Testing Equipment for Semiconductor Market

Testing Equipment for Semiconductor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700992 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

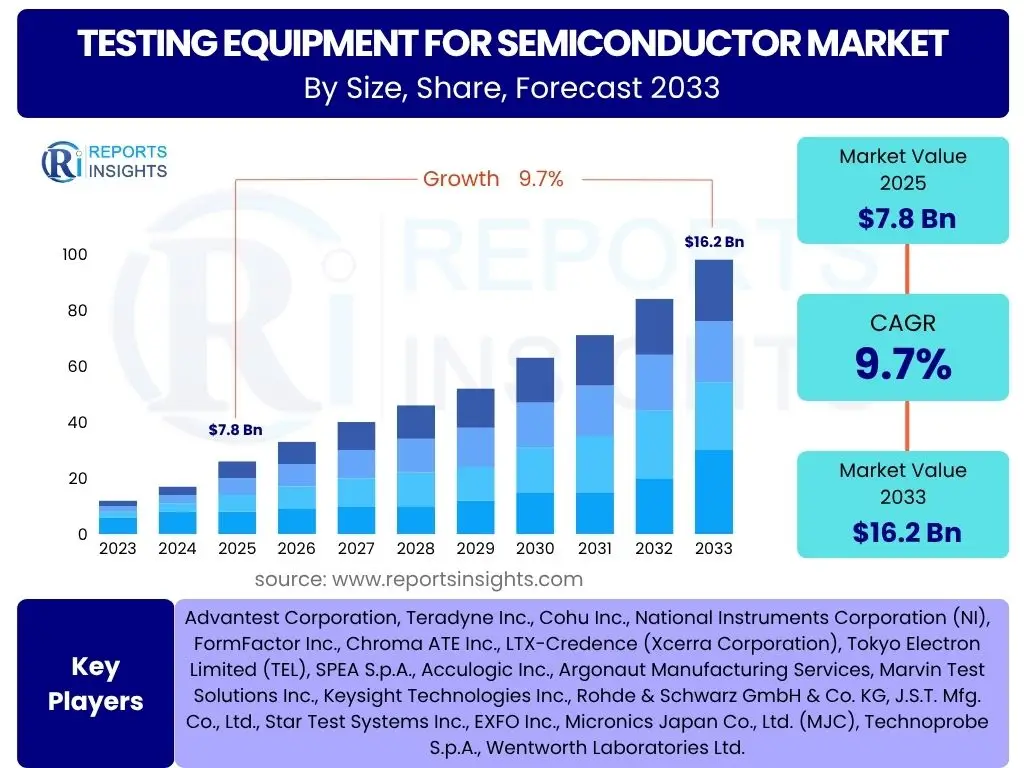

Testing Equipment for Semiconductor Market Size

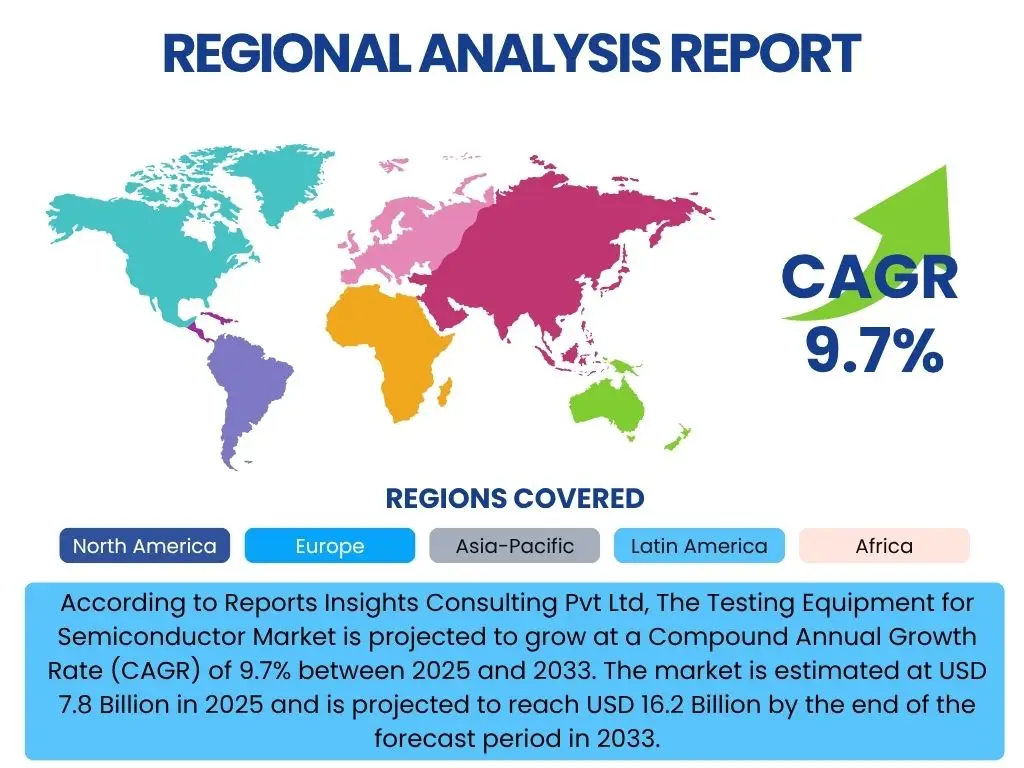

According to Reports Insights Consulting Pvt Ltd, The Testing Equipment for Semiconductor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.7% between 2025 and 2033. The market is estimated at USD 7.8 Billion in 2025 and is projected to reach USD 16.2 Billion by the end of the forecast period in 2033.

Key Testing Equipment for Semiconductor Market Trends & Insights

The Testing Equipment for Semiconductor Market is undergoing significant transformation, driven by an accelerating pace of technological innovation within the semiconductor industry. Users frequently inquire about the impact of advanced chip designs, the proliferation of AI and IoT devices, and the increasing demand for high-performance computing on test methodologies. A notable trend is the move towards more comprehensive and integrated testing solutions that can handle the complexity of heterogeneous integration and advanced packaging techniques, such as chiplets and 3D stacking. This necessitates equipment capable of higher parallelism, greater accuracy, and reduced test time, while also supporting diverse testing protocols across various semiconductor types, from memory to logic and mixed-signal components.

Another prominent insight revolves around the growing emphasis on automation and predictive analytics in testing. As manufacturing volumes increase and cycle times shorten, there is an imperative to reduce human intervention and leverage data for proactive maintenance and yield optimization. This includes the integration of robotics for automated material handling and the deployment of sophisticated software for test data analysis, fault localization, and process improvement. Furthermore, the industry is witnessing a shift towards "test-in-design" and "design-for-testability" principles, where testing considerations are incorporated much earlier in the product development lifecycle, aiming to enhance efficiency and reduce overall costs. This proactive approach helps mitigate risks associated with complex chip architectures and accelerates time-to-market for new semiconductor devices.

The rapid expansion of end-use applications, particularly in automotive electronics, 5G infrastructure, and data centers, is also shaping market trends. Each of these sectors imposes unique and stringent testing requirements, from reliability and safety in automotive to high-speed data integrity in 5G and data centers. Consequently, there is a rising demand for specialized test equipment that can perform robust functional, parametric, and burn-in tests under diverse environmental conditions. The ongoing geopolitical shifts and supply chain reconfigurations are additionally compelling semiconductor manufacturers to invest in localized production and testing capabilities, fostering regional market growth and technological advancements.

- Increased demand for advanced packaging and heterogeneous integration testing.

- Shift towards higher parallelism and multi-site testing for efficiency.

- Growing adoption of automation and robotics in test handling.

- Integration of advanced data analytics for yield improvement and predictive maintenance.

- Emphasis on "test-in-design" and "design-for-testability" methodologies.

- Surge in demand from automotive, 5G, and data center applications.

AI Impact Analysis on Testing Equipment for Semiconductor

Common user inquiries concerning AI's influence on the Testing Equipment for Semiconductor market frequently focus on how artificial intelligence can optimize test processes, enhance data analysis, and improve decision-making. AI is revolutionizing semiconductor testing by enabling smarter, more efficient, and cost-effective validation of complex integrated circuits. It is particularly impactful in areas like adaptive testing, where AI algorithms can learn from test results in real-time to adjust test parameters, skip redundant tests, or focus on areas with higher defect probabilities. This intelligent optimization significantly reduces overall test time and costs, addressing a critical bottleneck in semiconductor manufacturing.

Furthermore, AI-driven analytics are transforming how test data is interpreted and utilized. Traditional data analysis methods often struggle with the sheer volume and complexity of data generated during semiconductor testing. AI, through machine learning and deep learning models, can identify subtle patterns, correlations, and anomalies that might elude human engineers. This capability supports predictive failure analysis, root cause identification, and proactive quality control, leading to improved yield management and enhanced product reliability. The ability of AI to process vast datasets quickly also facilitates faster design iterations and more informed decisions regarding process improvements.

The long-term expectations for AI in this domain include the development of fully autonomous test systems and self-optimizing test flows. Users anticipate that AI will enable systems to perform self-calibration, fault diagnosis, and even self-repair, further minimizing downtime and operational expenses. AI's role in advancing simulation and virtual testing environments is also a key area of interest, allowing for more comprehensive validation before physical prototypes are even produced. This integration of AI across the entire test continuum promises a significant leap in efficiency, precision, and cost-effectiveness for the semiconductor industry.

- Optimization of test sequences and reduction of test time through adaptive learning.

- Enhanced fault detection and diagnosis via advanced pattern recognition in test data.

- Predictive maintenance for test equipment, minimizing downtime.

- Improved yield management through AI-driven anomaly detection and root cause analysis.

- Development of intelligent test platforms capable of autonomous decision-making.

- Facilitation of complex chip validation, including those designed for AI/ML applications.

Key Takeaways Testing Equipment for Semiconductor Market Size & Forecast

Analysis of common user questions regarding the Testing Equipment for Semiconductor market size and forecast reveals a strong interest in understanding the core growth catalysts, the segments poised for the most significant expansion, and the regional dynamics driving market evolution. A primary takeaway is the indispensable role of robust testing in enabling the continuous innovation within the semiconductor industry, particularly as chip complexity escalates with advancements like AI accelerators, IoT devices, and 5G communication modules. The forecast projects substantial growth, underpinned by the increasing demand for semiconductors across diverse end-use applications, which in turn necessitates more sophisticated and efficient testing solutions throughout the entire product lifecycle.

Another critical insight is the bifurcation of market growth drivers, encompassing both technological imperatives and economic expansion. Technologically, the shift towards higher transistor densities, advanced packaging solutions (e.g., 3D ICs, SiP), and specialized materials (e.g., SiC, GaN) directly translates into a requirement for new test methodologies and equipment capabilities. Economically, the global digital transformation, characterized by pervasive connectivity and data processing, fuels the overall demand for semiconductors, thereby creating a sustained need for testing equipment investments. The market's resilience is further highlighted by ongoing investments in R&D by leading players to develop next-generation test platforms that can address future challenges, such as quantum computing and neuromorphic chips.

Finally, the market forecast underscores the continued dominance of the Asia Pacific region, driven by its extensive semiconductor manufacturing ecosystem and significant capital expenditures in new fabs. However, North America and Europe are expected to maintain strong positions through their innovation in advanced research and development, particularly for high-value test solutions. The competitive landscape is characterized by continuous innovation, strategic partnerships, and mergers & acquisitions aimed at expanding product portfolios and geographic reach. Overall, the market is set for sustained expansion, propelled by the relentless evolution of semiconductor technology and its pervasive integration into nearly every aspect of modern life.

- Market growth primarily driven by escalating semiconductor complexity and demand from emerging technologies like AI, IoT, and 5G.

- Advanced packaging and heterogeneous integration are key technological drivers necessitating new test paradigms.

- Asia Pacific remains the largest and fastest-growing region due to high manufacturing capacity.

- Continuous R&D investments by market players are crucial for developing future-proof test solutions.

- The automotive, data center, and consumer electronics segments are major end-use application contributors to market expansion.

Testing Equipment for Semiconductor Market Drivers Analysis

The Testing Equipment for Semiconductor Market is propelled by several robust drivers, primarily stemming from the relentless pace of innovation within the semiconductor industry itself. The increasing complexity of integrated circuits, characterized by miniaturization, higher transistor densities, and the integration of diverse functionalities onto single chips, necessitates more sophisticated and accurate testing. This complexity extends to advanced packaging technologies like chiplets, System-in-Package (SiP), and 3D stacking, which demand novel test methods to ensure reliability and performance. As chips become more intricate, the demand for Automated Test Equipment (ATE) capable of comprehensive functional, parametric, and structural testing across multiple domains intensifies, driving market expansion.

Furthermore, the explosive growth of emerging technologies such as Artificial Intelligence (AI), 5G communication, the Internet of Things (IoT), and high-performance computing (HPC) significantly fuels the demand for semiconductor devices. Each of these applications requires specialized chips with stringent performance, power efficiency, and reliability specifications. For instance, AI processors demand extensive functional and power integrity testing, while 5G RF front-ends require precise high-frequency testing. This pervasive integration of semiconductors into critical infrastructure and consumer electronics mandates rigorous quality assurance, directly translating into increased investments in advanced testing equipment. The expansion of electric vehicles and autonomous driving also adds a layer of safety-critical testing requirements, further bolstering market growth.

Another significant driver is the global trend of increased capital expenditure by semiconductor manufacturers (IDMs and Foundries) and Outsourced Semiconductor Assembly and Test (OSAT) companies. To keep pace with demand and technological advancements, these entities are continuously investing in new fabs and expanding existing facilities. These investments inherently include the procurement of cutting-edge testing equipment to ensure high yields and product quality at scale. Government initiatives and incentives in various regions, aimed at bolstering domestic semiconductor manufacturing capabilities, also contribute to this capital expenditure, thereby creating a favorable environment for the testing equipment market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Semiconductor Device Complexity and Miniaturization | +1.5-2.0% | Global, particularly Asia Pacific (Taiwan, South Korea) and North America | Short to Long-term (2025-2033) |

| Proliferation of AI, 5G, IoT, and High-Performance Computing | +1.2-1.8% | Global, strong in North America, Europe, and Asia Pacific | Short to Medium-term (2025-2029) |

| Rising Capital Expenditure in New Fabs and OSAT Facilities | +1.0-1.5% | Asia Pacific (China, Taiwan), North America, Europe | Medium to Long-term (2027-2033) |

| Growth in Automotive Electronics and Electric Vehicles | +0.8-1.2% | Europe, North America, Japan, China | Medium to Long-term (2026-2033) |

Testing Equipment for Semiconductor Market Restraints Analysis

Despite robust growth drivers, the Testing Equipment for Semiconductor Market faces several notable restraints that could temper its expansion. One significant challenge is the high capital expenditure required for advanced testing equipment. Leading-edge ATE systems, handlers, and probers are technologically complex and command substantial prices, representing a significant upfront investment for semiconductor manufacturers and OSATs. This high cost can act as a barrier to entry for smaller players or limit the pace of technology upgrades, especially in economically sensitive periods. The need for continuous reinvestment in newer generations of equipment to keep pace with evolving chip designs further exacerbates this financial burden.

Another restraint is the extended product lifecycle and depreciation of existing equipment. Semiconductor test equipment is designed for durability and a long operational lifespan, which means replacement cycles can be quite long. While beneficial for the initial investors, it can limit the recurring revenue opportunities for equipment manufacturers. Furthermore, the specialized nature of these machines often leads to a limited customer base, making the market susceptible to the investment cycles and production fluctuations of a relatively small number of large semiconductor companies. This can create periods of slower demand for new equipment, even if the underlying semiconductor market is growing.

Moreover, geopolitical tensions and supply chain vulnerabilities pose considerable risks. Restrictions on technology transfer and export controls can disrupt the flow of critical components or finished equipment, impacting manufacturing and delivery schedules. The intricate global supply chain for high-precision components required for test equipment makes it susceptible to disruptions from natural disasters, pandemics, or trade disputes. Such disruptions can lead to increased lead times, higher costs, and uncertainty for both equipment manufacturers and their customers, thereby restraining market growth by delaying new investments and deployments.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure and Long Product Lifecycles | -0.7-1.0% | Global, affects emerging economies more significantly | Long-term (2025-2033) |

| Economic Downturns and Cyclicality of Semiconductor Industry | -0.5-0.8% | Global | Short to Medium-term (Periodic) |

| Geopolitical Tensions and Supply Chain Disruptions | -0.4-0.6% | Global, particularly impacting US-China trade routes | Short to Medium-term (Ongoing) |

Testing Equipment for Semiconductor Market Opportunities Analysis

The Testing Equipment for Semiconductor Market is ripe with opportunities, particularly stemming from the continuous evolution of semiconductor technology and the emergence of new application areas. The increasing adoption of advanced packaging technologies, such as Chiplets, System-in-Package (SiP), and Fan-Out Wafer-Level Packaging (FOWLP), presents a significant growth avenue. These packaging methods require integrated test solutions that can handle multi-die architectures and complex interconnections, moving beyond traditional single-die testing. Developing specialized equipment and software for these highly integrated and heterogeneous systems offers substantial revenue potential for market players. This shift necessitates innovation in wafer-level testing, known good die (KGD) testing, and post-assembly functional verification.

Another major opportunity lies in the burgeoning market for specialized semiconductors like Silicon Carbide (SiC) and Gallium Nitride (GaN), crucial for power electronics and high-frequency applications. These wide-bandgap (WBG) materials offer superior performance in high-power and high-temperature environments, making them ideal for electric vehicles, renewable energy systems, and 5G infrastructure. Testing these devices demands specialized equipment capable of handling higher voltages, currents, and temperatures, as well as unique measurement capabilities for their distinct material properties. Companies that can effectively address these niche but rapidly growing segments stand to gain a competitive edge and expand their market footprint significantly.

Furthermore, the ongoing digital transformation across industries, including automotive, industrial automation, and healthcare, creates sustained demand for customized and highly reliable semiconductor solutions. This trend drives the need for comprehensive and rigorous testing to ensure functional safety, cybersecurity, and long-term reliability. Opportunities also emerge from the increasing focus on sustainable manufacturing practices, prompting the development of energy-efficient test equipment and solutions that reduce power consumption during testing. The adoption of cloud-based test analytics and remote testing capabilities further extends market reach and operational efficiencies, particularly valuable in a globally distributed manufacturing ecosystem.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Packaging Test Solutions (Chiplets, SiP) | +1.0-1.5% | Global, strong in Asia Pacific and North America | Short to Medium-term (2025-2030) |

| Growth in Wide-Bandgap Semiconductor (SiC/GaN) Testing | +0.8-1.2% | Global, particularly Europe and Asia Pacific for EV and power electronics | Medium to Long-term (2026-2033) |

| Increasing Demand for In-Vehicle and Automotive Chip Testing | +0.7-1.0% | Europe, North America, Japan, China | Medium to Long-term (2026-2033) |

| Emergence of Quantum Computing and Neuromorphic Chip Testing | +0.5-0.8% | North America, Europe, select research hubs | Long-term (2030-2033) |

Testing Equipment for Semiconductor Market Challenges Impact Analysis

The Testing Equipment for Semiconductor Market faces several formidable challenges that require strategic responses from industry players. One significant hurdle is the rapid pace of technological obsolescence. As semiconductor designs evolve at an accelerated rate, existing test equipment can quickly become outdated, necessitating constant upgrades or complete replacements. This puts immense pressure on equipment manufacturers to innovate rapidly and on semiconductor companies to continuously invest in the latest test platforms, often before fully amortizing previous investments. Ensuring compatibility with future chip generations and developing modular, upgradable systems is critical to mitigating this challenge.

Another key challenge is the increasing complexity of test software and data management. Modern semiconductor testing generates enormous volumes of data, from parametric measurements to functional test results, across multiple test steps. Managing, analyzing, and deriving actionable insights from this data is complex and resource-intensive. Furthermore, the development of sophisticated test programs for highly integrated and specialized chips requires specialized programming skills and extensive validation, adding to development time and cost. The industry grapples with the need for robust data infrastructure and advanced analytical tools to harness this information effectively for yield improvement and quality control.

Finally, the shortage of skilled labor poses a considerable challenge. Designing, operating, and maintaining highly advanced semiconductor test equipment requires specialized expertise in electrical engineering, computer science, and materials science. The global talent pool for such specialized roles is limited, leading to intense competition for qualified professionals. This scarcity can impact the ability of companies to deploy new technologies efficiently, maintain equipment, and innovate. Training and retaining a skilled workforce, coupled with initiatives to promote STEM education, are crucial for overcoming this bottleneck and sustaining market growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence and Need for Constant Upgrades | -0.6-0.9% | Global | Long-term (2025-2033) |

| Increasing Complexity of Test Software and Data Management | -0.5-0.7% | Global | Medium to Long-term (2026-2033) |

| Shortage of Skilled Workforce and Specialized Engineers | -0.4-0.6% | Global, particularly North America and Europe | Long-term (2025-2033) |

Testing Equipment for Semiconductor Market - Updated Report Scope

This report provides a comprehensive analysis of the Testing Equipment for Semiconductor Market, encompassing detailed insights into market size, growth drivers, restraints, opportunities, and challenges. It covers the market landscape from historical trends to future projections, including in-depth segmentation and regional analyses. The scope focuses on various types of test equipment, their applications across different semiconductor manufacturing stages, and their end-use across diverse industries.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 7.8 Billion |

| Market Forecast in 2033 | USD 16.2 Billion |

| Growth Rate | 9.7% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Advantest Corporation, Teradyne Inc., Cohu Inc., National Instruments Corporation (NI), FormFactor Inc., Chroma ATE Inc., LTX-Credence (Xcerra Corporation), Tokyo Electron Limited (TEL), SPEA S.p.A., Acculogic Inc., Argonaut Manufacturing Services, Marvin Test Solutions Inc., Keysight Technologies Inc., Rohde & Schwarz GmbH & Co. KG, J.S.T. Mfg. Co., Ltd., Star Test Systems Inc., EXFO Inc., Micronics Japan Co., Ltd. (MJC), Technoprobe S.p.A., Wentworth Laboratories Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Testing Equipment for Semiconductor Market is extensively segmented to provide granular insights into its diverse components, reflecting the multifaceted nature of semiconductor manufacturing and testing processes. This segmentation allows for a detailed understanding of how different equipment types, applications, test methodologies, and end-use industries contribute to the overall market dynamics. By analyzing these segments, stakeholders can identify high-growth areas, assess competitive landscapes within specific niches, and tailor their strategies to capitalize on evolving market demands. The comprehensive breakdown highlights the specialized requirements that drive innovation across the entire value chain of semiconductor testing.

The primary segmentation categories include equipment type, which differentiates between Automated Test Equipment (ATE), Probers, and Handlers, recognizing their distinct roles in the test flow. ATE, for instance, is further broken down by the type of device it tests, such as logic, memory, mixed-signal, or RF components, reflecting the specialized nature of modern chip designs. The application segment delineates where the testing takes place—whether at Integrated Device Manufacturers (IDMs), Foundries, Outsourced Semiconductor Assembly and Test (OSAT) companies, or R&D facilities, each with unique operational needs and investment patterns. Understanding these application segments is crucial for equipment providers to target their solutions effectively.

Further segmentation by test type, such as wafer probing, package testing, burn-in testing, and system-level test (SLT), offers insights into the specific stages of chip validation and their corresponding equipment requirements. As chips become more complex, the importance of each test stage, especially early detection at wafer-level and comprehensive system-level validation, gains prominence. Finally, the end-use industry segmentation provides a view of demand drivers from various sectors, including consumer electronics, automotive, telecommunications, and industrial applications. This cross-industry perspective helps identify which economic sectors are generating the highest demand for new semiconductor devices and, consequently, advanced testing solutions, allowing for targeted market penetration strategies.

- By Type

- Automated Test Equipment (ATE)

- Probers

- Handlers

- By Application

- Foundry

- Integrated Device Manufacturer (IDM)

- Outsourced Semiconductor Assembly and Test (OSAT)

- Research & Development (R&D)

- By Test Type

- Wafer Probing

- Package Testing

- Burn-in Testing

- System-Level Test (SLT)

- By End-use Industry

- Consumer Electronics

- Automotive

- Telecommunications

- Industrial

- Healthcare

- Aerospace & Defense

- Data Centers

Regional Highlights

- Asia Pacific (APAC): Dominates the market due to its extensive semiconductor manufacturing ecosystem, including major foundries, IDMs, and OSATs in countries like Taiwan, South Korea, China, and Japan. The region accounts for the largest share of global semiconductor production and is projected to exhibit the highest growth rate, driven by continuous investments in new fab construction and capacity expansion, coupled with strong demand from consumer electronics and telecommunications sectors.

- North America: A significant market characterized by strong R&D activities, innovation in advanced chip designs (especially for AI, HPC, and specialized processors), and a robust presence of leading semiconductor companies and test equipment manufacturers. The region's focus on high-performance computing, automotive electronics, and defense applications drives demand for cutting-edge and highly sophisticated testing solutions.

- Europe: Exhibits steady growth, primarily fueled by the strong automotive electronics industry, industrial automation, and specialized semiconductor production (e.g., power semiconductors, sensors). European countries are investing in R&D and manufacturing capabilities to enhance regional self-sufficiency in semiconductor supply chains, leading to increased adoption of advanced testing equipment, particularly for functional safety and reliability.

- Latin America & Middle East and Africa (MEA): Represent emerging markets with nascent but growing semiconductor industries. While smaller in market share, these regions are witnessing gradual investments in electronics manufacturing and assembly, driven by local demand and government initiatives to diversify economies. This creates opportunities for basic and mid-range test equipment, with long-term potential for advanced solutions as industrialization progresses.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Testing Equipment for Semiconductor Market.- Advantest Corporation

- Teradyne Inc.

- Cohu Inc.

- National Instruments Corporation (NI)

- FormFactor Inc.

- Chroma ATE Inc.

- Tokyo Electron Limited (TEL)

- SPEA S.p.A.

- Acculogic Inc.

- Argonaut Manufacturing Services

- Marvin Test Solutions Inc.

- Keysight Technologies Inc.

- Rohde & Schwarz GmbH & Co. KG

- J.S.T. Mfg. Co., Ltd. (JST)

- Star Test Systems Inc.

- EXFO Inc.

- Micronics Japan Co., Ltd. (MJC)

- Technoprobe S.p.A.

- Wentworth Laboratories Ltd.

- ELES Semiconductor Equipment

Frequently Asked Questions

What is the current market size of the Testing Equipment for Semiconductor market?

The Testing Equipment for Semiconductor Market is estimated at USD 7.8 Billion in 2025 and is projected to grow to USD 16.2 Billion by 2033.

What are the key drivers for the growth of the Testing Equipment for Semiconductor market?

Key drivers include the increasing complexity and miniaturization of semiconductor devices, the proliferation of AI, 5G, and IoT technologies, and rising capital expenditure in new fabrication plants and OSAT facilities globally.

How is AI impacting the semiconductor testing equipment industry?

AI is significantly impacting the industry by enabling adaptive test methodologies for reduced test time, enhancing fault detection through advanced data analytics, and improving overall yield management and predictive maintenance for test equipment.

Which region holds the largest share in the Testing Equipment for Semiconductor market?

The Asia Pacific region currently holds the largest market share, driven by its extensive semiconductor manufacturing ecosystem, high capital investments, and significant production volumes in countries like Taiwan, South Korea, and China.

What are the main challenges faced by the Testing Equipment for Semiconductor market?

Major challenges include the rapid technological obsolescence of equipment necessitating constant upgrades, the increasing complexity of test software and data management, and the global shortage of skilled workforce and specialized engineers.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted