Wilson Disease Treatment Market

Wilson Disease Treatment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704102 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

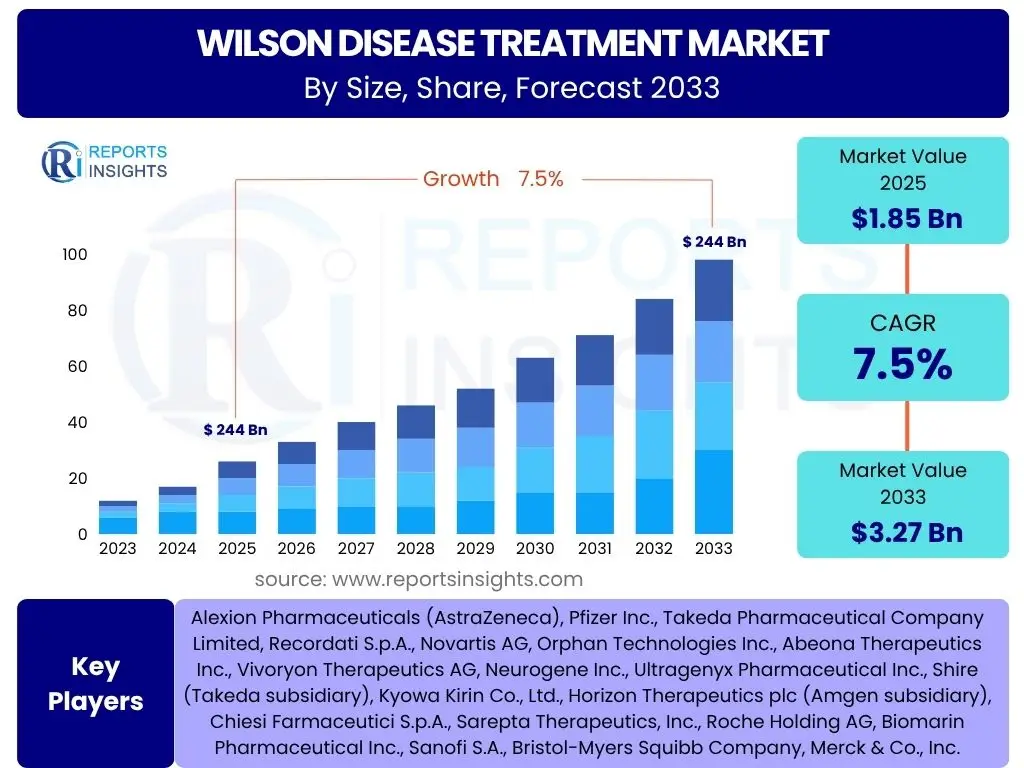

Wilson Disease Treatment Market Size

According to Reports Insights Consulting Pvt Ltd, The Wilson Disease Treatment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2025 and 2033. The market is estimated at USD 1.85 billion in 2025 and is projected to reach USD 3.27 billion by the end of the forecast period in 2033.

The expansion of the Wilson Disease Treatment market is fundamentally driven by the increasing global prevalence of this rare genetic disorder, coupled with significant advancements in diagnostic capabilities that lead to earlier and more accurate diagnoses. As awareness among healthcare professionals and the general public grows, a larger proportion of affected individuals are identified and brought into the treatment paradigm. This heightened diagnostic efficiency directly translates into a greater demand for effective therapeutic interventions, ranging from established pharmacological treatments to emerging novel therapies.

Furthermore, continuous research and development efforts by pharmaceutical and biotechnology companies are pivotal in shaping the market's trajectory. These endeavors focus on improving existing treatment modalities by reducing side effects, enhancing efficacy, and exploring entirely new therapeutic avenues such as gene therapies. The investment in clinical trials for new drugs and the strategic pursuit of orphan drug designations by companies underscore a robust commitment to addressing the unmet medical needs of Wilson Disease patients, thereby contributing substantially to market growth over the forecast period.

Key Wilson Disease Treatment Market Trends & Insights

Analysis of common inquiries regarding the Wilson Disease Treatment market reveals a strong interest in the evolution of therapeutic approaches, particularly the shift towards more targeted and personalized medicine. Users frequently inquire about the impact of genetic research on treatment development, the role of advanced diagnostics in early intervention, and the potential of non-pharmacological management strategies. There is also significant curiosity about the integration of digital health solutions and patient support programs in managing this chronic condition, indicating a broader focus beyond just drug efficacy to holistic patient care and quality of life improvements.

The market is witnessing a profound transformation driven by innovation in drug development and a deeper understanding of the disease's underlying pathophysiology. A key trend is the development of next-generation chelating agents and zinc therapies designed to offer improved tolerability profiles and enhanced efficacy compared to traditional treatments. These advancements aim to mitigate the burden of long-term adherence and reduce the incidence of adverse effects, which are common challenges in chronic disease management for Wilson Disease patients. The pursuit of safer and more patient-friendly oral formulations is also a significant area of focus, recognizing the importance of convenience in sustained therapy.

Another prominent trend involves the acceleration of research into gene therapies and other liver-directed therapeutic strategies. These novel approaches represent a paradigm shift from symptomatic management to potentially curative interventions, addressing the genetic defect directly. Although still largely in clinical development phases, the promise of a one-time or infrequent treatment could revolutionize the landscape for Wilson Disease. Complementing these therapeutic advancements, there is an increasing emphasis on precision medicine, where treatment regimens are tailored based on individual patient genetics, disease severity, and response patterns, optimizing outcomes and minimizing unnecessary side effects. This personalized approach is further supported by innovations in biomarker identification and advanced diagnostic techniques that allow for more accurate patient stratification and monitoring.

- Development of novel chelating agents with improved safety and efficacy profiles.

- Emergence of gene therapies and liver-directed therapies offering potential curative approaches.

- Advancements in diagnostic methodologies for earlier and more accurate disease detection.

- Increasing adoption of personalized medicine approaches based on genetic profiling.

- Integration of digital health platforms for remote monitoring and patient support.

- Growing focus on improving patient adherence through better tolerability and convenient formulations.

- Expansion of global awareness campaigns to reduce diagnostic delays.

AI Impact Analysis on Wilson Disease Treatment

Common user questions regarding the impact of Artificial Intelligence (AI) on Wilson Disease Treatment often revolve around its potential to accelerate drug discovery, enhance diagnostic accuracy, and optimize patient management. Users are keen to understand how AI can identify novel therapeutic targets, interpret complex medical imaging, and predict disease progression or treatment response. Concerns frequently expressed include data privacy, the validation of AI algorithms in rare diseases, and the potential for AI to augment rather than replace human expertise in clinical decision-making. There is a general expectation that AI will bring unprecedented efficiencies and insights to a condition that often requires lifelong, precise management.

AI's influence on the Wilson Disease Treatment market is multi-faceted, profoundly impacting various stages from fundamental research to patient care delivery. In drug discovery and development, AI algorithms are instrumental in analyzing vast datasets of genomic, proteomic, and clinical information to identify potential drug candidates and therapeutic pathways. This capability significantly reduces the time and cost associated with preclinical research, accelerating the identification of compounds that could modulate copper metabolism or repair genetic defects. Furthermore, AI can predict the efficacy and toxicity profiles of new molecules, streamlining the lead optimization process and increasing the probability of success in clinical trials for novel Wilson Disease therapies.

Beyond drug development, AI is transforming diagnostic processes and patient management. Machine learning models can analyze medical images, such as MRI scans of the brain and liver, to detect subtle signs of copper accumulation earlier and more accurately than conventional methods, aiding in prompt diagnosis, especially in atypical presentations. In patient management, AI-driven tools can monitor treatment adherence, track symptoms, and analyze patient-reported outcomes, providing clinicians with real-time insights to adjust therapies proactively. Predictive analytics, powered by AI, can also forecast disease progression or identify patients at higher risk of complications, enabling preventative interventions and personalized treatment adjustments, thereby enhancing overall patient outcomes and resource utilization within healthcare systems dedicated to rare diseases.

- Enhanced diagnostic accuracy through AI-powered image analysis and biomarker identification.

- Accelerated drug discovery and development by identifying novel therapeutic targets and predicting compound efficacy.

- Optimization of clinical trial design and patient selection using AI for data analysis.

- AI-driven personalized treatment regimens based on patient genetic profiles and disease progression.

- Improved patient monitoring and adherence through smart devices and AI-enabled digital health platforms.

- Predictive analytics for early identification of complications and proactive disease management.

- Facilitation of research by processing and synthesizing large volumes of rare disease data.

Key Takeaways Wilson Disease Treatment Market Size & Forecast

Analysis of common user questions regarding key takeaways from the Wilson Disease Treatment market size and forecast highlights a significant interest in growth drivers, emerging therapeutic classes, and the impact of diagnostics on market expansion. Users frequently inquire about the most impactful factors contributing to the projected growth, whether new treatments will displace existing ones, and the regional disparities in market development. There is a clear emphasis on understanding the long-term outlook for treatment options and the market's potential to address the current unmet needs of patients with Wilson Disease, including access to advanced therapies and improved quality of life.

A primary takeaway is the robust growth trajectory of the Wilson Disease Treatment market, underpinned by an increasing prevalence of diagnosed cases and an expanding pipeline of innovative therapies. The market is not merely growing due to general healthcare expenditure increases, but specifically driven by enhanced understanding of the disease, leading to more targeted and effective interventions. This growth signifies a positive trend for patients, as it implies greater investment in research and development, potentially leading to better outcomes and a broader array of treatment choices in the coming years. The forecast period is expected to see a shift from conventional symptom management to more disease-modifying or even curative approaches, which will fundamentally reshape market dynamics and patient expectations.

Furthermore, the market's future is heavily reliant on the successful translation of preclinical research into approved clinical therapies, particularly in the realm of gene therapy and other advanced biologics. While current treatments remain essential, the advent of new modalities promises to address limitations such as treatment adherence issues and the progression of neurological symptoms despite current therapy. The market's expansion will also be influenced by regional variations in diagnostic capabilities, healthcare infrastructure, and regulatory landscapes. Emerging economies, as their healthcare systems mature and awareness improves, are anticipated to contribute significantly to market expansion, offering new avenues for market penetration and patient access to necessary treatments, thereby reinforcing the global growth narrative for Wilson Disease therapies.

- Significant market growth driven by increased awareness, improved diagnostics, and a robust therapeutic pipeline.

- Emergence of gene therapies and other advanced biologics as future cornerstones of treatment.

- Ongoing shift towards personalized medicine approaches for optimized patient outcomes.

- Rising prevalence of diagnosed Wilson Disease cases globally fuels demand for therapies.

- Investments in research and development by pharmaceutical companies remain a strong market driver.

- Growing importance of early diagnosis and intervention in mitigating disease progression.

- Regional disparities in healthcare access and diagnostic capabilities will influence market penetration.

Wilson Disease Treatment Market Drivers Analysis

The Wilson Disease Treatment market is significantly propelled by several key factors that contribute to its projected growth. A fundamental driver is the increasing global incidence and prevalence of diagnosed Wilson Disease cases, which directly translates into a higher demand for therapeutic solutions. As diagnostic tools become more sophisticated and healthcare professionals gain a deeper understanding of the disease's varied clinical presentations, more individuals are identified and require lifelong treatment, thereby expanding the patient pool and market size. This enhanced diagnostic capability, particularly for early-stage disease, is critical in initiating timely intervention and improving patient outcomes, further solidifying the need for effective treatments.

Another powerful impetus for market expansion stems from the continuous advancements in research and development within the pharmaceutical and biotechnology sectors. Companies are heavily investing in developing novel therapeutic agents that offer improved efficacy, reduced side effects, and enhanced patient compliance compared to existing treatments. This includes the exploration of new chelating agents, zinc formulations, and, most notably, the pioneering work in gene therapies and other targeted biologics aimed at addressing the root cause of the disorder. The promise of these innovative therapies, coupled with a supportive regulatory environment that often provides orphan drug designations for rare diseases, incentivizes further investment and accelerates market entry for new treatments, driving both volume and value growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Prevalence & Diagnosis | +2.1% | Global, particularly Asia Pacific & North America | Short to Long-term (2025-2033) |

| Advancements in Drug Development (Novel Therapies) | +1.8% | North America, Europe, Key emerging markets | Medium to Long-term (2027-2033) |

| Growing Awareness & Early Intervention Programs | +1.5% | Global, especially developing regions | Short to Medium-term (2025-2030) |

| Favorable Government Support & Orphan Drug Designations | +1.0% | North America, Europe, Japan | Short to Long-term (2025-2033) |

Wilson Disease Treatment Market Restraints Analysis

Despite the positive growth outlook, the Wilson Disease Treatment market faces several significant restraints that could impede its expansion. One major challenge is the high cost associated with both existing and emerging advanced therapies. As a rare genetic disorder, the development and manufacturing of specialized drugs, particularly novel biologics and gene therapies, involve substantial research and development investments, which often translate into high price points for patients and healthcare systems. This can limit patient access, especially in regions with underdeveloped healthcare infrastructure or limited insurance coverage, potentially hindering broader market penetration and adoption of effective treatments.

Another notable restraint is the complexity and challenges associated with early and accurate diagnosis of Wilson Disease. Its varied clinical manifestations, which can mimic other neurological, hepatic, or psychiatric conditions, often lead to misdiagnosis or delayed diagnosis. This diagnostic dilemma means that many patients may only receive a confirmed diagnosis at advanced stages of the disease, when irreversible damage has already occurred, limiting the efficacy of some treatments and potentially reducing the overall addressable patient population for early intervention therapies. Furthermore, the limited availability of specialized diagnostic centers and trained healthcare professionals in many parts of the world exacerbates this issue, restricting market access and growth in underserved regions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Advanced Therapies | -1.2% | Global, especially emerging markets | Long-term (2025-2033) |

| Challenges in Early & Accurate Diagnosis | -0.9% | Global, more pronounced in developing regions | Short to Medium-term (2025-2030) |

| Side Effects & Patient Adherence Issues with Current Therapies | -0.7% | Global | Short to Long-term (2025-2033) |

| Limited Awareness Among General Physicians | -0.5% | Global, particularly rural areas | Short to Medium-term (2025-2030) |

Wilson Disease Treatment Market Opportunities Analysis

The Wilson Disease Treatment market presents significant opportunities for growth and innovation, driven by several evolving factors. A key opportunity lies in the burgeoning pipeline of novel therapeutic candidates, particularly gene therapies and small molecules designed to address specific aspects of copper metabolism or even correct the underlying genetic defect. These therapies promise to offer superior efficacy, improved safety profiles, and potentially one-time or infrequent administration, which could revolutionize patient care by enhancing treatment adherence and reducing the long-term burden of chronic medication. The successful clinical development and market approval of these agents will open up substantial new revenue streams and dramatically reshape the treatment landscape.

Another substantial opportunity is found in the expansion into untapped emerging markets, particularly in Asia Pacific, Latin America, and parts of the Middle East and Africa. These regions, characterized by large populations and developing healthcare infrastructures, represent a significant patient pool that is currently underserved due to limited diagnostic capabilities, lack of awareness, or restricted access to specialized treatments. As economic development progresses and healthcare expenditure increases in these areas, coupled with growing awareness campaigns and improving diagnostic networks, there will be a substantial demand for effective Wilson Disease treatments. Strategic investments in market penetration, local partnerships, and patient education programs in these regions can unlock considerable growth potential, expanding the global reach of existing and future therapies.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Pipeline Development of Gene Therapies & Novel Biologics | +2.5% | Global, led by developed markets | Medium to Long-term (2027-2033) |

| Expansion in Untapped Emerging Markets | +1.9% | Asia Pacific, Latin America, MEA | Medium to Long-term (2027-2033) |

| Technological Advancements in Diagnostics | +1.5% | Global | Short to Medium-term (2025-2030) |

| Strategic Collaborations & Partnerships | +1.0% | Global | Short to Long-term (2025-2033) |

Wilson Disease Treatment Market Challenges Impact Analysis

The Wilson Disease Treatment market faces several complex challenges that necessitate strategic approaches from stakeholders. A primary challenge is the significant delay often encountered in diagnosing Wilson Disease, primarily due to its heterogeneous clinical presentation which can mimic a wide array of neurological, hepatic, and psychiatric conditions. This diagnostic odyssey means that many patients are only diagnosed at advanced stages, when irreversible organ damage may have already occurred. Late diagnosis limits the effectiveness of early intervention strategies and often necessitates more aggressive or invasive treatments, complicating patient management and potentially impacting long-term outcomes, thereby reducing the addressable window for certain therapies.

Another substantial challenge revolves around ensuring long-term patient adherence to treatment regimens, which are typically lifelong. Existing chelating agents and zinc therapies can have notable side effects, impacting patient quality of life and potentially leading to non-compliance. Non-adherence is a critical issue as it can result in disease progression, clinical decompensation, and increased healthcare costs due to complications. Furthermore, the rarity of the disease, combined with its complex management, requires specialized expertise which may not be readily available in all healthcare settings, particularly in rural or underserved areas. This can lead to suboptimal care, fragmented treatment, and difficulties in monitoring disease progression and treatment response, posing a significant hurdle for effective market penetration and patient care globally.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Delayed & Misdiagnosis of Wilson Disease | -1.5% | Global, especially developing regions | Short to Long-term (2025-2033) |

| Patient Adherence & Side Effects of Existing Therapies | -1.0% | Global | Short to Long-term (2025-2033) |

| Limited Access to Specialized Care & Expertise | -0.8% | Global, more prevalent in rural/remote areas | Short to Medium-term (2025-2030) |

| High Cost of Screening & Long-term Monitoring | -0.6% | Global, particularly affecting public health systems | Short to Long-term (2025-2033) |

Wilson Disease Treatment Market - Updated Report Scope

This market research report provides a comprehensive analysis of the Wilson Disease Treatment market, offering an in-depth assessment of market size, trends, drivers, restraints, opportunities, and challenges across various segments and key geographical regions. The scope encompasses detailed insights into current and emerging therapeutic options, including chelating agents, zinc salts, and advanced pipeline therapies such as gene therapy. The report also integrates the impact of artificial intelligence on diagnostics and drug development, alongside a thorough competitive landscape analysis, to provide stakeholders with actionable intelligence for strategic decision-making in this critical rare disease market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 billion |

| Market Forecast in 2033 | USD 3.27 billion |

| Growth Rate | 7.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Alexion Pharmaceuticals (AstraZeneca), Pfizer Inc., Takeda Pharmaceutical Company Limited, Recordati S.p.A., Novartis AG, Orphan Technologies Inc., Abeona Therapeutics Inc., Vivoryon Therapeutics AG, Neurogene Inc., Ultragenyx Pharmaceutical Inc., Shire (Takeda subsidiary), Kyowa Kirin Co., Ltd., Horizon Therapeutics plc (Amgen subsidiary), Chiesi Farmaceutici S.p.A., Sarepta Therapeutics, Inc., Roche Holding AG, Biomarin Pharmaceutical Inc., Sanofi S.A., Bristol-Myers Squibb Company, Merck & Co., Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Wilson Disease Treatment market is comprehensively segmented to provide a granular understanding of its various facets, enabling targeted strategic planning. This segmentation, primarily by drug type, treatment type, route of administration, distribution channel, and end-user, offers a multi-dimensional view of how different therapeutic approaches and delivery mechanisms contribute to market dynamics. Each segment reflects unique demand patterns, technological advancements, and patient preferences, showcasing the diverse landscape of Wilson Disease management and identifying key areas of growth and opportunity for stakeholders. Analyzing these segments is crucial for identifying niches, understanding competitive positioning, and predicting future market shifts.

The segmentation by drug type, which includes chelating agents, zinc salts, and emerging therapies like Ammonium Tetrathiomolybdate, highlights the current pharmacological backbone of Wilson Disease treatment while also forecasting the impact of pipeline candidates. Chelating agents remain foundational, but zinc salts are gaining traction due to better tolerability for maintenance therapy. Furthermore, the segmentation by treatment type, differentiating between pharmacotherapy, liver transplantation, and the nascent but transformative gene therapy, illustrates the evolving spectrum of interventions from lifelong drug regimens to potentially curative genetic corrections. This reflects the increasing focus on addressing the root cause of the disease and improving patient quality of life substantially.

Further granular analysis through segmentation by route of administration (oral vs. injectable), distribution channels (hospital, retail, online, specialty pharmacies), and end-users (hospitals, specialty clinics, research institutions) provides critical insights into market access, patient convenience, and healthcare infrastructure influences. The growing prominence of specialty pharmacies and online platforms, for instance, underscores a shift towards more specialized and accessible drug delivery models, particularly for rare and chronic conditions requiring complex management. Understanding these interdependencies across segments is vital for developing effective market entry strategies, optimizing supply chains, and ensuring broad patient access to essential Wilson Disease treatments across different healthcare settings.

- By Drug Type:

- Chelating Agents (D-penicillamine, Trientine)

- Zinc Salts (Zinc Acetate)

- Ammonium Tetrathiomolybdate (ATTM)

- Other Drugs (e.g., Investigational therapies, combination therapies)

- By Treatment Type:

- Pharmacotherapy

- Liver Transplantation

- Gene Therapy (Emerging)

- By Route of Administration:

- Oral

- Injectable

- By Distribution Channel:

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Specialty Pharmacies

- By End-User:

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

- Research & Academic Institutions

Regional Highlights

The global Wilson Disease Treatment market exhibits significant regional variations, influenced by factors such as disease prevalence, healthcare infrastructure, diagnostic capabilities, and regulatory frameworks. North America and Europe currently dominate the market, largely due to a higher awareness of rare diseases, advanced diagnostic facilities, robust healthcare spending, and the presence of leading pharmaceutical and biotechnology companies investingheavily in rare disease research and development. These regions also benefit from established reimbursement policies and strong patient advocacy groups, which collectively ensure greater access to specialized treatments and drive the adoption of novel therapies as they enter the market.

The Asia Pacific region is poised for substantial growth in the forecast period, driven by its large population base, increasing healthcare expenditure, and improving diagnostic capabilities, particularly in countries like China, India, and Japan. While these countries may have a higher genetic predisposition for Wilson Disease in certain populations, historically, diagnosis has been challenging due to limited awareness and infrastructure. However, with economic development, expanding healthcare access, and the proliferation of specialized medical centers, there is a growing opportunity for market penetration. Latin America, the Middle East, and Africa also present emerging opportunities, albeit at a slower pace, contingent on healthcare reforms, increased investment in rare disease management, and a greater emphasis on early screening and diagnosis.

- North America: Dominant market share attributed to high awareness, advanced healthcare infrastructure, significant R&D investments, and favorable reimbursement policies. Leading in early adoption of novel therapies.

- Europe: Strong market presence due to robust healthcare systems, government support for rare diseases, and a focus on personalized medicine. Witnessing a steady increase in diagnosis rates and access to specialized treatments.

- Asia Pacific (APAC): Fastest-growing market segment driven by increasing prevalence, improving diagnostic infrastructure, rising healthcare expenditure, and growing awareness in populous countries like China and India.

- Latin America: Emerging market with growing potential, influenced by improving economic conditions, expanding healthcare access, and increasing efforts to address rare diseases, though challenges in diagnosis and affordability persist.

- Middle East & Africa (MEA): Nascent market for Wilson Disease treatment, with growth linked to evolving healthcare systems, increasing medical tourism, and rising awareness of genetic disorders, albeit with significant disparities across countries.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Wilson Disease Treatment Market.- Alexion Pharmaceuticals (AstraZeneca)

- Pfizer Inc.

- Takeda Pharmaceutical Company Limited

- Recordati S.p.A.

- Novartis AG

- Orphan Technologies Inc.

- Abeona Therapeutics Inc.

- Vivoryon Therapeutics AG

- Neurogene Inc.

- Ultragenyx Pharmaceutical Inc.

- Shire (Takeda subsidiary)

- Kyowa Kirin Co., Ltd.

- Horizon Therapeutics plc (Amgen subsidiary)

- Chiesi Farmaceutici S.p.A.

- Sarepta Therapeutics, Inc.

- Roche Holding AG

- Biomarin Pharmaceutical Inc.

- Sanofi S.A.

- Bristol-Myers Squibb Company

- Merck & Co., Inc.

Frequently Asked Questions

What are the primary treatment options for Wilson Disease?

The primary treatment options for Wilson Disease involve lifelong pharmacotherapy, predominantly with chelating agents such as D-penicillamine or Trientine, which help remove excess copper from the body, and zinc salts like Zinc Acetate, which block copper absorption. In cases of severe liver failure, liver transplantation may be a life-saving intervention. Emerging treatments, particularly gene therapies, are also under development and show promise for future curative approaches.

How is Wilson Disease diagnosed, and why is early diagnosis important?

Wilson Disease is diagnosed through a combination of clinical symptoms, serum ceruloplasmin levels, 24-hour urinary copper excretion, liver biopsy, and genetic testing for ATP7B gene mutations. Early diagnosis is crucial because timely intervention can prevent irreversible organ damage, particularly to the liver and brain, and significantly improve patient outcomes and quality of life by initiating copper-chelating or zinc therapy before severe symptoms manifest.

What is the market outlook for new therapies in Wilson Disease treatment?

The market outlook for new therapies in Wilson Disease treatment is highly promising, driven by a robust pipeline focusing on gene therapies and other innovative biologics. These novel approaches aim to offer more effective, tolerable, and potentially curative solutions compared to existing lifelong oral therapies. Successful clinical development and regulatory approval of these next-generation treatments are expected to significantly expand market value and improve patient care over the forecast period.

What are the main challenges in managing Wilson Disease?

Key challenges in managing Wilson Disease include its complex and varied clinical presentation, often leading to delayed or misdiagnosis. Ensuring lifelong patient adherence to treatment regimens, which can have side effects, is also a significant hurdle. Additionally, the high cost of advanced therapies and the limited availability of specialized care centers in some regions pose substantial challenges to effective disease management and equitable access to treatment.

How will artificial intelligence (AI) impact Wilson Disease treatment?

Artificial intelligence (AI) is set to significantly impact Wilson Disease treatment by enhancing diagnostic accuracy through advanced image analysis and biomarker identification. AI also accelerates drug discovery by efficiently analyzing vast datasets to identify novel therapeutic targets and predict compound efficacy. Furthermore, AI-driven tools can optimize patient monitoring, personalize treatment regimens, and improve adherence, leading to more precise and effective disease management strategies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted