Residential Drinking Water Treatment Equipment Market

Residential Drinking Water Treatment Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705376 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

Residential Drinking Water Treatment Equipment Market Size

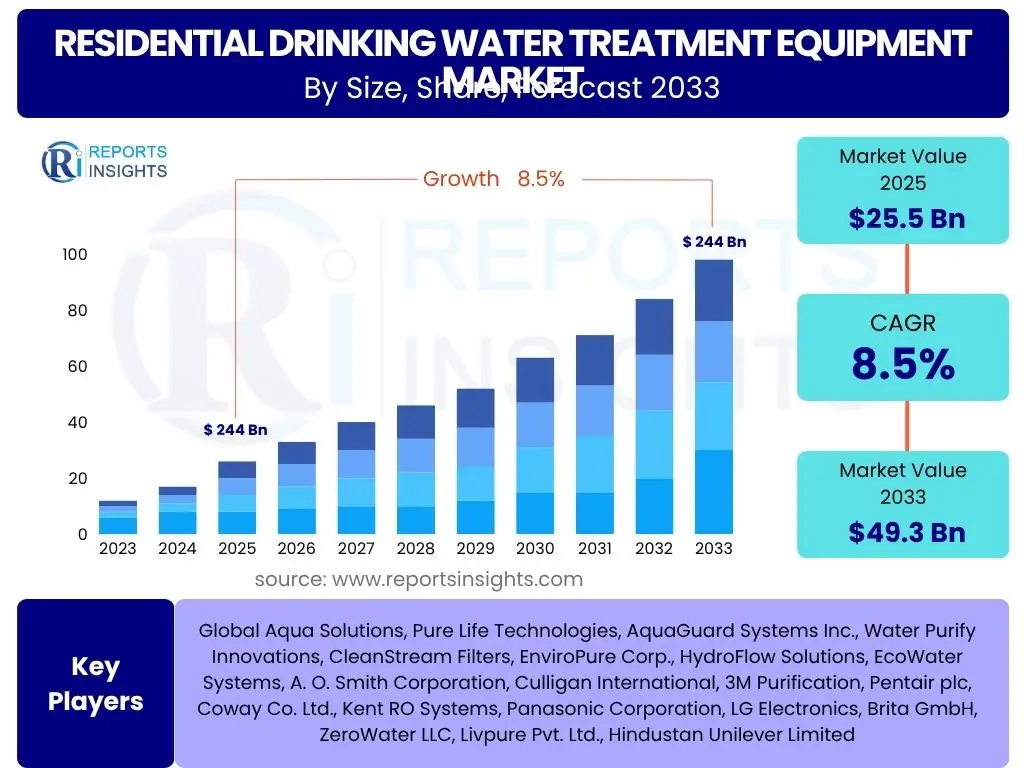

According to Reports Insights Consulting Pvt Ltd, The Residential Drinking Water Treatment Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 25.5 Billion in 2025 and is projected to reach USD 49.3 Billion by the end of the forecast period in 2033. This substantial growth is primarily driven by increasing consumer awareness regarding water quality, coupled with rising concerns over contaminants in municipal water supplies. The demand for advanced filtration technologies, alongside the burgeoning preference for healthier lifestyles, continues to fuel market expansion across various residential segments.

The market's expansion is further bolstered by technological advancements, leading to the development of more efficient, compact, and user-friendly water treatment solutions. Innovations such as smart water purifiers with IoT connectivity, real-time monitoring capabilities, and automated maintenance alerts are becoming increasingly popular. These advanced features not only enhance convenience but also provide greater assurance of water purity, appealing to a broader demographic of homeowners. Additionally, the urbanization trend and growth in residential construction across developing economies present significant opportunities for market players.

Key Residential Drinking Water Treatment Equipment Market Trends & Insights

The Residential Drinking Water Treatment Equipment market is witnessing several transformative trends driven by evolving consumer demands, technological innovation, and heightened environmental awareness. A prominent trend is the increasing adoption of point-of-use (POU) water treatment systems, such as under-sink and faucet-mounted filters, owing to their convenience, cost-effectiveness, and targeted contaminant removal. These systems address specific household needs, providing purified water directly at the tap for drinking and cooking, which aligns with consumer preferences for immediate and localized solutions.

Another significant trend is the integration of smart technologies and IoT capabilities into water treatment equipment. This allows for features like real-time water quality monitoring, filter replacement alerts, remote control via mobile applications, and predictive maintenance. Furthermore, there is a growing emphasis on sustainable and eco-friendly solutions, including systems that minimize water wastage during the purification process and utilize recyclable materials. The rising awareness about microplastics, pharmaceuticals, and emerging contaminants in water sources is also driving demand for advanced filtration technologies capable of removing these microscopic impurities, pushing manufacturers to innovate beyond traditional filtration methods.

- Increasing adoption of point-of-use (POU) water treatment systems for convenience and targeted purification.

- Integration of smart technologies, IoT connectivity, and AI-driven features for real-time monitoring and predictive maintenance.

- Growing consumer demand for eco-friendly and sustainable water treatment solutions that reduce water wastage and environmental footprint.

- Rising concerns over emerging contaminants, including microplastics, pharmaceuticals, and PFAS, driving innovation in advanced filtration technologies.

- Shift towards personalized water treatment solutions tailored to specific water quality issues and household needs.

- Expansion of subscription-based models for filter replacements and maintenance services, enhancing customer loyalty and recurring revenue streams.

- Miniaturization and aesthetic design improvements making water treatment systems more appealing for modern residential interiors.

AI Impact Analysis on Residential Drinking Water Treatment Equipment

Artificial Intelligence (AI) is poised to significantly revolutionize the residential drinking water treatment equipment market by enhancing operational efficiency, improving water quality management, and personalizing user experiences. Users frequently inquire about how AI can provide real-time water quality insights, automate system adjustments, and predict maintenance needs. AI algorithms can analyze vast datasets from sensors embedded in water treatment units, identifying patterns related to water usage, contaminant levels, and system performance. This predictive analytics capability allows for proactive maintenance, optimizing filter lifespan and ensuring consistent water purity, thereby minimizing downtime and reducing operational costs for consumers.

The application of AI extends to smart monitoring systems that can detect anomalies in water composition, such as sudden increases in chlorine or heavy metal levels, and automatically adjust filtration processes or alert homeowners. Furthermore, AI can personalize filtration settings based on local water quality reports, household consumption patterns, and individual preferences, providing truly tailored water treatment. Consumers are also interested in AI's potential for energy optimization within these systems, as intelligent algorithms can manage power consumption efficiently. The ability of AI to learn from user behavior and environmental factors promises a new generation of water treatment devices that are not only more effective but also more intuitive and resource-efficient.

- Real-time water quality monitoring: AI-powered sensors provide continuous data on water parameters, enabling immediate detection of contaminants and system irregularities.

- Predictive maintenance: AI algorithms analyze usage patterns and performance data to forecast filter replacement needs and potential equipment failures, prompting proactive servicing.

- Automated system optimization: AI can dynamically adjust filtration settings based on incoming water quality and household demand, ensuring optimal purification efficiency and reduced water wastage.

- Personalized water treatment profiles: AI learns user preferences and local water conditions to deliver customized water quality, addressing specific health concerns or taste preferences.

- Enhanced user interface and control: AI facilitates intuitive control through smart home integration and voice commands, improving the overall user experience.

- Energy efficiency: AI optimizes power consumption by managing system operations based on demand, leading to reduced electricity costs for homeowners.

- Fraud detection and authenticity verification: AI can help verify the authenticity of replacement filters and parts, combating the proliferation of counterfeit products.

Key Takeaways Residential Drinking Water Treatment Equipment Market Size & Forecast

The Residential Drinking Water Treatment Equipment market is set for robust growth, driven by escalating concerns over water safety and the increasing prevalence of waterborne diseases. Consumers are actively seeking reliable solutions to ensure access to clean drinking water, leading to a significant uptake of various treatment technologies. The market's upward trajectory is also supported by rising disposable incomes in emerging economies, allowing households to invest in more advanced and effective water purification systems. Technological innovations, particularly in membrane filtration and smart connectivity, are not only improving system performance but also making these devices more accessible and user-friendly, expanding the market's reach.

A crucial insight is the accelerating shift towards point-of-use and whole-house filtration systems, reflecting a broader trend of households taking greater control over their water quality. The integration of IoT and AI capabilities is transforming these devices from simple filters into intelligent home appliances that offer real-time monitoring, predictive maintenance, and personalized filtration. This evolution enhances consumer trust and drives repeat purchases. Furthermore, the market's resilience is demonstrated by its ability to adapt to new challenges, such as emerging contaminants and evolving regulatory landscapes, by continuously innovating and offering solutions that address these complex issues, solidifying its essential role in modern residential infrastructure.

- The residential water treatment equipment market is poised for significant growth, reaching nearly USD 50 Billion by 2033, driven by health consciousness and water quality concerns.

- Technological advancements, particularly in smart and IoT-enabled systems, are key enablers of market expansion and consumer adoption.

- Point-of-use and whole-house systems are gaining traction due to their convenience and comprehensive water treatment capabilities.

- Increasing disposable incomes in developing regions are fueling demand for advanced and premium water treatment solutions.

- Sustainability and energy efficiency are becoming critical factors influencing consumer purchasing decisions and product development.

- The market is adapting to emerging contaminants and evolving regulatory standards through continuous innovation in filtration technologies.

Residential Drinking Water Treatment Equipment Market Drivers Analysis

The growth of the Residential Drinking Water Treatment Equipment market is propelled by a confluence of critical factors, primarily centered around escalating concerns about water contamination and public health. Reports of deteriorating municipal water quality, often due to aging infrastructure, industrial pollutants, and agricultural runoff, have heightened consumer anxiety, prompting households to seek alternative purification methods. This heightened awareness about the presence of harmful substances like heavy metals, chemicals, bacteria, and viruses in tap water is a significant catalyst for demand.

Moreover, the rising incidence of waterborne diseases globally underscores the urgent need for effective water treatment solutions at the household level. Consumers are increasingly proactive in safeguarding their health, viewing water purification equipment as a necessary investment rather than a luxury. Urbanization trends, leading to increased pressure on existing water resources and infrastructure, further exacerbate water quality issues, especially in rapidly developing regions. This demographic shift, combined with improving economic conditions and rising disposable incomes in many parts of the world, empowers more households to afford and adopt sophisticated water treatment technologies, thereby driving market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Water Contamination & Quality Concerns | +1.8% | Global (esp. Asia Pacific, Latin America) | 2025-2033 (Long-term) |

| Rising Health Awareness & Incidence of Waterborne Diseases | +1.5% | Global (esp. North America, Europe) | 2025-2030 (Mid-term) |

| Rapid Urbanization & Infrastructure Deficiencies | +1.2% | Asia Pacific, Africa, Latin America | 2025-2033 (Long-term) |

| Technological Advancements in Filtration & Smart Systems | +1.0% | North America, Europe, Developed Asia Pacific | 2025-2033 (Long-term) |

| Growing Disposable Incomes & Improved Living Standards | +0.9% | Emerging Economies (China, India, Brazil) | 2025-2033 (Long-term) |

| Supportive Government Regulations & Standards | +0.7% | Europe, North America, Select Asian Countries | 2025-2028 (Short-term) |

| Marketing & Awareness Campaigns by Manufacturers | +0.6% | Global | 2025-2027 (Short-term) |

Residential Drinking Water Treatment Equipment Market Restraints Analysis

Despite robust growth drivers, the Residential Drinking Water Treatment Equipment market faces several significant restraints that could impede its full potential. One primary challenge is the high initial cost associated with advanced water treatment systems, particularly whole-house filtration and high-end reverse osmosis (RO) units. These significant upfront investments can be prohibitive for budget-conscious consumers, especially in price-sensitive markets or regions with lower disposable incomes. This cost barrier often pushes consumers towards less effective, cheaper alternatives or bottled water, limiting market penetration for sophisticated equipment.

Another restraint is the lack of widespread consumer awareness regarding the specific benefits and necessity of certain water treatment technologies, particularly in rural or underdeveloped areas. Many consumers may not fully understand the types of contaminants present in their water or the long-term health risks associated with untreated water, leading to complacency or a perception that existing municipal water is sufficiently safe. Furthermore, the recurring costs associated with filter replacements and system maintenance can deter potential buyers. The convenience and perceived purity of readily available bottled water also pose a competitive challenge, as some consumers prefer this option over investing in and maintaining a home filtration system.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment & Maintenance Costs | -1.5% | Global (esp. Developing Regions) | 2025-2033 (Long-term) |

| Lack of Awareness & Education in Certain Regions | -1.0% | Africa, Rural Asia Pacific, Latin America | 2025-2030 (Mid-term) |

| Perception of Bottled Water as a Viable Alternative | -0.8% | Global | 2025-2028 (Mid-term) |

| Complex Installation & Post-Sales Service Issues | -0.6% | Global | 2025-2027 (Short-term) |

| Counterfeit Products & Unregulated Market Players | -0.5% | Emerging Markets | 2025-2030 (Mid-term) |

Residential Drinking Water Treatment Equipment Market Opportunities Analysis

The Residential Drinking Water Treatment Equipment market is ripe with opportunities for growth and innovation, driven by evolving consumer needs and technological advancements. One significant opportunity lies in the untapped potential of emerging markets across Asia Pacific, Latin America, and Africa. These regions, characterized by rapid urbanization, increasing disposable incomes, and often compromised municipal water supplies, present a vast consumer base keen on investing in household water purification solutions. Manufacturers can tailor products to meet the specific economic and water quality challenges prevalent in these areas, offering more affordable yet effective systems.

Another key opportunity stems from the growing demand for smart and IoT-enabled water treatment solutions. As smart homes become more prevalent, integrating water purifiers with home automation systems, offering remote monitoring, predictive analytics, and automated maintenance reminders, provides a strong value proposition. There is also a burgeoning market for sustainable and eco-friendly products, including systems that minimize water wastage (e.g., zero-wastage RO systems) or utilize biodegradable filter materials. Furthermore, the expansion of direct-to-consumer sales channels and subscription-based service models for filter replacements and maintenance can enhance customer loyalty and generate recurring revenue, opening new business avenues for market players.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Markets (APAC, LATAM, MEA) | +2.0% | Asia Pacific, Latin America, Africa | 2025-2033 (Long-term) |

| Development of Smart & IoT-Enabled Water Purifiers | +1.5% | North America, Europe, Developed Asia Pacific | 2025-2033 (Long-term) |

| Focus on Sustainable & Eco-Friendly Solutions | +1.2% | Global (esp. Europe, North America) | 2025-2030 (Mid-term) |

| Growth of Subscription-Based Services & Direct Sales | +1.0% | Global | 2025-2028 (Mid-term) |

| Product Innovation for Specific Contaminants (e.g., PFAS) | +0.8% | North America, Europe | 2025-2030 (Mid-term) |

| Partnerships with Real Estate Developers & Builders | +0.7% | Global | 2025-2027 (Short-term) |

Residential Drinking Water Treatment Equipment Market Challenges Impact Analysis

The Residential Drinking Water Treatment Equipment market faces several inherent challenges that demand strategic navigation from industry players. A significant hurdle is the intense competition and market fragmentation, with numerous domestic and international manufacturers vying for market share. This fierce competition often leads to price wars, impacting profit margins and making it difficult for new entrants to establish a strong foothold. Furthermore, the proliferation of counterfeit products, particularly filters and replacement parts, poses a serious threat. These substandard imitations not only erode brand reputation and revenue but also compromise water quality and consumer safety, creating mistrust in the market.

Another challenge is the constant need for product innovation to address evolving water contaminants and consumer expectations. As new contaminants emerge and environmental regulations tighten, manufacturers must continually invest in research and development to update their technologies, which can be resource-intensive. The management of waste generated from used filters and membrane cartridges also presents an environmental and logistical challenge, requiring sustainable disposal or recycling solutions. Lastly, varying regulatory landscapes across different countries and regions necessitate product adaptations and compliance efforts, adding complexity and cost to market operations for global players.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition & Market Fragmentation | -1.2% | Global | 2025-2033 (Long-term) |

| Proliferation of Counterfeit Products | -1.0% | Emerging Markets (e.g., India, China) | 2025-2030 (Mid-term) |

| Disposal & Environmental Impact of Used Filters | -0.8% | Europe, North America | 2025-2033 (Long-term) |

| Rapid Technological Obsolescence & R&D Costs | -0.7% | Global | 2025-2028 (Mid-term) |

| Varying & Evolving Regulatory Landscape | -0.5% | Global | 2025-2027 (Short-term) |

| Supply Chain Disruptions & Raw Material Price Volatility | -0.4% | Global | 2025-2026 (Short-term) |

Residential Drinking Water Treatment Equipment Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Residential Drinking Water Treatment Equipment market, covering historical performance, current market dynamics, and future projections. The scope includes a detailed examination of market size, growth drivers, restraints, opportunities, and challenges. It further segments the market by various product types, technologies, applications, and distribution channels, offering a granular view of market trends and consumer preferences. The report also highlights key regional insights and profiles major market players, providing stakeholders with critical data for strategic decision-making and investment planning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 25.5 Billion |

| Market Forecast in 2033 | USD 49.3 Billion |

| Growth Rate | 8.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Aqua Solutions, Pure Life Technologies, AquaGuard Systems Inc., Water Purify Innovations, CleanStream Filters, EnviroPure Corp., HydroFlow Solutions, EcoWater Systems, A. O. Smith Corporation, Culligan International, 3M Purification, Pentair plc, Coway Co. Ltd., Kent RO Systems, Panasonic Corporation, LG Electronics, Brita GmbH, ZeroWater LLC, Livpure Pvt. Ltd., Hindustan Unilever Limited |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Residential Drinking Water Treatment Equipment market is extensively segmented to reflect the diverse needs and preferences of consumers, as well as the technological advancements within the industry. This segmentation provides a granular understanding of market dynamics, allowing for targeted strategies by manufacturers and distributors. Key segments include various product types, each designed to address specific water quality challenges, ranging from basic sediment removal to advanced chemical and microbial purification.

Further segmentation by technology highlights the dominant and emerging purification methods employed in residential settings, such as membrane filtration (RO, UF) and adsorption. The market is also analyzed based on application or end-use, distinguishing between systems primarily used for drinking water versus those for whole-house treatment. Lastly, distribution channels are critical for understanding how products reach consumers, encompassing both traditional retail and the rapidly growing e-commerce platforms, each with its unique advantages and consumer reach.

- By Product Type:

- Reverse Osmosis (RO) Systems: Highly effective for removing dissolved solids, salts, and various contaminants.

- Ultrafiltration (UF) Systems: Utilizes a membrane to remove suspended solids, bacteria, and viruses without removing beneficial minerals.

- Water Softeners: Designed to remove hardness-causing minerals like calcium and magnesium, preventing scale buildup.

- Distillation Systems: Boil water and condense the steam, effectively removing most inorganic minerals, metals, and some organic compounds.

- UV Filters: Use ultraviolet light to disinfect water by deactivating bacteria, viruses, and other microorganisms.

- Sediment Filters: Remove larger particles such as dirt, rust, and sand, often used as pre-filters.

- Activated Carbon Filters: Absorb chlorine, odors, tastes, and various organic chemicals.

- Faucet-Mounted Filters: Simple, cost-effective filters directly attached to the faucet for point-of-use purification.

- Countertop Filters: Portable units that sit on the counter and connect to the faucet or have their own reservoir.

- Under-Sink Filters: Installed beneath the sink, providing filtered water through a dedicated faucet.

- Whole-House Filters: Treat all water entering the home, protecting plumbing and appliances and providing filtered water at every tap.

- Shower Filters: Reduce chlorine and other contaminants in shower water, benefiting skin and hair health.

- Pitcher Filters: Manual, portable filters for small volumes of drinking water.

- Gravity-Fed Filters: Simple systems relying on gravity for filtration, often used for emergencies or off-grid living.

- Specialty Filters: Targeted solutions for specific contaminants like lead, fluoride, or specific heavy metals.

- By Technology:

- Membrane Filtration: Includes RO, UF, Nanofiltration (NF), and Microfiltration (MF) processes.

- Adsorption: Primarily uses activated carbon to bind contaminants to its surface.

- Ion Exchange: Utilized in water softeners to exchange hardness ions with sodium or potassium ions.

- Disinfection: Involves UV light, ozone, or chemical treatments to kill microorganisms.

- Sedimentation: Physical process where heavier particles settle out of water.

- Coagulation/Flocculation: Chemical processes used to clump small particles together for easier removal.

- By Application/End-Use:

- Kitchen/Drinking Water: Systems primarily installed for potable water use.

- Bathroom/Showering Water: Filters focused on improving water quality for personal hygiene.

- Whole Home Water: Comprehensive systems treating all incoming water for various household uses.

- By Distribution Channel:

- Online Retail (E-commerce): Growing channel offering convenience and wider product selection.

- Offline Retail:

- Specialty Stores: Focused on water treatment products, offering expert advice and installation.

- Supermarkets/Hypermarkets: Provide easy access to basic filtration products.

- Hardware Stores: Offer a range of DIY installation-friendly systems.

- Direct Sales: Manufacturers selling directly to consumers, often with installation and service packages.

Regional Highlights

- North America: The North American market holds a significant share, driven by high consumer awareness regarding water quality, stringent regulatory standards, and a strong emphasis on health and wellness. Aging water infrastructure in many parts of the U.S. and Canada, leading to concerns about lead and other contaminants, fuels demand for robust residential treatment solutions. The region is also a hub for technological innovation, with high adoption rates for smart and IoT-enabled water purifiers. Consumers in North America are increasingly investing in whole-house filtration systems and advanced point-of-use technologies, reflecting a proactive approach to household water safety. The presence of major market players and a well-established distribution network further contribute to market maturity and growth.

- Europe: Europe represents a mature but steadily growing market for residential drinking water treatment equipment. While municipal water quality is generally high in many European countries, concerns about specific contaminants, hard water issues, and the desire for enhanced taste drive demand. Countries like Germany, France, and the UK exhibit strong demand for water softeners and point-of-use filters. The region also shows a growing inclination towards sustainable and energy-efficient water treatment solutions, aligning with broader European environmental policies. Innovation in compact design and smart features is also a notable trend, catering to the diverse housing structures and consumer preferences across the continent.

- Asia Pacific (APAC): The Asia Pacific region is projected to be the fastest-growing market, primarily due to rapid urbanization, increasing industrialization, and a vast population facing severe water scarcity and pollution challenges. Countries like China and India are at the forefront of this growth, driven by deteriorating municipal water quality, rising disposable incomes, and a heightened awareness of waterborne diseases. The market here is characterized by a high demand for RO and UF systems capable of handling diverse and complex contaminants. Government initiatives to improve water access and quality, coupled with aggressive marketing by both local and international players, are further accelerating market penetration. The diversity of regional water sources and contamination profiles necessitates a wide array of specialized treatment solutions.

- Latin America: The Latin American market for residential drinking water treatment equipment is experiencing steady growth, propelled by concerns over public health, inconsistent municipal water quality, and a rising middle class. Countries such as Brazil, Mexico, and Argentina are key contributors to this growth, where consumers are increasingly opting for in-home water purification to ensure safety. Economic development and urbanization contribute to both the challenges in water infrastructure and the increased affordability of treatment solutions. The market is also seeing a shift towards more advanced filtration technologies as awareness about specific contaminants grows, moving beyond basic boiling or bottled water consumption.

- Middle East and Africa (MEA): The MEA region presents significant growth opportunities, particularly in countries facing extreme water scarcity and high levels of water stress. The reliance on desalination in some areas and the challenges of providing safe drinking water in others drive the adoption of residential treatment equipment. Rising health consciousness, coupled with increasing disposable incomes in oil-rich nations, contributes to the demand for advanced and reliable water purification systems. Infrastructure development and government initiatives aimed at improving living standards are also fostering market growth, though market penetration remains lower compared to developed regions, indicating substantial untapped potential for future expansion.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Residential Drinking Water Treatment Equipment Market.- Global Aqua Solutions

- Pure Life Technologies

- AquaGuard Systems Inc.

- Water Purify Innovations

- CleanStream Filters

- EnviroPure Corp.

- HydroFlow Solutions

- EcoWater Systems

- A. O. Smith Corporation

- Culligan International

- 3M Purification

- Pentair plc

- Coway Co. Ltd.

- Kent RO Systems

- Panasonic Corporation

- LG Electronics

- Brita GmbH

- ZeroWater LLC

- Livpure Pvt. Ltd.

- Hindustan Unilever Limited

Frequently Asked Questions

What are the primary drivers of growth in the Residential Drinking Water Treatment Equipment Market?

The primary drivers include increasing concerns over water contamination and health risks, rising incidences of waterborne diseases, deteriorating municipal water infrastructure, rapid urbanization, and growing disposable incomes. Additionally, continuous technological advancements in filtration and smart systems significantly contribute to market expansion by offering more effective and convenient solutions.

What are the key types of residential water treatment equipment available?

Key types of residential water treatment equipment include Reverse Osmosis (RO) systems, Ultrafiltration (UF) systems, water softeners, UV filters, sediment filters, and activated carbon filters. These are often categorized by installation type, such as point-of-use systems (faucet-mounted, under-sink, pitcher filters) and whole-house filtration systems, each addressing specific water quality needs.

How is AI influencing the Residential Drinking Water Treatment Equipment Market?

AI is influencing the market by enabling real-time water quality monitoring, predictive maintenance for filter replacement, automated system optimization, and personalized water treatment profiles. AI-powered systems enhance efficiency, reduce operational costs, and provide a more intelligent and user-friendly experience through smart home integration and remote control capabilities.

What are the main challenges faced by the Residential Drinking Water Treatment Equipment Market?

The main challenges include the high initial investment and maintenance costs for advanced systems, a lack of widespread consumer awareness in certain regions, intense market competition, and the proliferation of counterfeit products. Additionally, managing the environmental impact of used filters and adapting to rapid technological obsolescence pose ongoing challenges for manufacturers.

Which regions offer the most significant growth opportunities for residential water treatment equipment?

The Asia Pacific region, particularly countries like China and India, offers the most significant growth opportunities due to rapid urbanization, increasing water pollution, and rising disposable incomes. Latin America and parts of the Middle East and Africa also present substantial potential owing to improving economic conditions and growing awareness of water safety, driving demand for innovative and accessible solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted