Stainless Steel Kitchen Utensil Market

Stainless Steel Kitchen Utensil Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702185 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Stainless Steel Kitchen Utensil Market Size

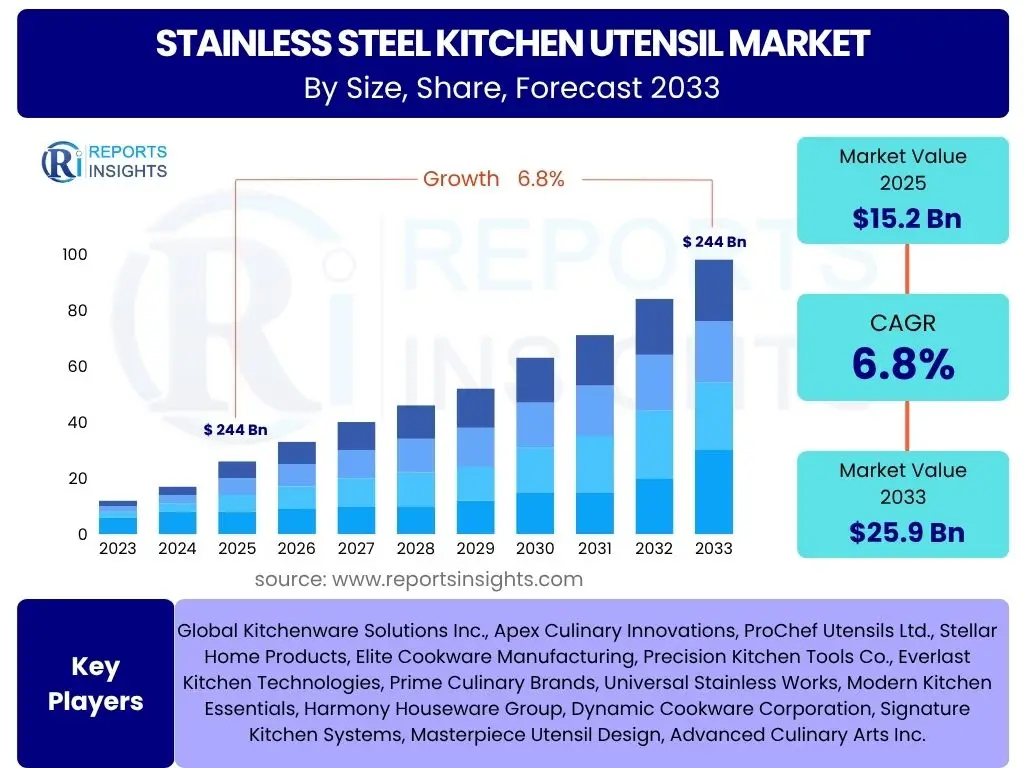

According to Reports Insights Consulting Pvt Ltd, The Stainless Steel Kitchen Utensil Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 15.2 Billion in 2025 and is projected to reach USD 25.9 Billion by the end of the forecast period in 2033.

Key Stainless Steel Kitchen Utensil Market Trends & Insights

The stainless steel kitchen utensil market is currently experiencing dynamic shifts driven by evolving consumer preferences, technological advancements, and a heightened focus on product longevity and aesthetics. Consumers are increasingly seeking not only functional but also visually appealing and durable kitchen tools, which stainless steel inherently offers. This trend is amplified by the widespread adoption of modern kitchen designs that prioritize sleek, metallic finishes, seamlessly integrating stainless steel utensils into the overall kitchen aesthetic. Furthermore, there is a growing awareness regarding the health and safety benefits associated with non-reactive and easy-to-clean materials, positioning stainless steel as a preferred choice over alternative materials that may pose concerns related to leaching or difficult maintenance.

Another significant trend reshaping the market is the burgeoning demand for specialized and ergonomically designed utensils. As culinary exploration gains popularity, consumers are investing in specific tools for various cooking techniques, ranging from baking to gourmet meal preparation. This demand fuels innovation in utensil design, focusing on improved grip, balanced weight, and enhanced functionality for specific tasks. The rise of e-commerce platforms has also democratized access to a wider array of international and niche stainless steel utensil brands, allowing consumers to discover products that align with their specific culinary needs and stylistic preferences, thereby accelerating market diversification and product availability.

Sustainability and ethical manufacturing practices are increasingly influencing purchasing decisions. While stainless steel is inherently durable and recyclable, consumers are beginning to inquire about the environmental footprint of production processes and the sourcing of raw materials. Brands that transparently communicate their commitment to sustainable practices, such as reducing waste, conserving energy, and ensuring ethical labor conditions, are gaining a competitive edge. This shift indicates a maturing market where consumer values extend beyond product utility to encompass the broader impact of their purchases, driving manufacturers to adopt more responsible production methods and supply chain management.

- Growing preference for durable and aesthetically pleasing kitchenware.

- Increased demand for specialized and ergonomically designed utensils.

- Expansion of online retail channels boosting product accessibility.

- Rising consumer awareness regarding hygiene and non-reactive materials.

- Emphasis on sustainable production and ethical sourcing practices.

AI Impact Analysis on Stainless Steel Kitchen Utensil

The integration of Artificial Intelligence (AI) within the manufacturing and distribution ecosystem of stainless steel kitchen utensils presents transformative potential, primarily by optimizing operational efficiencies and enhancing product development. In manufacturing, AI-powered systems can analyze vast datasets from production lines to predict machinery failures, optimize material usage, and ensure consistent product quality, minimizing defects and waste. This leads to higher precision in fabrication, improved consistency in finish, and reduced production costs, thereby making stainless steel utensils more competitive. Furthermore, AI can aid in supply chain management by forecasting demand with greater accuracy, optimizing inventory levels, and streamlining logistics, ensuring timely delivery and responsiveness to market fluctuations.

Beyond manufacturing, AI's influence extends to market research and consumer engagement. AI-driven analytics can process consumer feedback, purchasing patterns, and online trends to identify emerging preferences for specific utensil types, designs, or features. This data-driven insight empowers manufacturers to develop new products that are highly aligned with market demand, reducing the risk associated with product launches. For instance, AI could pinpoint a regional demand for a particular type of spatulas or the growing interest in modular utensil sets, allowing companies to tailor their offerings effectively. This predictive capability supports agile product development and targeted marketing strategies, ensuring that innovations resonate with the target audience.

The long-term impact of AI may also include the development of more advanced, "smart" kitchen ecosystems where utensils could potentially interact with smart appliances, though this is a more distant prospect for basic utensils. More immediately, AI-driven personalization tools on e-commerce platforms can offer customized recommendations to consumers based on their cooking habits, previous purchases, and browsing history, enhancing the online shopping experience and potentially increasing sales conversions. While the core functionality of a stainless steel utensil remains physical, AI's role lies in optimizing its journey from concept to consumer, ensuring efficiency, quality, and market relevance throughout the product lifecycle.

- Optimized manufacturing processes for improved efficiency and quality control.

- Enhanced supply chain management and demand forecasting.

- Data-driven product development based on consumer insights.

- Personalized marketing and sales recommendations for consumers.

- Potential for predictive maintenance in manufacturing machinery.

Key Takeaways Stainless Steel Kitchen Utensil Market Size & Forecast

The stainless steel kitchen utensil market is poised for robust growth, driven by fundamental shifts in consumer lifestyle and an increasing emphasis on product quality and durability. The projected Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033 underscores a stable and expanding market, reflecting sustained consumer investment in kitchenware. A primary insight is the market's resilience, even in the face of economic uncertainties, largely due to stainless steel's reputation for longevity and ease of maintenance, which appeals to budget-conscious and quality-seeking consumers alike. The forecasted increase in market value from USD 15.2 Billion to USD 25.9 Billion indicates significant opportunities for both established players and new entrants to capitalize on this upward trajectory.

A significant takeaway is the market's evolving segmentation, with growth driven not just by basic utility but by aesthetic appeal, ergonomic design, and specialized functions. This indicates a maturing consumer base that views kitchen utensils as both functional tools and extensions of their lifestyle and culinary aspirations. Consequently, manufacturers focusing on design innovation and product diversification are likely to capture a larger share of the expanding market. The widespread adoption of e-commerce platforms also signifies a critical shift in distribution channels, enabling broader market reach and direct-to-consumer engagement, which is essential for capturing future growth.

Ultimately, the market forecast highlights the enduring appeal of stainless steel as a material for kitchen essentials, supported by its hygienic properties, resistance to corrosion, and timeless aesthetic. The continuous growth trajectory suggests that while innovation in smart kitchen technology and alternative materials will play a role, the core demand for reliable, high-performing stainless steel utensils remains strong. Companies that prioritize sustainable practices, invest in product design aligned with modern culinary trends, and leverage digital distribution channels are best positioned to thrive within this promising market landscape.

- Consistent growth projected with a 6.8% CAGR, indicating market stability.

- Strong consumer demand for durable, hygienic, and aesthetically pleasing utensils.

- E-commerce platforms are pivotal in driving market expansion and accessibility.

- Design innovation and product specialization are key to market differentiation.

- Sustainability and ethical sourcing becoming critical factors for consumer choice.

Stainless Steel Kitchen Utensil Market Drivers Analysis

The stainless steel kitchen utensil market is significantly propelled by several intertwined factors that collectively contribute to its robust growth. A fundamental driver is the global increase in disposable income, particularly in emerging economies, which enables consumers to invest in higher-quality and more durable kitchenware. As living standards improve, households are transitioning from basic, low-cost utensils to premium, long-lasting stainless steel alternatives, recognizing their superior performance and longevity. This economic uplift is often accompanied by an expansion of the middle class, a demographic highly inclined to upgrade their home essentials.

Furthermore, the rising popularity of home cooking and culinary experimentation worldwide serves as a strong impetus for market expansion. Consumers, influenced by cooking shows, online tutorials, and health-conscious trends, are spending more time in their kitchens and require a wider array of specialized and reliable tools. Stainless steel utensils, known for their versatility, hygienic properties, and compatibility with various cooking methods, perfectly align with this burgeoning interest in diverse gastronomic pursuits. The material's non-reactive nature ensures food safety and preserves flavor, which is a critical consideration for health-aware consumers.

The hospitality and food service sectors also represent a substantial driver. With the continuous expansion of restaurants, hotels, cafes, and catering services globally, there is an ever-present demand for professional-grade, durable kitchen equipment capable of withstanding rigorous daily use. Stainless steel is the material of choice in commercial kitchens due to its resilience, ease of cleaning, and compliance with stringent hygiene standards. This commercial demand provides a stable base for the market, complementing the growth driven by residential consumers and ensuring continuous innovation in product performance and design.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Disposable Income | +1.5% | Asia Pacific, Latin America | Short to Mid-Term |

| Growth in Home Cooking & Culinary Trends | +1.2% | Global | Mid-Term |

| Expansion of Hospitality & Food Service Sector | +1.0% | North America, Europe, Asia Pacific | Long-Term |

| Rising Awareness of Hygiene & Durability | +0.8% | Global | Short to Mid-Term |

Stainless Steel Kitchen Utensil Market Restraints Analysis

Despite the strong growth drivers, the stainless steel kitchen utensil market faces several significant restraints that could potentially impede its expansion. One prominent challenge is the intense price sensitivity among certain consumer segments, particularly in developing markets or for basic utility items. While stainless steel offers durability, its initial cost can be higher compared to alternatives like plastic, aluminum, or silicone. This price differential can deter budget-conscious consumers, leading them to opt for less expensive materials, even if they compromise on longevity or hygiene, thereby limiting market penetration in certain segments.

Another key restraint is the availability and increasing popularity of alternative materials for kitchen utensils. Materials such as silicone, wood, bamboo, and various types of plastics have gained traction due to their specific advantages, including non-stick properties, lightweight design, heat resistance, and diverse color options. Silicone, for instance, is highly versatile for baking and non-stick cookware, while wood and bamboo appeal to eco-conscious consumers for their natural and renewable attributes. This diversification of material choices provides consumers with a broader range of options, introducing competitive pressure and potentially fragmenting the demand for stainless steel products.

Furthermore, volatility in raw material prices, particularly nickel and chromium which are key components of stainless steel, poses an ongoing challenge for manufacturers. Fluctuations in these commodity prices directly impact production costs, which can then be passed on to consumers, potentially affecting affordability and demand. Managing these cost variations while maintaining competitive pricing and profit margins requires sophisticated supply chain management and pricing strategies. Economic downturns or global supply chain disruptions can exacerbate this issue, making long-term planning and investment more complex for market participants.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Price Sensitivity & High Initial Cost | -0.9% | Global, particularly Emerging Markets | Short to Mid-Term |

| Availability of Alternative Materials | -0.8% | Global | Mid-Term |

| Volatile Raw Material Prices | -0.7% | Global | Short-Term |

| Market Saturation in Developed Regions | -0.5% | North America, Europe | Long-Term |

Stainless Steel Kitchen Utensil Market Opportunities Analysis

The stainless steel kitchen utensil market is rich with opportunities stemming from evolving consumer demands and technological advancements. One significant area of growth lies in the premiumization and specialization of products. As consumers become more discerning and invested in their culinary pursuits, there is an increasing willingness to pay for high-end, specialized utensils that offer superior performance, ergonomic design, and aesthetic appeal. This trend allows manufacturers to move beyond basic utility items and introduce innovative tools for niche cooking applications, gourmet food preparation, and specialized baking, commanding higher profit margins and fostering brand loyalty among passionate home cooks.

The expansion of e-commerce and direct-to-consumer (D2C) channels presents another substantial opportunity. Online platforms offer unparalleled reach to a global customer base, enabling brands to bypass traditional retail limitations and connect directly with consumers. This not only reduces distribution costs but also allows for more personalized marketing, direct customer feedback, and the ability to launch new products rapidly. The convenience of online shopping, coupled with detailed product descriptions and customer reviews, empowers consumers to make informed purchasing decisions, driving growth in online sales of stainless steel kitchen utensils, especially for premium or specialized items not readily available in physical stores.

Furthermore, an increasing focus on sustainable and eco-friendly products creates avenues for market differentiation. While stainless steel is inherently durable and recyclable, opportunities exist in promoting sustainable manufacturing processes, using recycled content, and ensuring ethical sourcing of raw materials. Brands that transparently communicate their commitment to environmental responsibility and provide products with extended lifespans will resonate strongly with a growing segment of environmentally conscious consumers. This aligns with broader global trends towards responsible consumption and offers a compelling value proposition beyond just product functionality, enhancing brand reputation and attracting a loyal customer base.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Premiumization & Specialization of Products | +1.1% | North America, Europe, Asia Pacific | Mid to Long-Term |

| E-commerce & Direct-to-Consumer Channel Expansion | +1.3% | Global | Short to Mid-Term |

| Focus on Sustainable & Eco-friendly Products | +0.9% | Europe, North America | Mid-Term |

| Growth in Emerging Markets | +1.0% | Asia Pacific, Latin America | Long-Term |

Stainless Steel Kitchen Utensil Market Challenges Impact Analysis

The stainless steel kitchen utensil market, despite its promising growth trajectory, confronts several challenges that demand strategic responses from industry participants. One significant challenge is intense market competition, stemming from a fragmented landscape with numerous local and international players. This high level of competition often leads to price wars, reduced profit margins, and a constant pressure for innovation. Differentiating products in a crowded market requires substantial investment in design, quality, and branding, making it difficult for new entrants to gain significant market share and for existing players to maintain their competitive edge without continuous adaptation and strong marketing efforts.

Another critical challenge involves intellectual property (IP) infringement and the proliferation of counterfeit products. The popularity and perceived value of well-known stainless steel kitchen utensil brands make them targets for imitation, particularly in regions with less stringent IP enforcement. Counterfeit products not only erode brand reputation and consumer trust but also undercut legitimate sales, impacting revenue and market share. Addressing this challenge requires robust legal frameworks, proactive monitoring of marketplaces, and consumer education campaigns to highlight the risks associated with non-genuine products, all of which incur significant costs for businesses.

Furthermore, disruptions in the global supply chain, exemplified by recent events such as pandemics, geopolitical tensions, and trade disputes, pose ongoing challenges. Manufacturers of stainless steel utensils rely on a global network for raw material sourcing, production, and distribution. Any disruption, whether it involves transportation delays, labor shortages, or increased logistical costs, can lead to production bottlenecks, inventory shortages, and increased lead times, ultimately affecting market supply and consumer satisfaction. Companies must therefore invest in resilient supply chain strategies, including diversification of suppliers and localized production where feasible, to mitigate these risks and ensure operational continuity.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition | -0.9% | Global | Ongoing |

| Intellectual Property Infringement & Counterfeits | -0.7% | Asia Pacific, Latin America | Long-Term |

| Global Supply Chain Disruptions | -0.8% | Global | Short to Mid-Term |

| Changing Consumer Preferences for Materials | -0.6% | North America, Europe | Mid-Term |

Stainless Steel Kitchen Utensil Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Stainless Steel Kitchen Utensil market, offering a detailed understanding of its current landscape, historical performance, and future growth prospects. It encapsulates market sizing, segmentation by product type, application, and distribution channel, alongside a thorough regional breakdown. The scope extends to identifying key market drivers, restraints, opportunities, and challenges, providing a holistic view of the forces shaping the industry. Furthermore, the report includes an assessment of competitive dynamics, highlighting the strategies of prominent market players and their impact on the overall market structure. This document serves as an essential resource for stakeholders seeking actionable insights into the stainless steel kitchen utensil industry's trajectory and potential investment avenues.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.2 Billion |

| Market Forecast in 2033 | USD 25.9 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Kitchenware Solutions Inc., Apex Culinary Innovations, ProChef Utensils Ltd., Stellar Home Products, Elite Cookware Manufacturing, Precision Kitchen Tools Co., Everlast Kitchen Technologies, Prime Culinary Brands, Universal Stainless Works, Modern Kitchen Essentials, Harmony Houseware Group, Dynamic Cookware Corporation, Signature Kitchen Systems, Masterpiece Utensil Design, Advanced Culinary Arts Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The global stainless steel kitchen utensil market is meticulously segmented to provide a granular understanding of its diverse components and growth dynamics. This comprehensive segmentation allows for a detailed analysis of distinct market behaviors across different product categories, end-user applications, and distribution channels, enabling stakeholders to identify specific growth opportunities and target specific consumer groups effectively. The primary segmentation distinguishes between various product types, acknowledging the specialized utility and demand for different kinds of utensils, from everyday cooking tools to specific baking or serving instruments. This categorization helps in understanding the demand patterns for individual utensil categories and their respective market sizes, allowing manufacturers to tailor their production and marketing strategies accordingly.

Further segmentation by application provides insight into the primary end-users of stainless steel kitchen utensils. The market is broadly divided into residential and commercial applications, reflecting the significant demand from individual households and the robust requirements of professional food service establishments. The residential segment is driven by evolving consumer lifestyles, increasing disposable incomes, and the growing trend of home cooking. Conversely, the commercial segment is characterized by demand for high-durability, professional-grade utensils that meet stringent hygiene standards and withstand heavy usage in hotels, restaurants, and catering services. Understanding these distinct application segments is crucial for product design, material specifications, and sales channel optimization.

The segmentation by distribution channel highlights the varied avenues through which stainless steel kitchen utensils reach consumers. This includes traditional retail formats like supermarkets, hypermarkets, specialty stores, and department stores, alongside the rapidly expanding online retail sector. The shift towards e-commerce platforms has significantly broadened market reach, offering convenience and a wider selection to consumers globally. Analyzing these distribution channels helps in understanding consumer purchasing preferences, optimizing supply chain logistics, and developing effective sales strategies that capitalize on both physical retail presence and digital market penetration. Each channel presents unique opportunities and challenges, requiring tailored approaches for maximum market capture.

- By Product Type: Cooking Utensils, Baking Utensils, Serving Utensils, Cutting Utensils, Specialty Utensils

- By Application: Residential, Commercial

- By Distribution Channel: Supermarkets & Hypermarkets, Specialty Stores, Online Retail, Department Stores, Other Retailers

Regional Highlights

- North America: This region maintains a significant market share, driven by high disposable incomes, a strong culture of home cooking, and a robust hospitality sector. The United States and Canada are key contributors, characterized by a preference for premium, durable kitchenware and strong online retail penetration. Innovation in ergonomic designs and smart kitchen integration also plays a role.

- Europe: A mature market with steady growth, primarily fueled by the region's culinary heritage, demand for high-quality craftsmanship, and increasing awareness of sustainable and hygienic kitchen solutions. Germany, the United Kingdom, and France are leading markets, with a growing emphasis on aesthetically pleasing and functionally superior utensils for both residential and commercial use.

- Asia Pacific (APAC): Expected to be the fastest-growing region, propelled by rapid urbanization, rising disposable incomes, and expanding middle-class populations in countries like China, India, and Japan. The burgeoning hospitality industry, coupled with a growing interest in diverse cuisines and home cooking, significantly boosts demand. Local manufacturing capabilities also contribute to market growth and competitive pricing.

- Latin America: This region exhibits promising growth potential, driven by improving economic conditions, increasing urbanization, and a gradual shift towards modern kitchen amenities. Brazil and Mexico are key markets, where consumers are increasingly seeking durable and functional kitchen utensils, reflecting a growing appreciation for quality home products.

- Middle East and Africa (MEA): While currently a smaller market, the MEA region is projected for steady growth due to increasing tourism, expansion of the food service sector, and rising living standards in countries like UAE, Saudi Arabia, and South Africa. Investments in hospitality infrastructure and a growing expatriate population contribute to the demand for diverse kitchenware.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Stainless Steel Kitchen Utensil Market.- Global Kitchenware Solutions Inc.

- Apex Culinary Innovations

- ProChef Utensils Ltd.

- Stellar Home Products

- Elite Cookware Manufacturing

- Precision Kitchen Tools Co.

- Everlast Kitchen Technologies

- Prime Culinary Brands

- Universal Stainless Works

- Modern Kitchen Essentials

- Harmony Houseware Group

- Dynamic Cookware Corporation

- Signature Kitchen Systems

- Masterpiece Utensil Design

- Advanced Culinary Arts Inc.

Frequently Asked Questions

What is the current market size and projected growth of the Stainless Steel Kitchen Utensil Market?

The Stainless Steel Kitchen Utensil Market is estimated at USD 15.2 Billion in 2025 and is projected to reach USD 25.9 Billion by 2033, growing at a Compound Annual Growth Rate (CAGR) of 6.8% during the forecast period.

What are the primary drivers contributing to the growth of the Stainless Steel Kitchen Utensil Market?

Key drivers include increasing disposable incomes, the global rise in home cooking and culinary exploration, the expansion of the hospitality and food service sectors, and a growing consumer preference for hygienic and durable kitchenware.

Which key trends are shaping the Stainless Steel Kitchen Utensil industry?

Major trends include a growing demand for specialized and ergonomically designed utensils, the significant expansion of online retail channels, increasing consumer emphasis on product aesthetics and premium quality, and a rising focus on sustainable manufacturing practices.

What are the main challenges faced by the Stainless Steel Kitchen Utensil Market?

Challenges include intense market competition, volatility in raw material prices, the increasing availability and popularity of alternative kitchen utensil materials, and the pervasive issue of intellectual property infringement and counterfeit products.

How is the Stainless Steel Kitchen Utensil Market segmented?

The market is segmented by product type (Cooking, Baking, Serving, Cutting, Specialty Utensils), by application (Residential, Commercial), and by distribution channel (Supermarkets & Hypermarkets, Specialty Stores, Online Retail, Department Stores, Other Retailers).

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted