Bioplastic and Biopolymer Market

Bioplastic and Biopolymer Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705762 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

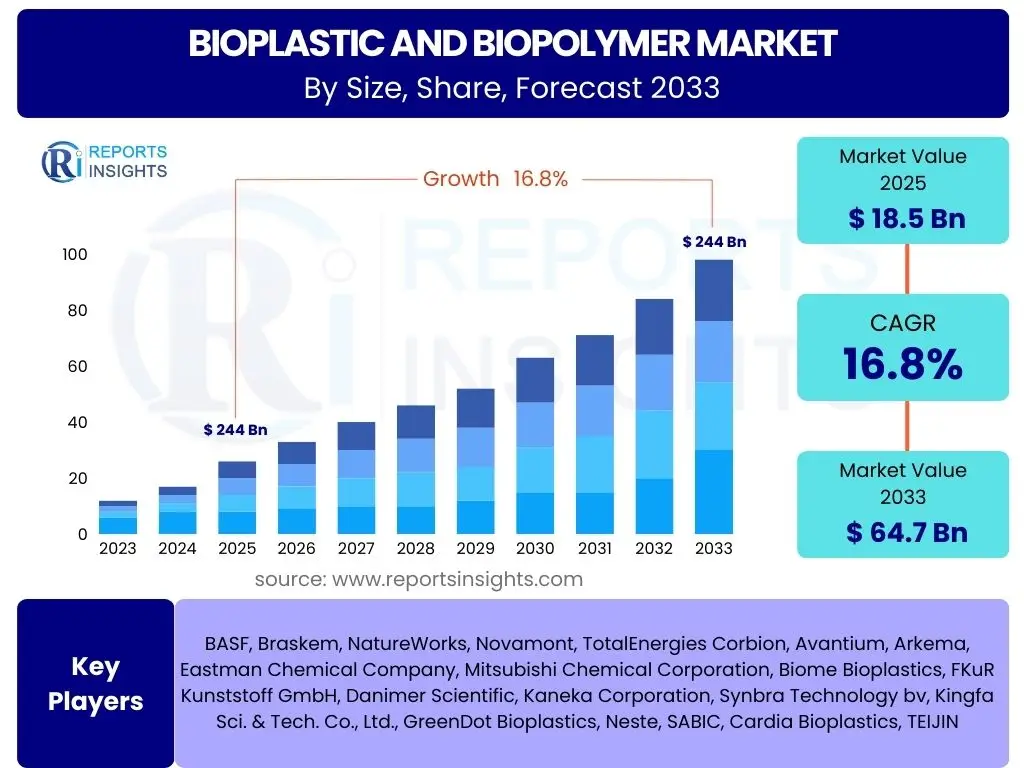

Bioplastic and Biopolymer Market Size

According to Reports Insights Consulting Pvt Ltd, The Bioplastic and Biopolymer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 16.8% between 2025 and 2033. The market is estimated at USD 18.5 Billion in 2025 and is projected to reach USD 64.7 Billion by the end of the forecast period in 2033.

Key Bioplastic and Biopolymer Market Trends & Insights

User inquiries frequently center on the evolving landscape of sustainable materials, particularly within the packaging and consumer goods sectors. A significant trend involves the escalating demand for environmentally benign alternatives to conventional plastics, driven by increasing environmental awareness and stringent regulatory frameworks globally. This demand is further amplified by corporate sustainability commitments and consumer preferences for eco-friendly products. Innovations in material science are continuously expanding the functional properties of bioplastics, making them suitable for a wider range of applications previously dominated by fossil-based polymers.

Another prominent insight revolves around the circular economy paradigm, where bioplastics are increasingly viewed as a crucial component for achieving closed-loop material cycles. This includes advancements in compostable and biodegradable plastics for single-use applications, alongside the development of bio-based 'drop-in' solutions that offer similar performance to traditional plastics but with a reduced carbon footprint. The market is also witnessing a trend towards diversifying feedstock sources, moving beyond first-generation crops to include agricultural waste, algae, and industrial by-products, enhancing the sustainability profile and reducing the potential for land-use competition. Furthermore, strategic collaborations across the value chain, from feedstock suppliers to end-product manufacturers, are becoming more common, fostering innovation and accelerating market adoption.

- Escalating demand for sustainable packaging and consumer goods.

- Increased regulatory pressure and corporate sustainability goals.

- Advancements in bio-based material properties and performance.

- Focus on circular economy principles, including enhanced biodegradability and recyclability.

- Diversification of renewable feedstock sources for production.

- Growing number of strategic partnerships and collaborations.

- Emergence of new application areas beyond traditional packaging.

AI Impact Analysis on Bioplastic and Biopolymer

Users frequently inquire about how artificial intelligence can accelerate the development, production, and sustainability of bioplastics and biopolymers. The primary themes emerging from these questions include the potential for AI to streamline research and development, optimize manufacturing processes, and improve the overall lifecycle management of these materials. There is a strong expectation that AI can drastically cut down the time and cost associated with discovering new bio-based materials and enhancing existing ones, moving beyond traditional trial-and-error methods to data-driven predictions.

Concerns often relate to the accessibility of AI technologies for smaller enterprises and the need for standardized data sets to feed AI models effectively. However, the overarching anticipation is that AI will play a transformative role in making bioplastics more competitive and widespread. This includes leveraging machine learning for predictive maintenance in production facilities, optimizing supply chain logistics for bio-based feedstocks, and developing smart sorting and recycling systems that can distinguish between various bioplastic types at end-of-life. AI is also seen as a tool to enhance the transparency of environmental impacts, allowing for more accurate lifecycle assessments and facilitating better decision-making throughout the bioplastic value chain.

- Accelerated material discovery and optimization through AI-driven simulations.

- Enhanced process efficiency and yield in bioplastic manufacturing using machine learning.

- Predictive analytics for feedstock supply chain management and logistics.

- Improved quality control and fault detection in production lines.

- Development of smart recycling and sorting technologies for complex bioplastic waste streams.

- More accurate environmental impact assessments and sustainability tracking.

- Personalized material design based on specific application requirements.

Key Takeaways Bioplastic and Biopolymer Market Size & Forecast

Common user questions regarding market takeaways often revolve around the most critical factors driving market expansion, the dominant segments, and the long-term viability of bioplastics. The core insight is the robust and sustained growth projected for the bioplastic and biopolymer market, driven primarily by an intensifying global focus on environmental sustainability and the urgent need to mitigate plastic pollution. This growth indicates a significant shift in industrial and consumer behavior towards more eco-friendly alternatives, establishing bioplastics not as niche products but as mainstream solutions. The forecast suggests substantial investment and innovation will continue to flow into this sector, propelling technological advancements and expanding application areas.

A key takeaway also includes the increasing differentiation within the bioplastics landscape, with distinct market trajectories for biodegradable/compostable materials versus durable bio-based plastics. While packaging remains the largest application segment, the diversification into automotive, consumer goods, and textiles signifies broader industrial acceptance and integration. Furthermore, the market's trajectory is heavily influenced by regulatory support and the establishment of dedicated infrastructure for collection, sorting, and processing of bioplastic waste. This highlights that market success is not solely dependent on material innovation but also on the development of a supportive ecosystem that ensures effective end-of-life management for these novel materials.

- Market poised for substantial and sustained growth through 2033.

- Environmental sustainability and regulatory mandates are primary growth catalysts.

- Packaging remains dominant, but diversification into new applications is accelerating.

- Significant investments in R&D and production capacity are expected.

- Demand for both biodegradable and durable bio-based plastics is strong.

- Development of robust end-of-life infrastructure is crucial for long-term success.

- Regional policies and consumer awareness play a pivotal role in market adoption.

Bioplastic and Biopolymer Market Drivers Analysis

The bioplastic and biopolymer market is experiencing significant growth propelled by several influential drivers. Foremost among these is the escalating global concern over environmental pollution, particularly the pervasive issue of plastic waste and its impact on ecosystems. Consumers, businesses, and governments are increasingly seeking sustainable alternatives to conventional fossil-based plastics, creating a strong market pull for bio-based and biodegradable materials. This collective awareness translates into a heightened demand for products with reduced carbon footprints and improved end-of-life options, making bioplastics an attractive solution for brands aiming to enhance their sustainability credentials and meet evolving consumer expectations.

Governmental regulations and policy initiatives worldwide are also acting as powerful catalysts for market expansion. Bans on single-use plastics, mandates for biodegradable packaging, and incentives for bio-based product development are compelling industries to transition towards bioplastics. These legislative actions create a predictable market environment and encourage investment in research, development, and scaling of bioplastic production capacities. Furthermore, the fluctuating prices of crude oil, which is the primary feedstock for conventional plastics, lend a degree of economic competitiveness to bioplastics, especially as their production technologies mature and scale, leading to improved cost-effectiveness and broader adoption across various industries.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Environmental Awareness and Consumer Demand | +5.0% | Global, particularly Europe, North America, APAC | Short to Long-term (2025-2033) |

| Stringent Government Regulations and Plastic Bans | +4.5% | Europe, Asia Pacific (China, India), North America | Short to Mid-term (2025-2029) |

| Brand Commitments to Sustainability and Circular Economy | +3.5% | Global, major consumer goods brands | Mid to Long-term (2027-2033) |

| Technological Advancements in Bioplastic Production | +2.5% | Global, key R&D hubs | Mid to Long-term (2027-2033) |

| Fluctuating Fossil Fuel Prices and Energy Security Concerns | +1.3% | Global | Short to Mid-term (2025-2029) |

Bioplastic and Biopolymer Market Restraints Analysis

Despite the strong growth potential, the bioplastic and biopolymer market faces several significant restraints that could impede its expansion. One of the primary limitations is the comparatively high production cost of bioplastics relative to conventional plastics. This cost disparity stems from factors such as smaller production scales, complex manufacturing processes, and the cost of specialized bio-based feedstocks. While economies of scale are improving, the initial capital investment required for new bioplastic production facilities remains substantial, often presenting a barrier to entry for new players and limiting rapid expansion for existing ones, especially in price-sensitive markets.

Another critical restraint is the performance limitation of certain bioplastic materials, particularly in terms of barrier properties, heat resistance, and long-term durability, which can restrict their applicability in highly demanding sectors like high-performance packaging or automotive components. While advancements are continuously being made, these material-specific challenges necessitate ongoing research and development to match or exceed the performance of traditional polymers across all applications. Furthermore, the limited infrastructure for the collection, sorting, and composting or recycling of bioplastics poses a significant hurdle. Without proper end-of-life management systems, the environmental benefits of bioplastics may not be fully realized, leading to confusion among consumers and waste management entities about appropriate disposal methods.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher Production Costs Compared to Conventional Plastics | -4.0% | Global | Short to Mid-term (2025-2030) |

| Performance Limitations (e.g., Barrier Properties, Durability) | -3.5% | Global, especially in demanding applications | Short to Mid-term (2025-2030) |

| Limited Recycling and Composting Infrastructure | -3.0% | Global, varies by region | Short to Mid-term (2025-2030) |

| Availability and Cost Volatility of Feedstock | -2.0% | Global | Short-term (2025-2027) |

| Consumer Confusion Regarding Disposal and Labeling | -1.5% | Global | Short to Mid-term (2025-2030) |

Bioplastic and Biopolymer Market Opportunities Analysis

Significant opportunities abound for the bioplastic and biopolymer market, driven by a confluence of technological advancements and evolving market demands. One of the most promising avenues lies in the expansion into new application areas that are currently dominated by conventional plastics. Sectors such as automotive interiors, electronic casings, medical devices, and textiles are increasingly exploring bioplastic alternatives, driven by sustainability targets and the potential for lighter, more environmentally friendly materials. The unique properties offered by certain biopolymers, such as biocompatibility and biodegradability, open doors for specialized applications in areas like drug delivery systems and surgical implants, presenting high-value market segments.

Further opportunities are emerging from continuous innovation in feedstock development and processing technologies. The shift towards non-food biomass, agricultural waste, and even CO2 as raw materials offers a sustainable and potentially cost-effective supply chain, reducing reliance on conventional agricultural crops. Advancements in polymerization techniques and blending technologies are enhancing material performance, addressing previous limitations and making bioplastics viable for a broader array of uses. Moreover, the development of advanced recycling technologies specifically designed for bio-based plastics, coupled with improved industrial composting infrastructure, represents a substantial opportunity to close the loop on material cycles and truly realize the circular economy potential of these materials, enhancing their appeal to environmentally conscious industries and consumers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into New Application Areas (Automotive, Electronics, Medical) | +4.0% | Global, particularly developed economies | Mid to Long-term (2028-2033) |

| Development of Advanced Bio-based Feedstocks | +3.5% | Global, regions with abundant biomass | Mid to Long-term (2028-2033) |

| Improvements in Bioplastic Processing Technologies | +3.0% | Global | Short to Mid-term (2025-2030) |

| Growing Investment in Recycling and Composting Infrastructure | +2.5% | Europe, North America, certain APAC countries | Mid to Long-term (2028-2033) |

| Strategic Collaborations and Partnerships Across Value Chain | +2.0% | Global | Short to Mid-term (2025-2030) |

Bioplastic and Biopolymer Market Challenges Impact Analysis

The bioplastic and biopolymer market faces several significant challenges that require concerted efforts from industry stakeholders, policymakers, and researchers. A primary hurdle is the challenge of scaling up production to meet the rapidly increasing demand. Current bioplastic production capacities are still relatively small compared to conventional plastics, leading to supply chain constraints and higher unit costs. Achieving true economies of scale requires substantial capital investment in new biorefineries and polymerization plants, which is a lengthy and complex process. This scaling challenge can hinder widespread adoption, especially for large-volume applications that require consistent and readily available material supplies.

Another key challenge is the lack of standardized definitions, labeling, and disposal guidelines for bioplastics across different regions. This creates confusion among consumers, manufacturers, and waste management operators regarding the proper end-of-life treatment for various bioplastic products. Without clear and harmonized standards, the effective collection, sorting, and processing of bioplastics for composting or recycling remain fragmented, undermining their environmental benefits and impeding the development of efficient circular systems. Furthermore, ensuring the economic viability of bioplastics, especially for small and medium-sized enterprises (SMEs), in comparison to well-established and cost-effective traditional plastics, presents an ongoing competitive challenge that necessitates continuous innovation in cost reduction and performance enhancement.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Scaling Up Production Capacity | -3.5% | Global | Short to Mid-term (2025-2030) |

| Lack of Standardized Definitions and Labeling | -3.0% | Global, especially regulatory bodies | Short to Mid-term (2025-2030) |

| Ensuring Economic Viability and Cost Competitiveness | -2.5% | Global | Short to Mid-term (2025-2030) |

| Consumer Education and Awareness Deficiencies | -2.0% | Global | Short to Mid-term (2025-2030) |

| Technical Limitations for Specific High-Performance Applications | -1.5% | Global | Mid to Long-term (2028-2033) |

Bioplastic and Biopolymer Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global bioplastic and biopolymer market, offering a detailed understanding of its current size, historical performance, and future growth projections. The report delves into key market trends, growth drivers, inherent restraints, emerging opportunities, and significant challenges that shape the industry landscape. It offers extensive segmentation analysis by product type, application, and regional dynamics, providing granular insights into market performance across various dimensions. Furthermore, the report includes a competitive analysis, profiling major industry players and assessing their strategic positions to offer a holistic view of the market's competitive environment and its future outlook.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 64.7 Billion |

| Growth Rate | 16.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | BASF, Braskem, NatureWorks, Novamont, TotalEnergies Corbion, Avantium, Arkema, Eastman Chemical Company, Mitsubishi Chemical Corporation, Biome Bioplastics, FKuR Kunststoff GmbH, Danimer Scientific, Kaneka Corporation, Synbra Technology bv, Kingfa Sci. & Tech. Co., Ltd., GreenDot Bioplastics, Neste, SABIC, Cardia Bioplastics, TEIJIN |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The bioplastic and biopolymer market is comprehensively segmented to provide granular insights into its diverse components and growth dynamics. This segmentation helps in understanding specific material trends, application-driven demand, and the implications of different end-of-life scenarios. The primary segmentation by type includes various bio-based polymers, each possessing unique properties and suited for different applications, ranging from compostable materials to durable bio-alternatives. This differentiation is crucial for identifying technological advancements and market preferences for specific polymer types.

Further analysis is conducted through application segmentation, which highlights the pervasive adoption of bioplastics across multiple industries, with packaging currently leading the demand. This segment also encompasses emerging areas such as automotive, textiles, and medical, showcasing the versatility and expanding utility of bioplastics beyond their traditional uses. Finally, segmentation by end-of-life options provides critical insights into the market's shift towards circular economy principles, distinguishing between biodegradable/compostable materials and durable bio-based plastics, thus informing strategies for waste management and infrastructure development within the evolving sustainable materials landscape.

- By Type:

- Polylactic Acid (PLA)

- Polyhydroxyalkanoates (PHA)

- Starch Blends

- Bio-Polyethylene (Bio-PE)

- Polybutylene Adipate Terephthalate (PBAT)

- Bio-Polyethylene Terephthalate (Bio-PET)

- Polybutylene Succinate (PBS)

- Cellulose Acetate

- Polyamides (PA)

- Other Bio-based Polymers

- By Application:

- Packaging

- Rigid Packaging

- Flexible Packaging

- Consumer Goods

- Electronics

- Appliances

- Toys

- Textiles

- Apparel

- Non-wovens

- Automotive

- Interior Components

- Under-the-hood applications

- Agriculture

- Mulch Films

- Seed Coatings

- Building & Construction

- Pipes

- Insulation

- Medical & Healthcare

- Implants

- Drug Delivery

- Others (Coatings, Adhesives, Fibers)

- Packaging

- By End-of-Life Option:

- Biodegradable/Compostable Bioplastics

- Durable/Non-biodegradable Bioplastics

Regional Highlights

- Europe: Europe is a pioneering region in the bioplastics market, driven by stringent environmental regulations, strong consumer awareness, and significant R&D investments. Countries like Germany, Italy, and France are leading the adoption of bioplastics, particularly in packaging and agriculture, supported by well-developed composting infrastructure and ambitious circular economy targets. The European Union's directives on single-use plastics and packaging waste heavily influence market growth, fostering innovation and industry collaboration.

- North America: North America presents a substantial and growing market for bioplastics, primarily fueled by increasing corporate sustainability initiatives and consumer demand for eco-friendly products. The United States is a key market, with rising interest from major brands in utilizing bioplastics for packaging and consumer goods. While regulatory drivers are less uniform than in Europe, state-level policies and voluntary industry commitments are propelling market expansion. Investments in advanced bioplastic technologies and feedstock development are also notable.

- Asia Pacific (APAC): The Asia Pacific region is rapidly emerging as a dominant force in the global bioplastics market, driven by robust economic growth, increasing industrialization, and growing environmental concerns, especially in populous countries like China, India, and Japan. Governments in this region are increasingly implementing policies to mitigate plastic pollution, stimulating demand for bioplastics in packaging, textiles, and agriculture. APAC is also a significant production hub, benefiting from favorable raw material availability and expanding manufacturing capacities.

- Latin America: The Latin American market for bioplastics is in its nascent stages but shows promising growth potential. Countries such as Brazil and Mexico are witnessing a gradual increase in awareness and adoption, particularly in the packaging sector. The abundance of biomass resources in the region provides a strong foundation for future bioplastic production, and increasing consumer environmental consciousness is expected to drive further market development, albeit at a slower pace compared to more mature markets.

- Middle East and Africa (MEA): The Middle East and Africa bioplastics market is currently smaller but is expected to grow as environmental awareness and sustainability efforts gain traction. Policies aimed at reducing plastic waste are beginning to emerge in some countries, particularly in the UAE and South Africa, which could catalyze demand. The region's reliance on fossil fuels for traditional plastic production presents both a challenge and an opportunity for diversification into bio-based alternatives, especially for countries looking to enhance their environmental profiles.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Bioplastic and Biopolymer Market.- BASF

- Braskem

- NatureWorks

- Novamont

- TotalEnergies Corbion

- Avantium

- Arkema

- Eastman Chemical Company

- Mitsubishi Chemical Corporation

- Biome Bioplastics

- FKuR Kunststoff GmbH

- Danimer Scientific

- Kaneka Corporation

- Synbra Technology bv

- Kingfa Sci. & Tech. Co., Ltd.

- GreenDot Bioplastics

- Neste

- SABIC

- Cardia Bioplastics

- TEIJIN

Frequently Asked Questions

What are bioplastics and biopolymers?

Bioplastics are a diverse family of materials that are either bio-based (derived from renewable biomass sources like corn starch, sugarcane, or cellulose) or biodegradable (capable of decomposing naturally in specific environments) or both. Biopolymers are a subset of bioplastics, referring specifically to polymers that are produced by living organisms or derived from biological sources.

Are all bioplastics biodegradable or compostable?

No, not all bioplastics are biodegradable or compostable. The term 'bioplastic' encompasses both bio-based plastics (which may or may not be biodegradable, e.g., Bio-PET) and biodegradable plastics (which may or may not be bio-based, e.g., PBAT). Only a subset of bioplastics is certified as compostable, meaning they can break down into natural elements in industrial composting facilities.

What are the main applications of bioplastics?

Bioplastics are primarily used in packaging, including rigid and flexible formats for food and beverages. Beyond packaging, their applications are rapidly expanding into consumer goods (electronics, toys), textiles, automotive components, agriculture (mulch films), and increasingly in medical and healthcare products like surgical sutures and implants.

What drives the growth of the bioplastic market?

The bioplastic market's growth is largely driven by increasing global environmental awareness, stringent government regulations on plastic waste, rising consumer demand for sustainable products, and corporate commitments to reduce their carbon footprint. Technological advancements that improve material performance and reduce production costs also contribute significantly.

What challenges does the bioplastic industry face?

Key challenges include higher production costs compared to conventional plastics, limitations in performance for certain demanding applications, and the lack of widespread and standardized infrastructure for collection, sorting, and composting/recycling. Consumer confusion regarding proper disposal and the need for scalable production capacities also present significant hurdles.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted