |

| Competition from Other Sustainable Alternatives | -1.0-2.0% | Global | Medium-term (2026-2030) |

| Consumer Education on Disposal | -0.5-1.0% | Global | Short- to Medium-term (2025-2029) |

Bioplastic Utensil Market - Updated Report Scope

This market research report offers a comprehensive analysis of the Bioplastic Utensil Market, detailing its current size, historical performance, and future growth projections from 2025 to 2033. It provides in-depth insights into market dynamics, including key drivers, restraints, opportunities, and challenges, along with a thorough segmentation analysis across material types, product types, applications, and end-uses. The report also highlights regional market trends and profiles leading companies, offering a strategic outlook for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 150 Million |

| Market Forecast in 2033 | USD 580 Million |

| Growth Rate | 18.5% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | NatureWorks LLC, Danimer Scientific, BASF SE, TotalEnergies Corbion, Novamont S.p.A., BIOPAK, Vegware, Genpak LLC, GreenGood, Bionatic GmbH & Co. KG, Biotrem, Huhtamaki Oyj (selected sustainable lines), Pactiv Evergreen Inc. (selected sustainable lines), Sulapac Oy, FKuR Kunststoff GmbH, TIPA Corp Ltd., Minima, Zhejiang Hisun Biomaterials Co., Ltd., Greenwave Bio |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The bioplastic utensil market is meticulously segmented to provide a granular understanding of its diverse components and growth opportunities. This segmentation allows for precise analysis of consumer preferences, technological advancements across different material types, and varying adoption rates across various end-use sectors. By categorizing the market based on material, product type, application, and end-use, stakeholders can identify specific niches, tailor product development, and formulate targeted market entry strategies. This comprehensive breakdown illuminates the complex interplay of factors driving demand and supply within the bioplastic utensil ecosystem.

Understanding each segment's unique characteristics, including market size, growth rate, and key influencing factors, is crucial for both new entrants and established players. For instance, the dominance of Polylactic Acid (PLA) in certain applications due to its cost-effectiveness, versus the emergence of Polyhydroxyalkanoates (PHA) for their superior biodegradability, reflects the evolving material landscape. Similarly, analyzing demand patterns from quick-service restaurants versus institutional catering provides critical insights into the varying needs and priorities of different application segments, enabling more effective market penetration and product positioning. This detailed segmentation analysis is fundamental for strategic decision-making and for capitalizing on the market's burgeoning potential.

- By Material:

- Polylactic Acid (PLA)

- Crystallized Polylactic Acid (CPLA)

- Polyhydroxyalkanoates (PHA)

- Starch Blends

- Cellulose Acetate

- Polybutylene Succinate (PBS)

- Others (e.g., Bamboo, Wood)

- By Product Type:

- Forks

- Spoons

- Knives

- Sporks

- Chopsticks

- Stirrers

- Other Specialty Utensils

- By Application:

- Food Service

- Restaurants

- Cafes

- Quick Service Restaurants (QSRs)

- Hotels

- Catering Services

- Airlines & Travel

- Institutional

- Schools

- Hospitals

- Corporate Canteens

- Household

- Retail Sales

- Events & Festivals

- Food Service

- By End-Use:

- Restaurants

- Cafes

- QSRs

- Hotels

- Catering

- Airlines

- Schools

- Hospitals

- Households

- Events

Regional Highlights

- North America: This region demonstrates a strong commitment to reducing plastic waste, driven by increasing consumer environmental awareness and state-level bans on single-use plastics. The market is characterized by a growing number of corporate sustainability initiatives and a relatively developed infrastructure for composting, particularly in urban areas. High disposable incomes also support consumer willingness to pay a premium for eco-friendly alternatives.

- Europe: Leading the global charge in sustainability, Europe has implemented stringent regulations such as the EU Single-Use Plastics Directive, which has significantly accelerated the adoption of bioplastic utensils. The region benefits from a robust circular economy framework, advanced waste management infrastructure, and high consumer demand for certified compostable products. Countries like Germany, France, and the UK are at the forefront of this transition.

- Asia Pacific (APAC): The APAC region is poised for substantial growth due to rapid urbanization, increasing awareness of environmental issues, and emerging regulatory frameworks in key countries like China, India, and ASEAN nations. While infrastructural challenges persist, the region's large population and burgeoning food service sector present immense opportunities. APAC is also a major hub for bioplastics manufacturing, driving innovation and cost reduction.

- Latin America: This region is an emerging market with growing environmental concerns and nascent legislative efforts to curb plastic pollution. While the adoption rate of bioplastic utensils is currently lower compared to North America and Europe, the increasing focus on sustainable tourism and a rising middle class are creating fertile ground for market expansion. Investments in waste management infrastructure will be crucial for accelerating growth.

- Middle East and Africa (MEA): The MEA region is at an early stage of bioplastic utensil adoption, though awareness is increasing, particularly in urban centers and among younger demographics. Governments in some Gulf Cooperation Council (GCC) countries are exploring sustainability initiatives, and the tourism sector is showing interest in eco-friendly alternatives. Economic diversification and a growing emphasis on environmental protection are expected to drive future growth in this region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Bioplastic Utensil Market.- NatureWorks LLC

- Danimer Scientific

- BASF SE

- TotalEnergies Corbion

- Novamont S.p.A.

- BIOPAK

- Vegware

- Genpak LLC

- GreenGood

- Bionatic GmbH & Co. KG

- Biotrem

- Huhtamaki Oyj (selected sustainable lines)

- Pactiv Evergreen Inc. (selected sustainable lines)

- Sulapac Oy

- FKuR Kunststoff GmbH

- TIPA Corp Ltd.

- Minima

- Zhejiang Hisun Biomaterials Co., Ltd.

- Greenwave Bio

Frequently Asked Questions

What is the current market size and projected growth of bioplastic utensils?

The Bioplastic Utensil Market is estimated at USD 150 Million in 2025 and is projected to reach USD 580 Million by 2033, demonstrating a significant Compound Annual Growth Rate (CAGR) of 18.5% during the forecast period. This rapid expansion is driven by increasing environmental concerns and global regulatory shifts.

What are the primary drivers for the bioplastic utensil market?

Key drivers include the escalating global plastic pollution crisis, stringent government regulations and bans on single-use plastics, rising consumer demand for eco-friendly products, and corporate sustainability initiatives aimed at reducing environmental footprint. Advancements in biopolymer technology also contribute significantly to market growth.

What are the main types of bioplastics used in utensils?

The primary types of bioplastics used in utensil manufacturing include Polylactic Acid (PLA), Crystallized Polylactic Acid (CPLA), Polyhydroxyalkanoates (PHA), Starch Blends, Cellulose Acetate, and Polybutylene Succinate (PBS). Each material offers distinct properties regarding biodegradability, heat resistance, and application suitability.

Are bioplastic utensils truly biodegradable or compostable?

Many bioplastic utensils are designed to be biodegradable or compostable, particularly those made from PLA, CPLA, or PHA. However, their degradation often requires specific conditions found in industrial composting facilities. While some newer formulations are home-compostable, proper disposal relies heavily on the availability and accessibility of appropriate waste management infrastructure to ensure their environmental benefits are realized.

How do government regulations impact the bioplastic utensil market?

Government regulations, especially bans on single-use conventional plastics and directives promoting sustainable alternatives, are a major catalyst for the bioplastic utensil market. These policies directly mandate the shift towards eco-friendly options, creating substantial demand and fostering innovation. Regulatory support, however, needs to be consistent and clear across regions to avoid market fragmentation and ensure proper disposal practices.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted