Casting and Splinting Market

Casting and Splinting Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704185 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Casting and Splinting Market Size

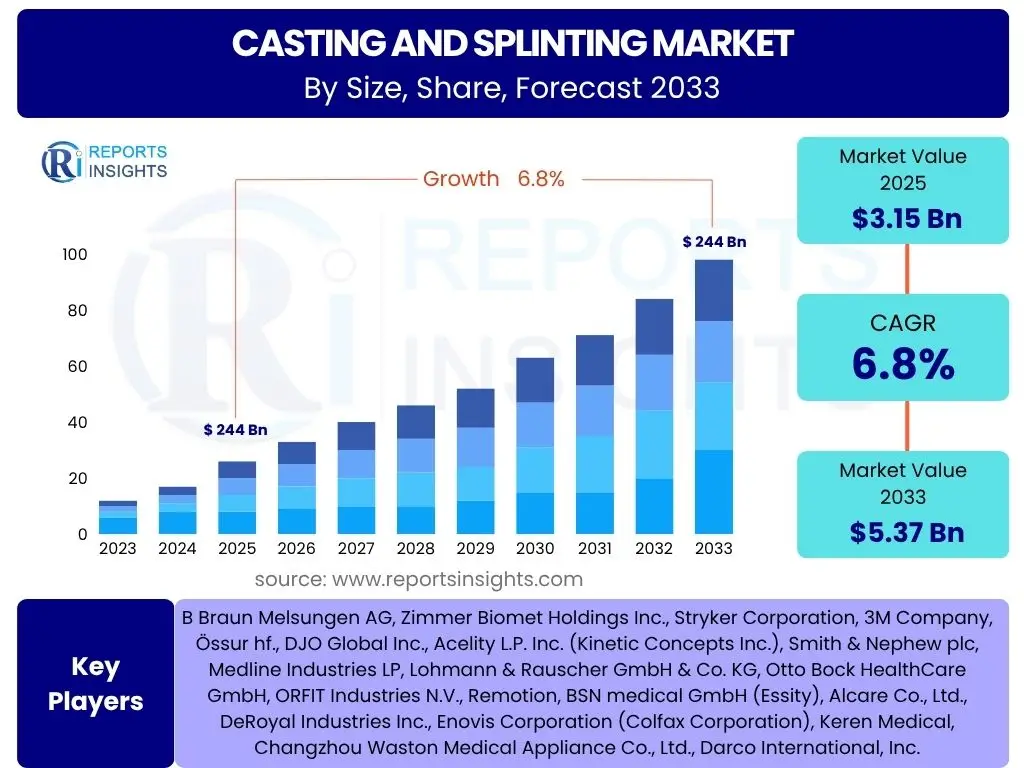

According to Reports Insights Consulting Pvt Ltd, The Casting and Splinting Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 3.15 Billion in 2025 and is projected to reach USD 5.37 Billion by the end of the forecast period in 2033.

Key Casting and Splinting Market Trends & Insights

The Casting and Splinting market is undergoing significant transformation driven by advancements in material science, increased focus on patient comfort, and the integration of digital technologies. User inquiries often highlight a strong interest in how traditional methods are evolving with modern innovations, emphasizing a move towards more ergonomic, lightweight, and efficient solutions. This includes a growing preference for synthetic materials over traditional plaster, owing to their enhanced durability, reduced weight, and superior water resistance. Furthermore, the market is witnessing an emphasis on custom-fit solutions, facilitated by advanced imaging and manufacturing techniques, ensuring better patient outcomes and reduced recovery times.

Another prominent trend observed is the expanding application of casting and splinting products beyond conventional fracture management to specialized areas such as sports medicine, rehabilitation, and preventative care. There is also an increasing demand for sustainable and biodegradable options, reflecting a broader industry shift towards environmental responsibility. Telemedicine and remote monitoring are influencing follow-up care, potentially reducing the need for repeated in-person clinic visits and optimizing patient management. These trends collectively indicate a dynamic market focused on innovation, patient-centricity, and operational efficiency.

- Shift towards advanced synthetic and thermoplastic materials for enhanced durability and comfort.

- Rising adoption of 3D printing and digital scanning for customized casting and splinting solutions.

- Increased demand for lightweight, breathable, and water-resistant products.

- Growing focus on eco-friendly and biodegradable casting materials.

- Expansion of applications in sports medicine, physical therapy, and emergency medical services.

- Integration of smart technologies for monitoring patient recovery and compliance.

AI Impact Analysis on Casting and Splinting

The integration of Artificial intelligence (AI) is poised to revolutionize the Casting and Splinting market, addressing common user concerns regarding precision, efficiency, and personalized patient care. Users are keen to understand how AI can improve diagnostic accuracy, optimize the fitting process, and enhance post-treatment rehabilitation. AI's capabilities in analyzing medical images, such as X-rays and MRI scans, can lead to more precise diagnoses of musculoskeletal injuries, guiding the optimal selection and application of casting or splinting. This reduces the margin of error and ensures that treatment protocols are tailored specifically to the individual's anatomy and injury severity, moving beyond a one-size-fits-all approach.

Furthermore, AI algorithms can process patient data to predict healing timelines and identify potential complications, allowing for proactive adjustments to treatment plans. In terms of manufacturing, AI-driven design software can facilitate the creation of highly customized casts and splints for 3D printing, considering specific patient contours and pressure points to minimize discomfort and improve efficacy. This level of personalization, coupled with the potential for AI-powered remote monitoring of recovery progress, promises to significantly enhance patient experience and outcomes, making the healing process more efficient and less burdensome. The adoption of AI is expected to streamline workflows for healthcare providers and enable a new era of precision orthotics.

- Enhanced diagnostic precision through AI-powered image analysis for musculoskeletal injuries.

- Optimization of cast and splint design via AI algorithms for custom-fit solutions.

- Predictive analytics for healing progression and complication risk assessment in rehabilitation.

- Integration of AI in robotic systems for automated or assisted application of casts and splints.

- Development of smart casts with AI capabilities for real-time monitoring of biomechanical data.

- Streamlined supply chain and inventory management for casting materials using AI forecasts.

Key Takeaways Casting and Splinting Market Size & Forecast

The Casting and Splinting market is projected for robust growth, driven primarily by the global increase in orthopedic injuries, an expanding elderly population prone to falls and fractures, and a surge in sports-related trauma. Users frequently inquire about the underlying factors contributing to this growth and where the most significant investment opportunities lie. The market’s upward trajectory is underpinned by continuous advancements in material science, which enable the development of more effective, lighter, and comfortable products that enhance patient compliance and accelerate recovery. This technological evolution extends to manufacturing processes, with innovations like 3D printing allowing for unprecedented levels of customization.

Significant opportunities are emerging from the adoption of advanced materials such as fiberglass, thermoplastics, and various synthetic composites, which offer superior performance characteristics compared to traditional plaster. Furthermore, the increasing penetration of healthcare services in developing economies and rising awareness about proper post-injury care are contributing factors to market expansion. The focus on patient-centric care models, which prioritize comfort, usability, and reduced recovery times, is guiding product development and market strategies. This suggests that stakeholders should prioritize research and development into innovative materials, personalized solutions, and digital integration to capitalize on the anticipated market growth.

- Consistent market expansion fueled by rising global incidence of orthopedic injuries and chronic conditions.

- Strong demand for advanced synthetic materials offering lightweight, durable, and water-resistant properties.

- Increasing adoption of personalized and custom-fitted casting solutions via digital technologies.

- Significant growth opportunities in emerging economies due to improving healthcare infrastructure.

- Emphasis on patient comfort, reduced immobilization time, and quicker recovery driving product innovation.

Casting and Splinting Market Drivers Analysis

The Casting and Splinting market is significantly propelled by several key drivers, most notably the escalating global incidence of fractures and musculoskeletal injuries. This rise is attributable to an aging global population, which is more susceptible to bone fragility conditions like osteoporosis, leading to higher rates of falls and fractures. Concurrently, an increase in sports participation and road accidents globally contributes substantially to the volume of injuries requiring immobilization, thus driving demand for casting and splinting products. The expanding availability and accessibility of healthcare services worldwide, especially in developing regions, further translates into a greater number of diagnosed and treated orthopedic conditions, directly boosting market growth.

Technological advancements in material science and manufacturing processes also act as a crucial driver. The shift from conventional plaster-based products to advanced synthetic and thermoplastic materials has revolutionized casting and splinting by offering superior properties such as lightweight design, enhanced durability, breathability, and water resistance. These innovations improve patient comfort and compliance, leading to better treatment outcomes. Moreover, the growing focus on rapid recovery and improved patient mobility necessitates more sophisticated and customizable immobilization solutions, pushing manufacturers to innovate and introduce advanced products into the market. This ongoing evolution in product offerings is a strong catalyst for market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Incidence of Fractures & Orthopedic Injuries | +1.2% | Global | 2025-2033 |

| Aging Global Population | +1.0% | North America, Europe, Asia Pacific | 2025-2033 |

| Technological Advancements in Materials | +0.8% | Global | 2025-2033 |

| Growing Participation in Sports Activities | +0.7% | North America, Europe, Asia Pacific | 2025-2033 |

| Rising Awareness about Advanced Fracture Management | +0.5% | Emerging Economies | 2027-2033 |

| Increasing Healthcare Expenditure and Infrastructure Development | +0.6% | Asia Pacific, Latin America, MEA | 2025-2033 |

Casting and Splinting Market Restraints Analysis

Despite robust growth prospects, the Casting and Splinting market faces several significant restraints that could impede its expansion. One primary concern is the relatively high cost associated with advanced casting and splinting materials, particularly synthetic and customized 3D-printed solutions, compared to traditional plaster of Paris. This cost disparity can be a deterrent for healthcare providers in resource-constrained settings or for patients with limited insurance coverage, leading to a preference for more economical, albeit less advanced, options. Additionally, the lack of adequate reimbursement policies for innovative casting technologies in some regions further exacerbates this issue, creating barriers to their widespread adoption and limiting market penetration.

Another restraint stems from the availability of alternative treatment modalities, such as external fixators, internal fixation devices, and non-surgical pain management techniques, which can sometimes be preferred for certain types of fractures or injuries. While casting and splinting remain fundamental, advancements in these alternatives provide physicians with broader options, potentially reducing the reliance on external immobilization in specific cases. Furthermore, environmental concerns related to the disposal of non-biodegradable synthetic casting materials are emerging as a challenge. The waste generated by these products necessitates specific waste management protocols, adding to healthcare operational costs and posing an ecological concern that could influence future market dynamics and product development strategies towards more sustainable alternatives.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Advanced Materials | -0.9% | Global, particularly Emerging Economies | 2025-2033 |

| Availability of Alternative Treatment Modalities | -0.7% | North America, Europe | 2025-2030 |

| Lack of Adequate Reimbursement Policies | -0.6% | Specific Countries within APAC, LATAM | 2025-2033 |

| Stringent Regulatory Approval Processes | -0.5% | North America, Europe | 2025-2029 |

| Environmental Concerns regarding Non-Biodegradable Waste | -0.4% | Global | 2028-2033 |

Casting and Splinting Market Opportunities Analysis

The Casting and Splinting market presents substantial opportunities driven by evolving technological landscapes and unmet patient needs. A key area of growth lies in the expansion of 3D printing and digital scanning technologies, which enable the creation of highly customized, lightweight, and breathable casts and splints. This personalization improves patient comfort, reduces skin complications, and allows for more precise immobilization, presenting a significant competitive advantage. As these technologies become more accessible and cost-effective, their adoption is expected to surge, particularly in specialized orthopedic clinics and trauma centers seeking to offer superior patient care. This offers manufacturers an avenue to develop innovative design software and materials compatible with additive manufacturing processes.

Another prominent opportunity resides in the burgeoning demand for eco-friendly and biodegradable casting materials. With increasing global awareness regarding environmental sustainability, there is a growing preference among healthcare providers and patients for products that minimize ecological footprint. Research and development into plant-based polymers, compostable composites, and other sustainable alternatives can open new market segments and enhance brand reputation. Furthermore, the rising prevalence of chronic conditions requiring prolonged immobilization, such as diabetic foot ulcers or certain neurological disorders, creates a continuous demand for advanced splinting solutions that offer comfort and long-term support. Lastly, expanding healthcare infrastructure and rising disposable incomes in emerging economies offer fertile ground for market penetration and growth, particularly for affordable yet high-quality products.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Adoption of 3D Printing for Customization | +1.3% | North America, Europe, Asia Pacific | 2025-2033 |

| Development of Biodegradable and Sustainable Materials | +1.1% | Global | 2027-2033 |

| Untapped Market Potential in Emerging Economies | +0.9% | Asia Pacific, Latin America, MEA | 2025-2033 |

| Rise in Home Healthcare and Remote Patient Monitoring | +0.8% | North America, Europe | 2026-2033 |

| Strategic Collaborations and Partnerships | +0.6% | Global | 2025-2031 |

| Increasing demand for Waterproof and Lightweight Casts | +0.7% | Global | 2025-2033 |

Casting and Splinting Market Challenges Impact Analysis

The Casting and Splinting market encounters several notable challenges that necessitate strategic navigation for sustained growth. One significant hurdle is the lack of standardization in casting and splinting techniques and materials across different healthcare systems and regions. This variability can lead to inconsistent patient outcomes, difficulty in training healthcare professionals, and complexities in regulatory compliance for manufacturers. Achieving global or even regional consensus on best practices and material specifications remains an ongoing challenge, potentially slowing down the adoption of new, advanced products that do not fit existing frameworks. Furthermore, the specialized skills required for proper application and removal of casts and splints, particularly for complex fractures, pose a training burden and can lead to complications if not executed correctly.

Another substantial challenge is managing the supply chain volatility for raw materials used in synthetic casts and splints. Fluctuations in the cost and availability of petroleum-based polymers and other chemical components can impact manufacturing costs and product pricing, subsequently affecting market accessibility and profitability. Moreover, intense market competition, characterized by the presence of numerous regional and international players, leads to pricing pressures and a continuous need for product differentiation. This competitive landscape demands consistent innovation, significant investment in research and development, and effective marketing strategies to maintain market share. Lastly, the increasing concern over environmental impact from non-biodegradable products and the need for sustainable alternatives presents both a challenge for existing product lines and an opportunity for innovation, but the transition can be costly and technically demanding.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Lack of Standardization in Application Techniques | -0.8% | Global | 2025-2033 |

| Supply Chain Volatility for Raw Materials | -0.7% | Global | 2025-2030 |

| Intense Market Competition and Pricing Pressures | -0.6% | Global | 2025-2033 |

| Skilled Professional Shortage for Complex Cases | -0.5% | North America, Europe | 2025-2033 |

| Adoption Barriers for High-Cost Advanced Technologies | -0.4% | Emerging Economies | 2025-2033 |

Casting and Splinting Market - Updated Report Scope

This comprehensive market research report on the Casting and Splinting market provides an in-depth analysis of current market dynamics, emerging trends, competitive landscape, and future growth projections. It covers a detailed segmentation analysis, regional insights, and profiles of key industry players, offering a holistic view of the market's potential and challenges. The report aims to assist stakeholders in making informed strategic decisions by delivering actionable insights derived from extensive primary and secondary research. It encompasses both historical data and future forecasts, allowing for a thorough understanding of market evolution and anticipated trajectory.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.15 Billion |

| Market Forecast in 2033 | USD 5.37 Billion |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 245 |

| Key Trends | >|

| Segments Covered | >|

| Key Companies Covered | B Braun Melsungen AG, Zimmer Biomet Holdings Inc., Stryker Corporation, 3M Company, Össur hf., DJO Global Inc., Acelity L.P. Inc. (Kinetic Concepts Inc.), Smith & Nephew plc, Medline Industries LP, Lohmann & Rauscher GmbH & Co. KG, Otto Bock HealthCare GmbH, ORFIT Industries N.V., Remotion, BSN medical GmbH (Essity), Alcare Co., Ltd., DeRoyal Industries Inc., Enovis Corporation (Colfax Corporation), Keren Medical, Changzhou Waston Medical Appliance Co., Ltd., Darco International, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Casting and Splinting market is intricately segmented across various dimensions, including product type, material, application, and end-use, providing a granular view of its diverse components and their respective contributions to market growth. This segmentation helps in identifying specific areas of high demand, technological shifts, and emerging preferences, enabling stakeholders to tailor their strategies effectively. The product segmentation differentiates between casting products, which are typically used for complete immobilization, and splinting products, designed for partial or temporary immobilization, both further subdivided into various forms and accessories.

Material segmentation highlights the transition from traditional plaster to advanced synthetic, thermoplastic, and emerging biodegradable options, each offering distinct advantages in terms of weight, durability, and patient comfort. Application segmentation covers a broad spectrum from acute fracture management and orthopedic deformity correction to specialized uses in sports medicine and rehabilitation, reflecting the versatility of these products. Finally, the end-use segmentation categorizes the market by the primary healthcare settings where these products are utilized, such as hospitals, orthopedic clinics, and homecare, indicating the varying demands and service models prevalent across the healthcare continuum. This comprehensive segmentation underscores the multifaceted nature of the market and the diverse needs it addresses.

- By Product: Casting Products (Casting Tapes, Casting Accessories), Splinting Products (Pre-fabricated Splints, Customizable Splints)

- By Material: Fiberglass, Plaster of Paris, Thermoplastics, Polyester, Others (e.g., bio-degradable polymers)

- By Application: Fracture Management, Orthopedic Deformity Correction, Trauma and Sports Injuries, Rehabilitation, Other Applications

- By End-Use: Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers (ASCs), Specialty Clinics, Homecare Settings

- By Region: North America, Europe, Asia Pacific (APAC), Latin America, Middle East & Africa (MEA)

Regional Highlights

- North America: Expected to maintain a dominant market share due to advanced healthcare infrastructure, high incidence of sports injuries, and rapid adoption of technologically advanced products. Strong presence of key market players and favorable reimbursement policies also contribute to its leading position.

- Europe: A significant market driven by an aging population, increasing prevalence of orthopedic conditions, and a strong focus on patient-centric care. Germany, UK, and France are key contributors, investing in innovative materials and customized solutions.

- Asia Pacific (APAC): Projected to exhibit the highest growth rate during the forecast period. This growth is fueled by improving healthcare access, rising disposable incomes, increasing awareness about advanced treatments, and a large patient pool, particularly in countries like China and India.

- Latin America: Showing steady growth due to expanding healthcare expenditure and increasing demand for orthopedic care. Brazil and Mexico are emerging as key markets within the region.

- Middle East & Africa (MEA): Expected to experience moderate growth, driven by developing healthcare infrastructure, increasing medical tourism, and a growing incidence of injuries.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Casting and Splinting Market.- B Braun Melsungen AG

- Zimmer Biomet Holdings Inc.

- Stryker Corporation

- 3M Company

- Össur hf.

- DJO Global Inc.

- Acelity L.P. Inc. (Kinetic Concepts Inc.)

- Smith & Nephew plc

- Medline Industries LP

- Lohmann & Rauscher GmbH & Co. KG

- Otto Bock HealthCare GmbH

- ORFIT Industries N.V.

- Remotion

- BSN medical GmbH (Essity)

- Alcare Co., Ltd.

- DeRoyal Industries Inc.

- Enovis Corporation (Colfax Corporation)

- Keren Medical

- Changzhou Waston Medical Appliance Co., Ltd.

- Darco International, Inc.

Frequently Asked Questions

What is the projected growth rate for the Casting and Splinting Market?

The Casting and Splinting Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, reaching an estimated USD 5.37 Billion by 2033.

What are the key materials driving innovation in this market?

Key materials driving innovation include advanced synthetic fibers (like fiberglass and polyester), thermoplastics for custom molding, and emerging biodegradable polymers, offering benefits such as lightweight design, durability, and patient comfort.

How is AI impacting the Casting and Splinting industry?

AI is impacting the industry by enhancing diagnostic precision, optimizing custom cast and splint design via 3D printing, enabling predictive analytics for healing, and potentially integrating into robotic assistance for application and remote monitoring.

Which region is expected to lead the Casting and Splinting market?

North America is anticipated to maintain its dominant market share due to its advanced healthcare infrastructure, high incidence of injuries, and rapid adoption of technologically advanced medical solutions.

What are the main challenges faced by the Casting and Splinting market?

The primary challenges include the high cost of advanced materials, lack of standardization in application techniques, supply chain volatility for raw materials, and intense market competition leading to pricing pressures.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted