Automotive Diagnostic Scanner Market

Automotive Diagnostic Scanner Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701172 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

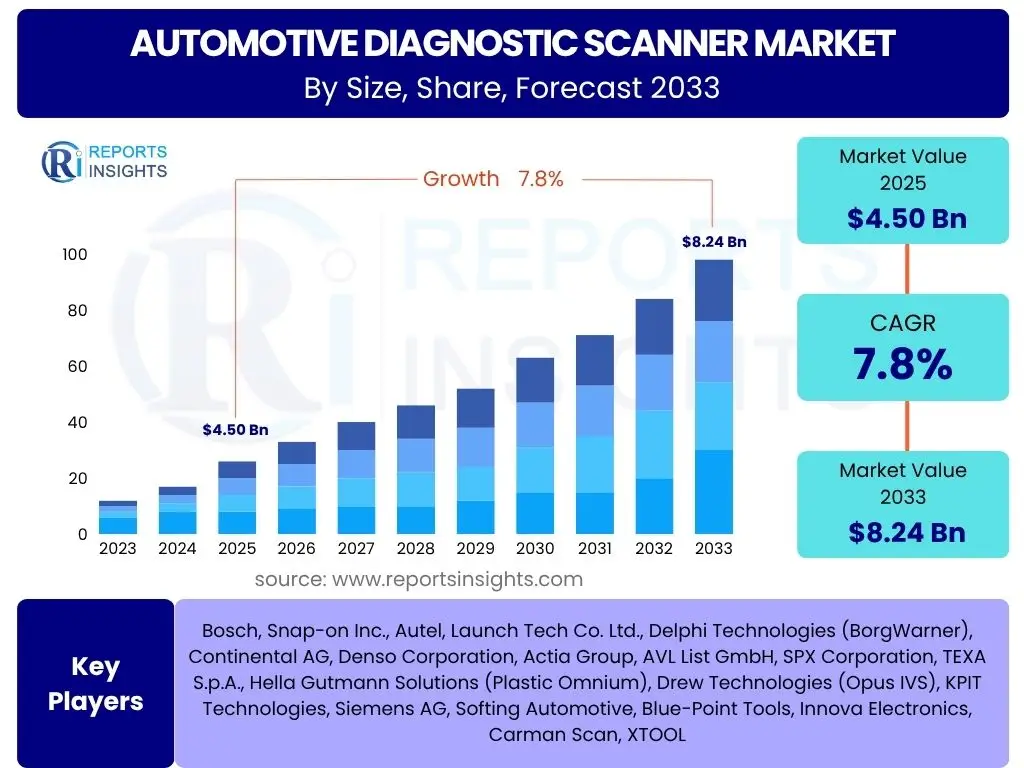

Automotive Diagnostic Scanner Market Size

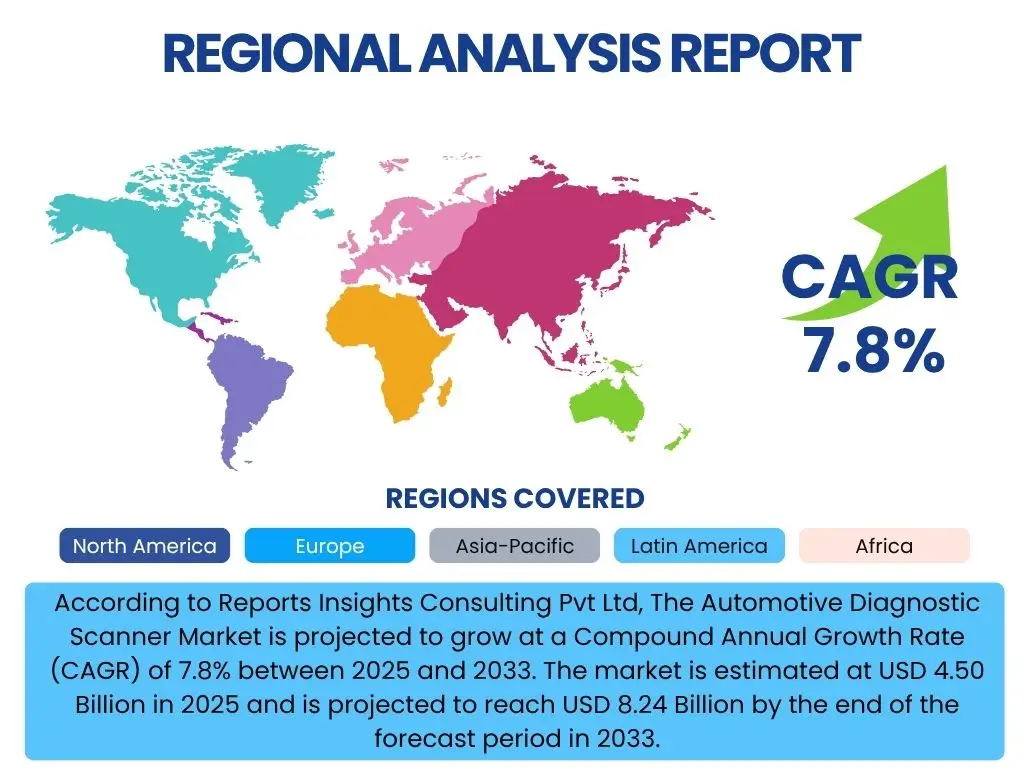

According to Reports Insights Consulting Pvt Ltd, The Automotive Diagnostic Scanner Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 4.50 Billion in 2025 and is projected to reach USD 8.24 Billion by the end of the forecast period in 2033.

Key Automotive Diagnostic Scanner Market Trends & Insights

The Automotive Diagnostic Scanner Market is currently undergoing a transformative phase driven by rapid advancements in vehicle technology and consumer expectations. A primary trend involves the increasing complexity of modern vehicles, particularly with the proliferation of advanced driver-assistance systems (ADAS), electric vehicles (EVs), and sophisticated infotainment units. These vehicles generate vast amounts of data, necessitating more powerful and intelligent diagnostic tools capable of interpreting intricate electronic systems and software anomalies. The shift from traditional combustion engines to electric powertrains introduces new diagnostic requirements, focusing on battery health, electric motor performance, and charging infrastructure compatibility.

Another significant trend is the growing demand for wireless and mobile-based diagnostic solutions. As automotive technicians and vehicle owners seek greater convenience and efficiency, Bluetooth and Wi-Fi enabled scanners that integrate with smartphones or tablets are gaining traction. This trend enhances portability, allows for over-the-air (OTA) updates, and facilitates remote diagnostics, which is becoming increasingly vital for fleet management and post-sales support. Furthermore, the integration of cloud-based platforms is enabling real-time data access, collaborative diagnostics among multiple technicians, and the aggregation of diagnostic data for predictive maintenance insights.

The aftermarket segment is also witnessing a robust trend towards Do-It-Yourself (DIY) and prosumer-grade diagnostic tools. With the rising cost of professional repairs and increased consumer awareness, individuals are seeking affordable yet capable scanners for basic troubleshooting and routine maintenance. This is paralleled by a trend in professional workshops adopting multi-brand diagnostic tools that can service a wide range of vehicle models, reducing the need for proprietary OEM-specific equipment and improving operational efficiency.

- Shift towards advanced vehicle architectures (EVs, ADAS) requiring sophisticated diagnostics.

- Increased adoption of wireless and mobile-based diagnostic solutions for enhanced flexibility.

- Growth in cloud-based platforms enabling remote diagnostics and data analytics.

- Rising demand for DIY and prosumer-grade diagnostic tools in the aftermarket.

- Expansion of multi-brand diagnostic capabilities for broader vehicle coverage.

- Emphasis on cybersecurity features within diagnostic tools to protect vehicle data.

- Emergence of predictive diagnostics through real-time data analysis.

AI Impact Analysis on Automotive Diagnostic Scanner

Artificial Intelligence (AI) is poised to revolutionize the automotive diagnostic scanner market by enhancing the accuracy, speed, and predictive capabilities of troubleshooting processes. Users are increasingly curious about how AI can move diagnostics beyond simple fault code reading to more proactive and intelligent system analysis. AI algorithms can process vast datasets of vehicle performance, sensor readings, and historical repair data to identify subtle patterns and anomalies that human technicians might miss. This allows for more precise identification of root causes, reducing diagnostic time and improving repair efficacy. For instance, AI can correlate multiple seemingly unrelated fault codes or sensor readings to pinpoint a complex system failure that is not immediately obvious.

Furthermore, AI is instrumental in developing predictive maintenance solutions within diagnostic systems. By continuously monitoring vehicle parameters and applying machine learning models, AI can forecast potential component failures before they occur. This transition from reactive repairs to proactive maintenance significantly reduces vehicle downtime, enhances safety, and lowers overall ownership costs for consumers and fleet operators. Users anticipate diagnostic tools that not only tell them what is wrong but also suggest the most probable solutions, drawing from a global database of repair experiences and technical service bulletins. The integration of natural language processing (NLP) also allows for more intuitive user interfaces, where technicians can describe symptoms in plain language, and the AI system can interpret and suggest relevant diagnostic procedures.

Another area of significant impact is the automation of diagnostic workflows and technician training. AI-powered systems can guide technicians step-by-step through complex diagnostic procedures, providing real-time data interpretation and repair recommendations. This reduces the reliance on highly specialized human expertise and can help onboard less experienced technicians more rapidly. Concerns often revolve around the accuracy of AI suggestions, data privacy, and the need for human oversight. However, the overarching expectation is that AI will make diagnostic processes more efficient, accessible, and less prone to human error, ultimately leading to a more reliable and cost-effective vehicle maintenance ecosystem.

- Enabling predictive maintenance by analyzing vehicle data for early fault detection.

- Enhancing diagnostic accuracy through advanced pattern recognition in complex systems.

- Automating troubleshooting workflows and providing step-by-step repair guidance.

- Facilitating natural language interaction for intuitive diagnostic input.

- Personalizing diagnostic recommendations based on vehicle history and usage patterns.

- Improving efficiency by reducing diagnostic time and avoiding unnecessary part replacements.

- Supporting remote diagnostics with intelligent data analysis from connected vehicles.

Key Takeaways Automotive Diagnostic Scanner Market Size & Forecast

The Automotive Diagnostic Scanner Market is poised for substantial growth, driven by an confluence of technological advancements, evolving vehicle architectures, and increasing demands for efficiency in vehicle maintenance. A primary takeaway is the significant shift from hardware-centric diagnostic tools to software-driven and connectivity-enabled solutions. This transformation is not merely about identifying fault codes but about providing comprehensive vehicle health reports, predictive insights, and integration with broader automotive ecosystems. The market's expansion is intrinsically linked to the global rise in vehicle parc, particularly the rapid adoption of electric vehicles and sophisticated internal combustion engine vehicles equipped with extensive electronic control units (ECUs) and ADAS.

Another crucial insight is the accelerating importance of data in diagnostics. Modern scanners are becoming powerful data acquisition and analysis tools, capable of capturing real-time sensor data, interpreting complex network communications (like CAN, LIN, and Ethernet), and utilizing cloud-based platforms for comparative analysis. This data-driven approach is enhancing diagnostic precision and paving the way for advanced applications such as over-the-air (OTA) software updates for vehicle systems, which can resolve issues without a physical visit to a service center. The focus is increasingly on providing actionable intelligence to technicians and vehicle owners, enabling faster and more accurate repairs, and ultimately improving vehicle uptime and safety.

The market forecast indicates robust opportunities across various segments, including professional workshops, OEM service centers, and the burgeoning DIY and aftermarket sectors. Geographical expansion, particularly in emerging economies with growing vehicle sales and increasing awareness of vehicle maintenance, will play a pivotal role. Stakeholders need to focus on developing scalable, user-friendly, and technologically advanced solutions that cater to the diverse needs of this dynamic market. The emphasis will remain on interoperability, cybersecurity, and the integration of emerging technologies like AI to deliver superior diagnostic capabilities and maintain a competitive edge.

- Market demonstrates robust growth driven by vehicle complexity and electrification.

- Shift towards software-defined and cloud-connected diagnostic platforms.

- Data analytics and AI integration are becoming central to diagnostic accuracy and prediction.

- Significant growth opportunities exist in professional, OEM, and aftermarket segments.

- Interoperability and cybersecurity are critical considerations for future product development.

- Emerging markets present substantial untapped potential for market expansion.

- Focus on providing holistic vehicle health insights beyond simple fault codes.

Automotive Diagnostic Scanner Market Drivers Analysis

The Automotive Diagnostic Scanner Market is significantly propelled by several key factors that underscore the growing necessity for sophisticated diagnostic tools. The increasing sophistication of modern vehicles, characterized by complex electronic systems, numerous ECUs, and advanced software, makes traditional manual troubleshooting insufficient. This complexity mandates the use of specialized diagnostic scanners to accurately identify, interpret, and resolve vehicle issues, driving demand across all market segments. Furthermore, the global proliferation of electric vehicles (EVs) and hybrid vehicles, each with unique diagnostic requirements related to battery management, power electronics, and motor control, is a powerful growth catalyst. These vehicles cannot be effectively serviced without specialized diagnostic equipment, creating a new and expanding niche within the market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing vehicle electrification and complexity | +1.8% | North America, Europe, Asia Pacific | 2025-2033 (Long-term) |

| Rising demand for predictive maintenance | +1.5% | Global | 2025-2033 (Medium to Long-term) |

| Growth in the aftermarket and DIY segment | +1.2% | Asia Pacific, North America, Europe | 2025-2030 (Medium-term) |

| Stringent emission norms and safety regulations | +0.8% | Europe, North America, China | 2025-2033 (Long-term) |

Automotive Diagnostic Scanner Market Restraints Analysis

Despite robust growth prospects, the Automotive Diagnostic Scanner Market faces certain restraints that could impede its full potential. A primary constraint is the high initial cost associated with advanced, multi-functional diagnostic scanners, particularly those offering comprehensive OEM-level capabilities or specialized features for complex vehicle systems like ADAS or EVs. This high cost can be a barrier for smaller independent repair shops or individual vehicle owners, limiting market penetration in cost-sensitive segments. Additionally, the rapid pace of technological advancements in vehicle electronics leads to frequent updates in diagnostic software and hardware. This constant need for upgrades and training to keep pace with evolving vehicle models and diagnostic protocols can impose significant financial and operational burdens on service providers, potentially leading to slower adoption rates for the latest technologies.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial cost of advanced diagnostic tools | -0.9% | Global, particularly emerging economies | 2025-2030 (Medium-term) |

| Lack of standardization across vehicle manufacturers | -0.7% | Global | 2025-2033 (Long-term) |

| Shortage of skilled technicians for complex diagnostics | -0.6% | North America, Europe | 2025-2033 (Long-term) |

| Data security and privacy concerns | -0.5% | Europe (GDPR), North America | 2025-2033 (Long-term) |

Automotive Diagnostic Scanner Market Opportunities Analysis

The Automotive Diagnostic Scanner Market is rich with opportunities arising from several emerging trends and evolving market dynamics. The significant growth of the connected car ecosystem presents a lucrative avenue for integrated diagnostic solutions. As vehicles become more connected, real-time data streaming and over-the-air (OTA) diagnostics become feasible, enabling remote troubleshooting, software updates, and predictive maintenance without requiring a physical visit to a service center. This not only enhances convenience for vehicle owners but also creates new service models for diagnostic tool providers and automotive service networks. Furthermore, the burgeoning demand in emerging economies, particularly in Asia Pacific and Latin America, with their rapidly expanding vehicle parc and growing automotive aftermarket, offers substantial untapped potential. These regions are witnessing increased adoption of advanced vehicles, creating a strong need for accessible and affordable diagnostic solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with connected car ecosystem and OTA updates | +1.3% | Global | 2025-2033 (Long-term) |

| Expansion into emerging markets with growing vehicle parc | +1.0% | Asia Pacific, Latin America, Middle East | 2025-2033 (Long-term) |

| Development of AI and Machine Learning-powered diagnostics | +1.1% | Global | 2025-2033 (Long-term) |

| Growth of subscription-based diagnostic software models | +0.9% | North America, Europe | 2025-2030 (Medium-term) |

Automotive Diagnostic Scanner Market Challenges Impact Analysis

The Automotive Diagnostic Scanner Market faces several notable challenges that require strategic navigation for sustained growth. One significant challenge is the rapid technological obsolescence inherent in the automotive industry. As vehicle manufacturers continually introduce new models with updated electronic architectures, proprietary software, and communication protocols, diagnostic tool manufacturers must constantly innovate and update their products. This necessitates substantial investment in research and development, as well as ongoing software updates, posing a challenge for smaller players and increasing development costs. Furthermore, ensuring interoperability across a vast array of vehicle makes and models, each potentially using different diagnostic interfaces and data formats, remains a persistent hurdle. Achieving universal compatibility while maintaining diagnostic depth is a complex engineering task.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid technological obsolescence of vehicle systems | -0.8% | Global | 2025-2033 (Long-term) |

| Interoperability issues with diverse vehicle platforms | -0.7% | Global | 2025-2033 (Long-term) |

| Cybersecurity threats and data privacy regulations | -0.6% | Europe, North America | 2025-2033 (Long-term) |

| Counterfeit diagnostic tools in the aftermarket | -0.5% | Asia Pacific, Latin America | 2025-2030 (Medium-term) |

Automotive Diagnostic Scanner Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Automotive Diagnostic Scanner Market, covering historical data, current market dynamics, and future projections from 2025 to 2033. It examines market size, growth drivers, restraints, opportunities, and challenges, along with detailed segmentation and regional insights. The report offers a strategic overview for stakeholders seeking to understand market trends and competitive landscapes.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.50 Billion |

| Market Forecast in 2033 | USD 8.24 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Bosch, Snap-on Inc., Autel, Launch Tech Co. Ltd., Delphi Technologies (BorgWarner), Continental AG, Denso Corporation, Actia Group, AVL List GmbH, SPX Corporation, TEXA S.p.A., Hella Gutmann Solutions (Plastic Omnium), Drew Technologies (Opus IVS), KPIT Technologies, Siemens AG, Softing Automotive, Blue-Point Tools, Innova Electronics, Carman Scan, XTOOL |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automotive Diagnostic Scanner Market is meticulously segmented to provide a granular understanding of its diverse components and growth avenues. These segments delineate the market based on the type of scanner, the vehicle it services, its connectivity method, and its primary application, reflecting the varied needs of end-users ranging from individual car owners to professional repair shops and OEM dealerships. Understanding these distinctions is crucial for identifying specific market niches and tailoring product development and marketing strategies. Each segment possesses unique characteristics and growth drivers, contributing distinctly to the overall market dynamics and offering varied opportunities for market participants.

- By Type:

- Handheld Diagnostic Scanners: Portable, user-friendly devices suitable for quick diagnostics and basic fault code reading.

- PC-based Diagnostic Scanners: Software-driven solutions requiring a computer, offering advanced functionalities and extensive data analysis capabilities.

- Mobile-based Diagnostic Scanners: Leverage smartphone/tablet apps for diagnostics, often wireless, providing convenience and accessibility.

- By Vehicle Type:

- Passenger Vehicles: Scanners designed for cars, SUVs, and other light-duty vehicles, representing the largest segment.

- Commercial Vehicles: Tools specifically for trucks, buses, and heavy-duty vehicles, catering to unique industrial and fleet requirements.

- By Connectivity:

- Wired Diagnostic Scanners: Rely on physical cable connections (OBD-II, USB) for direct communication.

- Wireless Diagnostic Scanners: Utilize Bluetooth, Wi-Fi, or other wireless protocols for flexible and remote connectivity.

- By Application:

- Automotive Repair Shops: Independent garages and service centers requiring versatile tools for multi-brand vehicle servicing.

- OEM Dealerships: Authorized service centers using proprietary or dedicated OEM diagnostic equipment.

- Diagnostic Centers: Specialized facilities focusing solely on vehicle diagnostics and troubleshooting.

- Vehicle Owners/DIY: Consumer-grade scanners for basic diagnostics, monitoring, and minor troubleshooting.

- Others: Includes fleet operators, academic institutions, and automotive component manufacturers for testing and development.

- By Sales Channel:

- OEM: Diagnostic tools supplied directly by vehicle manufacturers for their authorized service networks.

- Aftermarket: Diagnostic tools sold independently to repair shops, individuals, and other non-OEM service providers.

Regional Highlights

- North America: This region is a leading market, characterized by a high adoption rate of advanced automotive technologies, a robust aftermarket segment, and stringent emission regulations. The increasing complexity of vehicles, coupled with a strong DIY culture and the prevalence of connected cars, drives the demand for sophisticated diagnostic scanners. Early adoption of EV technology and advanced driver-assistance systems (ADAS) further fuels growth, particularly for intelligent, AI-integrated diagnostic solutions.

- Europe: Europe represents a mature and technologically advanced market, largely influenced by strict environmental norms and a strong emphasis on vehicle safety. Countries like Germany, the UK, and France are key contributors, driven by a large vehicle parc, high average vehicle age, and the presence of major automotive OEMs and aftermarket service providers. The region is also at the forefront of electric vehicle adoption, spurring demand for specialized EV diagnostic tools.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing market due to rapid urbanization, increasing disposable incomes, and the burgeoning vehicle production and sales, especially in countries like China, India, and Japan. The expanding middle class and the growing awareness about vehicle maintenance contribute significantly to the aftermarket segment. Furthermore, the increasing manufacturing footprint of global automotive players and the rising adoption of connected car technologies in the region create immense opportunities for diagnostic scanner manufacturers.

- Latin America: This region is an emerging market for automotive diagnostic scanners, driven by a growing vehicle parc, increasing consumer awareness, and the modernization of automotive workshops. While cost-effectiveness remains a key consideration, the demand for basic to mid-range diagnostic tools is steadily rising, presenting opportunities for manufacturers to offer solutions tailored to regional economic conditions and vehicle types.

- Middle East and Africa (MEA): The MEA market is gradually expanding, fueled by increasing vehicle sales, particularly in the Gulf Cooperation Council (GCC) countries, and a rising focus on enhancing vehicle service infrastructure. The presence of a significant used car market also contributes to the demand for diagnostic tools in the aftermarket segment. Investments in automotive service centers and the adoption of modern vehicle technologies are expected to accelerate market growth in the coming years.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Diagnostic Scanner Market.- Robert Bosch GmbH

- Snap-on Inc.

- Autel Intelligent Technology Corp., Ltd.

- Launch Tech Co. Ltd.

- Delphi Technologies (BorgWarner Inc.)

- Continental AG

- Denso Corporation

- Actia Group

- AVL List GmbH

- SPX Corporation

- TEXA S.p.A.

- Hella Gutmann Solutions (Plastic Omnium)

- Drew Technologies (Opus IVS)

- KPIT Technologies

- Siemens AG

- Softing Automotive

- Blue-Point Tools

- Innova Electronics Corporation

- Carman Scan

- XTOOL

Frequently Asked Questions

Analyze common user questions about the Automotive Diagnostic Scanner market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is an Automotive Diagnostic Scanner?

An automotive diagnostic scanner is an electronic tool used to interface with a vehicle's On-Board Diagnostics (OBD) system. It reads and interprets diagnostic trouble codes (DTCs), monitors real-time sensor data, and performs various system tests to identify and troubleshoot vehicle issues. These scanners range from basic code readers for consumers to advanced systems for professional technicians, crucial for maintaining modern vehicles with complex electronic control units (ECUs).

How is AI impacting automotive diagnostic scanners?

AI is transforming automotive diagnostic scanners by enabling predictive maintenance, enhancing diagnostic accuracy, and automating troubleshooting. AI algorithms analyze vast datasets to anticipate failures, pinpoint root causes more efficiently, and provide guided repair recommendations. This leads to faster, more precise diagnostics, reducing downtime and improving overall vehicle reliability, moving beyond simple fault code interpretation to intelligent system analysis.

What are the key trends driving the Automotive Diagnostic Scanner Market?

Key trends include the increasing complexity of modern vehicles (especially EVs and ADAS-equipped cars), the shift towards wireless and cloud-based diagnostic solutions, the rising demand for predictive maintenance, and the growth of the DIY and aftermarket segments. These trends push for more sophisticated, connected, and user-friendly diagnostic tools that can handle advanced vehicle systems and data analysis requirements.

What are the primary challenges in the Automotive Diagnostic Scanner Market?

Major challenges include the rapid technological obsolescence of vehicle systems, leading to constant update requirements for scanners; interoperability issues due to diverse vehicle communication protocols; growing concerns over data security and privacy; and the prevalence of counterfeit diagnostic tools. Addressing these requires continuous innovation, standardization efforts, and robust cybersecurity measures from manufacturers.

Which regions are key players in the Automotive Diagnostic Scanner Market?

North America and Europe are mature markets driven by technological adoption and stringent regulations. Asia Pacific is the fastest-growing region, fueled by expanding vehicle sales and increasing awareness in countries like China and India. Latin America and MEA are emerging markets with significant growth potential, as their automotive sectors modernize and vehicle parc continues to expand, leading to a rising demand for diagnostic tools.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted