Metal Casting Market

Metal Casting Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704255 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

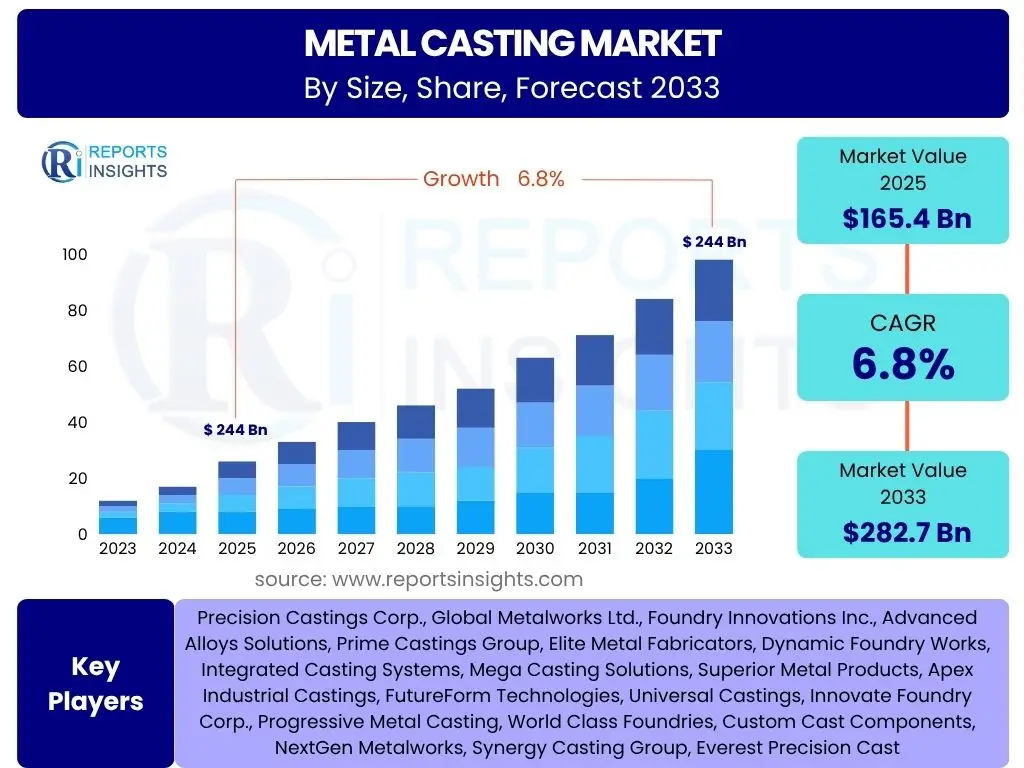

Metal Casting Market Size

According to Reports Insights Consulting Pvt Ltd, The Metal Casting Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 165.4 billion in 2025 and is projected to reach USD 282.7 billion by the end of the forecast period in 2033.

Key Metal Casting Market Trends & Insights

The Metal Casting market is undergoing significant transformation driven by advancements in materials science, manufacturing processes, and increasing demand from various end-use industries. Key trends revolve around the pursuit of lightweighting in automotive and aerospace sectors, the growing adoption of automation and digitalization, and a strong emphasis on sustainable manufacturing practices. Companies are increasingly investing in research and development to enhance the efficiency, precision, and environmental footprint of casting processes, moving towards smarter and more integrated production lines.

Insights into the market indicate a shift towards higher-value, performance-critical castings, particularly those made from advanced alloys such as aluminum and magnesium, due to their strength-to-weight ratio benefits. Furthermore, the integration of simulation software and additive manufacturing technologies is enabling faster prototyping and more complex designs, pushing the boundaries of traditional casting capabilities. The market is also witnessing a consolidation trend, with larger players acquiring specialized foundries to expand their technological capabilities and market reach.

Sustainability and environmental compliance are becoming paramount, driving innovation in energy-efficient furnaces, waste heat recovery systems, and improved recycling of scrap materials. The push for circular economy principles is leading to significant investments in green casting technologies and processes that reduce emissions and material waste. These efforts are not only driven by regulatory pressures but also by corporate responsibility goals and consumer demand for environmentally friendly products.

- Lightweighting initiatives in automotive and aerospace industries.

- Increased adoption of automation, robotics, and Industry 4.0 solutions.

- Growing focus on sustainable and environmentally friendly casting processes.

- Advancements in material science, including high-strength and advanced alloys.

- Integration of simulation software and generative design for optimized casting.

- Shift towards high-precision and complex geometries.

AI Impact Analysis on Metal Casting

The integration of Artificial Intelligence (AI) is fundamentally reshaping the metal casting industry, addressing challenges such as quality control, process optimization, and predictive maintenance. Common user questions often focus on how AI can reduce defects, optimize energy consumption, and improve overall operational efficiency. AI-driven solutions are enabling foundries to move beyond traditional trial-and-error approaches, leading to more predictable and robust manufacturing processes.

Concerns typically revolve around the initial investment costs, the need for skilled personnel to implement and manage AI systems, and data security. However, the expectations for AI's influence are high, particularly concerning its ability to analyze vast amounts of production data in real-time, identify subtle patterns indicative of impending issues, and recommend proactive adjustments. This level of insight was previously unattainable, offering a competitive edge to early adopters.

AI's influence is evident in several key areas, from automating visual inspection of castings for surface defects to optimizing furnace temperatures and melt compositions to achieve desired material properties. Generative design algorithms, powered by AI, are also being employed to create complex, lightweight structures that are inherently suitable for casting, reducing material usage and enhancing performance. This holistic impact on design, production, and quality assurance positions AI as a transformative force within the metal casting domain.

- Enhanced quality control through AI-powered visual inspection systems.

- Optimization of casting parameters and processes via machine learning algorithms.

- Predictive maintenance for casting machinery, minimizing downtime.

- Generative design for complex, lightweight casting structures.

- Improved energy efficiency through AI-driven process optimization.

- Automated defect detection and classification, reducing scrap rates.

Key Takeaways Metal Casting Market Size & Forecast

The Metal Casting market is poised for robust expansion over the forecast period, driven primarily by sustained demand from the automotive, industrial machinery, and construction sectors. A key takeaway is the increasing emphasis on advanced materials and sophisticated casting techniques to meet stringent performance requirements across various applications. The market's growth trajectory is also significantly influenced by emerging economies where industrialization and infrastructure development are creating substantial opportunities for metal casting products.

The forecast highlights a clear trend towards value-added services, including post-casting machining, heat treatment, and surface finishing, as manufacturers seek to offer comprehensive solutions. This integrated approach not only enhances product quality but also streamlines supply chains for end-users. Furthermore, the imperative for environmental sustainability is a defining factor, compelling industry players to invest in green technologies and processes that reduce carbon footprint and waste generation, thereby shaping future market dynamics and competitive landscapes.

Digitalization and automation are identified as critical enablers for future growth, allowing foundries to achieve higher levels of precision, efficiency, and flexibility. The ability to leverage data analytics for process control and predictive insights will differentiate market leaders. Overall, the market is characterized by a balance of traditional manufacturing strengths and an accelerating adoption of cutting-edge technologies, ensuring its continued relevance and expansion in the global industrial landscape.

- Significant growth anticipated, fueled by strong demand from diverse industries.

- Increasing adoption of advanced materials and high-precision casting techniques.

- Emerging economies present substantial growth opportunities.

- Focus on value-added services and integrated solutions to meet customer needs.

- Sustainability initiatives are driving innovation in green casting processes.

- Digitalization and automation are critical for enhancing efficiency and precision.

Metal Casting Market Drivers Analysis

The expansion of the global automotive industry, particularly the rising demand for lightweight and fuel-efficient vehicles, stands as a primary driver for the metal casting market. Modern vehicles increasingly utilize aluminum and magnesium castings for engine blocks, transmission cases, and structural components to reduce overall vehicle weight, directly contributing to improved fuel economy and reduced emissions. This trend is further amplified by the accelerating shift towards electric vehicles (EVs), which also rely heavily on lightweight castings for battery housings, motor components, and structural frames to maximize range and performance.

Rapid urbanization and significant investments in infrastructure development across developing regions are also propelling market growth. Construction projects, from commercial buildings to transportation networks, require a substantial volume of cast metal components for structural elements, plumbing, and various machinery. The industrial machinery sector, encompassing equipment for manufacturing, agriculture, and mining, consistently demands high-strength, durable castings, thereby ensuring a steady base for market consumption. Furthermore, the global energy sector, including renewable energy installations like wind turbines and solar panel structures, necessitates large, complex castings, contributing to specialized market segments.

Technological advancements in casting processes, such as improved die-casting techniques, sand casting automation, and the integration of simulation software, enable the production of more intricate designs with superior material properties. These innovations reduce material waste and energy consumption, making casting a more attractive and cost-effective manufacturing method. The continuous pursuit of higher precision and performance in end-use applications across aerospace and defense also drives the demand for specialized, high-integrity metal castings.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Automotive Industry & EV Adoption | +1.8% | Global, particularly APAC, Europe, North America | Short to Long-term (2025-2033) |

| Infrastructure Development & Urbanization | +1.5% | APAC, Latin America, Middle East & Africa | Medium to Long-term (2027-2033) |

| Demand from Industrial Machinery & Equipment | +1.2% | Global, stable demand | Continuous |

| Technological Advancements in Casting Processes | +1.0% | Global, R&D focused regions | Short to Medium-term (2025-2029) |

| Rising Demand for Lightweight Components | +1.3% | Global, especially developed economies | Short to Long-term (2025-2033) |

Metal Casting Market Restraints Analysis

The metal casting market faces significant challenges from the volatility of raw material prices, particularly for metals like aluminum, copper, and iron. Fluctuations in commodity markets can directly impact production costs, making it difficult for foundries to maintain stable profit margins and competitive pricing. This unpredictability necessitates complex risk management strategies and can deter long-term investment in capacity expansion, especially for smaller and medium-sized enterprises that lack robust hedging mechanisms.

Stringent environmental regulations are another major restraint. Foundries are energy-intensive operations and often generate significant emissions and waste, including hazardous byproducts. Compliance with evolving environmental protection laws, such as those related to air quality, water discharge, and waste disposal, requires substantial capital expenditure on pollution control equipment and sustainable practices. These regulatory burdens can increase operational costs and complexity, particularly in regions with strict environmental enforcement.

The high capital investment required for establishing and modernizing casting facilities poses a considerable barrier to entry and expansion. Advanced machinery, automation systems, and specialized infrastructure demand significant financial outlay, often making it challenging for new players to compete or for existing players to rapidly scale up. Additionally, the metal casting industry often grapples with a shortage of skilled labor, including metallurgists, foundry technicians, and automation experts, which can hinder production efficiency and the adoption of new technologies.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -0.8% | Global | Continuous, Short-term fluctuations |

| Stringent Environmental Regulations | -0.7% | Europe, North America, parts of Asia | Medium to Long-term (2025-2033) |

| High Capital Investment Requirements | -0.6% | Global | Long-term |

| Shortage of Skilled Labor | -0.5% | Developed economies, specific regions | Medium to Long-term (2025-2033) |

| Competition from Alternative Manufacturing Processes | -0.4% | Global, specific high-value components | Medium-term (2027-2033) |

Metal Casting Market Opportunities Analysis

The increasing adoption of Industry 4.0 and smart manufacturing principles presents a significant opportunity for the metal casting market. Integrating advanced technologies such as IoT sensors, AI-driven analytics, and real-time monitoring systems can vastly improve process efficiency, quality control, and predictive maintenance within foundries. This digital transformation enables manufacturers to achieve higher precision, reduce scrap rates, optimize energy consumption, and respond more flexibly to market demands, thereby enhancing their competitive edge and profitability.

The burgeoning demand for recycled metals, driven by sustainability mandates and cost efficiency, offers a substantial growth avenue. Foundries that invest in advanced recycling technologies and processes can capitalize on the availability of secondary raw materials, reducing their reliance on volatile primary metal markets and lowering their environmental footprint. This aligns with global efforts toward a circular economy and positions companies to meet growing customer and regulatory expectations for sustainable production.

Expansion into emerging markets, particularly in Southeast Asia, Africa, and parts of Latin America, where industrialization and infrastructure development are rapidly accelerating, provides untapped potential. These regions are experiencing growth in automotive manufacturing, construction, and general industrial sectors, creating new demand centers for cast components. Furthermore, the development of niche applications in sectors like medical devices, consumer electronics, and specialized machinery, requiring high-precision, custom castings, offers opportunities for diversification and premium product offerings.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Industry 4.0 & Smart Manufacturing Adoption | +1.4% | Global, particularly developed economies | Short to Long-term (2025-2033) |

| Growing Demand for Recycled Metals | +1.1% | Global, strong in Europe & North America | Medium to Long-term (2027-2033) |

| Expansion into Emerging Markets | +0.9% | APAC, Latin America, Middle East & Africa | Medium to Long-term (2027-2033) |

| Additive Manufacturing Integration (Hybrid Processes) | +0.8% | Global, R&D intensive regions | Medium-term (2027-2030) |

| Development of Niche & High-Value Applications | +0.7% | Global, focused on specialized foundries | Continuous |

Metal Casting Market Challenges Impact Analysis

The metal casting industry faces significant challenges related to its energy-intensive nature, particularly in light of rising global energy prices and increased pressure for carbon emission reductions. Foundries rely heavily on electricity and natural gas for melting and heating processes, making them vulnerable to energy market volatility and increasing operational costs. This energy dependency necessitates substantial investment in energy-efficient technologies and alternative energy sources, adding complexity to operational planning and impacting profitability, especially for businesses in regions with high energy costs.

Effective waste management and disposal remain a persistent challenge for metal casting operations. The process generates various waste streams, including sand, slag, dust, and hazardous materials, requiring careful handling and costly disposal or recycling. Compliance with evolving environmental regulations concerning waste reduction and responsible disposal demands continuous innovation and investment in advanced waste treatment and recycling facilities, placing a financial and logistical burden on foundries. Inadequate waste management can also lead to reputational damage and regulatory fines.

Global supply chain disruptions, exemplified by recent events such as the COVID-19 pandemic and geopolitical tensions, pose a significant challenge. These disruptions can lead to shortages of essential raw materials, components, and equipment, causing production delays and increasing procurement costs. The complex, interconnected nature of the global market means that localized issues can have cascading effects, impacting lead times and the reliability of operations worldwide. This necessitates the diversification of supply chains and increased localized sourcing, which can be a complex and costly endeavor for multinational players.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Energy Consumption & Costs | -0.9% | Global, particularly Europe & Asia | Continuous |

| Waste Management & Environmental Compliance | -0.8% | Global, especially developed economies | Long-term |

| Global Supply Chain Disruptions | -0.7% | Global | Short to Medium-term (2025-2027) |

| Intense Competition from Low-Cost Regions | -0.6% | Developed economies | Continuous |

| Technological Obsolescence & Adaptation Speed | -0.5% | Global, R&D focused regions | Medium-term (2027-2030) |

Metal Casting Market - Updated Report Scope

This market research report provides a comprehensive analysis of the Metal Casting Market, offering insights into market size, growth trends, competitive landscape, and strategic opportunities from 2019 to 2033. It details the market's evolution, current dynamics, and future projections, segmenting the market by process, material, and end-use industry, with a thorough regional assessment. The report highlights the impact of key drivers, restraints, opportunities, and challenges, along with the influence of emerging technologies like AI and Industry 4.0 on market trajectory.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 165.4 billion |

| Market Forecast in 2033 | USD 282.7 billion |

| Growth Rate | 6.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Precision Castings Corp., Global Metalworks Ltd., Foundry Innovations Inc., Advanced Alloys Solutions, Prime Castings Group, Elite Metal Fabricators, Dynamic Foundry Works, Integrated Casting Systems, Mega Casting Solutions, Superior Metal Products, Apex Industrial Castings, FutureForm Technologies, Universal Castings, Innovate Foundry Corp., Progressive Metal Casting, World Class Foundries, Custom Cast Components, NextGen Metalworks, Synergy Casting Group, Everest Precision Cast |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Metal Casting market is extensively segmented by process, material, and end-use industry, reflecting the diverse applications and technological nuances within the sector. Each segment plays a crucial role in the overall market dynamics, driven by specific industrial demands and material properties. Understanding these segmentations is vital for stakeholders to identify growth pockets, tailor product offerings, and devise effective market strategies. The intricate interplay between advanced casting processes, specialized materials, and stringent industry requirements defines the competitive landscape and innovation trajectory of the market.

Process segmentation highlights the prevalence of various casting techniques, each suited for particular part complexities, material types, and production volumes. For instance, Die Casting is dominant in high-volume production for automotive and electronics due to its precision and speed, while Investment Casting caters to aerospace and medical industries for intricate designs and high integrity. Material segmentation underscores the shift towards lightweight non-ferrous alloys like aluminum and magnesium, driven by fuel efficiency and performance demands, alongside the consistent demand for traditional ferrous metals in heavy industries. This diverse material landscape necessitates specialized foundry capabilities and expertise.

The end-use industry segmentation showcases the broad applicability of metal castings across critical economic sectors. The Automotive & Transportation segment remains a cornerstone, with evolving vehicle designs and the rise of electric vehicles continuously shaping demand for specialized castings. Industrial Machinery, Construction, and Energy sectors provide stable and growing demand for robust, durable components. The Electrical & Electronics and Medical Devices industries represent high-growth, high-value segments requiring precision and reliability, thereby contributing significantly to market innovation and technological advancement within the metal casting domain.

- By Process:

- Die Casting: Dominant for high-volume, precision parts, favored in automotive and electronics. Includes High-Pressure, Low-Pressure, and Gravity Die Casting.

- Sand Casting: Versatile for various metals and part sizes, widely used for large and complex components in industrial machinery and construction.

- Investment Casting: Known for producing highly accurate, complex parts with excellent surface finish, critical for aerospace, medical, and defense sectors.

- Shell Molding: Offers better dimensional accuracy and surface finish than traditional sand casting, suitable for medium-sized production runs.

- Lost Foam Casting: Ideal for intricate, near-net-shape castings, reducing machining requirements and material waste.

- Continuous Casting: Primarily for producing semi-finished products like billets, blooms, and slabs, serving as raw material for further processing.

- Centrifugal Casting: Used for cylindrical or symmetrical parts like pipes, tubes, and rings, offering high density and purity.

- Others: Encompasses various specialized and emerging casting methods.

- By Material:

- Ferrous Metals: Includes Cast Iron (Gray, Ductile, Malleable) and Cast Steel, prized for strength, durability, and cost-effectiveness in heavy industries.

- Non-Ferrous Metals: Comprises Aluminum Alloys (lightweighting in automotive, aerospace), Copper Alloys (electrical conductivity, corrosion resistance), Magnesium Alloys (ultra-lightweight, high strength-to-weight ratio), Zinc Alloys (die casting, decorative applications), Titanium Alloys (high performance, aerospace, medical), Lead Alloys, Nickel Alloys, and others.

- By End-Use Industry:

- Automotive & Transportation: Major consumer for engine blocks, chassis components, wheels, and electric vehicle parts. Includes Passenger Vehicles, Commercial Vehicles, Electric Vehicles, Aerospace & Defense, and Railways.

- Industrial Machinery: Supplies components for agriculture, construction, textile, and mining equipment, as well as machine tools.

- Construction: Provides castings for pipes, fittings, structural elements, and architectural applications.

- Electrical & Electronics: Used for electrical enclosures, connectors, heat sinks, and various electronic components.

- Energy: Critical for components in oil & gas exploration, power generation (turbines), and renewable energy systems.

- Medical Devices: Demands high-precision, biocompatible castings for surgical instruments and implants.

- Consumer Goods: Applications range from household appliances to recreational equipment.

- Others: Includes marine, defense, and artistic castings.

Regional Highlights

- Asia Pacific (APAC): APAC represents the largest and fastest-growing market for metal casting, primarily driven by robust industrialization, rapid urbanization, and a flourishing automotive manufacturing sector in countries like China, India, Japan, and South Korea. Significant investments in infrastructure development, coupled with a growing middle class, fuel demand for industrial machinery, construction components, and consumer goods. The region benefits from a large labor force and developing manufacturing capabilities, making it a global hub for casting production and consumption.

- North America: The North American market is characterized by a mature industrial base and a strong emphasis on technological advancement and lightweighting. The automotive and aerospace & defense industries are key drivers, demanding high-precision, complex castings. Focus on automation, Industry 4.0 integration, and sustainable manufacturing practices is prominent, positioning the region at the forefront of advanced casting technologies. Increased domestic manufacturing initiatives also contribute to market stability.

- Europe: Europe stands as a significant market, known for its high-quality production, stringent environmental regulations, and focus on innovation. Germany, France, and Italy are key contributors, driven by strong automotive, industrial machinery, and energy sectors. The region is increasingly adopting advanced casting processes and materials, with a strong emphasis on circular economy principles and energy efficiency in manufacturing operations. Demand for specialized and complex castings for high-performance applications is consistently high.

- Latin America: The Latin American metal casting market is witnessing steady growth, particularly in Brazil and Mexico, propelled by expanding automotive production, infrastructure projects, and a developing industrial sector. While still growing, the region faces challenges related to economic volatility and reliance on foreign investments. Opportunities lie in improving manufacturing efficiencies and meeting local demand for basic and semi-complex castings.

- Middle East & Africa (MEA): The MEA region is an emerging market for metal casting, primarily influenced by investments in oil & gas infrastructure, construction, and nascent automotive assembly. Saudi Arabia, UAE, and South Africa are leading the regional growth. Diversification efforts away from oil dependency are expected to stimulate demand for industrial and manufacturing components. The region presents long-term growth potential as industrialization progresses.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Metal Casting Market.- Precision Castings Corp.

- Global Metalworks Ltd.

- Foundry Innovations Inc.

- Advanced Alloys Solutions

- Prime Castings Group

- Elite Metal Fabricators

- Dynamic Foundry Works

- Integrated Casting Systems

- Mega Casting Solutions

- Superior Metal Products

- Apex Industrial Castings

- FutureForm Technologies

- Universal Castings

- Innovate Foundry Corp.

- Progressive Metal Casting

- World Class Foundries

- Custom Cast Components

- NextGen Metalworks

- Synergy Casting Group

- Everest Precision Cast

Frequently Asked Questions

What is the projected growth rate for the Metal Casting Market?

The Metal Casting Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, driven by increasing demand across various industries and technological advancements.

Which factors are primarily driving the Metal Casting Market growth?

Key drivers include the global automotive industry's demand for lightweight components, significant infrastructure development, growth in industrial machinery, and advancements in casting technologies leading to more efficient and precise production.

How is Artificial Intelligence impacting the Metal Casting industry?

AI is transforming the industry by enabling enhanced quality control through automated inspection, optimizing casting processes for efficiency, facilitating predictive maintenance for machinery, and supporting generative design for complex, lightweight components.

Which region dominates the Metal Casting Market?

The Asia Pacific (APAC) region currently dominates the Metal Casting Market due to rapid industrialization, extensive automotive manufacturing, and significant infrastructure development, particularly in countries like China and India.

What are the main challenges faced by the Metal Casting Market?

Major challenges include high energy consumption and fluctuating costs, stringent environmental regulations requiring substantial compliance investments, and disruptions in global supply chains that impact raw material availability and logistics.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted