Metal Treatment Chemical Market

Metal Treatment Chemical Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704267 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

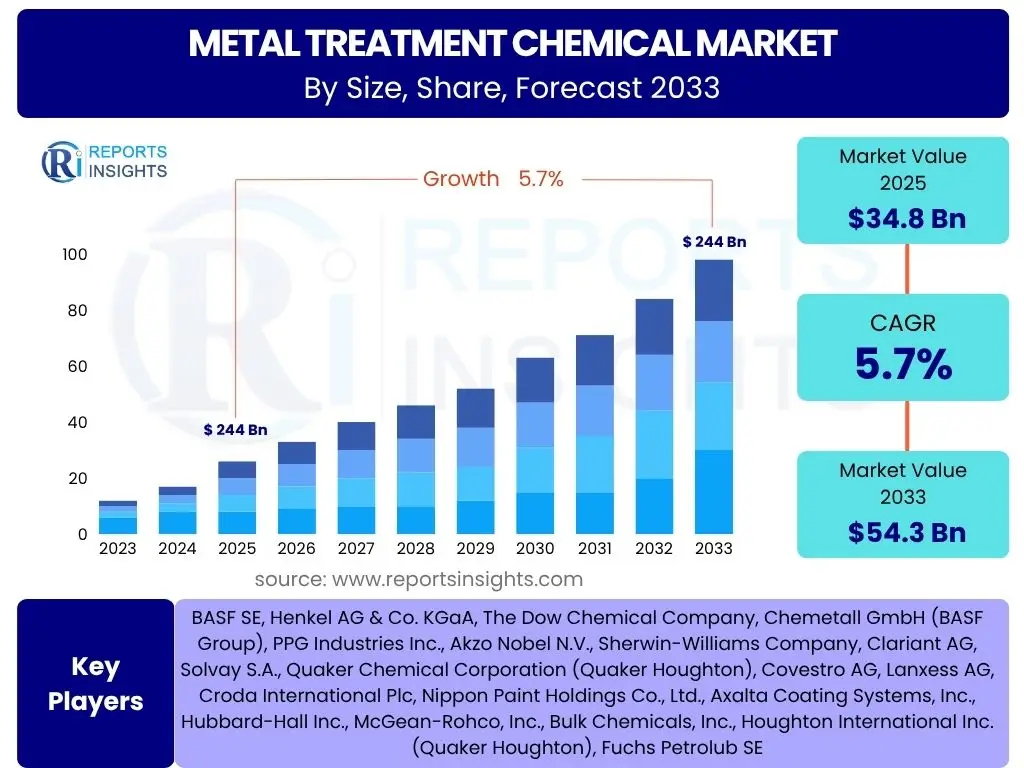

Metal Treatment Chemical Market Size

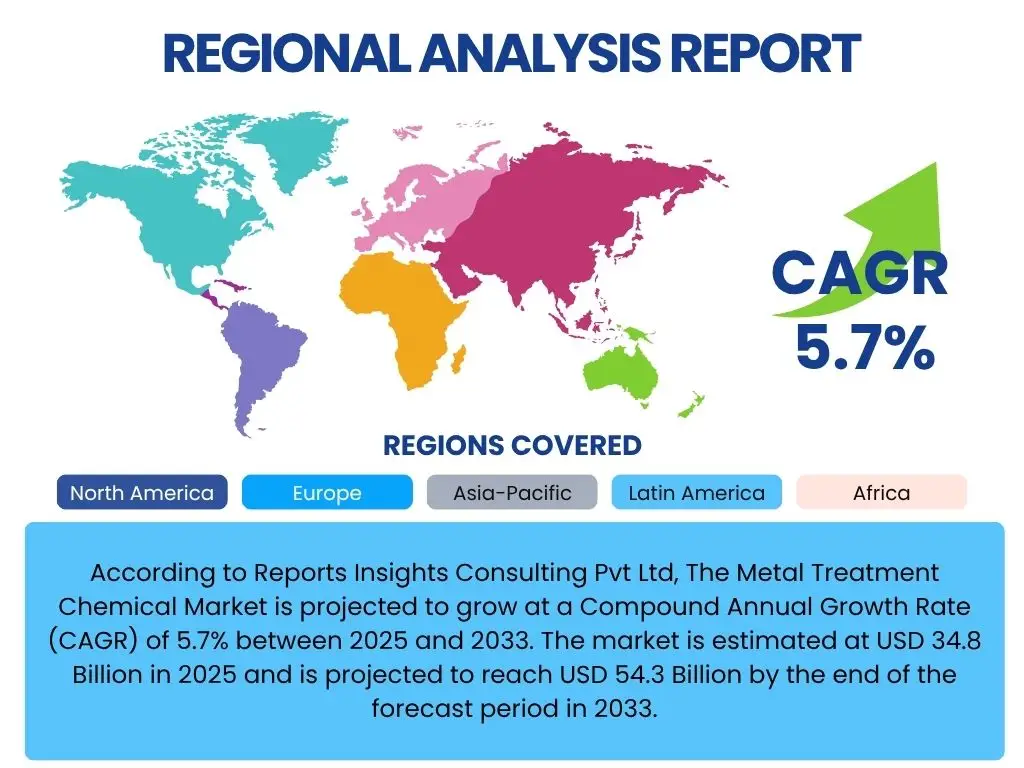

According to Reports Insights Consulting Pvt Ltd, The Metal Treatment Chemical Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.7% between 2025 and 2033. The market is estimated at USD 34.8 Billion in 2025 and is projected to reach USD 54.3 Billion by the end of the forecast period in 2033.

Key Metal Treatment Chemical Market Trends & Insights

Analysis of common user inquiries regarding the Metal Treatment Chemical market reveals a strong interest in the evolution of sustainable practices, the impact of digitalization, and the increasing demand for specialized, high-performance solutions. Users frequently seek information on how environmental regulations are shaping product innovation and the adoption of greener alternatives. There is also significant curiosity about the integration of advanced manufacturing techniques and the growing need for chemical treatments that enhance material properties for emerging industrial applications.

- Shift towards eco-friendly and bio-based metal treatment chemicals.

- Rising adoption of digitalization and automation in treatment processes.

- Increasing demand for high-performance coatings and specialized surface treatments.

- Growth in the electric vehicle (EV) sector driving new material and treatment requirements.

- Focus on circular economy principles and waste reduction in chemical manufacturing.

- Advancements in nanotechnology for enhanced material properties.

AI Impact Analysis on Metal Treatment Chemical

User questions regarding the influence of Artificial Intelligence (AI) on the Metal Treatment Chemical market predominantly revolve around process optimization, predictive maintenance, and quality control. Stakeholders are keen to understand how AI can improve efficiency, reduce waste, and enhance the consistency of chemical application. Concerns also emerge about the initial investment required for AI integration and the need for skilled personnel to manage these advanced systems. Expectations are high for AI to enable more precise chemical formulations and real-time monitoring capabilities.

- Optimization of chemical formulations and dosages for improved performance and reduced consumption.

- Predictive maintenance for treatment equipment, minimizing downtime and operational costs.

- Enhanced quality control through real-time data analysis and anomaly detection.

- Accelerated research and development of new metal treatment chemicals using AI-driven simulations.

- Streamlined supply chain management and inventory optimization for raw materials.

- Improved safety protocols through AI-powered risk assessment and monitoring.

Key Takeaways Metal Treatment Chemical Market Size & Forecast

Common user questions regarding the Metal Treatment Chemical market size and forecast highlight a strong interest in understanding the primary growth drivers and the regional market dynamics. Users frequently inquire about which end-use industries are contributing most significantly to market expansion and the projected trajectory of market value over the next decade. There is a clear demand for insights into the long-term viability of current technologies and the potential for disruptive innovations to influence future market sizing, alongside a keen focus on sustainability as a pervasive market influence.

- The market is poised for steady growth, driven by industrial expansion and technological advancements.

- Significant opportunities exist in sustainable and eco-friendly chemical solutions.

- Automotive and general industrial sectors remain key demand generators.

- Asia Pacific is expected to lead market expansion due to rapid industrialization.

- Regulatory landscapes globally will increasingly influence product development and market adoption.

- Investment in R&D for novel, high-performance treatment chemicals is crucial for competitive advantage.

Metal Treatment Chemical Market Drivers Analysis

The Metal Treatment Chemical market is propelled by a confluence of factors, prominently including the robust expansion of the manufacturing and industrial sectors globally. As industries like automotive, aerospace, construction, and electronics continue to innovate and expand, the demand for high-performance materials and components intensifies, necessitating advanced metal treatment solutions for durability, aesthetics, and functionality. Moreover, stringent regulatory frameworks related to corrosion protection, surface finishing, and material longevity are compelling industries to adopt superior chemical treatments to meet compliance standards and enhance product lifespan. This regulatory push often favors advanced, environmentally compliant chemistries, further stimulating market growth.

Additionally, the increasing focus on lightweighting in sectors such as automotive and aerospace, driven by fuel efficiency and emission reduction goals, fuels demand for specialized treatment chemicals that enable the use of advanced alloys and composites. The growing adoption of electric vehicles also creates new requirements for battery components and structural materials, which often necessitate specific chemical treatments to ensure performance and safety. Furthermore, rapid urbanization and infrastructure development in emerging economies are creating a substantial need for durable metal components, which in turn drives the demand for effective metal treatment chemicals to protect against environmental degradation and wear.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Automotive and Aerospace Industries | +1.2% | Global, particularly North America, Europe, Asia Pacific | Medium-term (2025-2029) |

| Stringent Regulatory Standards for Material Durability | +0.9% | Europe, North America, East Asia | Long-term (2025-2033) |

| Increasing Demand for Lightweight Materials | +0.8% | Global, especially China, USA, Germany | Medium-term (2026-2031) |

| Infrastructure Development and Urbanization | +0.7% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2027-2033) |

| Technological Advancements in Surface Engineering | +0.6% | Developed Economies | Continuous |

Metal Treatment Chemical Market Restraints Analysis

The Metal Treatment Chemical market faces significant restraints, primarily stemming from the increasingly stringent environmental regulations governing the use and disposal of industrial chemicals. Many traditional metal treatment processes involve hazardous substances, and evolving global regulations, such as REACH in Europe and similar initiatives in other regions, impose strict limits on emissions and waste, driving up compliance costs and forcing manufacturers to invest in more expensive, greener alternatives. This regulatory pressure can hinder market growth, particularly for companies reliant on older, less compliant chemistries, and it often necessitates substantial R&D investments to develop new, environmentally friendly formulations that meet performance requirements.

Furthermore, the volatility in raw material prices poses a consistent challenge to market stability and profitability. The production of metal treatment chemicals relies on various raw materials, including specialty chemicals, acids, and alkalis, whose prices can fluctuate significantly due to geopolitical events, supply chain disruptions, or changes in global demand. This unpredictability makes long-term planning and pricing strategies difficult for manufacturers, potentially squeezing profit margins and deterring investment in new production capacities. Additionally, the high initial capital investment required for installing advanced metal treatment facilities and effluent treatment plants can be a barrier for new entrants and small to medium-sized enterprises, limiting overall market expansion.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations | -1.0% | Global, particularly Europe, North America | Long-term (2025-2033) |

| Volatile Raw Material Prices | -0.8% | Global | Continuous |

| High Capital Investment for Advanced Systems | -0.6% | Developing Economies | Medium-term (2025-2030) |

| Disposal Challenges of Hazardous Waste | -0.5% | Global | Long-term (2026-2033) |

| Economic Downturns and Industrial Slowdown | -0.7% | Global, cyclical | Short-term (cyclical) |

Metal Treatment Chemical Market Opportunities Analysis

The Metal Treatment Chemical market is rich with emerging opportunities, particularly in the development and widespread adoption of green and sustainable chemical solutions. As industries globally intensify their focus on environmental responsibility and carbon footprint reduction, there is a burgeoning demand for bio-based, low-VOC (volatile organic compound), and non-toxic alternatives to traditional metal treatment chemicals. This shift opens avenues for innovation in product formulation and process optimization, allowing companies to differentiate themselves and capture a growing segment of environmentally conscious consumers and businesses. The drive towards a circular economy further encourages the development of chemicals that facilitate recycling and minimize waste generation.

Another significant opportunity lies in the expanding industrial base of emerging economies, particularly in Asia Pacific, Latin America, and parts of Africa. These regions are experiencing rapid urbanization, infrastructure development, and industrialization, leading to increased manufacturing activities across various sectors, including automotive, construction, and general industrial. This growth fuels a natural increase in demand for metal treatment chemicals to protect new assets and ensure the longevity of manufactured goods. Furthermore, the burgeoning field of additive manufacturing (3D printing) presents a unique opportunity, as printed metal parts often require specialized post-treatment chemicals for surface finishing, corrosion protection, and enhancing mechanical properties, creating a niche market for advanced chemical solutions tailored to these innovative processes.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Green and Sustainable Chemicals | +1.5% | Global | Long-term (2025-2033) |

| Growing Industrialization in Emerging Economies | +1.3% | Asia Pacific, Latin America, MEA | Long-term (2025-2033) |

| Technological Advancements in Additive Manufacturing | +1.0% | North America, Europe, East Asia | Medium-term (2026-2032) |

| Increasing Demand for Customized Solutions | +0.8% | Developed Economies | Continuous |

| Research & Development in Nanocoatings and Smart Surfaces | +0.7% | Global, particularly R&D hubs | Long-term (2027-2033) |

Metal Treatment Chemical Market Challenges Impact Analysis

The Metal Treatment Chemical market encounters several persistent challenges that can impede its growth trajectory. One significant hurdle is the complexity and dynamic nature of global regulatory compliance. Manufacturers must navigate a patchwork of environmental, health, and safety regulations that vary significantly by region and country, often requiring substantial investments in R&D and operational adjustments to ensure products meet diverse local standards. The constant evolution of these regulations means continuous monitoring and adaptation, which can be costly and time-consuming, posing a barrier to market entry and expansion for many companies.

Another formidable challenge is the management and disposal of hazardous waste generated during metal treatment processes. Many chemicals used are corrosive, toxic, or environmentally detrimental, necessitating specialized and expensive waste treatment facilities and disposal methods. The increasing public and regulatory scrutiny on industrial waste management places immense pressure on companies to adopt more sustainable practices, which can increase operational costs and complexity. Furthermore, intense competition within the market, coupled with the need for high levels of product performance and consistency, puts pressure on pricing and profit margins. Companies must continuously innovate and differentiate their offerings while maintaining cost-effectiveness, which demands significant investment in R&D and advanced manufacturing capabilities.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex Regulatory Compliance Landscape | -0.9% | Global | Long-term (2025-2033) |

| High Cost of Waste Management and Disposal | -0.7% | Global | Continuous |

| Intense Market Competition and Price Pressure | -0.6% | Global | Continuous |

| Shortage of Skilled Labor and Expertise | -0.5% | Developed Economies | Medium-term (2025-2030) |

| Resistance to Adopting New Technologies | -0.4% | Traditional Industrial Sectors | Long-term (2027-2033) |

Metal Treatment Chemical Market - Updated Report Scope

This comprehensive market research report offers an in-depth analysis of the Metal Treatment Chemical market, providing a detailed overview of its current landscape, historical performance, and future growth projections. The scope encompasses a thorough examination of market dynamics, including key drivers, restraints, opportunities, and challenges influencing the industry. It delves into extensive segmentation analysis by chemical type, application, and end-use industry, providing granular insights into the market's structure and evolving trends across various geographical regions. The report also features a competitive landscape analysis, profiling leading companies and their strategic initiatives, alongside an assessment of emerging technologies and their potential impact on market growth.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 34.8 Billion |

| Market Forecast in 2033 | USD 54.3 Billion |

| Growth Rate | 5.7% |

| Number of Pages | 256 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | BASF SE, Henkel AG & Co. KGaA, The Dow Chemical Company, Chemetall GmbH (BASF Group), PPG Industries Inc., Akzo Nobel N.V., Sherwin-Williams Company, Clariant AG, Solvay S.A., Quaker Chemical Corporation (Quaker Houghton), Covestro AG, Lanxess AG, Croda International Plc, Nippon Paint Holdings Co., Ltd., Axalta Coating Systems, Inc., Hubbard-Hall Inc., McGean-Rohco, Inc., Bulk Chemicals, Inc., Houghton International Inc. (Quaker Houghton), Fuchs Petrolub SE |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Metal Treatment Chemical market is meticulously segmented to provide a granular understanding of its diverse components and drivers. These segmentations allow for a detailed examination of market dynamics across various chemical types, applications, and end-use industries, offering strategic insights into niche markets and high-growth areas. The analysis highlights how different chemical formulations cater to specific industrial needs, from surface preparation to corrosion resistance and aesthetic enhancement. Understanding these segments is crucial for identifying emerging trends, competitive landscapes, and potential investment opportunities within the broader metal treatment chemical ecosystem.

- By Type: Cleaners, Conversion Coatings, Plating Chemicals, Paint Strippers, Lubricants, Passivation Chemicals, Others (e.g., rust removers, descalers).

- By Application: Corrosion Protection, Surface Finishing, Lubrication, Cleaning, Paint Removal, Heat Treatment, Welding, Other Applications (e.g., bonding, sealing).

- By End-Use Industry: Automotive, Aerospace, General Industrial, Construction, Marine, Electronics, Packaging, Healthcare, Heavy Machinery, Energy, Other End-Use Industries (e.g., consumer goods, defense).

Regional Highlights

- Asia Pacific (APAC): Dominates the market due to rapid industrialization, burgeoning automotive manufacturing, significant infrastructure development, and increasing foreign investments in manufacturing hubs like China, India, Japan, and South Korea.

- North America: Exhibits substantial growth driven by technological advancements, strong automotive and aerospace sectors, and a robust focus on high-performance and specialty chemicals, particularly in the United States and Canada.

- Europe: A mature market characterized by stringent environmental regulations driving innovation in green chemistries, a strong automotive industry, and significant investments in advanced manufacturing in countries such as Germany, France, and the UK.

- Latin America: Showing steady growth influenced by expanding manufacturing bases, particularly in automotive and construction sectors in Brazil and Mexico, coupled with increasing industrialization.

- Middle East & Africa (MEA): Emerging as a growing market due to diversifying economies, infrastructure projects, and developing industrial capacities, especially in the GCC countries and South Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Metal Treatment Chemical Market.- BASF SE

- Henkel AG & Co. KGaA

- The Dow Chemical Company

- Chemetall GmbH (BASF Group)

- PPG Industries Inc.

- Akzo Nobel N.V.

- Sherwin-Williams Company

- Clariant AG

- Solvay S.A.

- Quaker Chemical Corporation (Quaker Houghton)

- Covestro AG

- Lanxess AG

- Croda International Plc

- Nippon Paint Holdings Co., Ltd.

- Axalta Coating Systems, Inc.

- Hubbard-Hall Inc.

- McGean-Rohco, Inc.

- Bulk Chemicals, Inc.

- Houghton International Inc. (Quaker Houghton)

- Fuchs Petrolub SE

Frequently Asked Questions

Analyze common user questions about the Metal Treatment Chemical market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the current market size and projected growth rate of the Metal Treatment Chemical market?

The Metal Treatment Chemical market is estimated at USD 34.8 Billion in 2025 and is projected to reach USD 54.3 Billion by 2033, growing at a Compound Annual Growth Rate (CAGR) of 5.7% during the forecast period.

Which factors are primarily driving the growth of the Metal Treatment Chemical market?

Key drivers include the expansion of the automotive and aerospace industries, stringent regulatory standards for material durability, increasing demand for lightweight materials, and robust infrastructure development in emerging economies.

What are the main types of Metal Treatment Chemicals?

The market primarily includes Cleaners, Conversion Coatings, Plating Chemicals, Paint Strippers, Lubricants, and Passivation Chemicals, each serving distinct purposes in metal surface preparation and protection.

How are environmental regulations impacting the Metal Treatment Chemical market?

Environmental regulations are significantly shaping the market by increasing demand for eco-friendly and sustainable chemical solutions, driving R&D into bio-based alternatives, and escalating compliance costs for traditional hazardous chemicals.

Which region holds the largest share in the Metal Treatment Chemical market?

Asia Pacific is currently the largest and fastest-growing region in the Metal Treatment Chemical market, attributed to rapid industrialization, strong manufacturing sector growth, and significant investments in developing economies like China and India.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted